Download as docx, pdf, or txt

You might also like

- IMS Proschool CFP EbookDocument140 pagesIMS Proschool CFP EbookNielesh AmbreNo ratings yet

- The 6 Steps of Financial PlanningDocument4 pagesThe 6 Steps of Financial PlanningCT SunilkumarNo ratings yet

- MERS Bankruptcy and IdahoDocument17 pagesMERS Bankruptcy and IdahoForeclosure Fraud100% (1)

- What Is Financial Planning?: Life GoalsDocument16 pagesWhat Is Financial Planning?: Life GoalsrahsatputeNo ratings yet

- Ifp 1 Introduction To Financial Planning PDFDocument5 pagesIfp 1 Introduction To Financial Planning PDFIMS ProschoolNo ratings yet

- Ifp 1 Introduction To Financial PlanningDocument5 pagesIfp 1 Introduction To Financial PlanningSukumarNo ratings yet

- Wealth Management in Delhi and NCR Research Report On Scope of Wealth Management in Delhi and NCR 95pDocument98 pagesWealth Management in Delhi and NCR Research Report On Scope of Wealth Management in Delhi and NCR 95pSajal AroraNo ratings yet

- Weekly Report 1Document10 pagesWeekly Report 1NidhiKachhawaNo ratings yet

- Black Book ProjectDocument69 pagesBlack Book Projectganeshsable247No ratings yet

- Financial Planning Made Easy: A Beginner's Handbook to Financial SecurityFrom EverandFinancial Planning Made Easy: A Beginner's Handbook to Financial SecurityNo ratings yet

- LESSON 20: What Is Personal Finance? TargetDocument8 pagesLESSON 20: What Is Personal Finance? TargetMai RuizNo ratings yet

- Fin Planning Goes Beyond Saving Taxes: Monitor Your Budget To Keep Tabs On InflowsDocument1 pageFin Planning Goes Beyond Saving Taxes: Monitor Your Budget To Keep Tabs On InflowsaravindascribdNo ratings yet

- Chapter 1Document22 pagesChapter 1Trushant MandharkarNo ratings yet

- FINAL MahantheshDocument138 pagesFINAL MahantheshKapil DevNo ratings yet

- For Chapter 1Document36 pagesFor Chapter 1Giella MagnayeNo ratings yet

- For A Rich Future: Owning A Car, A HouseDocument11 pagesFor A Rich Future: Owning A Car, A Housedbsmba2015No ratings yet

- RM - J229 - Research PaperDocument10 pagesRM - J229 - Research PaperRishikaNo ratings yet

- Chapter 6Document7 pagesChapter 6Erika GueseNo ratings yet

- 6 Financial LiteracyDocument7 pages6 Financial LiteracyELDREI VICEDONo ratings yet

- Research Report Financial PlanningDocument43 pagesResearch Report Financial PlanningManasi KalgutkarNo ratings yet

- Financial AdvisorsDocument100 pagesFinancial AdvisorsNipul BafnaNo ratings yet

- Financial PlanningDocument47 pagesFinancial PlanningNishaTambeNo ratings yet

- FT 405 FMAJ Investment Advisor - NotesDocument43 pagesFT 405 FMAJ Investment Advisor - NotesanjaliNo ratings yet

- CFP EbookDocument81 pagesCFP EbookNikhil parabNo ratings yet

- Financial Planning and Tax ManagementDocument11 pagesFinancial Planning and Tax Managementrohit maddeshiyaNo ratings yet

- PFM Blackbook 19022014Document57 pagesPFM Blackbook 19022014dp100% (1)

- 7 Steps To Financial LiteracyDocument16 pages7 Steps To Financial Literacyjoshua mugwisiNo ratings yet

- Chapter 1: Introduction To Financial PlanningDocument71 pagesChapter 1: Introduction To Financial PlanningSarojkumar ChhuraNo ratings yet

- Financial Planning GodrejDocument199 pagesFinancial Planning GodrejriteshnaikNo ratings yet

- Introduction To Personal Finance.Document26 pagesIntroduction To Personal Finance.djdannex791No ratings yet

- Financial PlanningDocument6 pagesFinancial PlanningSheikh NadeemNo ratings yet

- THE FINANCIAL BLUEPRINT: MASTERING PERSONAL FINANCES FOR A PROSPEROUS FUTUREFrom EverandTHE FINANCIAL BLUEPRINT: MASTERING PERSONAL FINANCES FOR A PROSPEROUS FUTURENo ratings yet

- Digital Assignment - 1: Submitted To: Submitted byDocument7 pagesDigital Assignment - 1: Submitted To: Submitted byMonashreeNo ratings yet

- Bba V PFP Unit 1Document15 pagesBba V PFP Unit 1RaghuNo ratings yet

- Standard of Living: Explain The Benefits of Financial Education?Document9 pagesStandard of Living: Explain The Benefits of Financial Education?NoreenNo ratings yet

- Black Book (Pradnya More)Document74 pagesBlack Book (Pradnya More)ahmedsirajkhan147No ratings yet

- Financial LiteracyDocument5 pagesFinancial LiteracysandeepchauhansatechnologiesNo ratings yet

- Personal Finance - PDF RoomDocument144 pagesPersonal Finance - PDF RoomEllie HoangNo ratings yet

- Unit 1 Financial Planning and Tax ManagementDocument18 pagesUnit 1 Financial Planning and Tax ManagementnoroNo ratings yet

- Personal FDXFFinancial PlanningDocument34 pagesPersonal FDXFFinancial Planningmanali.270694No ratings yet

- Module 1 Introd. To PFDocument35 pagesModule 1 Introd. To PFPrisha SinghaniaNo ratings yet

- UntitledDocument27 pagesUntitledSeryl AñonuevoNo ratings yet

- Financial AccountingDocument221 pagesFinancial AccountingAditya AgnihotriNo ratings yet

- Personal Financial ManagementDocument4 pagesPersonal Financial ManagementhelenNo ratings yet

- What You Should Know About Financial PlanningDocument16 pagesWhat You Should Know About Financial PlanningrvarathanNo ratings yet

- KMBN FM02 Financial Planning and Tax ManagementDocument25 pagesKMBN FM02 Financial Planning and Tax ManagementShubham SinghNo ratings yet

- Handout in Unit 4D and 4EDocument10 pagesHandout in Unit 4D and 4EArgie Cayabyab CagunotNo ratings yet

- Financial Literacy ReportDocument12 pagesFinancial Literacy Reportrafaelmariahanne2029No ratings yet

- Home Financial Consumers Learn Financial Planning BasicsDocument4 pagesHome Financial Consumers Learn Financial Planning BasicsVJ BrajdarNo ratings yet

- Financial Behavior Modification Starter Guide: A Simple Guide to Managing Your FinancesFrom EverandFinancial Behavior Modification Starter Guide: A Simple Guide to Managing Your FinancesRating: 3 out of 5 stars3/5 (1)

- Retirement Planning GuideDocument26 pagesRetirement Planning GuideKalaivani ArunachalamNo ratings yet

- Financial Advisor PRINTDocument6 pagesFinancial Advisor PRINTNMRaycNo ratings yet

- Financial Planning ProcessDocument3 pagesFinancial Planning ProcessAtiya IftikharNo ratings yet

- How To Do Financial PlanningDocument25 pagesHow To Do Financial PlanningAlFakir Fikri AlTakiriNo ratings yet

- Financial PlanDocument222 pagesFinancial PlanADITYA BADHENo ratings yet

- Money Mastery 101: A Guide to Personal Finance: Road To Success, #1From EverandMoney Mastery 101: A Guide to Personal Finance: Road To Success, #1No ratings yet

- The HPAX Wealth Blueprint: Your Ultimate Guide to Financial Freedom: various topics related to personal finance and wealth generationFrom EverandThe HPAX Wealth Blueprint: Your Ultimate Guide to Financial Freedom: various topics related to personal finance and wealth generationNo ratings yet

- Cash Advance Form - NewDocument1 pageCash Advance Form - NewBENAZIR BORRERONo ratings yet

- Salary Slip (00856333 March, 2019)Document1 pageSalary Slip (00856333 March, 2019)AurangzebNo ratings yet

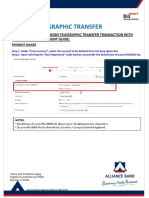

- How To Perform Foreign Telegraphic TransferDocument33 pagesHow To Perform Foreign Telegraphic TransferBerney RyxlerNo ratings yet

- TVS Balance SheetDocument6 pagesTVS Balance SheetNihal LamgeNo ratings yet

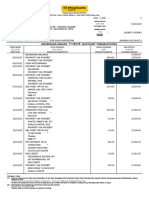

- Account Statement For Account Number2416000101054929: Branch DetailsDocument29 pagesAccount Statement For Account Number2416000101054929: Branch DetailsRajkumarsinghNo ratings yet

- T3TFT - Funds Transfer - R12.01Document245 pagesT3TFT - Funds Transfer - R12.01Mohammad NaeemNo ratings yet

- Projected Profit Rates Feb 2023Document14 pagesProjected Profit Rates Feb 2023adeelNo ratings yet

- Afar 04Document3 pagesAfar 04yvonneNo ratings yet

- Life Insurance Products in NepalDocument13 pagesLife Insurance Products in NepalSachin PangeniNo ratings yet

- Lesson 29 - General AnnuitiesDocument67 pagesLesson 29 - General AnnuitiesAlfredo LabadorNo ratings yet

- Surecut ShearsDocument1 pageSurecut ShearsMilan BarcaNo ratings yet

- MR - Venkatramanan Narayanasamy: Mobile BankingDocument2 pagesMR - Venkatramanan Narayanasamy: Mobile BankingAathu HappyNo ratings yet

- Tentative ChapterisationDocument13 pagesTentative ChapterisationNikhil kumarNo ratings yet

- Sdoc 05 30 SiDocument18 pagesSdoc 05 30 Sijabulile.mhlengiNo ratings yet

- Why Gratuity Trust Fund Approval Is RequiredDocument1 pageWhy Gratuity Trust Fund Approval Is RequiredTikaram ChaudharyNo ratings yet

- 20 Solved Exercises On Accounting EntriesDocument5 pages20 Solved Exercises On Accounting EntriesScribdTranslationsNo ratings yet

- Retail Banking and Wealth ManagementDocument36 pagesRetail Banking and Wealth Managementamanjotkaur10sainiNo ratings yet

- Abanes The Factors Affecting The Budgeting Skills and Spending Behavior Among Senior High School Students of Thy Covenant Montessori School in S.Y. 2019 2020Document27 pagesAbanes The Factors Affecting The Budgeting Skills and Spending Behavior Among Senior High School Students of Thy Covenant Montessori School in S.Y. 2019 2020Bjarne Lex Francis AgbonNo ratings yet

- 31692the Basic Principles of Guaranteed Payday LoansDocument2 pages31692the Basic Principles of Guaranteed Payday Loanskordan3gzcNo ratings yet

- Pay Slip For The Month of July-2023: Bandhan Bank LimitedDocument1 pagePay Slip For The Month of July-2023: Bandhan Bank LimitedBIKRAM KUMAR BEHERA0% (1)

- SimpleInterest Compound InterestDocument44 pagesSimpleInterest Compound InterestAnk KoliNo ratings yet

- Law On P, M, A ActivityDocument2 pagesLaw On P, M, A ActivityLFGS Finals100% (2)

- Ibs Equine Park 1 31/10/23Document6 pagesIbs Equine Park 1 31/10/23alvinlun.cbsmyNo ratings yet

- Unit 5 MFRBDocument21 pagesUnit 5 MFRBSweety TuladharNo ratings yet

- NPCI ResearchDocument4 pagesNPCI ResearchUtkarsh TyagiNo ratings yet

- OpTransactionHistoryUX510 06 2023Document5 pagesOpTransactionHistoryUX510 06 2023srm finservNo ratings yet

- Payslip Nov2021Document1 pagePayslip Nov2021SiddharthNo ratings yet

- Lat Soal Time Value of MoneyDocument3 pagesLat Soal Time Value of MoneyHendra G. AngjayaNo ratings yet

- Simple and Compound Interest - SSC - CDSDocument14 pagesSimple and Compound Interest - SSC - CDSphysicspalanichamyNo ratings yet