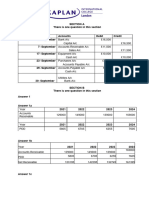

Partnership Dis.03.14.2024

Partnership Dis.03.14.2024

You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Accounting Policy Memo - Cash Equivalents & ST InvestmentsDocument2 pagesAccounting Policy Memo - Cash Equivalents & ST Investmentsdalebowen100% (1)

- Application 1 (Basic Steps in Accounting)Document2 pagesApplication 1 (Basic Steps in Accounting)Maria Nezka Advincula86% (7)

- Online Food Delivery ServiceDocument20 pagesOnline Food Delivery ServicevyapakNo ratings yet

- Chapter 6 PPT (AIS - James Hall)Document9 pagesChapter 6 PPT (AIS - James Hall)Nur-aima MortabaNo ratings yet

- Partnership DissolutionDocument46 pagesPartnership Dissolutionxenovia chuchuNo ratings yet

- Accounting For Partnership DissolutionDocument51 pagesAccounting For Partnership DissolutionRica Ella RestauroNo ratings yet

- Accounting For Partnership DissolutionDocument49 pagesAccounting For Partnership DissolutionTULIO, Jeremy I.No ratings yet

- M5a Liquidation P1 SBDocument10 pagesM5a Liquidation P1 SBKenzel lawasNo ratings yet

- AC - IntAcctg-A LSLiquidation.Document41 pagesAC - IntAcctg-A LSLiquidation.Janesene SolNo ratings yet

- MODULE 5-Part 1Document5 pagesMODULE 5-Part 1trixie maeNo ratings yet

- MODULE 5-Part 1Document5 pagesMODULE 5-Part 1Mary Joy CabilNo ratings yet

- M5c Liquidation P3 SBDocument5 pagesM5c Liquidation P3 SBKenzel lawasNo ratings yet

- 1stLecture-Partnership LiquidationDocument25 pages1stLecture-Partnership LiquidationRechelle Dalusung100% (1)

- Module 5 Accounting 2 Partnership Liquidation by InstallmentDocument9 pagesModule 5 Accounting 2 Partnership Liquidation by InstallmentJemima TapioNo ratings yet

- ACW1100 Tutorial Week2Document12 pagesACW1100 Tutorial Week2林志成No ratings yet

- Classroom Exerisises On Presentation of Financial Statements PDFDocument2 pagesClassroom Exerisises On Presentation of Financial Statements PDFalyssaNo ratings yet

- Solution in Partnership Liquidation InstallmentDocument20 pagesSolution in Partnership Liquidation InstallmentNikki GarciaNo ratings yet

- Marbella - Accounting For Special TransactionsDocument4 pagesMarbella - Accounting For Special TransactionsMelch Yvan Racasa MarbellaNo ratings yet

- Chapter Five PrintDocument18 pagesChapter Five PrintGedionNo ratings yet

- Joint Arrangement Answer KeyDocument8 pagesJoint Arrangement Answer KeyMonica DespiNo ratings yet

- Total Assets 335,000 80,000: Additional InformationDocument8 pagesTotal Assets 335,000 80,000: Additional InformationHohohoNo ratings yet

- #Chapter 4 Asignación (Recovered)Document22 pages#Chapter 4 Asignación (Recovered)adrianasofiagomez14No ratings yet

- M5b Liquidation P2 SBDocument6 pagesM5b Liquidation P2 SBKenzel lawasNo ratings yet

- SEM III - Advanced Accounting (EM)Document4 pagesSEM III - Advanced Accounting (EM)Abdul MalikNo ratings yet

- PRACTICE EXAM AnswersDocument7 pagesPRACTICE EXAM Answersarhamjain269No ratings yet

- Asm ACCOUNTINGDocument16 pagesAsm ACCOUNTINGVũ Khánh HuyềnNo ratings yet

- May 2017 Advanced Financial Accounting & Reporting Final Pre-BoardDocument20 pagesMay 2017 Advanced Financial Accounting & Reporting Final Pre-BoardPatrick ArazoNo ratings yet

- Hedge Fund Reports and Financial StatementDocument96 pagesHedge Fund Reports and Financial StatementOlivier MNo ratings yet

- PartnershipDocument10 pagesPartnershipShaz NagaNo ratings yet

- Accounting For Special Transactions - Module 4Document9 pagesAccounting For Special Transactions - Module 4Jcel JcelNo ratings yet

- DIY LiquidationDocument27 pagesDIY LiquidationJOYCE C ANDADORNo ratings yet

- Accounting 10 ColumnsDocument2 pagesAccounting 10 ColumnsTRIXIEJOY INIONNo ratings yet

- Buscom ReportDocument2 pagesBuscom ReportJashly FuentesNo ratings yet

- Examination Question and Answers, Set F (Problem Solving), Chapter 15 - Statement of Cash FlowDocument3 pagesExamination Question and Answers, Set F (Problem Solving), Chapter 15 - Statement of Cash Flowjohn carlos doringoNo ratings yet

- Partnership 2021 - Long ProblemsDocument5 pagesPartnership 2021 - Long ProblemsMichael MagdaogNo ratings yet

- Paper 8 FM ECODocument361 pagesPaper 8 FM ECOmhdsameem123No ratings yet

- Partnership LiquidationDocument28 pagesPartnership LiquidationDela cruz, Hainrich (Hain)No ratings yet

- Pa Revision For FinalsDocument9 pagesPa Revision For FinalsKhải Hưng NguyễnNo ratings yet

- Fabm2 2nd PrelimDocument2 pagesFabm2 2nd PrelimAngelica NacisNo ratings yet

- Module-2 Equity Valuation Numerical For StudentsDocument11 pagesModule-2 Equity Valuation Numerical For Studentsgaurav supadeNo ratings yet

- 07 Activity AtanezDocument2 pages07 Activity AtanezSteff Atañez100% (1)

- Final Activity 3 QuestionDocument2 pagesFinal Activity 3 QuestionSze ChristienyNo ratings yet

- Chapter 2 - Partnership Formation ObjectivesDocument10 pagesChapter 2 - Partnership Formation ObjectivesSapphire AliasNo ratings yet

- Partnership Liquidation Answer KeyDocument16 pagesPartnership Liquidation Answer KeyJerickho JNo ratings yet

- Micolob - Tla 2 - Answers SheetDocument18 pagesMicolob - Tla 2 - Answers SheetHaries MicolobNo ratings yet

- Partnership Accounting: FormationDocument6 pagesPartnership Accounting: FormationLee SuarezNo ratings yet

- Long QuizDocument5 pagesLong QuizMitch Tokong MinglanaNo ratings yet

- Mba ZC415 Ec-3r First Sem 2022-2023Document4 pagesMba ZC415 Ec-3r First Sem 2022-2023Ravi KaviNo ratings yet

- Introduction To Group Statements - FASSET Class - 15 May 2021Document22 pagesIntroduction To Group Statements - FASSET Class - 15 May 2021Mike NdunaNo ratings yet

- HandOut No 2 Busfin Financial StatementsDocument5 pagesHandOut No 2 Busfin Financial Statementsnatalie clyde matesNo ratings yet

- Problem 2 - AccountingcyleDocument13 pagesProblem 2 - AccountingcyleGio BurburanNo ratings yet

- Illustration KK Co. Perpetual ClosingDocument9 pagesIllustration KK Co. Perpetual ClosingNAOL BIFTUNo ratings yet

- Partnership LiquidationDocument6 pagesPartnership LiquidationMonica MangobaNo ratings yet

- Ac 1104 - Partnership LiquidationDocument46 pagesAc 1104 - Partnership LiquidationNarikoNo ratings yet

- FA2 Chapter 4-Partnership-LiquidationDocument20 pagesFA2 Chapter 4-Partnership-LiquidationAyren Dela CruzNo ratings yet

- Business Combi PrelimDocument4 pagesBusiness Combi PrelimmcespressoblendNo ratings yet

- Poa 2012 Jan p.2.q.1 1Document4 pagesPoa 2012 Jan p.2.q.1 1RealGenius (Carl)No ratings yet

- Ast Discussion 4 - Partnership Liquidation For PrintDocument4 pagesAst Discussion 4 - Partnership Liquidation For PrintCHRISTINE TABULOGNo ratings yet

- Module 2Document6 pagesModule 2trixie mae0% (1)

- Module 2Document6 pagesModule 2Mary Joy CabilNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- Experimental Marketing in Indian Hotels PDFDocument11 pagesExperimental Marketing in Indian Hotels PDFAli ShalabyNo ratings yet

- Ib Chapter 7Document31 pagesIb Chapter 7K60 Nguyễn Thị Thanh HàNo ratings yet

- EEA Life Pricing 20160701Document1 pageEEA Life Pricing 20160701Southey CapitalNo ratings yet

- Management Advisory Services - PreboardDocument13 pagesManagement Advisory Services - PreboardAngelica Estrada100% (4)

- Saint Louis College-Cebu: (Servant Leaders For Mission)Document4 pagesSaint Louis College-Cebu: (Servant Leaders For Mission)Marc Graham NacuaNo ratings yet

- Rural Marketing MixDocument2 pagesRural Marketing MixKhushi SiviaNo ratings yet

- VMG Myanmar Company ProfileDocument10 pagesVMG Myanmar Company Profilehtetarkar022023No ratings yet

- Sap Customer Relationship ManagementDocument27 pagesSap Customer Relationship ManagementkulkarnihNo ratings yet

- Bridge Course For AccountingDocument4 pagesBridge Course For Accountingaysha banuNo ratings yet

- A STRATEGY FOR E-TYPE Final Project PART 2 PDFDocument2 pagesA STRATEGY FOR E-TYPE Final Project PART 2 PDFLuis Felipe Arenas100% (1)

- كتاب التسويق الاستراتيجيsDocument388 pagesكتاب التسويق الاستراتيجيsMaria SayedNo ratings yet

- The Promise and Peril of Real OptionsDocument17 pagesThe Promise and Peril of Real OptionsAmit Kumar JainNo ratings yet

- NX9523 - Biz Professional Practise Coursework (w21068666) - 05112022Document12 pagesNX9523 - Biz Professional Practise Coursework (w21068666) - 05112022Jorris NgNo ratings yet

- External Audit ThesisDocument8 pagesExternal Audit ThesisLisa Riley100% (2)

- Celebrity EndorsementDocument8 pagesCelebrity EndorsementMuhammad ZubairNo ratings yet

- 2021 HCI BT Essay Question 2Document5 pages2021 HCI BT Essay Question 2CHUA MING XIU HCINo ratings yet

- Ast MidtermDocument4 pagesAst MidtermCathleen Drew TuazonNo ratings yet

- Jonathan Herjanto - 2301890434 Devin Verdian - 2301888846 Ashraf Budi Rifdiansyah - 2301919284 Jericko Panlen Liem - 2301883593Document25 pagesJonathan Herjanto - 2301890434 Devin Verdian - 2301888846 Ashraf Budi Rifdiansyah - 2301919284 Jericko Panlen Liem - 2301883593Johan FNo ratings yet

- Accounting Concept (Or Convention) Involved in Preparing A Provision For Doubtful Debts Account.Document2 pagesAccounting Concept (Or Convention) Involved in Preparing A Provision For Doubtful Debts Account.sharvin_94100% (3)

- Milestone 2 Java Done Vol 2Document21 pagesMilestone 2 Java Done Vol 2Erial dearv EscatinNo ratings yet

- 12th Commerce - Public Exam - Key Answer March - 2022-23 (EM)Document11 pages12th Commerce - Public Exam - Key Answer March - 2022-23 (EM)baharipriyan788No ratings yet

- Primary Vs Secondary DemandDocument4 pagesPrimary Vs Secondary DemandVivek MadupuNo ratings yet

- What Is The Difference Between Bussiness Plan and Project ProposalDocument6 pagesWhat Is The Difference Between Bussiness Plan and Project ProposalshumetNo ratings yet

- Ever Bilena Cosmetic Direct Sales Case Study by Rivera and Chua PDFDocument15 pagesEver Bilena Cosmetic Direct Sales Case Study by Rivera and Chua PDFPrecious Mole Tipas ES AnnexNo ratings yet

- Jawaban Inter 1 Modul 9Document4 pagesJawaban Inter 1 Modul 9Sebastian T.MNo ratings yet

- SIP VIP PPT 14-15 SalesDocument19 pagesSIP VIP PPT 14-15 SalesAshutoshNo ratings yet

- Ratio Analysis Of: Bata Shoe Company (BD) LTDDocument19 pagesRatio Analysis Of: Bata Shoe Company (BD) LTDMonjur HasanNo ratings yet

Download as pdf or txt

You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Accounting Policy Memo - Cash Equivalents & ST InvestmentsDocument2 pagesAccounting Policy Memo - Cash Equivalents & ST Investmentsdalebowen100% (1)

- Application 1 (Basic Steps in Accounting)Document2 pagesApplication 1 (Basic Steps in Accounting)Maria Nezka Advincula86% (7)

- Online Food Delivery ServiceDocument20 pagesOnline Food Delivery ServicevyapakNo ratings yet

- Chapter 6 PPT (AIS - James Hall)Document9 pagesChapter 6 PPT (AIS - James Hall)Nur-aima MortabaNo ratings yet

- Partnership DissolutionDocument46 pagesPartnership Dissolutionxenovia chuchuNo ratings yet

- Accounting For Partnership DissolutionDocument51 pagesAccounting For Partnership DissolutionRica Ella RestauroNo ratings yet

- Accounting For Partnership DissolutionDocument49 pagesAccounting For Partnership DissolutionTULIO, Jeremy I.No ratings yet

- M5a Liquidation P1 SBDocument10 pagesM5a Liquidation P1 SBKenzel lawasNo ratings yet

- AC - IntAcctg-A LSLiquidation.Document41 pagesAC - IntAcctg-A LSLiquidation.Janesene SolNo ratings yet

- MODULE 5-Part 1Document5 pagesMODULE 5-Part 1trixie maeNo ratings yet

- MODULE 5-Part 1Document5 pagesMODULE 5-Part 1Mary Joy CabilNo ratings yet

- M5c Liquidation P3 SBDocument5 pagesM5c Liquidation P3 SBKenzel lawasNo ratings yet

- 1stLecture-Partnership LiquidationDocument25 pages1stLecture-Partnership LiquidationRechelle Dalusung100% (1)

- Module 5 Accounting 2 Partnership Liquidation by InstallmentDocument9 pagesModule 5 Accounting 2 Partnership Liquidation by InstallmentJemima TapioNo ratings yet

- ACW1100 Tutorial Week2Document12 pagesACW1100 Tutorial Week2林志成No ratings yet

- Classroom Exerisises On Presentation of Financial Statements PDFDocument2 pagesClassroom Exerisises On Presentation of Financial Statements PDFalyssaNo ratings yet

- Solution in Partnership Liquidation InstallmentDocument20 pagesSolution in Partnership Liquidation InstallmentNikki GarciaNo ratings yet

- Marbella - Accounting For Special TransactionsDocument4 pagesMarbella - Accounting For Special TransactionsMelch Yvan Racasa MarbellaNo ratings yet

- Chapter Five PrintDocument18 pagesChapter Five PrintGedionNo ratings yet

- Joint Arrangement Answer KeyDocument8 pagesJoint Arrangement Answer KeyMonica DespiNo ratings yet

- Total Assets 335,000 80,000: Additional InformationDocument8 pagesTotal Assets 335,000 80,000: Additional InformationHohohoNo ratings yet

- #Chapter 4 Asignación (Recovered)Document22 pages#Chapter 4 Asignación (Recovered)adrianasofiagomez14No ratings yet

- M5b Liquidation P2 SBDocument6 pagesM5b Liquidation P2 SBKenzel lawasNo ratings yet

- SEM III - Advanced Accounting (EM)Document4 pagesSEM III - Advanced Accounting (EM)Abdul MalikNo ratings yet

- PRACTICE EXAM AnswersDocument7 pagesPRACTICE EXAM Answersarhamjain269No ratings yet

- Asm ACCOUNTINGDocument16 pagesAsm ACCOUNTINGVũ Khánh HuyềnNo ratings yet

- May 2017 Advanced Financial Accounting & Reporting Final Pre-BoardDocument20 pagesMay 2017 Advanced Financial Accounting & Reporting Final Pre-BoardPatrick ArazoNo ratings yet

- Hedge Fund Reports and Financial StatementDocument96 pagesHedge Fund Reports and Financial StatementOlivier MNo ratings yet

- PartnershipDocument10 pagesPartnershipShaz NagaNo ratings yet

- Accounting For Special Transactions - Module 4Document9 pagesAccounting For Special Transactions - Module 4Jcel JcelNo ratings yet

- DIY LiquidationDocument27 pagesDIY LiquidationJOYCE C ANDADORNo ratings yet

- Accounting 10 ColumnsDocument2 pagesAccounting 10 ColumnsTRIXIEJOY INIONNo ratings yet

- Buscom ReportDocument2 pagesBuscom ReportJashly FuentesNo ratings yet

- Examination Question and Answers, Set F (Problem Solving), Chapter 15 - Statement of Cash FlowDocument3 pagesExamination Question and Answers, Set F (Problem Solving), Chapter 15 - Statement of Cash Flowjohn carlos doringoNo ratings yet

- Partnership 2021 - Long ProblemsDocument5 pagesPartnership 2021 - Long ProblemsMichael MagdaogNo ratings yet

- Paper 8 FM ECODocument361 pagesPaper 8 FM ECOmhdsameem123No ratings yet

- Partnership LiquidationDocument28 pagesPartnership LiquidationDela cruz, Hainrich (Hain)No ratings yet

- Pa Revision For FinalsDocument9 pagesPa Revision For FinalsKhải Hưng NguyễnNo ratings yet

- Fabm2 2nd PrelimDocument2 pagesFabm2 2nd PrelimAngelica NacisNo ratings yet

- Module-2 Equity Valuation Numerical For StudentsDocument11 pagesModule-2 Equity Valuation Numerical For Studentsgaurav supadeNo ratings yet

- 07 Activity AtanezDocument2 pages07 Activity AtanezSteff Atañez100% (1)

- Final Activity 3 QuestionDocument2 pagesFinal Activity 3 QuestionSze ChristienyNo ratings yet

- Chapter 2 - Partnership Formation ObjectivesDocument10 pagesChapter 2 - Partnership Formation ObjectivesSapphire AliasNo ratings yet

- Partnership Liquidation Answer KeyDocument16 pagesPartnership Liquidation Answer KeyJerickho JNo ratings yet

- Micolob - Tla 2 - Answers SheetDocument18 pagesMicolob - Tla 2 - Answers SheetHaries MicolobNo ratings yet

- Partnership Accounting: FormationDocument6 pagesPartnership Accounting: FormationLee SuarezNo ratings yet

- Long QuizDocument5 pagesLong QuizMitch Tokong MinglanaNo ratings yet

- Mba ZC415 Ec-3r First Sem 2022-2023Document4 pagesMba ZC415 Ec-3r First Sem 2022-2023Ravi KaviNo ratings yet

- Introduction To Group Statements - FASSET Class - 15 May 2021Document22 pagesIntroduction To Group Statements - FASSET Class - 15 May 2021Mike NdunaNo ratings yet

- HandOut No 2 Busfin Financial StatementsDocument5 pagesHandOut No 2 Busfin Financial Statementsnatalie clyde matesNo ratings yet

- Problem 2 - AccountingcyleDocument13 pagesProblem 2 - AccountingcyleGio BurburanNo ratings yet

- Illustration KK Co. Perpetual ClosingDocument9 pagesIllustration KK Co. Perpetual ClosingNAOL BIFTUNo ratings yet

- Partnership LiquidationDocument6 pagesPartnership LiquidationMonica MangobaNo ratings yet

- Ac 1104 - Partnership LiquidationDocument46 pagesAc 1104 - Partnership LiquidationNarikoNo ratings yet

- FA2 Chapter 4-Partnership-LiquidationDocument20 pagesFA2 Chapter 4-Partnership-LiquidationAyren Dela CruzNo ratings yet

- Business Combi PrelimDocument4 pagesBusiness Combi PrelimmcespressoblendNo ratings yet

- Poa 2012 Jan p.2.q.1 1Document4 pagesPoa 2012 Jan p.2.q.1 1RealGenius (Carl)No ratings yet

- Ast Discussion 4 - Partnership Liquidation For PrintDocument4 pagesAst Discussion 4 - Partnership Liquidation For PrintCHRISTINE TABULOGNo ratings yet

- Module 2Document6 pagesModule 2trixie mae0% (1)

- Module 2Document6 pagesModule 2Mary Joy CabilNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- Experimental Marketing in Indian Hotels PDFDocument11 pagesExperimental Marketing in Indian Hotels PDFAli ShalabyNo ratings yet

- Ib Chapter 7Document31 pagesIb Chapter 7K60 Nguyễn Thị Thanh HàNo ratings yet

- EEA Life Pricing 20160701Document1 pageEEA Life Pricing 20160701Southey CapitalNo ratings yet

- Management Advisory Services - PreboardDocument13 pagesManagement Advisory Services - PreboardAngelica Estrada100% (4)

- Saint Louis College-Cebu: (Servant Leaders For Mission)Document4 pagesSaint Louis College-Cebu: (Servant Leaders For Mission)Marc Graham NacuaNo ratings yet

- Rural Marketing MixDocument2 pagesRural Marketing MixKhushi SiviaNo ratings yet

- VMG Myanmar Company ProfileDocument10 pagesVMG Myanmar Company Profilehtetarkar022023No ratings yet

- Sap Customer Relationship ManagementDocument27 pagesSap Customer Relationship ManagementkulkarnihNo ratings yet

- Bridge Course For AccountingDocument4 pagesBridge Course For Accountingaysha banuNo ratings yet

- A STRATEGY FOR E-TYPE Final Project PART 2 PDFDocument2 pagesA STRATEGY FOR E-TYPE Final Project PART 2 PDFLuis Felipe Arenas100% (1)

- كتاب التسويق الاستراتيجيsDocument388 pagesكتاب التسويق الاستراتيجيsMaria SayedNo ratings yet

- The Promise and Peril of Real OptionsDocument17 pagesThe Promise and Peril of Real OptionsAmit Kumar JainNo ratings yet

- NX9523 - Biz Professional Practise Coursework (w21068666) - 05112022Document12 pagesNX9523 - Biz Professional Practise Coursework (w21068666) - 05112022Jorris NgNo ratings yet

- External Audit ThesisDocument8 pagesExternal Audit ThesisLisa Riley100% (2)

- Celebrity EndorsementDocument8 pagesCelebrity EndorsementMuhammad ZubairNo ratings yet

- 2021 HCI BT Essay Question 2Document5 pages2021 HCI BT Essay Question 2CHUA MING XIU HCINo ratings yet

- Ast MidtermDocument4 pagesAst MidtermCathleen Drew TuazonNo ratings yet

- Jonathan Herjanto - 2301890434 Devin Verdian - 2301888846 Ashraf Budi Rifdiansyah - 2301919284 Jericko Panlen Liem - 2301883593Document25 pagesJonathan Herjanto - 2301890434 Devin Verdian - 2301888846 Ashraf Budi Rifdiansyah - 2301919284 Jericko Panlen Liem - 2301883593Johan FNo ratings yet

- Accounting Concept (Or Convention) Involved in Preparing A Provision For Doubtful Debts Account.Document2 pagesAccounting Concept (Or Convention) Involved in Preparing A Provision For Doubtful Debts Account.sharvin_94100% (3)

- Milestone 2 Java Done Vol 2Document21 pagesMilestone 2 Java Done Vol 2Erial dearv EscatinNo ratings yet

- 12th Commerce - Public Exam - Key Answer March - 2022-23 (EM)Document11 pages12th Commerce - Public Exam - Key Answer March - 2022-23 (EM)baharipriyan788No ratings yet

- Primary Vs Secondary DemandDocument4 pagesPrimary Vs Secondary DemandVivek MadupuNo ratings yet

- What Is The Difference Between Bussiness Plan and Project ProposalDocument6 pagesWhat Is The Difference Between Bussiness Plan and Project ProposalshumetNo ratings yet

- Ever Bilena Cosmetic Direct Sales Case Study by Rivera and Chua PDFDocument15 pagesEver Bilena Cosmetic Direct Sales Case Study by Rivera and Chua PDFPrecious Mole Tipas ES AnnexNo ratings yet

- Jawaban Inter 1 Modul 9Document4 pagesJawaban Inter 1 Modul 9Sebastian T.MNo ratings yet

- SIP VIP PPT 14-15 SalesDocument19 pagesSIP VIP PPT 14-15 SalesAshutoshNo ratings yet

- Ratio Analysis Of: Bata Shoe Company (BD) LTDDocument19 pagesRatio Analysis Of: Bata Shoe Company (BD) LTDMonjur HasanNo ratings yet