Lecture Notes - Utilization and Impairment-2

Lecture Notes - Utilization and Impairment-2

You might also like

- Nike Inc. Cost of Capital Case AnalysisDocument7 pagesNike Inc. Cost of Capital Case Analysisrmdelmando100% (6)

- Chap 010Document17 pagesChap 010van tinh khucNo ratings yet

- King Enterprises Is A Book Wholesaler King Hired A NewDocument1 pageKing Enterprises Is A Book Wholesaler King Hired A Newtrilocksp SinghNo ratings yet

- Financial Accounting - Fixed AssetsDocument5 pagesFinancial Accounting - Fixed Assetsearlalegre48No ratings yet

- ACC201 PPTs - 1T2018 - Workshop 07 - Week 08Document18 pagesACC201 PPTs - 1T2018 - Workshop 07 - Week 08Luu MinhNo ratings yet

- Mcgrawhill NotesDocument9 pagesMcgrawhill NotesJ ZNo ratings yet

- Financial Accounting - Information For Decisions - Session 5 - Chapter 7 PPT gFWXdxUqrsDocument55 pagesFinancial Accounting - Information For Decisions - Session 5 - Chapter 7 PPT gFWXdxUqrsmukul3087_305865623No ratings yet

- III. Accounting Treatment For Non-Current AssetsDocument6 pagesIII. Accounting Treatment For Non-Current AssetsCezar CalinNo ratings yet

- LKAS 16 - TheoryDocument27 pagesLKAS 16 - Theoryshafeeibrahim75No ratings yet

- BBA II Chapter 3 Depreciation AccountingDocument28 pagesBBA II Chapter 3 Depreciation AccountingSiddharth Salgaonkar100% (1)

- E - Learning Content DepreciationDocument14 pagesE - Learning Content DepreciationNikhil JadhavNo ratings yet

- Ias 16Document44 pagesIas 16Faraz Ahmed QuddusiNo ratings yet

- Accounting For Property, Plant, and EquipmentDocument33 pagesAccounting For Property, Plant, and Equipmentnatinaelbahiru74No ratings yet

- INTANGIBLESDocument40 pagesINTANGIBLESPhoebe Dayrit CunananNo ratings yet

- Ias 16 & Ias 40Document47 pagesIas 16 & Ias 40Etiel Films / ኢትኤል ፊልሞች100% (1)

- Topic Vii:: Long-Lived Nonmonetary AssetsDocument23 pagesTopic Vii:: Long-Lived Nonmonetary AssetsDiana Maria100% (1)

- Depreciation and AmortisationDocument25 pagesDepreciation and AmortisationNikhil RamalingamNo ratings yet

- FoA-CH-III - PPE - 2021Document17 pagesFoA-CH-III - PPE - 2021medhane negaNo ratings yet

- Accounting For Non-Current AssetsDocument8 pagesAccounting For Non-Current AssetsvladsteinarminNo ratings yet

- Unit 2 PpeDocument82 pagesUnit 2 PpeHirut GetachewNo ratings yet

- What Are The Main Types of Depreciation Methods?: #1 Straight-Line Depreciation MethodDocument23 pagesWhat Are The Main Types of Depreciation Methods?: #1 Straight-Line Depreciation MethodShamarat RahmanNo ratings yet

- Chapter 3 Property, Plant and EquipmentDocument6 pagesChapter 3 Property, Plant and Equipmentvchandy22No ratings yet

- Ias 16 PpeDocument168 pagesIas 16 PpeValeria PetrovNo ratings yet

- Module 4Document10 pagesModule 4bhettyna noayNo ratings yet

- R30 Long Lived AssetsDocument33 pagesR30 Long Lived AssetsSiddhu Sai100% (1)

- Csfas Pas16Document29 pagesCsfas Pas16Jack GriffoNo ratings yet

- Module On Impairment of AssetsDocument4 pagesModule On Impairment of AssetsDaniellaNo ratings yet

- CH 09 In-Class Problems - Fall 2013Document4 pagesCH 09 In-Class Problems - Fall 2013StephNo ratings yet

- Property Plant and EquipmentDocument32 pagesProperty Plant and EquipmentKyllie CamantigueNo ratings yet

- Fair Value Matching PrincipleDocument5 pagesFair Value Matching PrincipleGracie Kiarie100% (1)

- ACC 1100 Days 14&15 Long-Lived Assets PDFDocument25 pagesACC 1100 Days 14&15 Long-Lived Assets PDFYevhenii VdovenkoNo ratings yet

- Lecture Notes Iass 16 EtcDocument31 pagesLecture Notes Iass 16 Etcmayillahmansaray40No ratings yet

- Property, Plant and Equipment - DepreciationDocument34 pagesProperty, Plant and Equipment - DepreciationSharmaineMiranda50% (2)

- F7 - C2 & C3A PPE & Borrowing Cost AnsDocument53 pagesF7 - C2 & C3A PPE & Borrowing Cost AnsK59 Vo Doan Hoang AnhNo ratings yet

- Lkas 16 Ppe SliitDocument39 pagesLkas 16 Ppe SliitSuwani HettiarachchiNo ratings yet

- 2.1. Property Plant and Equipment IAS 16Document7 pages2.1. Property Plant and Equipment IAS 16Priya Satheesh100% (1)

- Accunting Exam 3Document4 pagesAccunting Exam 3Trixie SannadNo ratings yet

- Fundamentals of AccountingDocument76 pagesFundamentals of AccountingNo MoreNo ratings yet

- Chapter 11Document26 pagesChapter 11ENG ZI QINGNo ratings yet

- Week 10 - 02 - Module 23 - Property, Plant & Equipment (Part 2)Document10 pagesWeek 10 - 02 - Module 23 - Property, Plant & Equipment (Part 2)지마리No ratings yet

- DepreciationDocument8 pagesDepreciationbhanu100% (1)

- 10.11 AS 26 Intangible AssetsDocument5 pages10.11 AS 26 Intangible AssetsAnakin SkywalkerNo ratings yet

- 17.11.2020 IAS 16 Property, Plant and EquipmentDocument12 pages17.11.2020 IAS 16 Property, Plant and EquipmentLolita IsakhanyanNo ratings yet

- Application of Ifrs (Ind As) For Transactions: Unit - 2Document40 pagesApplication of Ifrs (Ind As) For Transactions: Unit - 2Talla Mokshitha100% (1)

- IAS 16 Property Plant and EquipmentDocument12 pagesIAS 16 Property Plant and Equipmentwaseefahmad89No ratings yet

- Prepare Financial Report 3rdDocument12 pagesPrepare Financial Report 3rdTegene Tesfaye100% (1)

- 10 Week 10 CHPT 14n15 NCADocument47 pages10 Week 10 CHPT 14n15 NCA1621995944No ratings yet

- Lecture Notes Chapter 10 (2022) - Student VerDocument50 pagesLecture Notes Chapter 10 (2022) - Student VerThương Đỗ100% (1)

- Long-Lived Assets Pratt, Financial Accounting 7e, Chapter 9Document7 pagesLong-Lived Assets Pratt, Financial Accounting 7e, Chapter 9chetandeepakNo ratings yet

- More ConceptsDocument47 pagesMore ConceptsGurkirat Singh100% (1)

- Equip. Note PDFDocument16 pagesEquip. Note PDFhailush girmay100% (1)

- Presentationprint TempDocument67 pagesPresentationprint TempMd EndrisNo ratings yet

- #21 Depreciation & Depletion (Notes For 6205)Document4 pages#21 Depreciation & Depletion (Notes For 6205)Claudine DuhapaNo ratings yet

- International Accounting Standard 16 Property, Plant and EquipmentDocument29 pagesInternational Accounting Standard 16 Property, Plant and EquipmentAbdullah Shaker TahaNo ratings yet

- Ias 16 Property Plant Equipment v1 080713Document7 pagesIas 16 Property Plant Equipment v1 080713Phebieon MukwenhaNo ratings yet

- Accounting Standard 6 - DepreciationDocument34 pagesAccounting Standard 6 - DepreciationSarthak Gupta100% (2)

- CHAPTER 10 - PROPERTY, PLANT AND EQUIPMENT (v2)Document20 pagesCHAPTER 10 - PROPERTY, PLANT AND EQUIPMENT (v2)VerrelyNo ratings yet

- Pas 38 - Intangible AssetsDocument21 pagesPas 38 - Intangible AssetsMa. Franceska Loiz T. RiveraNo ratings yet

- Chapter 10 - Fixed Assets and Intangible AssetsDocument94 pagesChapter 10 - Fixed Assets and Intangible AssetsAsti RahmadaniaNo ratings yet

- Financial Accounting IIDocument13 pagesFinancial Accounting IITimi DeleNo ratings yet

- Investments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsFrom EverandInvestments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsNo ratings yet

- Herbal MedicationsDocument34 pagesHerbal MedicationsJosh PagnamitanNo ratings yet

- Cardiovascular DiseasesDocument46 pagesCardiovascular DiseasesJosh PagnamitanNo ratings yet

- Parenteral InjectionsDocument39 pagesParenteral InjectionsJosh PagnamitanNo ratings yet

- Maternal and Child Health Nursing Flashcards QuizletDocument1 pageMaternal and Child Health Nursing Flashcards QuizletJosh PagnamitanNo ratings yet

- Accenture Service Design Tale Two Coffee Shops TranscriptDocument2 pagesAccenture Service Design Tale Two Coffee Shops TranscriptAmilcar Alvarez de LeonNo ratings yet

- Entrep ComputationDocument18 pagesEntrep ComputationEmman RevillaNo ratings yet

- Chapter 11: The Capital MarketDocument5 pagesChapter 11: The Capital MarketMike RajasNo ratings yet

- CV Unit 9Document13 pagesCV Unit 9amrutraj gNo ratings yet

- WCM Principle 4 HeijunkaDocument33 pagesWCM Principle 4 HeijunkaSaurabh KothawadeNo ratings yet

- RM Assignment GuidelinesDocument2 pagesRM Assignment Guidelinessayanchakrabortymba2022No ratings yet

- Sample Marketing Plan SonicDocument11 pagesSample Marketing Plan SonicJames Benedict MalabananNo ratings yet

- FMCG Case StudyDocument5 pagesFMCG Case StudyDini PutriNo ratings yet

- Rolling Budget and Forecast : Model KeyDocument2 pagesRolling Budget and Forecast : Model KeyomernoumanNo ratings yet

- Chapter 2 Customer Based Brand EquityDocument39 pagesChapter 2 Customer Based Brand EquityAditya UpretiNo ratings yet

- Microsoft Dynamics CRM 2016 ReadinessDocument7 pagesMicrosoft Dynamics CRM 2016 ReadinessyoussefNo ratings yet

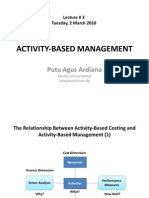

- Activity Based ManagementDocument27 pagesActivity Based ManagementKomang PNNo ratings yet

- SwotDocument7 pagesSwotBiren PachalNo ratings yet

- The Similarities and Differences Between Bangladesh and VietnamDocument8 pagesThe Similarities and Differences Between Bangladesh and VietnamOnin HasanNo ratings yet

- Example Company (Pty) LTD: Cashbook TransactionsDocument8 pagesExample Company (Pty) LTD: Cashbook TransactionsShakkuNo ratings yet

- SCMchapter 4Document39 pagesSCMchapter 4KgnasNo ratings yet

- Managerial Accounting: Tools For Business Decision-MakingDocument69 pagesManagerial Accounting: Tools For Business Decision-MakingdavidNo ratings yet

- Best Twitter Campaign: AirbnbDocument4 pagesBest Twitter Campaign: AirbnbMaryam KhanNo ratings yet

- TB Chapter 01Document28 pagesTB Chapter 01josephnikolaiNo ratings yet

- ch03Document62 pagesch03Mona ElzaherNo ratings yet

- Gitman pmf13 ppt08Document70 pagesGitman pmf13 ppt08Ali Sam100% (1)

- Questionnaire For CadburyDocument5 pagesQuestionnaire For CadburyManish Rajwani100% (2)

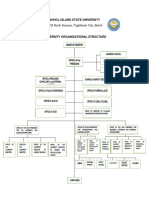

- Bohol Island State UniversityDocument3 pagesBohol Island State UniversityJude Vincent MacalosNo ratings yet

- Esg Sustainable Advantage 1Document20 pagesEsg Sustainable Advantage 1Jalagandeeswaran KalimuthuNo ratings yet

- 3705 Assignment 2Document4 pages3705 Assignment 2givenl193No ratings yet

- Online Marketing Using Social Media Performed by Star-Up Entrepreneurs in Kediri RegencyDocument7 pagesOnline Marketing Using Social Media Performed by Star-Up Entrepreneurs in Kediri RegencyYulindo Laksa DiartaNo ratings yet

- Accounting EnglishDocument17 pagesAccounting EnglishDiana Irimescu0% (1)

Download as pdf or txt

You might also like

- Nike Inc. Cost of Capital Case AnalysisDocument7 pagesNike Inc. Cost of Capital Case Analysisrmdelmando100% (6)

- Chap 010Document17 pagesChap 010van tinh khucNo ratings yet

- King Enterprises Is A Book Wholesaler King Hired A NewDocument1 pageKing Enterprises Is A Book Wholesaler King Hired A Newtrilocksp SinghNo ratings yet

- Financial Accounting - Fixed AssetsDocument5 pagesFinancial Accounting - Fixed Assetsearlalegre48No ratings yet

- ACC201 PPTs - 1T2018 - Workshop 07 - Week 08Document18 pagesACC201 PPTs - 1T2018 - Workshop 07 - Week 08Luu MinhNo ratings yet

- Mcgrawhill NotesDocument9 pagesMcgrawhill NotesJ ZNo ratings yet

- Financial Accounting - Information For Decisions - Session 5 - Chapter 7 PPT gFWXdxUqrsDocument55 pagesFinancial Accounting - Information For Decisions - Session 5 - Chapter 7 PPT gFWXdxUqrsmukul3087_305865623No ratings yet

- III. Accounting Treatment For Non-Current AssetsDocument6 pagesIII. Accounting Treatment For Non-Current AssetsCezar CalinNo ratings yet

- LKAS 16 - TheoryDocument27 pagesLKAS 16 - Theoryshafeeibrahim75No ratings yet

- BBA II Chapter 3 Depreciation AccountingDocument28 pagesBBA II Chapter 3 Depreciation AccountingSiddharth Salgaonkar100% (1)

- E - Learning Content DepreciationDocument14 pagesE - Learning Content DepreciationNikhil JadhavNo ratings yet

- Ias 16Document44 pagesIas 16Faraz Ahmed QuddusiNo ratings yet

- Accounting For Property, Plant, and EquipmentDocument33 pagesAccounting For Property, Plant, and Equipmentnatinaelbahiru74No ratings yet

- INTANGIBLESDocument40 pagesINTANGIBLESPhoebe Dayrit CunananNo ratings yet

- Ias 16 & Ias 40Document47 pagesIas 16 & Ias 40Etiel Films / ኢትኤል ፊልሞች100% (1)

- Topic Vii:: Long-Lived Nonmonetary AssetsDocument23 pagesTopic Vii:: Long-Lived Nonmonetary AssetsDiana Maria100% (1)

- Depreciation and AmortisationDocument25 pagesDepreciation and AmortisationNikhil RamalingamNo ratings yet

- FoA-CH-III - PPE - 2021Document17 pagesFoA-CH-III - PPE - 2021medhane negaNo ratings yet

- Accounting For Non-Current AssetsDocument8 pagesAccounting For Non-Current AssetsvladsteinarminNo ratings yet

- Unit 2 PpeDocument82 pagesUnit 2 PpeHirut GetachewNo ratings yet

- What Are The Main Types of Depreciation Methods?: #1 Straight-Line Depreciation MethodDocument23 pagesWhat Are The Main Types of Depreciation Methods?: #1 Straight-Line Depreciation MethodShamarat RahmanNo ratings yet

- Chapter 3 Property, Plant and EquipmentDocument6 pagesChapter 3 Property, Plant and Equipmentvchandy22No ratings yet

- Ias 16 PpeDocument168 pagesIas 16 PpeValeria PetrovNo ratings yet

- Module 4Document10 pagesModule 4bhettyna noayNo ratings yet

- R30 Long Lived AssetsDocument33 pagesR30 Long Lived AssetsSiddhu Sai100% (1)

- Csfas Pas16Document29 pagesCsfas Pas16Jack GriffoNo ratings yet

- Module On Impairment of AssetsDocument4 pagesModule On Impairment of AssetsDaniellaNo ratings yet

- CH 09 In-Class Problems - Fall 2013Document4 pagesCH 09 In-Class Problems - Fall 2013StephNo ratings yet

- Property Plant and EquipmentDocument32 pagesProperty Plant and EquipmentKyllie CamantigueNo ratings yet

- Fair Value Matching PrincipleDocument5 pagesFair Value Matching PrincipleGracie Kiarie100% (1)

- ACC 1100 Days 14&15 Long-Lived Assets PDFDocument25 pagesACC 1100 Days 14&15 Long-Lived Assets PDFYevhenii VdovenkoNo ratings yet

- Lecture Notes Iass 16 EtcDocument31 pagesLecture Notes Iass 16 Etcmayillahmansaray40No ratings yet

- Property, Plant and Equipment - DepreciationDocument34 pagesProperty, Plant and Equipment - DepreciationSharmaineMiranda50% (2)

- F7 - C2 & C3A PPE & Borrowing Cost AnsDocument53 pagesF7 - C2 & C3A PPE & Borrowing Cost AnsK59 Vo Doan Hoang AnhNo ratings yet

- Lkas 16 Ppe SliitDocument39 pagesLkas 16 Ppe SliitSuwani HettiarachchiNo ratings yet

- 2.1. Property Plant and Equipment IAS 16Document7 pages2.1. Property Plant and Equipment IAS 16Priya Satheesh100% (1)

- Accunting Exam 3Document4 pagesAccunting Exam 3Trixie SannadNo ratings yet

- Fundamentals of AccountingDocument76 pagesFundamentals of AccountingNo MoreNo ratings yet

- Chapter 11Document26 pagesChapter 11ENG ZI QINGNo ratings yet

- Week 10 - 02 - Module 23 - Property, Plant & Equipment (Part 2)Document10 pagesWeek 10 - 02 - Module 23 - Property, Plant & Equipment (Part 2)지마리No ratings yet

- DepreciationDocument8 pagesDepreciationbhanu100% (1)

- 10.11 AS 26 Intangible AssetsDocument5 pages10.11 AS 26 Intangible AssetsAnakin SkywalkerNo ratings yet

- 17.11.2020 IAS 16 Property, Plant and EquipmentDocument12 pages17.11.2020 IAS 16 Property, Plant and EquipmentLolita IsakhanyanNo ratings yet

- Application of Ifrs (Ind As) For Transactions: Unit - 2Document40 pagesApplication of Ifrs (Ind As) For Transactions: Unit - 2Talla Mokshitha100% (1)

- IAS 16 Property Plant and EquipmentDocument12 pagesIAS 16 Property Plant and Equipmentwaseefahmad89No ratings yet

- Prepare Financial Report 3rdDocument12 pagesPrepare Financial Report 3rdTegene Tesfaye100% (1)

- 10 Week 10 CHPT 14n15 NCADocument47 pages10 Week 10 CHPT 14n15 NCA1621995944No ratings yet

- Lecture Notes Chapter 10 (2022) - Student VerDocument50 pagesLecture Notes Chapter 10 (2022) - Student VerThương Đỗ100% (1)

- Long-Lived Assets Pratt, Financial Accounting 7e, Chapter 9Document7 pagesLong-Lived Assets Pratt, Financial Accounting 7e, Chapter 9chetandeepakNo ratings yet

- More ConceptsDocument47 pagesMore ConceptsGurkirat Singh100% (1)

- Equip. Note PDFDocument16 pagesEquip. Note PDFhailush girmay100% (1)

- Presentationprint TempDocument67 pagesPresentationprint TempMd EndrisNo ratings yet

- #21 Depreciation & Depletion (Notes For 6205)Document4 pages#21 Depreciation & Depletion (Notes For 6205)Claudine DuhapaNo ratings yet

- International Accounting Standard 16 Property, Plant and EquipmentDocument29 pagesInternational Accounting Standard 16 Property, Plant and EquipmentAbdullah Shaker TahaNo ratings yet

- Ias 16 Property Plant Equipment v1 080713Document7 pagesIas 16 Property Plant Equipment v1 080713Phebieon MukwenhaNo ratings yet

- Accounting Standard 6 - DepreciationDocument34 pagesAccounting Standard 6 - DepreciationSarthak Gupta100% (2)

- CHAPTER 10 - PROPERTY, PLANT AND EQUIPMENT (v2)Document20 pagesCHAPTER 10 - PROPERTY, PLANT AND EQUIPMENT (v2)VerrelyNo ratings yet

- Pas 38 - Intangible AssetsDocument21 pagesPas 38 - Intangible AssetsMa. Franceska Loiz T. RiveraNo ratings yet

- Chapter 10 - Fixed Assets and Intangible AssetsDocument94 pagesChapter 10 - Fixed Assets and Intangible AssetsAsti RahmadaniaNo ratings yet

- Financial Accounting IIDocument13 pagesFinancial Accounting IITimi DeleNo ratings yet

- Investments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsFrom EverandInvestments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsNo ratings yet

- Herbal MedicationsDocument34 pagesHerbal MedicationsJosh PagnamitanNo ratings yet

- Cardiovascular DiseasesDocument46 pagesCardiovascular DiseasesJosh PagnamitanNo ratings yet

- Parenteral InjectionsDocument39 pagesParenteral InjectionsJosh PagnamitanNo ratings yet

- Maternal and Child Health Nursing Flashcards QuizletDocument1 pageMaternal and Child Health Nursing Flashcards QuizletJosh PagnamitanNo ratings yet

- Accenture Service Design Tale Two Coffee Shops TranscriptDocument2 pagesAccenture Service Design Tale Two Coffee Shops TranscriptAmilcar Alvarez de LeonNo ratings yet

- Entrep ComputationDocument18 pagesEntrep ComputationEmman RevillaNo ratings yet

- Chapter 11: The Capital MarketDocument5 pagesChapter 11: The Capital MarketMike RajasNo ratings yet

- CV Unit 9Document13 pagesCV Unit 9amrutraj gNo ratings yet

- WCM Principle 4 HeijunkaDocument33 pagesWCM Principle 4 HeijunkaSaurabh KothawadeNo ratings yet

- RM Assignment GuidelinesDocument2 pagesRM Assignment Guidelinessayanchakrabortymba2022No ratings yet

- Sample Marketing Plan SonicDocument11 pagesSample Marketing Plan SonicJames Benedict MalabananNo ratings yet

- FMCG Case StudyDocument5 pagesFMCG Case StudyDini PutriNo ratings yet

- Rolling Budget and Forecast : Model KeyDocument2 pagesRolling Budget and Forecast : Model KeyomernoumanNo ratings yet

- Chapter 2 Customer Based Brand EquityDocument39 pagesChapter 2 Customer Based Brand EquityAditya UpretiNo ratings yet

- Microsoft Dynamics CRM 2016 ReadinessDocument7 pagesMicrosoft Dynamics CRM 2016 ReadinessyoussefNo ratings yet

- Activity Based ManagementDocument27 pagesActivity Based ManagementKomang PNNo ratings yet

- SwotDocument7 pagesSwotBiren PachalNo ratings yet

- The Similarities and Differences Between Bangladesh and VietnamDocument8 pagesThe Similarities and Differences Between Bangladesh and VietnamOnin HasanNo ratings yet

- Example Company (Pty) LTD: Cashbook TransactionsDocument8 pagesExample Company (Pty) LTD: Cashbook TransactionsShakkuNo ratings yet

- SCMchapter 4Document39 pagesSCMchapter 4KgnasNo ratings yet

- Managerial Accounting: Tools For Business Decision-MakingDocument69 pagesManagerial Accounting: Tools For Business Decision-MakingdavidNo ratings yet

- Best Twitter Campaign: AirbnbDocument4 pagesBest Twitter Campaign: AirbnbMaryam KhanNo ratings yet

- TB Chapter 01Document28 pagesTB Chapter 01josephnikolaiNo ratings yet

- ch03Document62 pagesch03Mona ElzaherNo ratings yet

- Gitman pmf13 ppt08Document70 pagesGitman pmf13 ppt08Ali Sam100% (1)

- Questionnaire For CadburyDocument5 pagesQuestionnaire For CadburyManish Rajwani100% (2)

- Bohol Island State UniversityDocument3 pagesBohol Island State UniversityJude Vincent MacalosNo ratings yet

- Esg Sustainable Advantage 1Document20 pagesEsg Sustainable Advantage 1Jalagandeeswaran KalimuthuNo ratings yet

- 3705 Assignment 2Document4 pages3705 Assignment 2givenl193No ratings yet

- Online Marketing Using Social Media Performed by Star-Up Entrepreneurs in Kediri RegencyDocument7 pagesOnline Marketing Using Social Media Performed by Star-Up Entrepreneurs in Kediri RegencyYulindo Laksa DiartaNo ratings yet

- Accounting EnglishDocument17 pagesAccounting EnglishDiana Irimescu0% (1)