Acc Group Assignment Elaine (1) Final Report

Acc Group Assignment Elaine (1) Final Report

You might also like

- Assignment# 3 Magic TimberDocument5 pagesAssignment# 3 Magic TimberASAD ULLAH0% (2)

- R0 - Internal Electrical-Boq With CostDocument12 pagesR0 - Internal Electrical-Boq With Costshruti widhani33% (3)

- UAC2021 HandbookDocument71 pagesUAC2021 Handbookaldo serena sandresNo ratings yet

- BOQ Pharma UtilitiesDocument109 pagesBOQ Pharma UtilitiesSajeshKumarNo ratings yet

- Memorandum of Agreement: Samson ConstructionDocument7 pagesMemorandum of Agreement: Samson ConstructionMimi KasukaNo ratings yet

- FarahDocument7 pagesFarahMijan RahmanNo ratings yet

- 4597 AAB SC 07 Addendum 2 R0v0 63Document1 page4597 AAB SC 07 Addendum 2 R0v0 63danieldumapitNo ratings yet

- 9300 Perbaikan Hmi Siemens Smart 700 Ie Model. 1p 6av6 648-0bc11-3ax0 Sn. S Zvd5ydd046991 Pt. FaratuDocument2 pages9300 Perbaikan Hmi Siemens Smart 700 Ie Model. 1p 6av6 648-0bc11-3ax0 Sn. S Zvd5ydd046991 Pt. FaratuFitri YaniNo ratings yet

- GADDocument3 pagesGADphcabaconganNo ratings yet

- Revised Estimate Street Lights For Workers Accomodation at Goa - 15 MAY 2023Document6 pagesRevised Estimate Street Lights For Workers Accomodation at Goa - 15 MAY 2023tnd tbecNo ratings yet

- KanyaririDocument15 pagesKanyaririsatejaNo ratings yet

- Tugas Pengantar Akuntansi - Timotius Siagian 1 C3Document8 pagesTugas Pengantar Akuntansi - Timotius Siagian 1 C3Timotius SiagianNo ratings yet

- Budget Pipe Rack New Tank OleoDocument28 pagesBudget Pipe Rack New Tank OleokamprettelanjangNo ratings yet

- Maxime Project ReportDocument60 pagesMaxime Project ReportMOHD GULZARNo ratings yet

- Quotation For 05 KW OFF GRID:: Quotation Date: 18 May, 2021 Unit Price (RS.) Quantity Total Cost (RS.)Document2 pagesQuotation For 05 KW OFF GRID:: Quotation Date: 18 May, 2021 Unit Price (RS.) Quantity Total Cost (RS.)ImranFazal100% (1)

- Wote Technical Training InstituteDocument1 pageWote Technical Training Institutemambopeter123No ratings yet

- BA 205 AnswerDocument5 pagesBA 205 AnswerAnhar Polo CanacanNo ratings yet

- HH221434 HH221410 B TaperedRollerBearings TSF (TaperedSinglewithFlange) Imperial PDFDocument5 pagesHH221434 HH221410 B TaperedRollerBearings TSF (TaperedSinglewithFlange) Imperial PDFjcojedar2009No ratings yet

- 460-ST-Q PT. Artajaya Langgengsentosa - EJF - 1Document1 page460-ST-Q PT. Artajaya Langgengsentosa - EJF - 1Nia WullandariNo ratings yet

- Financials - Dhobhi BhaiyaDocument9 pagesFinancials - Dhobhi Bhaiyaprince joshiNo ratings yet

- Financial Work ScheduleDocument1 pageFinancial Work ScheduleSisay chaneNo ratings yet

- Q-19 - 01-005 - MKE - R3 - Instalasi of Vertical Pump IP (Foundation Reducer Modification)Document2 pagesQ-19 - 01-005 - MKE - R3 - Instalasi of Vertical Pump IP (Foundation Reducer Modification)Suprayitno SupraNo ratings yet

- 790 Repair Chiller No. 1Document1 page790 Repair Chiller No. 1Rangga NoparaNo ratings yet

- Ragama OpticalDocument1 pageRagama Optical5hy7pyqhdbNo ratings yet

- Hydrant System OfferDocument5 pagesHydrant System OfferMd. Sujaur RahmanNo ratings yet

- Hydrant System OfferDocument5 pagesHydrant System OfferMd. Sujaur RahmanNo ratings yet

- Financial Model For BrandsDocument60 pagesFinancial Model For BrandsAnjali SrivastavaNo ratings yet

- Profit & Loss Accounts: Wing Chair GirogioDocument3 pagesProfit & Loss Accounts: Wing Chair Girogiofarsi786No ratings yet

- TATA KRISHNA LabourDocument13 pagesTATA KRISHNA LabourSUPRIYA NANDINo ratings yet

- Template de Mo Company Balance Sheet BudgetDocument2 pagesTemplate de Mo Company Balance Sheet BudgetDuta Hotel Group100% (1)

- Sample Budget Worksheet - Care and Shelter ComponentsDocument1 pageSample Budget Worksheet - Care and Shelter Componentsyourxmen2910No ratings yet

- Quotation S00345Document1 pageQuotation S00345Muhammad Tanvir MohsinNo ratings yet

- Acc106 Assignment 2 Tie Beauty Enterprise FinalDocument15 pagesAcc106 Assignment 2 Tie Beauty Enterprise Finalnur anisNo ratings yet

- By Pass Valve BifurcationDocument5 pagesBy Pass Valve BifurcationSarthak EnterprisesNo ratings yet

- Financial StatementsDocument10 pagesFinancial Statementsassg USMNo ratings yet

- S.No Description Qty Rate (RS.) Amount (RS.) RXQ12ARY6 - Daikin VRV X 12HP ODU Cooling OnlyDocument10 pagesS.No Description Qty Rate (RS.) Amount (RS.) RXQ12ARY6 - Daikin VRV X 12HP ODU Cooling Onlysenthil kumarNo ratings yet

- Fire 3Document2 pagesFire 3Kanaklata Civil Hospital SonitpurNo ratings yet

- 80 HP Kishore Pump Estimate, 88345Document1 page80 HP Kishore Pump Estimate, 88345aakashgupta viaanshNo ratings yet

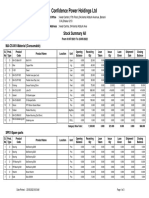

- Confidence Power Holdings LTD: Stock Summary AllDocument3 pagesConfidence Power Holdings LTD: Stock Summary AllAshik RahmanNo ratings yet

- Job Information: CCK Engineering & Construction Co.,Ltd. 1Document90 pagesJob Information: CCK Engineering & Construction Co.,Ltd. 1Kriengsak RuangdechNo ratings yet

- Shield Project Summary Phased BudgetDocument1 pageShield Project Summary Phased BudgetBinay BhandariNo ratings yet

- Budget Proposal: Optic Fibres and TowrsDocument5 pagesBudget Proposal: Optic Fibres and TowrsrjiveNo ratings yet

- Cash Flow Projection of MCV: SQM SQM RP.M/SQM RP.M/SQM SQM SQM RP.M US$. Tho Rp. MDocument26 pagesCash Flow Projection of MCV: SQM SQM RP.M/SQM RP.M/SQM SQM SQM RP.M US$. Tho Rp. Mangg4interNo ratings yet

- Appendix CDocument6 pagesAppendix CPat SulaimanNo ratings yet

- Stock Without ValueDocument57 pagesStock Without ValueAsian Techno Traders Pvt.Ltd. (Asian Staff)No ratings yet

- Tata Motors PresentationDocument121 pagesTata Motors PresentationSrikanth Reddy VemulaNo ratings yet

- Group 2 Business PlanDocument15 pagesGroup 2 Business PlanJam ReformaNo ratings yet

- Part Number 6311-Z-NR-C3, Deep Groove Ball Bearings (6000, 6200, 6300, 6400)Document3 pagesPart Number 6311-Z-NR-C3, Deep Groove Ball Bearings (6000, 6200, 6300, 6400)Travis DavisNo ratings yet

- Bapak Kevin 6963.2Document1 pageBapak Kevin 6963.2whatsup arwanNo ratings yet

- Jinkosolar Holding Co., LTD.: Q3 2017 Earnings Call PresentationDocument10 pagesJinkosolar Holding Co., LTD.: Q3 2017 Earnings Call PresentationAshutosh KumarNo ratings yet

- Overhead ApportionmentDocument3 pagesOverhead ApportionmentHassanAbsarQaimkhaniNo ratings yet

- Repair Chiller No. 2Document1 pageRepair Chiller No. 2Rangga NoparaNo ratings yet

- AssignmentDocument4 pagesAssignmentMenna MohamedNo ratings yet

- Delivery Note-Number Painting KafdDocument5 pagesDelivery Note-Number Painting KafdAbdul samee MianNo ratings yet

- Fees Structure of Top 4 NitDocument4 pagesFees Structure of Top 4 Nitsujeet kumarNo ratings yet

- Flexible BudgetDocument4 pagesFlexible BudgetSeli Fitria Rahma DiantikaNo ratings yet

- Final DPRDocument10 pagesFinal DPRGateway ComputersNo ratings yet

- Pt. Engineering Indonesia: Mvl'.ADocument4 pagesPt. Engineering Indonesia: Mvl'.AYudhi HerwantoNo ratings yet

- WorkshitDocument12 pagesWorkshitLukman ArimartaNo ratings yet

- 46KWp - Fincera DHA LahoreDocument3 pages46KWp - Fincera DHA Lahoretaibamalik457No ratings yet

- Engineering Service Revenues World Summary: Market Values & Financials by CountryFrom EverandEngineering Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Speed Changers, Drives & Gears World Summary: Market Values & Financials by CountryFrom EverandSpeed Changers, Drives & Gears World Summary: Market Values & Financials by CountryNo ratings yet

- ServitisationDocument32 pagesServitisation256850100% (1)

- Ibm Gatt and WtoDocument14 pagesIbm Gatt and Wto6038 Mugilan kNo ratings yet

- Commonwealth Bank StatementDocument5 pagesCommonwealth Bank StatementKate YehNo ratings yet

- Transcript Teleconference Financial Results Q1 2023Document16 pagesTranscript Teleconference Financial Results Q1 2023Cirlea CatalinNo ratings yet

- ICAB Advance Level Strategic Business Management Compilation of Chapterwise Theory For Exam May June 2020Document459 pagesICAB Advance Level Strategic Business Management Compilation of Chapterwise Theory For Exam May June 2020Optimal Management Solution100% (1)

- Ifii LK TW Iii 2022Document76 pagesIfii LK TW Iii 2022Sourav DuttaNo ratings yet

- Solved The Outstanding Stock in Red Blue and Green Corporations EachDocument1 pageSolved The Outstanding Stock in Red Blue and Green Corporations EachAnbu jaromiaNo ratings yet

- Soumil Final Project PDFDocument56 pagesSoumil Final Project PDFSoumil SoganiNo ratings yet

- Puccio Erbahar 2016Document26 pagesPuccio Erbahar 2016Vatsla BhatiaNo ratings yet

- Ch04 Strategic Planning Human Resource Planning and Job AnalysisDocument74 pagesCh04 Strategic Planning Human Resource Planning and Job AnalysisMohammedNo ratings yet

- Zinger Electronics, INC.: by Group 11 Marketing D'Document5 pagesZinger Electronics, INC.: by Group 11 Marketing D'jasmirsinghNo ratings yet

- 4303177Document6 pages4303177mohitgaba19No ratings yet

- Expected para Jumbles Questions PDF For SSC Tier II ExamsDocument44 pagesExpected para Jumbles Questions PDF For SSC Tier II Examsbijoyp348No ratings yet

- Case Study RubricDocument4 pagesCase Study RubricBrijendra SinghNo ratings yet

- Economics 2015: Sāmoa School CertificateDocument26 pagesEconomics 2015: Sāmoa School CertificatemonyNo ratings yet

- Dissertation On T&P of M&M Ltd.Document49 pagesDissertation On T&P of M&M Ltd.sampada_naradNo ratings yet

- Sap Business Bydesign Customer Relationship Management: OpensapDocument28 pagesSap Business Bydesign Customer Relationship Management: OpensapGaurab BanerjiNo ratings yet

- Accounting For DiscountsDocument2 pagesAccounting For DiscountsYamateNo ratings yet

- Innovación de Ciclo RapidoDocument10 pagesInnovación de Ciclo RapidoJuan David Ramirez SalazarNo ratings yet

- Updated Arrears Estimator Clerical StaffDocument8 pagesUpdated Arrears Estimator Clerical Staffkmuraleedharan09No ratings yet

- International Business Law and Its Environment 9th Edition Schaffer Solutions Manual DownloadDocument8 pagesInternational Business Law and Its Environment 9th Edition Schaffer Solutions Manual DownloadJohn Stewart100% (17)

- Chapter 2Document4 pagesChapter 2Roselie Cuenca94% (16)

- Commission Agreement - (GCC-Power Plant)Document2 pagesCommission Agreement - (GCC-Power Plant)Jonalyn TellesNo ratings yet

- Aluminum PorterDocument2 pagesAluminum PorterAmir ShameemNo ratings yet

- The Grat DreprestionDocument29 pagesThe Grat DreprestionAwura KwayowaaNo ratings yet

- Return On SalesDocument2 pagesReturn On SalesMa Terresa TejadaNo ratings yet

- BEC Vantage PG 8Document1 pageBEC Vantage PG 8juanNo ratings yet

Download as docx, pdf, or txt

You might also like

- Assignment# 3 Magic TimberDocument5 pagesAssignment# 3 Magic TimberASAD ULLAH0% (2)

- R0 - Internal Electrical-Boq With CostDocument12 pagesR0 - Internal Electrical-Boq With Costshruti widhani33% (3)

- UAC2021 HandbookDocument71 pagesUAC2021 Handbookaldo serena sandresNo ratings yet

- BOQ Pharma UtilitiesDocument109 pagesBOQ Pharma UtilitiesSajeshKumarNo ratings yet

- Memorandum of Agreement: Samson ConstructionDocument7 pagesMemorandum of Agreement: Samson ConstructionMimi KasukaNo ratings yet

- FarahDocument7 pagesFarahMijan RahmanNo ratings yet

- 4597 AAB SC 07 Addendum 2 R0v0 63Document1 page4597 AAB SC 07 Addendum 2 R0v0 63danieldumapitNo ratings yet

- 9300 Perbaikan Hmi Siemens Smart 700 Ie Model. 1p 6av6 648-0bc11-3ax0 Sn. S Zvd5ydd046991 Pt. FaratuDocument2 pages9300 Perbaikan Hmi Siemens Smart 700 Ie Model. 1p 6av6 648-0bc11-3ax0 Sn. S Zvd5ydd046991 Pt. FaratuFitri YaniNo ratings yet

- GADDocument3 pagesGADphcabaconganNo ratings yet

- Revised Estimate Street Lights For Workers Accomodation at Goa - 15 MAY 2023Document6 pagesRevised Estimate Street Lights For Workers Accomodation at Goa - 15 MAY 2023tnd tbecNo ratings yet

- KanyaririDocument15 pagesKanyaririsatejaNo ratings yet

- Tugas Pengantar Akuntansi - Timotius Siagian 1 C3Document8 pagesTugas Pengantar Akuntansi - Timotius Siagian 1 C3Timotius SiagianNo ratings yet

- Budget Pipe Rack New Tank OleoDocument28 pagesBudget Pipe Rack New Tank OleokamprettelanjangNo ratings yet

- Maxime Project ReportDocument60 pagesMaxime Project ReportMOHD GULZARNo ratings yet

- Quotation For 05 KW OFF GRID:: Quotation Date: 18 May, 2021 Unit Price (RS.) Quantity Total Cost (RS.)Document2 pagesQuotation For 05 KW OFF GRID:: Quotation Date: 18 May, 2021 Unit Price (RS.) Quantity Total Cost (RS.)ImranFazal100% (1)

- Wote Technical Training InstituteDocument1 pageWote Technical Training Institutemambopeter123No ratings yet

- BA 205 AnswerDocument5 pagesBA 205 AnswerAnhar Polo CanacanNo ratings yet

- HH221434 HH221410 B TaperedRollerBearings TSF (TaperedSinglewithFlange) Imperial PDFDocument5 pagesHH221434 HH221410 B TaperedRollerBearings TSF (TaperedSinglewithFlange) Imperial PDFjcojedar2009No ratings yet

- 460-ST-Q PT. Artajaya Langgengsentosa - EJF - 1Document1 page460-ST-Q PT. Artajaya Langgengsentosa - EJF - 1Nia WullandariNo ratings yet

- Financials - Dhobhi BhaiyaDocument9 pagesFinancials - Dhobhi Bhaiyaprince joshiNo ratings yet

- Financial Work ScheduleDocument1 pageFinancial Work ScheduleSisay chaneNo ratings yet

- Q-19 - 01-005 - MKE - R3 - Instalasi of Vertical Pump IP (Foundation Reducer Modification)Document2 pagesQ-19 - 01-005 - MKE - R3 - Instalasi of Vertical Pump IP (Foundation Reducer Modification)Suprayitno SupraNo ratings yet

- 790 Repair Chiller No. 1Document1 page790 Repair Chiller No. 1Rangga NoparaNo ratings yet

- Ragama OpticalDocument1 pageRagama Optical5hy7pyqhdbNo ratings yet

- Hydrant System OfferDocument5 pagesHydrant System OfferMd. Sujaur RahmanNo ratings yet

- Hydrant System OfferDocument5 pagesHydrant System OfferMd. Sujaur RahmanNo ratings yet

- Financial Model For BrandsDocument60 pagesFinancial Model For BrandsAnjali SrivastavaNo ratings yet

- Profit & Loss Accounts: Wing Chair GirogioDocument3 pagesProfit & Loss Accounts: Wing Chair Girogiofarsi786No ratings yet

- TATA KRISHNA LabourDocument13 pagesTATA KRISHNA LabourSUPRIYA NANDINo ratings yet

- Template de Mo Company Balance Sheet BudgetDocument2 pagesTemplate de Mo Company Balance Sheet BudgetDuta Hotel Group100% (1)

- Sample Budget Worksheet - Care and Shelter ComponentsDocument1 pageSample Budget Worksheet - Care and Shelter Componentsyourxmen2910No ratings yet

- Quotation S00345Document1 pageQuotation S00345Muhammad Tanvir MohsinNo ratings yet

- Acc106 Assignment 2 Tie Beauty Enterprise FinalDocument15 pagesAcc106 Assignment 2 Tie Beauty Enterprise Finalnur anisNo ratings yet

- By Pass Valve BifurcationDocument5 pagesBy Pass Valve BifurcationSarthak EnterprisesNo ratings yet

- Financial StatementsDocument10 pagesFinancial Statementsassg USMNo ratings yet

- S.No Description Qty Rate (RS.) Amount (RS.) RXQ12ARY6 - Daikin VRV X 12HP ODU Cooling OnlyDocument10 pagesS.No Description Qty Rate (RS.) Amount (RS.) RXQ12ARY6 - Daikin VRV X 12HP ODU Cooling Onlysenthil kumarNo ratings yet

- Fire 3Document2 pagesFire 3Kanaklata Civil Hospital SonitpurNo ratings yet

- 80 HP Kishore Pump Estimate, 88345Document1 page80 HP Kishore Pump Estimate, 88345aakashgupta viaanshNo ratings yet

- Confidence Power Holdings LTD: Stock Summary AllDocument3 pagesConfidence Power Holdings LTD: Stock Summary AllAshik RahmanNo ratings yet

- Job Information: CCK Engineering & Construction Co.,Ltd. 1Document90 pagesJob Information: CCK Engineering & Construction Co.,Ltd. 1Kriengsak RuangdechNo ratings yet

- Shield Project Summary Phased BudgetDocument1 pageShield Project Summary Phased BudgetBinay BhandariNo ratings yet

- Budget Proposal: Optic Fibres and TowrsDocument5 pagesBudget Proposal: Optic Fibres and TowrsrjiveNo ratings yet

- Cash Flow Projection of MCV: SQM SQM RP.M/SQM RP.M/SQM SQM SQM RP.M US$. Tho Rp. MDocument26 pagesCash Flow Projection of MCV: SQM SQM RP.M/SQM RP.M/SQM SQM SQM RP.M US$. Tho Rp. Mangg4interNo ratings yet

- Appendix CDocument6 pagesAppendix CPat SulaimanNo ratings yet

- Stock Without ValueDocument57 pagesStock Without ValueAsian Techno Traders Pvt.Ltd. (Asian Staff)No ratings yet

- Tata Motors PresentationDocument121 pagesTata Motors PresentationSrikanth Reddy VemulaNo ratings yet

- Group 2 Business PlanDocument15 pagesGroup 2 Business PlanJam ReformaNo ratings yet

- Part Number 6311-Z-NR-C3, Deep Groove Ball Bearings (6000, 6200, 6300, 6400)Document3 pagesPart Number 6311-Z-NR-C3, Deep Groove Ball Bearings (6000, 6200, 6300, 6400)Travis DavisNo ratings yet

- Bapak Kevin 6963.2Document1 pageBapak Kevin 6963.2whatsup arwanNo ratings yet

- Jinkosolar Holding Co., LTD.: Q3 2017 Earnings Call PresentationDocument10 pagesJinkosolar Holding Co., LTD.: Q3 2017 Earnings Call PresentationAshutosh KumarNo ratings yet

- Overhead ApportionmentDocument3 pagesOverhead ApportionmentHassanAbsarQaimkhaniNo ratings yet

- Repair Chiller No. 2Document1 pageRepair Chiller No. 2Rangga NoparaNo ratings yet

- AssignmentDocument4 pagesAssignmentMenna MohamedNo ratings yet

- Delivery Note-Number Painting KafdDocument5 pagesDelivery Note-Number Painting KafdAbdul samee MianNo ratings yet

- Fees Structure of Top 4 NitDocument4 pagesFees Structure of Top 4 Nitsujeet kumarNo ratings yet

- Flexible BudgetDocument4 pagesFlexible BudgetSeli Fitria Rahma DiantikaNo ratings yet

- Final DPRDocument10 pagesFinal DPRGateway ComputersNo ratings yet

- Pt. Engineering Indonesia: Mvl'.ADocument4 pagesPt. Engineering Indonesia: Mvl'.AYudhi HerwantoNo ratings yet

- WorkshitDocument12 pagesWorkshitLukman ArimartaNo ratings yet

- 46KWp - Fincera DHA LahoreDocument3 pages46KWp - Fincera DHA Lahoretaibamalik457No ratings yet

- Engineering Service Revenues World Summary: Market Values & Financials by CountryFrom EverandEngineering Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Speed Changers, Drives & Gears World Summary: Market Values & Financials by CountryFrom EverandSpeed Changers, Drives & Gears World Summary: Market Values & Financials by CountryNo ratings yet

- ServitisationDocument32 pagesServitisation256850100% (1)

- Ibm Gatt and WtoDocument14 pagesIbm Gatt and Wto6038 Mugilan kNo ratings yet

- Commonwealth Bank StatementDocument5 pagesCommonwealth Bank StatementKate YehNo ratings yet

- Transcript Teleconference Financial Results Q1 2023Document16 pagesTranscript Teleconference Financial Results Q1 2023Cirlea CatalinNo ratings yet

- ICAB Advance Level Strategic Business Management Compilation of Chapterwise Theory For Exam May June 2020Document459 pagesICAB Advance Level Strategic Business Management Compilation of Chapterwise Theory For Exam May June 2020Optimal Management Solution100% (1)

- Ifii LK TW Iii 2022Document76 pagesIfii LK TW Iii 2022Sourav DuttaNo ratings yet

- Solved The Outstanding Stock in Red Blue and Green Corporations EachDocument1 pageSolved The Outstanding Stock in Red Blue and Green Corporations EachAnbu jaromiaNo ratings yet

- Soumil Final Project PDFDocument56 pagesSoumil Final Project PDFSoumil SoganiNo ratings yet

- Puccio Erbahar 2016Document26 pagesPuccio Erbahar 2016Vatsla BhatiaNo ratings yet

- Ch04 Strategic Planning Human Resource Planning and Job AnalysisDocument74 pagesCh04 Strategic Planning Human Resource Planning and Job AnalysisMohammedNo ratings yet

- Zinger Electronics, INC.: by Group 11 Marketing D'Document5 pagesZinger Electronics, INC.: by Group 11 Marketing D'jasmirsinghNo ratings yet

- 4303177Document6 pages4303177mohitgaba19No ratings yet

- Expected para Jumbles Questions PDF For SSC Tier II ExamsDocument44 pagesExpected para Jumbles Questions PDF For SSC Tier II Examsbijoyp348No ratings yet

- Case Study RubricDocument4 pagesCase Study RubricBrijendra SinghNo ratings yet

- Economics 2015: Sāmoa School CertificateDocument26 pagesEconomics 2015: Sāmoa School CertificatemonyNo ratings yet

- Dissertation On T&P of M&M Ltd.Document49 pagesDissertation On T&P of M&M Ltd.sampada_naradNo ratings yet

- Sap Business Bydesign Customer Relationship Management: OpensapDocument28 pagesSap Business Bydesign Customer Relationship Management: OpensapGaurab BanerjiNo ratings yet

- Accounting For DiscountsDocument2 pagesAccounting For DiscountsYamateNo ratings yet

- Innovación de Ciclo RapidoDocument10 pagesInnovación de Ciclo RapidoJuan David Ramirez SalazarNo ratings yet

- Updated Arrears Estimator Clerical StaffDocument8 pagesUpdated Arrears Estimator Clerical Staffkmuraleedharan09No ratings yet

- International Business Law and Its Environment 9th Edition Schaffer Solutions Manual DownloadDocument8 pagesInternational Business Law and Its Environment 9th Edition Schaffer Solutions Manual DownloadJohn Stewart100% (17)

- Chapter 2Document4 pagesChapter 2Roselie Cuenca94% (16)

- Commission Agreement - (GCC-Power Plant)Document2 pagesCommission Agreement - (GCC-Power Plant)Jonalyn TellesNo ratings yet

- Aluminum PorterDocument2 pagesAluminum PorterAmir ShameemNo ratings yet

- The Grat DreprestionDocument29 pagesThe Grat DreprestionAwura KwayowaaNo ratings yet

- Return On SalesDocument2 pagesReturn On SalesMa Terresa TejadaNo ratings yet

- BEC Vantage PG 8Document1 pageBEC Vantage PG 8juanNo ratings yet