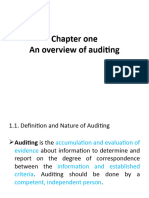

UNIT 1 Auditing

UNIT 1 Auditing

You might also like

- COMPANY Asset Handover FormDocument1 pageCOMPANY Asset Handover FormOluwatomisin Sotubo100% (3)

- AuditingDocument27 pagesAuditingaazamchNo ratings yet

- Magill - 1983 07 01Document49 pagesMagill - 1983 07 01Malachy BrowneNo ratings yet

- UNIT 1 AuditingDocument4 pagesUNIT 1 Auditingzelalem kebedeNo ratings yet

- UNIT 1 AuditingDocument3 pagesUNIT 1 AuditingKhalid MuhammadNo ratings yet

- Audit I CH IDocument4 pagesAudit I CH IAhmedNo ratings yet

- Chapter 1Document6 pagesChapter 1dejen mengstieNo ratings yet

- Auditing Principles and PrinciplesDocument17 pagesAuditing Principles and Principlesmelkamuaemiro1No ratings yet

- Audit Two AaaDocument84 pagesAudit Two AaaYonasNo ratings yet

- Audit IIDocument85 pagesAudit IISamuel DebebeNo ratings yet

- Audit I CHAPTER 2Document38 pagesAudit I CHAPTER 2Samuel GirmaNo ratings yet

- Auditing Principles and Practice I Unit 1&2Document14 pagesAuditing Principles and Practice I Unit 1&2ALEM LEMMANo ratings yet

- Auditing 1 Chaper 1-4Document23 pagesAuditing 1 Chaper 1-4oliifan HundeNo ratings yet

- Chapter 1 Overview of AuditingDocument28 pagesChapter 1 Overview of AuditingTesfaye Desalegn100% (1)

- Mid Term Exam-Auditing IDocument5 pagesMid Term Exam-Auditing IAmara PrabasariNo ratings yet

- Auditing Chapter 1Document12 pagesAuditing Chapter 1JewelNo ratings yet

- Audit IIDocument77 pagesAudit II፩ne LoveNo ratings yet

- Auditing & Taxation (Chapter 1)Document9 pagesAuditing & Taxation (Chapter 1)ponyking86No ratings yet

- Principles and Practice of AuditingDocument55 pagesPrinciples and Practice of Auditingdanucandy2No ratings yet

- AUDITING one 2015 √√√√√√√√√√√√πππππDocument41 pagesAUDITING one 2015 √√√√√√√√√√√√πππππoliifan HundeNo ratings yet

- Audit Term PaperDocument39 pagesAudit Term Papersamuel kebedeNo ratings yet

- Audit Techniques and ProceduresDocument119 pagesAudit Techniques and Procedures04beingsammyNo ratings yet

- Auditing Principle I - CH 1Document6 pagesAuditing Principle I - CH 1keyruebrahim44No ratings yet

- AuditingTheory SW1Document2 pagesAuditingTheory SW1Ara AlcantaraNo ratings yet

- 1 The Nature, Purpose and Scope of AuditingDocument12 pages1 The Nature, Purpose and Scope of Auditingyebegashet100% (2)

- Name: Jalaica B. Rico Course & Year: BSA - 3 Instruction: Please Answer The Following Questions. Just Click The Reply Button and Type Your AnswerDocument2 pagesName: Jalaica B. Rico Course & Year: BSA - 3 Instruction: Please Answer The Following Questions. Just Click The Reply Button and Type Your AnswerRico, Jalaica B.No ratings yet

- Introduction To Auditing: 1.1 DefinitionDocument14 pagesIntroduction To Auditing: 1.1 Definitionmokhtar mohaNo ratings yet

- Audit ProjectDocument23 pagesAudit ProjectPriyanka KhotNo ratings yet

- Differences Between Auditing and Accounting: 1. MeaningDocument8 pagesDifferences Between Auditing and Accounting: 1. MeaningJemson YandugNo ratings yet

- AuditingDocument8 pagesAuditingIniya AnandNo ratings yet

- PRINCIPLES OF AUDITING by Ricardo VillanuevaDocument42 pagesPRINCIPLES OF AUDITING by Ricardo Villanuevarivi.villanueva.sjcNo ratings yet

- My ReportDocument5 pagesMy ReportZaber ChowdhuryNo ratings yet

- UNIT-2 Audit and Audit Procedure Audit EvidenceDocument12 pagesUNIT-2 Audit and Audit Procedure Audit EvidenceLohith Kumar SNo ratings yet

- Mid-Term Exam - IA - Ashilla Nadiya Amany - 2002030013Document7 pagesMid-Term Exam - IA - Ashilla Nadiya Amany - 2002030013Ashilla Nadya AmanyNo ratings yet

- Auditing CH 1Document20 pagesAuditing CH 1Nigussie BerhanuNo ratings yet

- AUDITING one 2015 √√√√√√√√√√√√πππππDocument13 pagesAUDITING one 2015 √√√√√√√√√√√√πππππoliifan HundeNo ratings yet

- Responsibilities of AuditorsDocument3 pagesResponsibilities of AuditorsGandreti JagadeeshNo ratings yet

- Auditing PresentationDocument54 pagesAuditing PresentationMuzaFarNo ratings yet

- IntenshipDocument38 pagesIntenshiplovely siva100% (1)

- Soundarya WordDocument73 pagesSoundarya WordFranklin RjamesNo ratings yet

- Auditing-Principles-And-Practices-I Handout BestDocument34 pagesAuditing-Principles-And-Practices-I Handout Besttarekegn gezahegnNo ratings yet

- Audit I-Chapter OneDocument7 pagesAudit I-Chapter Onethedalesh weldeNo ratings yet

- Unit - 1 Introduction To AuditingDocument10 pagesUnit - 1 Introduction To AuditingDarshan PanditNo ratings yet

- @audit CW1Document8 pages@audit CW1bujernest7No ratings yet

- Auditing Unit 1Document34 pagesAuditing Unit 1ShaifaliChauhanNo ratings yet

- Research Report 2020Document67 pagesResearch Report 2020RUPAM SINGHNo ratings yet

- AUDITING 2013 Best .Docx..bakDocument34 pagesAUDITING 2013 Best .Docx..bakoliifan HundeNo ratings yet

- Auditing & Assurance Principles-Lesson 1Document12 pagesAuditing & Assurance Principles-Lesson 1Joe P PokaranNo ratings yet

- The Role of Auditors With Their Clients and Third PartiesDocument45 pagesThe Role of Auditors With Their Clients and Third PartiesInamul HaqueNo ratings yet

- 7.0 Topic 7 Public Sector Auditing 7.1 S PDFDocument17 pages7.0 Topic 7 Public Sector Auditing 7.1 S PDFhezronNo ratings yet

- Internal AuditDocument5 pagesInternal Auditnehagupta4915No ratings yet

- AUDITING PRINCIPLES I - NotesDocument69 pagesAUDITING PRINCIPLES I - Notesyebegashet100% (1)

- Chapter No:-1 1.1: Introduction of Audit: Stakeholders Material Legal PersonDocument31 pagesChapter No:-1 1.1: Introduction of Audit: Stakeholders Material Legal PersonmadhuriNo ratings yet

- Classification of AuditDocument24 pagesClassification of AuditFazal MohammadNo ratings yet

- Auditing Resbonsibilities and Objectives: Research Title: Subject: Auditing Course Professor: Bahaa El-Kady &Document18 pagesAuditing Resbonsibilities and Objectives: Research Title: Subject: Auditing Course Professor: Bahaa El-Kady &Mohamed AbdulazizNo ratings yet

- Auditing Resbonsibilities and Objectives: Research Title: Subject: Auditing Course Professor: Bahaa El-Kady &Document18 pagesAuditing Resbonsibilities and Objectives: Research Title: Subject: Auditing Course Professor: Bahaa El-Kady &Mohamed AbdulazizNo ratings yet

- Revision Notes: Auditing and Investigations Audit ObjectivesDocument51 pagesRevision Notes: Auditing and Investigations Audit ObjectivesGeraldwerreNo ratings yet

- Course: Auditing (481) Semester: Spring 2021 Assignment No.1 Q. 1 Define Auditing and Describe Its Various Techniques? AnswerDocument20 pagesCourse: Auditing (481) Semester: Spring 2021 Assignment No.1 Q. 1 Define Auditing and Describe Its Various Techniques? Answergemixon120No ratings yet

- Chapter One Audit IDocument41 pagesChapter One Audit ISalih AkadarNo ratings yet

- Principles of Auditing FinishedDocument85 pagesPrinciples of Auditing FinishedDeepan KumarNo ratings yet

- Topic 1 INTRO TO AUDITING - 211114 - 152450Document7 pagesTopic 1 INTRO TO AUDITING - 211114 - 152450Mirajii OlomiiNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- ዘምዘምDocument4 pagesዘምዘምprimhaile assefaNo ratings yet

- Docker Course ProfileDocument7 pagesDocker Course Profileprimhaile assefaNo ratings yet

- Hailemichael CVDocument2 pagesHailemichael CVprimhaile assefaNo ratings yet

- G9 Chemistry TG 2023 Web 38 75Document50 pagesG9 Chemistry TG 2023 Web 38 75primhaile assefaNo ratings yet

- Hawassa District Bank Trainee Exam ResultDocument45 pagesHawassa District Bank Trainee Exam Resultprimhaile assefaNo ratings yet

- Dessie District Bank Trainee Exam ResultDocument39 pagesDessie District Bank Trainee Exam Resultprimhaile assefaNo ratings yet

- HNS COC Level 4 Practice Exam Full Package NewDocument8 pagesHNS COC Level 4 Practice Exam Full Package Newprimhaile assefa100% (2)

- Chapter 2Document14 pagesChapter 2primhaile assefaNo ratings yet

- A.A Bank Trainee 2022 Exam ResultDocument102 pagesA.A Bank Trainee 2022 Exam Resultprimhaile assefaNo ratings yet

- Jimma District - Bank Trainee Exam ResultDocument21 pagesJimma District - Bank Trainee Exam Resultprimhaile assefaNo ratings yet

- Mentenance Chapter 3Document10 pagesMentenance Chapter 3primhaile assefaNo ratings yet

- Mussie BaDocument11 pagesMussie Baprimhaile assefaNo ratings yet

- Chap 2Document31 pagesChap 2primhaile assefaNo ratings yet

- Financial Management 3RD Degree AcctnDocument154 pagesFinancial Management 3RD Degree Acctnprimhaile assefaNo ratings yet

- To: Merqconsultancy PLC: Application For Qualitative and Quantitative DatacollectorDocument3 pagesTo: Merqconsultancy PLC: Application For Qualitative and Quantitative Datacollectorprimhaile assefaNo ratings yet

- Entrepreneurship and Small Business Management For Year III, Horticulture Students, 2020/21Document225 pagesEntrepreneurship and Small Business Management For Year III, Horticulture Students, 2020/21primhaile assefaNo ratings yet

- 2nd Week Exam ScheduleDocument1 page2nd Week Exam Scheduleprimhaile assefaNo ratings yet

- DesDocument21 pagesDesprimhaile assefaNo ratings yet

- Huawei QuestionDocument60 pagesHuawei Questionprimhaile assefaNo ratings yet

- Aristotle PDFDocument6 pagesAristotle PDFAnonymous p5jZCn100% (1)

- CH 12Document39 pagesCH 12Eric YaoNo ratings yet

- GST India - TDS Solution - SAP - SD - FIDocument13 pagesGST India - TDS Solution - SAP - SD - FISachin BhalekarNo ratings yet

- CH 1 - Introduction To Financial ManagementDocument18 pagesCH 1 - Introduction To Financial Managementmaheshbendigeri5945No ratings yet

- CIR Vs AlgueDocument1 pageCIR Vs AlgueLouie SalladorNo ratings yet

- Acct Statement - XX6222 - 02062023Document2 pagesAcct Statement - XX6222 - 02062023Yaman KaswanNo ratings yet

- PG-QP - 02: Q. B. No.Document16 pagesPG-QP - 02: Q. B. No.Vamsi KrishnaNo ratings yet

- Mt-Ii Final AssignmentDocument4 pagesMt-Ii Final Assignmentapi-269508649No ratings yet

- Constitution Notes: You Will Be Writing Questions at Home Tonight. There Are 14 Slides of Information To Take Notes OnDocument16 pagesConstitution Notes: You Will Be Writing Questions at Home Tonight. There Are 14 Slides of Information To Take Notes OnIuzi ValentinNo ratings yet

- Jackson 1.4 Homework Problem SolutionDocument4 pagesJackson 1.4 Homework Problem SolutionJhonNo ratings yet

- From: United States CorporationDocument5 pagesFrom: United States CorporationLeo M100% (2)

- Lib JpegDocument3 pagesLib JpegMomoNo ratings yet

- IALEIA Certification 2013Document15 pagesIALEIA Certification 2013Christian MousseauNo ratings yet

- El Cóndor Pasa: Daniel Alomía Robles / TraditionalDocument1 pageEl Cóndor Pasa: Daniel Alomía Robles / TraditionalJames Wilfrido Cardenas AmezquitaNo ratings yet

- FBWDocument4 pagesFBWS SrikantNo ratings yet

- Nift&swiftpptxDocument37 pagesNift&swiftpptxSamia YounasNo ratings yet

- LEOUEL SANTOS, Petitioner Vs COURT OF APPEALS, DefendantDocument2 pagesLEOUEL SANTOS, Petitioner Vs COURT OF APPEALS, Defendantprince pacasumNo ratings yet

- Foreclosure Defense Strategy 10-4-09Document6 pagesForeclosure Defense Strategy 10-4-09YourEminenceNo ratings yet

- Accounting Standards in The East Asia Region: By: M. Zubaidur RahmanDocument16 pagesAccounting Standards in The East Asia Region: By: M. Zubaidur Rahmanemerson deasisNo ratings yet

- PDF High Performance Boards Improving and Energizing Your Governance 1St Edition Cossin Ebook Full ChapterDocument53 pagesPDF High Performance Boards Improving and Energizing Your Governance 1St Edition Cossin Ebook Full Chapterdebbie.mitchell437100% (2)

- Benjamin C. Santos and Estrella, Remitio & Associates For Petitioner. Rodolfo V. Gumban For Private RespondentDocument5 pagesBenjamin C. Santos and Estrella, Remitio & Associates For Petitioner. Rodolfo V. Gumban For Private RespondentLouisa FerrarenNo ratings yet

- (Name of The Association)Document4 pages(Name of The Association)ChanChi Domocmat LaresNo ratings yet

- AJmera Cement ProjectDocument60 pagesAJmera Cement ProjectHiren ChauhanNo ratings yet

- MCQ Midterms in Land Titles - 2020 - Answer KeyDocument21 pagesMCQ Midterms in Land Titles - 2020 - Answer KeyAr-Reb AquinoNo ratings yet

- The Role of The Wife in IslamDocument2 pagesThe Role of The Wife in IslamShadab AnjumNo ratings yet

- SOP For Procedure of PurchasingDocument2 pagesSOP For Procedure of PurchasingtridentindiacompanyNo ratings yet

- Anti Plunder ActDocument3 pagesAnti Plunder ActmeriiNo ratings yet

- Kinds of Cheques: Cabigting, Maria Queenie Lilirae Purzuelo, DanielleDocument51 pagesKinds of Cheques: Cabigting, Maria Queenie Lilirae Purzuelo, DanielleRae De CastroNo ratings yet

Download as docx, pdf, or txt

You might also like

- COMPANY Asset Handover FormDocument1 pageCOMPANY Asset Handover FormOluwatomisin Sotubo100% (3)

- AuditingDocument27 pagesAuditingaazamchNo ratings yet

- Magill - 1983 07 01Document49 pagesMagill - 1983 07 01Malachy BrowneNo ratings yet

- UNIT 1 AuditingDocument4 pagesUNIT 1 Auditingzelalem kebedeNo ratings yet

- UNIT 1 AuditingDocument3 pagesUNIT 1 AuditingKhalid MuhammadNo ratings yet

- Audit I CH IDocument4 pagesAudit I CH IAhmedNo ratings yet

- Chapter 1Document6 pagesChapter 1dejen mengstieNo ratings yet

- Auditing Principles and PrinciplesDocument17 pagesAuditing Principles and Principlesmelkamuaemiro1No ratings yet

- Audit Two AaaDocument84 pagesAudit Two AaaYonasNo ratings yet

- Audit IIDocument85 pagesAudit IISamuel DebebeNo ratings yet

- Audit I CHAPTER 2Document38 pagesAudit I CHAPTER 2Samuel GirmaNo ratings yet

- Auditing Principles and Practice I Unit 1&2Document14 pagesAuditing Principles and Practice I Unit 1&2ALEM LEMMANo ratings yet

- Auditing 1 Chaper 1-4Document23 pagesAuditing 1 Chaper 1-4oliifan HundeNo ratings yet

- Chapter 1 Overview of AuditingDocument28 pagesChapter 1 Overview of AuditingTesfaye Desalegn100% (1)

- Mid Term Exam-Auditing IDocument5 pagesMid Term Exam-Auditing IAmara PrabasariNo ratings yet

- Auditing Chapter 1Document12 pagesAuditing Chapter 1JewelNo ratings yet

- Audit IIDocument77 pagesAudit II፩ne LoveNo ratings yet

- Auditing & Taxation (Chapter 1)Document9 pagesAuditing & Taxation (Chapter 1)ponyking86No ratings yet

- Principles and Practice of AuditingDocument55 pagesPrinciples and Practice of Auditingdanucandy2No ratings yet

- AUDITING one 2015 √√√√√√√√√√√√πππππDocument41 pagesAUDITING one 2015 √√√√√√√√√√√√πππππoliifan HundeNo ratings yet

- Audit Term PaperDocument39 pagesAudit Term Papersamuel kebedeNo ratings yet

- Audit Techniques and ProceduresDocument119 pagesAudit Techniques and Procedures04beingsammyNo ratings yet

- Auditing Principle I - CH 1Document6 pagesAuditing Principle I - CH 1keyruebrahim44No ratings yet

- AuditingTheory SW1Document2 pagesAuditingTheory SW1Ara AlcantaraNo ratings yet

- 1 The Nature, Purpose and Scope of AuditingDocument12 pages1 The Nature, Purpose and Scope of Auditingyebegashet100% (2)

- Name: Jalaica B. Rico Course & Year: BSA - 3 Instruction: Please Answer The Following Questions. Just Click The Reply Button and Type Your AnswerDocument2 pagesName: Jalaica B. Rico Course & Year: BSA - 3 Instruction: Please Answer The Following Questions. Just Click The Reply Button and Type Your AnswerRico, Jalaica B.No ratings yet

- Introduction To Auditing: 1.1 DefinitionDocument14 pagesIntroduction To Auditing: 1.1 Definitionmokhtar mohaNo ratings yet

- Audit ProjectDocument23 pagesAudit ProjectPriyanka KhotNo ratings yet

- Differences Between Auditing and Accounting: 1. MeaningDocument8 pagesDifferences Between Auditing and Accounting: 1. MeaningJemson YandugNo ratings yet

- AuditingDocument8 pagesAuditingIniya AnandNo ratings yet

- PRINCIPLES OF AUDITING by Ricardo VillanuevaDocument42 pagesPRINCIPLES OF AUDITING by Ricardo Villanuevarivi.villanueva.sjcNo ratings yet

- My ReportDocument5 pagesMy ReportZaber ChowdhuryNo ratings yet

- UNIT-2 Audit and Audit Procedure Audit EvidenceDocument12 pagesUNIT-2 Audit and Audit Procedure Audit EvidenceLohith Kumar SNo ratings yet

- Mid-Term Exam - IA - Ashilla Nadiya Amany - 2002030013Document7 pagesMid-Term Exam - IA - Ashilla Nadiya Amany - 2002030013Ashilla Nadya AmanyNo ratings yet

- Auditing CH 1Document20 pagesAuditing CH 1Nigussie BerhanuNo ratings yet

- AUDITING one 2015 √√√√√√√√√√√√πππππDocument13 pagesAUDITING one 2015 √√√√√√√√√√√√πππππoliifan HundeNo ratings yet

- Responsibilities of AuditorsDocument3 pagesResponsibilities of AuditorsGandreti JagadeeshNo ratings yet

- Auditing PresentationDocument54 pagesAuditing PresentationMuzaFarNo ratings yet

- IntenshipDocument38 pagesIntenshiplovely siva100% (1)

- Soundarya WordDocument73 pagesSoundarya WordFranklin RjamesNo ratings yet

- Auditing-Principles-And-Practices-I Handout BestDocument34 pagesAuditing-Principles-And-Practices-I Handout Besttarekegn gezahegnNo ratings yet

- Audit I-Chapter OneDocument7 pagesAudit I-Chapter Onethedalesh weldeNo ratings yet

- Unit - 1 Introduction To AuditingDocument10 pagesUnit - 1 Introduction To AuditingDarshan PanditNo ratings yet

- @audit CW1Document8 pages@audit CW1bujernest7No ratings yet

- Auditing Unit 1Document34 pagesAuditing Unit 1ShaifaliChauhanNo ratings yet

- Research Report 2020Document67 pagesResearch Report 2020RUPAM SINGHNo ratings yet

- AUDITING 2013 Best .Docx..bakDocument34 pagesAUDITING 2013 Best .Docx..bakoliifan HundeNo ratings yet

- Auditing & Assurance Principles-Lesson 1Document12 pagesAuditing & Assurance Principles-Lesson 1Joe P PokaranNo ratings yet

- The Role of Auditors With Their Clients and Third PartiesDocument45 pagesThe Role of Auditors With Their Clients and Third PartiesInamul HaqueNo ratings yet

- 7.0 Topic 7 Public Sector Auditing 7.1 S PDFDocument17 pages7.0 Topic 7 Public Sector Auditing 7.1 S PDFhezronNo ratings yet

- Internal AuditDocument5 pagesInternal Auditnehagupta4915No ratings yet

- AUDITING PRINCIPLES I - NotesDocument69 pagesAUDITING PRINCIPLES I - Notesyebegashet100% (1)

- Chapter No:-1 1.1: Introduction of Audit: Stakeholders Material Legal PersonDocument31 pagesChapter No:-1 1.1: Introduction of Audit: Stakeholders Material Legal PersonmadhuriNo ratings yet

- Classification of AuditDocument24 pagesClassification of AuditFazal MohammadNo ratings yet

- Auditing Resbonsibilities and Objectives: Research Title: Subject: Auditing Course Professor: Bahaa El-Kady &Document18 pagesAuditing Resbonsibilities and Objectives: Research Title: Subject: Auditing Course Professor: Bahaa El-Kady &Mohamed AbdulazizNo ratings yet

- Auditing Resbonsibilities and Objectives: Research Title: Subject: Auditing Course Professor: Bahaa El-Kady &Document18 pagesAuditing Resbonsibilities and Objectives: Research Title: Subject: Auditing Course Professor: Bahaa El-Kady &Mohamed AbdulazizNo ratings yet

- Revision Notes: Auditing and Investigations Audit ObjectivesDocument51 pagesRevision Notes: Auditing and Investigations Audit ObjectivesGeraldwerreNo ratings yet

- Course: Auditing (481) Semester: Spring 2021 Assignment No.1 Q. 1 Define Auditing and Describe Its Various Techniques? AnswerDocument20 pagesCourse: Auditing (481) Semester: Spring 2021 Assignment No.1 Q. 1 Define Auditing and Describe Its Various Techniques? Answergemixon120No ratings yet

- Chapter One Audit IDocument41 pagesChapter One Audit ISalih AkadarNo ratings yet

- Principles of Auditing FinishedDocument85 pagesPrinciples of Auditing FinishedDeepan KumarNo ratings yet

- Topic 1 INTRO TO AUDITING - 211114 - 152450Document7 pagesTopic 1 INTRO TO AUDITING - 211114 - 152450Mirajii OlomiiNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- ዘምዘምDocument4 pagesዘምዘምprimhaile assefaNo ratings yet

- Docker Course ProfileDocument7 pagesDocker Course Profileprimhaile assefaNo ratings yet

- Hailemichael CVDocument2 pagesHailemichael CVprimhaile assefaNo ratings yet

- G9 Chemistry TG 2023 Web 38 75Document50 pagesG9 Chemistry TG 2023 Web 38 75primhaile assefaNo ratings yet

- Hawassa District Bank Trainee Exam ResultDocument45 pagesHawassa District Bank Trainee Exam Resultprimhaile assefaNo ratings yet

- Dessie District Bank Trainee Exam ResultDocument39 pagesDessie District Bank Trainee Exam Resultprimhaile assefaNo ratings yet

- HNS COC Level 4 Practice Exam Full Package NewDocument8 pagesHNS COC Level 4 Practice Exam Full Package Newprimhaile assefa100% (2)

- Chapter 2Document14 pagesChapter 2primhaile assefaNo ratings yet

- A.A Bank Trainee 2022 Exam ResultDocument102 pagesA.A Bank Trainee 2022 Exam Resultprimhaile assefaNo ratings yet

- Jimma District - Bank Trainee Exam ResultDocument21 pagesJimma District - Bank Trainee Exam Resultprimhaile assefaNo ratings yet

- Mentenance Chapter 3Document10 pagesMentenance Chapter 3primhaile assefaNo ratings yet

- Mussie BaDocument11 pagesMussie Baprimhaile assefaNo ratings yet

- Chap 2Document31 pagesChap 2primhaile assefaNo ratings yet

- Financial Management 3RD Degree AcctnDocument154 pagesFinancial Management 3RD Degree Acctnprimhaile assefaNo ratings yet

- To: Merqconsultancy PLC: Application For Qualitative and Quantitative DatacollectorDocument3 pagesTo: Merqconsultancy PLC: Application For Qualitative and Quantitative Datacollectorprimhaile assefaNo ratings yet

- Entrepreneurship and Small Business Management For Year III, Horticulture Students, 2020/21Document225 pagesEntrepreneurship and Small Business Management For Year III, Horticulture Students, 2020/21primhaile assefaNo ratings yet

- 2nd Week Exam ScheduleDocument1 page2nd Week Exam Scheduleprimhaile assefaNo ratings yet

- DesDocument21 pagesDesprimhaile assefaNo ratings yet

- Huawei QuestionDocument60 pagesHuawei Questionprimhaile assefaNo ratings yet

- Aristotle PDFDocument6 pagesAristotle PDFAnonymous p5jZCn100% (1)

- CH 12Document39 pagesCH 12Eric YaoNo ratings yet

- GST India - TDS Solution - SAP - SD - FIDocument13 pagesGST India - TDS Solution - SAP - SD - FISachin BhalekarNo ratings yet

- CH 1 - Introduction To Financial ManagementDocument18 pagesCH 1 - Introduction To Financial Managementmaheshbendigeri5945No ratings yet

- CIR Vs AlgueDocument1 pageCIR Vs AlgueLouie SalladorNo ratings yet

- Acct Statement - XX6222 - 02062023Document2 pagesAcct Statement - XX6222 - 02062023Yaman KaswanNo ratings yet

- PG-QP - 02: Q. B. No.Document16 pagesPG-QP - 02: Q. B. No.Vamsi KrishnaNo ratings yet

- Mt-Ii Final AssignmentDocument4 pagesMt-Ii Final Assignmentapi-269508649No ratings yet

- Constitution Notes: You Will Be Writing Questions at Home Tonight. There Are 14 Slides of Information To Take Notes OnDocument16 pagesConstitution Notes: You Will Be Writing Questions at Home Tonight. There Are 14 Slides of Information To Take Notes OnIuzi ValentinNo ratings yet

- Jackson 1.4 Homework Problem SolutionDocument4 pagesJackson 1.4 Homework Problem SolutionJhonNo ratings yet

- From: United States CorporationDocument5 pagesFrom: United States CorporationLeo M100% (2)

- Lib JpegDocument3 pagesLib JpegMomoNo ratings yet

- IALEIA Certification 2013Document15 pagesIALEIA Certification 2013Christian MousseauNo ratings yet

- El Cóndor Pasa: Daniel Alomía Robles / TraditionalDocument1 pageEl Cóndor Pasa: Daniel Alomía Robles / TraditionalJames Wilfrido Cardenas AmezquitaNo ratings yet

- FBWDocument4 pagesFBWS SrikantNo ratings yet

- Nift&swiftpptxDocument37 pagesNift&swiftpptxSamia YounasNo ratings yet

- LEOUEL SANTOS, Petitioner Vs COURT OF APPEALS, DefendantDocument2 pagesLEOUEL SANTOS, Petitioner Vs COURT OF APPEALS, Defendantprince pacasumNo ratings yet

- Foreclosure Defense Strategy 10-4-09Document6 pagesForeclosure Defense Strategy 10-4-09YourEminenceNo ratings yet

- Accounting Standards in The East Asia Region: By: M. Zubaidur RahmanDocument16 pagesAccounting Standards in The East Asia Region: By: M. Zubaidur Rahmanemerson deasisNo ratings yet

- PDF High Performance Boards Improving and Energizing Your Governance 1St Edition Cossin Ebook Full ChapterDocument53 pagesPDF High Performance Boards Improving and Energizing Your Governance 1St Edition Cossin Ebook Full Chapterdebbie.mitchell437100% (2)

- Benjamin C. Santos and Estrella, Remitio & Associates For Petitioner. Rodolfo V. Gumban For Private RespondentDocument5 pagesBenjamin C. Santos and Estrella, Remitio & Associates For Petitioner. Rodolfo V. Gumban For Private RespondentLouisa FerrarenNo ratings yet

- (Name of The Association)Document4 pages(Name of The Association)ChanChi Domocmat LaresNo ratings yet

- AJmera Cement ProjectDocument60 pagesAJmera Cement ProjectHiren ChauhanNo ratings yet

- MCQ Midterms in Land Titles - 2020 - Answer KeyDocument21 pagesMCQ Midterms in Land Titles - 2020 - Answer KeyAr-Reb AquinoNo ratings yet

- The Role of The Wife in IslamDocument2 pagesThe Role of The Wife in IslamShadab AnjumNo ratings yet

- SOP For Procedure of PurchasingDocument2 pagesSOP For Procedure of PurchasingtridentindiacompanyNo ratings yet

- Anti Plunder ActDocument3 pagesAnti Plunder ActmeriiNo ratings yet

- Kinds of Cheques: Cabigting, Maria Queenie Lilirae Purzuelo, DanielleDocument51 pagesKinds of Cheques: Cabigting, Maria Queenie Lilirae Purzuelo, DanielleRae De CastroNo ratings yet