ECON 112 Chapter 3

ECON 112 Chapter 3

You might also like

- IGCSE Economics Revision NotesDocument58 pagesIGCSE Economics Revision NotesCrystal Wong87% (209)

- Notes On All TopicsDocument56 pagesNotes On All TopicspotpalNo ratings yet

- Btech Economics Updated Study Material Till 8th Feb 2022-WedDocument106 pagesBtech Economics Updated Study Material Till 8th Feb 2022-WedJashanpreet SinghNo ratings yet

- Lesson 1 Basic MicroeconomicsDocument16 pagesLesson 1 Basic MicroeconomicsMickaela GulisNo ratings yet

- Unit II MaterialDocument35 pagesUnit II MaterialPRAVEENKUMAR MNo ratings yet

- Ajo, Mark Sherwin Assign. MicroeconomicsDocument4 pagesAjo, Mark Sherwin Assign. MicroeconomicsMark Sherwin AjoNo ratings yet

- Part 1 EconomicsDocument22 pagesPart 1 EconomicsDennisBrionesNo ratings yet

- Emv 222 Lecture GuideDocument23 pagesEmv 222 Lecture Guidealica studioNo ratings yet

- Economics Syllabus ConcisedDocument43 pagesEconomics Syllabus ConcisedshakirafarleyNo ratings yet

- Economics Defined: Production of GoodsDocument22 pagesEconomics Defined: Production of Goods'Sabur-akin AkinadeNo ratings yet

- Economics For Managers Course No: 401: Rup Ratan Pine Mob: 01552438118Document30 pagesEconomics For Managers Course No: 401: Rup Ratan Pine Mob: 01552438118rifath rafiqNo ratings yet

- Economic and Social DevelopmentDocument17 pagesEconomic and Social Developmentjohnsonadolph777No ratings yet

- S.5 Economics Production Theory PDFDocument60 pagesS.5 Economics Production Theory PDFAhurira MichaelNo ratings yet

- Macro Economics Cycle Contribute To The Growth BetweenDocument5 pagesMacro Economics Cycle Contribute To The Growth BetweenQNo ratings yet

- EconomyDocument138 pagesEconomyShambhavi SrivastavaNo ratings yet

- ECON1220 (Midterms)Document492 pagesECON1220 (Midterms)meganyaptanNo ratings yet

- EcotaxaDocument8 pagesEcotaxaMark Leo Lamigo JacintoNo ratings yet

- L 01 - Introduction PDFDocument26 pagesL 01 - Introduction PDFMd:Sulayman MSMNo ratings yet

- Applied Economics Power PointDocument213 pagesApplied Economics Power Pointjonathan malasigNo ratings yet

- Introduction To Agricultural Economics (AEB 212) : Group: Student Numbers: VENUE: Lecture Theatre 311/003Document46 pagesIntroduction To Agricultural Economics (AEB 212) : Group: Student Numbers: VENUE: Lecture Theatre 311/003Thabo ChuchuNo ratings yet

- Introduction To Microeconomics (ECO 111)Document386 pagesIntroduction To Microeconomics (ECO 111)angaNo ratings yet

- App Econ NotesDocument8 pagesApp Econ Notesdanie.hermosaNo ratings yet

- Economic SystemDocument15 pagesEconomic SystemMaylyn MasilangNo ratings yet

- Topic 2 - ProductionDocument20 pagesTopic 2 - ProductionlingtonjacksonNo ratings yet

- Circular Flow of Funds: Through The EconomyDocument10 pagesCircular Flow of Funds: Through The EconomyHaji Saif UllahNo ratings yet

- Edexcel Glossary Theme1Document13 pagesEdexcel Glossary Theme1Stinkytofu DianaNo ratings yet

- EE NotesDocument49 pagesEE NotesAkshatNo ratings yet

- Introduction To EconomicsDocument12 pagesIntroduction To EconomicsBaro LeeNo ratings yet

- EE NotesDocument26 pagesEE NotesShobhitNo ratings yet

- Applied Economics. ReviewerDocument9 pagesApplied Economics. ReviewerKISS VALERY CAMACHONo ratings yet

- Allocation of ResourcesDocument14 pagesAllocation of ResourcesAzar Anjum RiazNo ratings yet

- Appilied Economics ReviewerDocument12 pagesAppilied Economics ReviewereveNo ratings yet

- Session - 2 - Production - Supply - and - Demand - (Handouts)Document7 pagesSession - 2 - Production - Supply - and - Demand - (Handouts)RHOEL ARIES PEÑAMANTE PINTONo ratings yet

- Theory of Production 1Document6 pagesTheory of Production 1Sky ceeNo ratings yet

- Eco Notes PreliminaryDocument24 pagesEco Notes Preliminaryhell noNo ratings yet

- National Income and AccountingDocument24 pagesNational Income and Accountingmouli poliparthiNo ratings yet

- IBDP Economics HL Chapter 1 NotesDocument6 pagesIBDP Economics HL Chapter 1 NotesAditya Rathi100% (1)

- Summary03 FinalDocument36 pagesSummary03 Finaltomec72872No ratings yet

- Ss 1 Production EconomicsDocument23 pagesSs 1 Production Economicsgabrielfavour2010No ratings yet

- Chapter 1 Revisiting Economics As A Social ScienceDocument4 pagesChapter 1 Revisiting Economics As A Social ScienceMaxNo ratings yet

- Igcse Economics NotesDocument6 pagesIgcse Economics NotesMunni Chetan0% (1)

- Chapter 6.Pptx NiosDocument20 pagesChapter 6.Pptx Niosamita venkateshNo ratings yet

- Chapter 23 & Introduction - Measuring A Nation's IncomeDocument75 pagesChapter 23 & Introduction - Measuring A Nation's IncomeFTU K59 Trần Yến LinhNo ratings yet

- O.L Business PDFDocument159 pagesO.L Business PDFSeif MahmoudNo ratings yet

- Unit 7A National Product and Its Measurement BitinfonepalDocument57 pagesUnit 7A National Product and Its Measurement BitinfonepalYogendra KshetriNo ratings yet

- Year 11 Eco NotesDocument38 pagesYear 11 Eco NotesNathan CaoNo ratings yet

- Ecs1501 Study Summary 159885885556653Document6 pagesEcs1501 Study Summary 159885885556653Kirk HöllNo ratings yet

- EcooooonDocument4 pagesEcooooonBlessa BernabeNo ratings yet

- Principle of Economics1 (Chapter2)Document7 pagesPrinciple of Economics1 (Chapter2)MA ValdezNo ratings yet

- Introduction To EconomicsDocument36 pagesIntroduction To EconomicsLea Guico100% (1)

- What Is Economics The Study Of?Document6 pagesWhat Is Economics The Study Of?Marga GrecuNo ratings yet

- Chapter 1Document5 pagesChapter 1nelsNo ratings yet

- The Global Economy by HAZEL MAY CERAFICADocument21 pagesThe Global Economy by HAZEL MAY CERAFICAHazel May CeraficaNo ratings yet

- Principles of EconomicsDocument23 pagesPrinciples of EconomicsKangoma Fodie MansarayNo ratings yet

- Macroeconomics Chap 12 Production and GrowthDocument3 pagesMacroeconomics Chap 12 Production and GrowthChau GiangNo ratings yet

- Binder 1Document64 pagesBinder 1El-rohy KalongoNo ratings yet

- BBAEZ4A CHAPTER 3 Production, Income and Spending in The Mixed EconomyDocument35 pagesBBAEZ4A CHAPTER 3 Production, Income and Spending in The Mixed EconomyEl-rohy KalongoNo ratings yet

- The Study of Economics Pt. 1Document3 pagesThe Study of Economics Pt. 1black gearNo ratings yet

- Mora, Jonathan A. BSA-5ADocument58 pagesMora, Jonathan A. BSA-5Aasd zxcNo ratings yet

- Chapter 4 WorksheetDocument11 pagesChapter 4 WorksheetdewetmonjaNo ratings yet

- Chapter 2 WorksheetDocument5 pagesChapter 2 WorksheetdewetmonjaNo ratings yet

- Bman Intro ChapterDocument6 pagesBman Intro ChapterdewetmonjaNo ratings yet

- Life Sciences P2 Nov 2019 EngDocument14 pagesLife Sciences P2 Nov 2019 EngdewetmonjaNo ratings yet

- Chapter 4 ECON 112Document11 pagesChapter 4 ECON 112dewetmonjaNo ratings yet

- Chapter 2 ECON 112Document7 pagesChapter 2 ECON 112dewetmonjaNo ratings yet

- ECON 112 Summaries Chapters 1Document12 pagesECON 112 Summaries Chapters 1dewetmonjaNo ratings yet

- 2005 ITAD RulingsDocument461 pages2005 ITAD RulingsJerwin DaveNo ratings yet

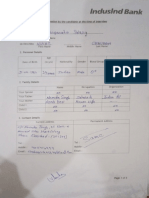

- Banking & Insurance: Project On HDFC BankDocument36 pagesBanking & Insurance: Project On HDFC Bankvrathi87No ratings yet

- Instructions / Checklist For Filling KYC FormDocument22 pagesInstructions / Checklist For Filling KYC FormAiyazz ShaikhNo ratings yet

- Sources of Finance DefinitionDocument6 pagesSources of Finance Definitionpallavi4846100% (1)

- PNB Personal Loan Scheme-Pnb Sahyog Covid 19Document17 pagesPNB Personal Loan Scheme-Pnb Sahyog Covid 19Nishesh KumarNo ratings yet

- Garden City High School: Budget ExpensesDocument3 pagesGarden City High School: Budget ExpensesKyjuan T. KingNo ratings yet

- Financial Management Term PaperDocument6 pagesFinancial Management Term Paperc5h71zzc100% (1)

- CIR V Central LuzonDocument2 pagesCIR V Central LuzonAgnes FranciscoNo ratings yet

- A Project Report HDFC BANKDocument48 pagesA Project Report HDFC BANKVikas SinghNo ratings yet

- Last Resort 2Document2 pagesLast Resort 2Francis TutorNo ratings yet

- Nonstate Institutions-Banks and CorporationsDocument20 pagesNonstate Institutions-Banks and CorporationsEisenhower SabaNo ratings yet

- Role of Government and RBI in Money Market - IndianMoneyDocument10 pagesRole of Government and RBI in Money Market - IndianMoneyKushNo ratings yet

- INTRODUCTION TO CO OperativeDocument30 pagesINTRODUCTION TO CO OperativeAkash MauryaNo ratings yet

- R.A Act No.1400 Land Reform Act of 1955Document8 pagesR.A Act No.1400 Land Reform Act of 1955Nadine FrogosoNo ratings yet

- Definition of Capital AllowancesDocument9 pagesDefinition of Capital AllowancesAdesolaNo ratings yet

- Emerging Markets Review: James Foye, Aljo Ša Valentinčič TDocument15 pagesEmerging Markets Review: James Foye, Aljo Ša Valentinčič TDessy ParamitaNo ratings yet

- Franchise QuizDocument2 pagesFranchise QuizCattleyaNo ratings yet

- ConstitutionDocument10 pagesConstitutionapi-234193160No ratings yet

- S 15 - Efficient Capital Markets and Behavioral ChallengesDocument27 pagesS 15 - Efficient Capital Markets and Behavioral ChallengesAninda DuttaNo ratings yet

- Report - 06 03 2024 - 03 59 20Document1 pageReport - 06 03 2024 - 03 59 20vlasbod18No ratings yet

- Investment Strategy Based On Gearing RatioDocument11 pagesInvestment Strategy Based On Gearing RatiomanmeetNo ratings yet

- DB On BF ModelDocument56 pagesDB On BF ModelMyie Cruz-VictorNo ratings yet

- India - MS Economics Aug 2022Document11 pagesIndia - MS Economics Aug 2022Salim MiyaNo ratings yet

- Shareholder Value Creation: An OverviewDocument5 pagesShareholder Value Creation: An OverviewggeettNo ratings yet

- Business PlanDocument38 pagesBusiness PlanHONEY SHEN BULADACONo ratings yet

- Resrch Ratio AnalysisDocument68 pagesResrch Ratio AnalysisGyan Bikram ShahNo ratings yet

- SUBJECT: Law of Investment.: Chanakya National Law University, PatnaDocument30 pagesSUBJECT: Law of Investment.: Chanakya National Law University, PatnaPammi ShergillNo ratings yet

- ReceiptsDocument9 pagesReceiptsinfoNo ratings yet

- Foreign Capital and Economic Growth of IndiaDocument23 pagesForeign Capital and Economic Growth of IndiaMitesh ShahNo ratings yet

- Adobe Scan 18 Oct 2021Document25 pagesAdobe Scan 18 Oct 2021Topviralhub videosNo ratings yet

Download as pdf or txt

You might also like

- IGCSE Economics Revision NotesDocument58 pagesIGCSE Economics Revision NotesCrystal Wong87% (209)

- Notes On All TopicsDocument56 pagesNotes On All TopicspotpalNo ratings yet

- Btech Economics Updated Study Material Till 8th Feb 2022-WedDocument106 pagesBtech Economics Updated Study Material Till 8th Feb 2022-WedJashanpreet SinghNo ratings yet

- Lesson 1 Basic MicroeconomicsDocument16 pagesLesson 1 Basic MicroeconomicsMickaela GulisNo ratings yet

- Unit II MaterialDocument35 pagesUnit II MaterialPRAVEENKUMAR MNo ratings yet

- Ajo, Mark Sherwin Assign. MicroeconomicsDocument4 pagesAjo, Mark Sherwin Assign. MicroeconomicsMark Sherwin AjoNo ratings yet

- Part 1 EconomicsDocument22 pagesPart 1 EconomicsDennisBrionesNo ratings yet

- Emv 222 Lecture GuideDocument23 pagesEmv 222 Lecture Guidealica studioNo ratings yet

- Economics Syllabus ConcisedDocument43 pagesEconomics Syllabus ConcisedshakirafarleyNo ratings yet

- Economics Defined: Production of GoodsDocument22 pagesEconomics Defined: Production of Goods'Sabur-akin AkinadeNo ratings yet

- Economics For Managers Course No: 401: Rup Ratan Pine Mob: 01552438118Document30 pagesEconomics For Managers Course No: 401: Rup Ratan Pine Mob: 01552438118rifath rafiqNo ratings yet

- Economic and Social DevelopmentDocument17 pagesEconomic and Social Developmentjohnsonadolph777No ratings yet

- S.5 Economics Production Theory PDFDocument60 pagesS.5 Economics Production Theory PDFAhurira MichaelNo ratings yet

- Macro Economics Cycle Contribute To The Growth BetweenDocument5 pagesMacro Economics Cycle Contribute To The Growth BetweenQNo ratings yet

- EconomyDocument138 pagesEconomyShambhavi SrivastavaNo ratings yet

- ECON1220 (Midterms)Document492 pagesECON1220 (Midterms)meganyaptanNo ratings yet

- EcotaxaDocument8 pagesEcotaxaMark Leo Lamigo JacintoNo ratings yet

- L 01 - Introduction PDFDocument26 pagesL 01 - Introduction PDFMd:Sulayman MSMNo ratings yet

- Applied Economics Power PointDocument213 pagesApplied Economics Power Pointjonathan malasigNo ratings yet

- Introduction To Agricultural Economics (AEB 212) : Group: Student Numbers: VENUE: Lecture Theatre 311/003Document46 pagesIntroduction To Agricultural Economics (AEB 212) : Group: Student Numbers: VENUE: Lecture Theatre 311/003Thabo ChuchuNo ratings yet

- Introduction To Microeconomics (ECO 111)Document386 pagesIntroduction To Microeconomics (ECO 111)angaNo ratings yet

- App Econ NotesDocument8 pagesApp Econ Notesdanie.hermosaNo ratings yet

- Economic SystemDocument15 pagesEconomic SystemMaylyn MasilangNo ratings yet

- Topic 2 - ProductionDocument20 pagesTopic 2 - ProductionlingtonjacksonNo ratings yet

- Circular Flow of Funds: Through The EconomyDocument10 pagesCircular Flow of Funds: Through The EconomyHaji Saif UllahNo ratings yet

- Edexcel Glossary Theme1Document13 pagesEdexcel Glossary Theme1Stinkytofu DianaNo ratings yet

- EE NotesDocument49 pagesEE NotesAkshatNo ratings yet

- Introduction To EconomicsDocument12 pagesIntroduction To EconomicsBaro LeeNo ratings yet

- EE NotesDocument26 pagesEE NotesShobhitNo ratings yet

- Applied Economics. ReviewerDocument9 pagesApplied Economics. ReviewerKISS VALERY CAMACHONo ratings yet

- Allocation of ResourcesDocument14 pagesAllocation of ResourcesAzar Anjum RiazNo ratings yet

- Appilied Economics ReviewerDocument12 pagesAppilied Economics ReviewereveNo ratings yet

- Session - 2 - Production - Supply - and - Demand - (Handouts)Document7 pagesSession - 2 - Production - Supply - and - Demand - (Handouts)RHOEL ARIES PEÑAMANTE PINTONo ratings yet

- Theory of Production 1Document6 pagesTheory of Production 1Sky ceeNo ratings yet

- Eco Notes PreliminaryDocument24 pagesEco Notes Preliminaryhell noNo ratings yet

- National Income and AccountingDocument24 pagesNational Income and Accountingmouli poliparthiNo ratings yet

- IBDP Economics HL Chapter 1 NotesDocument6 pagesIBDP Economics HL Chapter 1 NotesAditya Rathi100% (1)

- Summary03 FinalDocument36 pagesSummary03 Finaltomec72872No ratings yet

- Ss 1 Production EconomicsDocument23 pagesSs 1 Production Economicsgabrielfavour2010No ratings yet

- Chapter 1 Revisiting Economics As A Social ScienceDocument4 pagesChapter 1 Revisiting Economics As A Social ScienceMaxNo ratings yet

- Igcse Economics NotesDocument6 pagesIgcse Economics NotesMunni Chetan0% (1)

- Chapter 6.Pptx NiosDocument20 pagesChapter 6.Pptx Niosamita venkateshNo ratings yet

- Chapter 23 & Introduction - Measuring A Nation's IncomeDocument75 pagesChapter 23 & Introduction - Measuring A Nation's IncomeFTU K59 Trần Yến LinhNo ratings yet

- O.L Business PDFDocument159 pagesO.L Business PDFSeif MahmoudNo ratings yet

- Unit 7A National Product and Its Measurement BitinfonepalDocument57 pagesUnit 7A National Product and Its Measurement BitinfonepalYogendra KshetriNo ratings yet

- Year 11 Eco NotesDocument38 pagesYear 11 Eco NotesNathan CaoNo ratings yet

- Ecs1501 Study Summary 159885885556653Document6 pagesEcs1501 Study Summary 159885885556653Kirk HöllNo ratings yet

- EcooooonDocument4 pagesEcooooonBlessa BernabeNo ratings yet

- Principle of Economics1 (Chapter2)Document7 pagesPrinciple of Economics1 (Chapter2)MA ValdezNo ratings yet

- Introduction To EconomicsDocument36 pagesIntroduction To EconomicsLea Guico100% (1)

- What Is Economics The Study Of?Document6 pagesWhat Is Economics The Study Of?Marga GrecuNo ratings yet

- Chapter 1Document5 pagesChapter 1nelsNo ratings yet

- The Global Economy by HAZEL MAY CERAFICADocument21 pagesThe Global Economy by HAZEL MAY CERAFICAHazel May CeraficaNo ratings yet

- Principles of EconomicsDocument23 pagesPrinciples of EconomicsKangoma Fodie MansarayNo ratings yet

- Macroeconomics Chap 12 Production and GrowthDocument3 pagesMacroeconomics Chap 12 Production and GrowthChau GiangNo ratings yet

- Binder 1Document64 pagesBinder 1El-rohy KalongoNo ratings yet

- BBAEZ4A CHAPTER 3 Production, Income and Spending in The Mixed EconomyDocument35 pagesBBAEZ4A CHAPTER 3 Production, Income and Spending in The Mixed EconomyEl-rohy KalongoNo ratings yet

- The Study of Economics Pt. 1Document3 pagesThe Study of Economics Pt. 1black gearNo ratings yet

- Mora, Jonathan A. BSA-5ADocument58 pagesMora, Jonathan A. BSA-5Aasd zxcNo ratings yet

- Chapter 4 WorksheetDocument11 pagesChapter 4 WorksheetdewetmonjaNo ratings yet

- Chapter 2 WorksheetDocument5 pagesChapter 2 WorksheetdewetmonjaNo ratings yet

- Bman Intro ChapterDocument6 pagesBman Intro ChapterdewetmonjaNo ratings yet

- Life Sciences P2 Nov 2019 EngDocument14 pagesLife Sciences P2 Nov 2019 EngdewetmonjaNo ratings yet

- Chapter 4 ECON 112Document11 pagesChapter 4 ECON 112dewetmonjaNo ratings yet

- Chapter 2 ECON 112Document7 pagesChapter 2 ECON 112dewetmonjaNo ratings yet

- ECON 112 Summaries Chapters 1Document12 pagesECON 112 Summaries Chapters 1dewetmonjaNo ratings yet

- 2005 ITAD RulingsDocument461 pages2005 ITAD RulingsJerwin DaveNo ratings yet

- Banking & Insurance: Project On HDFC BankDocument36 pagesBanking & Insurance: Project On HDFC Bankvrathi87No ratings yet

- Instructions / Checklist For Filling KYC FormDocument22 pagesInstructions / Checklist For Filling KYC FormAiyazz ShaikhNo ratings yet

- Sources of Finance DefinitionDocument6 pagesSources of Finance Definitionpallavi4846100% (1)

- PNB Personal Loan Scheme-Pnb Sahyog Covid 19Document17 pagesPNB Personal Loan Scheme-Pnb Sahyog Covid 19Nishesh KumarNo ratings yet

- Garden City High School: Budget ExpensesDocument3 pagesGarden City High School: Budget ExpensesKyjuan T. KingNo ratings yet

- Financial Management Term PaperDocument6 pagesFinancial Management Term Paperc5h71zzc100% (1)

- CIR V Central LuzonDocument2 pagesCIR V Central LuzonAgnes FranciscoNo ratings yet

- A Project Report HDFC BANKDocument48 pagesA Project Report HDFC BANKVikas SinghNo ratings yet

- Last Resort 2Document2 pagesLast Resort 2Francis TutorNo ratings yet

- Nonstate Institutions-Banks and CorporationsDocument20 pagesNonstate Institutions-Banks and CorporationsEisenhower SabaNo ratings yet

- Role of Government and RBI in Money Market - IndianMoneyDocument10 pagesRole of Government and RBI in Money Market - IndianMoneyKushNo ratings yet

- INTRODUCTION TO CO OperativeDocument30 pagesINTRODUCTION TO CO OperativeAkash MauryaNo ratings yet

- R.A Act No.1400 Land Reform Act of 1955Document8 pagesR.A Act No.1400 Land Reform Act of 1955Nadine FrogosoNo ratings yet

- Definition of Capital AllowancesDocument9 pagesDefinition of Capital AllowancesAdesolaNo ratings yet

- Emerging Markets Review: James Foye, Aljo Ša Valentinčič TDocument15 pagesEmerging Markets Review: James Foye, Aljo Ša Valentinčič TDessy ParamitaNo ratings yet

- Franchise QuizDocument2 pagesFranchise QuizCattleyaNo ratings yet

- ConstitutionDocument10 pagesConstitutionapi-234193160No ratings yet

- S 15 - Efficient Capital Markets and Behavioral ChallengesDocument27 pagesS 15 - Efficient Capital Markets and Behavioral ChallengesAninda DuttaNo ratings yet

- Report - 06 03 2024 - 03 59 20Document1 pageReport - 06 03 2024 - 03 59 20vlasbod18No ratings yet

- Investment Strategy Based On Gearing RatioDocument11 pagesInvestment Strategy Based On Gearing RatiomanmeetNo ratings yet

- DB On BF ModelDocument56 pagesDB On BF ModelMyie Cruz-VictorNo ratings yet

- India - MS Economics Aug 2022Document11 pagesIndia - MS Economics Aug 2022Salim MiyaNo ratings yet

- Shareholder Value Creation: An OverviewDocument5 pagesShareholder Value Creation: An OverviewggeettNo ratings yet

- Business PlanDocument38 pagesBusiness PlanHONEY SHEN BULADACONo ratings yet

- Resrch Ratio AnalysisDocument68 pagesResrch Ratio AnalysisGyan Bikram ShahNo ratings yet

- SUBJECT: Law of Investment.: Chanakya National Law University, PatnaDocument30 pagesSUBJECT: Law of Investment.: Chanakya National Law University, PatnaPammi ShergillNo ratings yet

- ReceiptsDocument9 pagesReceiptsinfoNo ratings yet

- Foreign Capital and Economic Growth of IndiaDocument23 pagesForeign Capital and Economic Growth of IndiaMitesh ShahNo ratings yet

- Adobe Scan 18 Oct 2021Document25 pagesAdobe Scan 18 Oct 2021Topviralhub videosNo ratings yet