Download as pdf or txt

You might also like

- Fundamental Analysis of Indian Pharmaceutical Companies: June 2018Document25 pagesFundamental Analysis of Indian Pharmaceutical Companies: June 2018Prakhar BhatnagarNo ratings yet

- Research Paper On Capital StructureDocument12 pagesResearch Paper On Capital StructureJack AroraNo ratings yet

- Measuring Financial Health of A Public Limited Company Using Z' Score Model - A Case StudyDocument18 pagesMeasuring Financial Health of A Public Limited Company Using Z' Score Model - A Case Studytrinanjan bhowalNo ratings yet

- 139 April2019Document11 pages139 April2019vaibhav pachputeNo ratings yet

- DR +Khushbu+JainDocument6 pagesDR +Khushbu+JainSonali MoreNo ratings yet

- Financial Performance Analysis of Corporation BankDocument8 pagesFinancial Performance Analysis of Corporation BankManjunath ShettyNo ratings yet

- Financial Performance AnalysisDocument8 pagesFinancial Performance AnalysisJanus GalangNo ratings yet

- Trend Analysis Final Project by ArjitDocument37 pagesTrend Analysis Final Project by Arjitsandeepkaur1131992No ratings yet

- A Study On Financial Analysis and Performance of Kotak Mahindra BankDocument12 pagesA Study On Financial Analysis and Performance of Kotak Mahindra BankAkash DevNo ratings yet

- Comparative Studyon Financial Performanceof Hindustan Unileverand Nestle IndiaDocument8 pagesComparative Studyon Financial Performanceof Hindustan Unileverand Nestle Indianeha.talele22.stNo ratings yet

- A Comparative Analysis of The Financial Ratios of Selected Banks in The India For The Period of 2011-2014Document17 pagesA Comparative Analysis of The Financial Ratios of Selected Banks in The India For The Period of 2011-2014Rawan AbuzaidNo ratings yet

- Performance Analysis of Mutual Fund: A Comparative Study of The Selected Debt Mutual Fund Scheme in IndiaDocument5 pagesPerformance Analysis of Mutual Fund: A Comparative Study of The Selected Debt Mutual Fund Scheme in IndiaaqsakhanaljedeelNo ratings yet

- University School of Business Studies Talwandi Sabo: SynopsisDocument10 pagesUniversity School of Business Studies Talwandi Sabo: SynopsisInder Dhaliwal KangarhNo ratings yet

- Performance and Evaluation of Mutual FundsDocument6 pagesPerformance and Evaluation of Mutual FundsManali RanaNo ratings yet

- Comparative Study On Financial PerformanceDocument8 pagesComparative Study On Financial PerformancedurranibroseNo ratings yet

- Literature Review Analysis of Recorded Facts of Business PDFDocument8 pagesLiterature Review Analysis of Recorded Facts of Business PDFMohammed YASEENNo ratings yet

- Wa0004.Document50 pagesWa0004.pradhanraja05679No ratings yet

- 25-11-2023-1700920501-7-Ijfm-3. Ijfm - A Project Report On Financial Analysis of Reliance Industries Limited Through Comparative Balance SheetsDocument10 pages25-11-2023-1700920501-7-Ijfm-3. Ijfm - A Project Report On Financial Analysis of Reliance Industries Limited Through Comparative Balance SheetsAbhay ShuklaNo ratings yet

- Aeee PDFDocument21 pagesAeee PDFMane DaralNo ratings yet

- Aditya PatnaikDocument55 pagesAditya PatnaikAD CREATIONNo ratings yet

- Impact of Non-Performing Asset On Profitability and Efficiency of Banking Sector in IndiaDocument10 pagesImpact of Non-Performing Asset On Profitability and Efficiency of Banking Sector in Indiarohan mohapatraNo ratings yet

- SSRN-id3090997 - MFDocument8 pagesSSRN-id3090997 - MFsameer balamNo ratings yet

- Performance Evaluation of 10 Listed Bank Stocks & Comparison With Nifty 50Document6 pagesPerformance Evaluation of 10 Listed Bank Stocks & Comparison With Nifty 50Bijal DanichaNo ratings yet

- Financial Structure Analysis of Indian Companies: A Review of LiteratureDocument9 pagesFinancial Structure Analysis of Indian Companies: A Review of LiteratureVįňäý Ğøwđã VįñîNo ratings yet

- Julia18gsob1010373 Bba FinalDocument35 pagesJulia18gsob1010373 Bba FinalVijayakumar ChNo ratings yet

- .. Current 2018 Feb BDj0Gy8teJzklCWDocument14 pages.. Current 2018 Feb BDj0Gy8teJzklCWRAHUL KUMARNo ratings yet

- A Study On Evaluation of Financial Performance of FMCG Sector Prepared by Krutika R. Tank Under The Guidance of Dr. Hitesh ShuklaDocument16 pagesA Study On Evaluation of Financial Performance of FMCG Sector Prepared by Krutika R. Tank Under The Guidance of Dr. Hitesh ShuklaKRTNo ratings yet

- Comparative Study of Microfinance Institutions in India: March 2021Document8 pagesComparative Study of Microfinance Institutions in India: March 2021shubham475hNo ratings yet

- Chapter: 3 Research MethodologyDocument21 pagesChapter: 3 Research MethodologySamyuktha KNo ratings yet

- Sudeshnaa Final Yr ProjectDocument15 pagesSudeshnaa Final Yr ProjectShri hariniNo ratings yet

- Mutual Funds in India A Comparative Study of Select Public Sector and Private Sector CompaniesDocument13 pagesMutual Funds in India A Comparative Study of Select Public Sector and Private Sector Companiesarcherselevators0% (1)

- JETIR2302448Document7 pagesJETIR2302448Rupak RoyNo ratings yet

- Impactof Capitalstructureon Financial PerformanceanditsdeterminantsDocument11 pagesImpactof Capitalstructureon Financial PerformanceanditsdeterminantsLehar GabaNo ratings yet

- Ijrmec 749 54572Document14 pagesIjrmec 749 54572eunkyung ChoiNo ratings yet

- The Impact of Capital Structure On The Profitability of Publicly Traded Manufacturing Firms in BangladeshDocument5 pagesThe Impact of Capital Structure On The Profitability of Publicly Traded Manufacturing Firms in BangladeshAnonymous XIwe3KKNo ratings yet

- Incn15 Fin 059 PDFDocument15 pagesIncn15 Fin 059 PDFchirag_nrmba15No ratings yet

- IJMSS10 March 4335Document23 pagesIJMSS10 March 4335Avinash TiwariNo ratings yet

- A Study On Financial Perfomance of Alakode Service Co-Operative BankDocument58 pagesA Study On Financial Perfomance of Alakode Service Co-Operative BankjineshshajiNo ratings yet

- Camel ModelDocument8 pagesCamel ModelRabinNo ratings yet

- Comparison Between Some Debt Equity & Mutual FundsDocument20 pagesComparison Between Some Debt Equity & Mutual FundsJayesh PatelNo ratings yet

- A Critical Analysis: Related PapersDocument13 pagesA Critical Analysis: Related PapersAmit MishraNo ratings yet

- Literature Review of Performance Evaluation of Mutual FundDocument8 pagesLiterature Review of Performance Evaluation of Mutual FundafdtsadhrNo ratings yet

- 1 PBDocument10 pages1 PBxyzNo ratings yet

- Merger of ICICIDocument12 pagesMerger of ICICIVlkjogfijnb LjunvodiNo ratings yet

- A Study On Financial Performance Analysis at City Union BankDocument30 pagesA Study On Financial Performance Analysis at City Union BankArnab BaruaNo ratings yet

- 2dharmendra S Mistry - Pdfa Comparative Study of The Profitability Performance in TheDocument15 pages2dharmendra S Mistry - Pdfa Comparative Study of The Profitability Performance in ThePsubbu RajNo ratings yet

- Performance Analysis of Mutual Funds - A Comparative Study On Equity Diversified Mutual FundDocument17 pagesPerformance Analysis of Mutual Funds - A Comparative Study On Equity Diversified Mutual FundAnjali KajariaNo ratings yet

- Main ProjectDocument60 pagesMain ProjectRAJA SHEKHARNo ratings yet

- Financial Performance of Power and Co. by Amisha VaghaniDocument11 pagesFinancial Performance of Power and Co. by Amisha VaghaniAplus DigitalNo ratings yet

- Financial Performance Analysis Through Position Statements of Selected FMCG CompaniesDocument8 pagesFinancial Performance Analysis Through Position Statements of Selected FMCG Companiesswati jindalNo ratings yet

- Sudhir Final Doc (1) (Autosaved) NEWDocument45 pagesSudhir Final Doc (1) (Autosaved) NEWArvindsingh1857gmailNo ratings yet

- UntitledDocument68 pagesUntitledSurendra SkNo ratings yet

- SynopsisDocument11 pagesSynopsisshiv infotech0% (1)

- Neha Sharma Final Synopsis CapstoneDocument14 pagesNeha Sharma Final Synopsis CapstoneinxxxsNo ratings yet

- BushraDocument75 pagesBushraDhakeerath KsdNo ratings yet

- "Equity Research On Banking Sector": A Project Report OnDocument47 pages"Equity Research On Banking Sector": A Project Report OnMansi GuptaNo ratings yet

- An Analysis of Financial Performance of Bhargav Bikas Bank LimitedDocument8 pagesAn Analysis of Financial Performance of Bhargav Bikas Bank LimitedNamuna Joshi100% (2)

- MHRD-II YearDocument8 pagesMHRD-II YearANKIT SHENDENo ratings yet

- Corporate Governance, Firm Profitability, and Share Valuation in the PhilippinesFrom EverandCorporate Governance, Firm Profitability, and Share Valuation in the PhilippinesNo ratings yet

- Assignment Nicmar PGCM 21Document19 pagesAssignment Nicmar PGCM 21punyadeep75% (4)

- Global CityDocument3 pagesGlobal CityKimNo ratings yet

- 2 Joint ArrangementsDocument3 pages2 Joint ArrangementsCha ChieNo ratings yet

- LC & Standby LCDocument8 pagesLC & Standby LCmanith_kim13No ratings yet

- Banking-Comunicare in Afaceri in Limba EnglezaDocument9 pagesBanking-Comunicare in Afaceri in Limba EnglezaMincu IulianNo ratings yet

- 04 Rittenberg SM Ch4 9-14-10 FINALDocument55 pages04 Rittenberg SM Ch4 9-14-10 FINALemanuelu4No ratings yet

- Analysis of Accounting Treatment of Capital Expenditure and Revenue ExpenditureDocument8 pagesAnalysis of Accounting Treatment of Capital Expenditure and Revenue ExpenditureMong MickoNo ratings yet

- Finincial Analysis of Tumkur Grain Merchants Co-Operative BankDocument110 pagesFinincial Analysis of Tumkur Grain Merchants Co-Operative BankPrashanth PB50% (2)

- Peter England-Madhura GarmentsDocument17 pagesPeter England-Madhura Garmentswintoday01100% (2)

- Agriculture Marketing Lec No 6Document27 pagesAgriculture Marketing Lec No 6MUZAMMIL GHORINo ratings yet

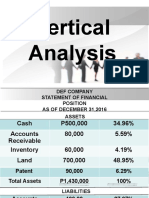

- Vertical AnalysisDocument8 pagesVertical AnalysisHannah Mae BautistaNo ratings yet

- Chaikin Power Gauge Report GMCR 29feb2012Document4 pagesChaikin Power Gauge Report GMCR 29feb2012Chaikin Analytics, LLCNo ratings yet

- Standard Costing and Variance Analysis FormulasDocument2 pagesStandard Costing and Variance Analysis FormulasRashid HussainNo ratings yet

- Wa0112.Document10 pagesWa0112.ali aliNo ratings yet

- What Ever Happened To The East Asian Developmental State The Unfolding DebateDocument23 pagesWhat Ever Happened To The East Asian Developmental State The Unfolding DebateCiCi GebreegziabherNo ratings yet

- Charlene MancusoDocument6 pagesCharlene MancusoThe News-HeraldNo ratings yet

- ErewwytruDocument6 pagesErewwytruMarjorie Joy DanzilNo ratings yet

- Corruption in Pakistan - Nguyễn Thị Thu Hằng - 425068 - MGT353Document4 pagesCorruption in Pakistan - Nguyễn Thị Thu Hằng - 425068 - MGT353Hằng ThuNo ratings yet

- Careers After COVID-19Document12 pagesCareers After COVID-19Iqbal Pugar RamadhanNo ratings yet

- Managing Supply Chain With Third Party Logistics Provider - An Overview of The IntegrationDocument8 pagesManaging Supply Chain With Third Party Logistics Provider - An Overview of The IntegrationKishore Kumar Galla100% (1)

- MINE1x Course SyllabusDocument6 pagesMINE1x Course Syllabusik43207No ratings yet

- ACCTG11B8-58-6 Answer KeysDocument3 pagesACCTG11B8-58-6 Answer KeysEUBELLE DAVE SOLATARIONo ratings yet

- CLBS Financial Statement 1Document6 pagesCLBS Financial Statement 1Peter Cranzo MeisterNo ratings yet

- 3.0 Cooperative Law (Notes and Activities) PDFDocument18 pages3.0 Cooperative Law (Notes and Activities) PDFmae camaganNo ratings yet

- Theories of Trade Theories of Trade Unions in India Unions in IndiaDocument27 pagesTheories of Trade Theories of Trade Unions in India Unions in IndiaKaruppasamy PandianNo ratings yet

- Quiz AKL - ConsolidationDocument2 pagesQuiz AKL - Consolidationsuciati_liaNo ratings yet

- Chapter 4 - Procurement & SourcingDocument7 pagesChapter 4 - Procurement & SourcingMaham ShaikhNo ratings yet

- Successful Capital Transfer Registration EUR 680,00: Charges: 2,50 EUR Shared (SHA)Document2 pagesSuccessful Capital Transfer Registration EUR 680,00: Charges: 2,50 EUR Shared (SHA)Annick RoumpazanisNo ratings yet

- Section 6-7 Group ADocument31 pagesSection 6-7 Group AVictor RudenkoNo ratings yet

- Bond ValuationDocument2 pagesBond ValuationIkram Ul Haq0% (1)