Download as pdf or txt

You might also like

- Global Technology Audit Guide (IPPF) PDFDocument32 pagesGlobal Technology Audit Guide (IPPF) PDFpuromon100% (4)

- Cost AccountingDocument31 pagesCost AccountingRayala SaisrinivasNo ratings yet

- BALTIC EXCHANGE - GuidetoMarketBenchmarksDocument143 pagesBALTIC EXCHANGE - GuidetoMarketBenchmarksEisilisNo ratings yet

- IMS Powerpoint MaterialDocument24 pagesIMS Powerpoint Materialrhamarao100% (1)

- Cost and MGMT Accti Chapter 1 Introduction and Cost ClassificationDocument17 pagesCost and MGMT Accti Chapter 1 Introduction and Cost ClassificationMahlet AbrahaNo ratings yet

- Cost and Management Accounting I Chapter I: Fundamentals of Cost AccountingDocument19 pagesCost and Management Accounting I Chapter I: Fundamentals of Cost AccountingFear Part 2No ratings yet

- 01 Full CH Cost and Management AccountingDocument35 pages01 Full CH Cost and Management Accountingsabit hussenNo ratings yet

- Cost Acc 1 Module Chapter 1Document56 pagesCost Acc 1 Module Chapter 1Khalid MuhammadNo ratings yet

- Chapter 1Document4 pagesChapter 1Aklil TeganewNo ratings yet

- Chapter 1Document14 pagesChapter 1narrNo ratings yet

- Chapter 1 and 2Document13 pagesChapter 1 and 2limenihNo ratings yet

- Chapter 1 Overview of CostDocument13 pagesChapter 1 Overview of Costnewaybeyene5No ratings yet

- 1 Chapter 1&2 Cost & MGT AccountingDocument12 pages1 Chapter 1&2 Cost & MGT AccountingMinaw BelayNo ratings yet

- Ch01 Introduction To Cost AccountingDocument5 pagesCh01 Introduction To Cost AccountingRenelyn FiloteoNo ratings yet

- ACCT 321-Managerial Accounting-1Document106 pagesACCT 321-Managerial Accounting-1Fabio NyagemiNo ratings yet

- Cost Accounting Aims To Report, Analyze, and Lead To The Improvement of Internal Cost Controls and EfficiencyDocument23 pagesCost Accounting Aims To Report, Analyze, and Lead To The Improvement of Internal Cost Controls and EfficiencyAmin HoqNo ratings yet

- Cost and Management AccountingDocument51 pagesCost and Management Accountingabhijeet0% (1)

- M.ac B.com Vi SemDocument41 pagesM.ac B.com Vi Semgankitrauniyar123No ratings yet

- CMA-I - CH - 1Document15 pagesCMA-I - CH - 1addisutadesse443No ratings yet

- Management Accounting - Unit1Document15 pagesManagement Accounting - Unit1anil gondNo ratings yet

- Unit 3 Basant Kumar 22gsob2010021 AccountingDocument24 pagesUnit 3 Basant Kumar 22gsob2010021 AccountingRavi guptaNo ratings yet

- Cost & Mgt. Acct - I, Lecture Note - Chapter 1 & 2Document35 pagesCost & Mgt. Acct - I, Lecture Note - Chapter 1 & 2Yonas BamlakuNo ratings yet

- Module 1 PDFDocument13 pagesModule 1 PDFWaridi GroupNo ratings yet

- Management Accounting (MA)Document114 pagesManagement Accounting (MA)Shivangi Patel100% (1)

- MA AssignmentDocument8 pagesMA AssignmentPradhyum NagarNo ratings yet

- Cost Accounting PDFDocument35 pagesCost Accounting PDFSanta-ana Jerald JuanoNo ratings yet

- Accounting Finance For EngineersDocument16 pagesAccounting Finance For EngineersSubashiиy PяabakaяaиNo ratings yet

- CAPE Unit 2 - Costing Principles CMA & FADocument5 pagesCAPE Unit 2 - Costing Principles CMA & FAPrecious CodringtonNo ratings yet

- Module 1 - Accounting and BusinessDocument16 pagesModule 1 - Accounting and BusinessNiña Sharie Cardenas100% (1)

- Chapter 1 AccDocument6 pagesChapter 1 AccMarta Fdez-FournierNo ratings yet

- Management AccountingDocument11 pagesManagement AccountingGabriel BelmonteNo ratings yet

- Managerial AccountingDocument5 pagesManagerial Accountingjaninemaeserpa14No ratings yet

- Managerial Accounting-EXTREMEDocument3 pagesManagerial Accounting-EXTREMEAbzreil AmerolNo ratings yet

- C.A-I Chapter-1Document6 pagesC.A-I Chapter-1Tariku KolchaNo ratings yet

- Chapter One Management AccountingDocument26 pagesChapter One Management AccountingsirnateNo ratings yet

- Bba 304 PDFDocument522 pagesBba 304 PDFsureshbaddha86% (7)

- Adv. Accountancy Paper-2Document17 pagesAdv. Accountancy Paper-2Avadhut PaymalleNo ratings yet

- ACCT 1003 Summary Notes 1Document4 pagesACCT 1003 Summary Notes 1roy JohnsonNo ratings yet

- Chapetr1-Overview of Cost and Management AccountingDocument12 pagesChapetr1-Overview of Cost and Management AccountingNetsanet BelayNo ratings yet

- Cost and Management Accounting Unit 1 NotesDocument13 pagesCost and Management Accounting Unit 1 NotesAliyah AliNo ratings yet

- Financial Accounting and Cost AccountingDocument34 pagesFinancial Accounting and Cost AccountinggeraldNo ratings yet

- Lectures Note On Cost and Management AccountingDocument59 pagesLectures Note On Cost and Management AccountingMusa HassanNo ratings yet

- Management Acc 1Document30 pagesManagement Acc 1AbhishekNo ratings yet

- Cost Accounting IDocument60 pagesCost Accounting Isamuel debebe50% (2)

- Financial Accounting and Cost AccountingDocument6 pagesFinancial Accounting and Cost AccountingdranilshindeNo ratings yet

- Subject Financial Accounting and Reporting Chapter/Unit Chapter 2/part 1 Lesson Title Accounting and Business Lesson ObjectivesDocument16 pagesSubject Financial Accounting and Reporting Chapter/Unit Chapter 2/part 1 Lesson Title Accounting and Business Lesson ObjectivesAzuma JunichiNo ratings yet

- Actg35 1Document2 pagesActg35 1api-3744266No ratings yet

- Management Accounting Unit No 1st BBA 5th SemesterDocument4 pagesManagement Accounting Unit No 1st BBA 5th SemesterDrVivek SansonNo ratings yet

- Accounting I UnitDocument28 pagesAccounting I UnitBalasaranyasiddhuNo ratings yet

- Fin. Acct.-review-Lesson 1Document6 pagesFin. Acct.-review-Lesson 1SALENE WHYTENo ratings yet

- Cost and MGT Acc IDocument38 pagesCost and MGT Acc IBrhane WeldegebrialNo ratings yet

- Cost Chapter OneDocument25 pagesCost Chapter OneDEREJENo ratings yet

- Strat Cost ReviewerDocument27 pagesStrat Cost ReviewerGabrielle Anne MagsanocNo ratings yet

- Managerial AccountingDocument7 pagesManagerial Accountinglena moseroNo ratings yet

- Chapter-1 125626Document11 pagesChapter-1 125626Jelna CeladaNo ratings yet

- Management Account Sem 1Document28 pagesManagement Account Sem 1Darshan VadherNo ratings yet

- ACT1107 - Introduction To Management AccountingDocument4 pagesACT1107 - Introduction To Management AccountingJamil MacabandingNo ratings yet

- Introduction To Management Accounting: Asst Prof. Jonlen DesaDocument22 pagesIntroduction To Management Accounting: Asst Prof. Jonlen DesaAryanSainiNo ratings yet

- Ans.1) (Chapter 1) : Management Accounting Is The Process of Identification, Measurement, Accumulation, AnalysisDocument27 pagesAns.1) (Chapter 1) : Management Accounting Is The Process of Identification, Measurement, Accumulation, AnalysisAnshuNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet

- On The Occasion of His 90th Birthday, November 14th, 1996. Otto HarrassowitzDocument2 pagesOn The Occasion of His 90th Birthday, November 14th, 1996. Otto HarrassowitzAbdu YaYa AbeshaNo ratings yet

- Usu Business AdministrationDocument4 pagesUsu Business AdministrationAbdu YaYa AbeshaNo ratings yet

- Delgado Community College Foundation. Inc. New Orleans, Louisiana Financlu. Statements JUNE 30, 20U AND 2010Document21 pagesDelgado Community College Foundation. Inc. New Orleans, Louisiana Financlu. Statements JUNE 30, 20U AND 2010Abdu YaYa AbeshaNo ratings yet

- Chapter One InternationalDocument11 pagesChapter One InternationalAbdu YaYa AbeshaNo ratings yet

- BSBA Marketing 1Document2 pagesBSBA Marketing 1Abdu YaYa AbeshaNo ratings yet

- OB Chapter 6Document51 pagesOB Chapter 6Abdu YaYa AbeshaNo ratings yet

- Chapter Two INTERNATIONALDocument12 pagesChapter Two INTERNATIONALAbdu YaYa AbeshaNo ratings yet

- OB Chapter 5Document37 pagesOB Chapter 5Abdu YaYa AbeshaNo ratings yet

- Marketing UNIT Five ComprehensiveDocument70 pagesMarketing UNIT Five ComprehensiveAbdu YaYa AbeshaNo ratings yet

- HRMMMMMMMDocument6 pagesHRMMMMMMMAbdu YaYa AbeshaNo ratings yet

- Macroeconomics Chapter - 2 (Two) pdf6kDocument12 pagesMacroeconomics Chapter - 2 (Two) pdf6kAbdu YaYa AbeshaNo ratings yet

- Chapter 1-Accounting in ActionDocument49 pagesChapter 1-Accounting in ActionAbdu YaYa AbeshaNo ratings yet

- Chapter 3 - Organization of A Computer SystemsDocument7 pagesChapter 3 - Organization of A Computer SystemsAbdu YaYa AbeshaNo ratings yet

- ECONOMICSSSSSSSSSSSSSSSDocument12 pagesECONOMICSSSSSSSSSSSSSSSAbdu YaYa AbeshaNo ratings yet

- CMA Individual Assignment 1 & 2Document3 pagesCMA Individual Assignment 1 & 2Abdu YaYa Abesha100% (2)

- MAR50 No FaqDocument39 pagesMAR50 No FaqRenu MundhraNo ratings yet

- Internal Audit Report ABCDocument3 pagesInternal Audit Report ABCSalsa ArdilaNo ratings yet

- Comprehensive Audit Problem Julie AngeloDocument8 pagesComprehensive Audit Problem Julie AngeloAnonymous LC5kFdtcNo ratings yet

- Study Notes - Internal ControlDocument4 pagesStudy Notes - Internal ControlJohn Mark EramilNo ratings yet

- Incremental Analysis QiuzzerDocument4 pagesIncremental Analysis QiuzzerMa Teresa B. CerezoNo ratings yet

- Accounts 2019 FinalDocument210 pagesAccounts 2019 FinalPrashant Singh100% (1)

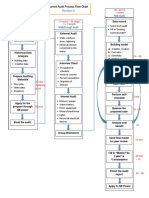

- Revision 2 - Current Audit Process Flow ChartDocument1 pageRevision 2 - Current Audit Process Flow ChartVy ThoaiNo ratings yet

- Chapter 7 Internal Control: True/False QuestionsDocument20 pagesChapter 7 Internal Control: True/False QuestionsashlyNo ratings yet

- CLINTON FOUNDATION - Charles Ortel Audit General - ExhibitsDocument29 pagesCLINTON FOUNDATION - Charles Ortel Audit General - ExhibitsBigMamaTEANo ratings yet

- Review of Modern Inventory Management Techniques: September 2016Document23 pagesReview of Modern Inventory Management Techniques: September 2016Mohamad SyafiqNo ratings yet

- Aeb SM CH14 1Document28 pagesAeb SM CH14 1fitriNo ratings yet

- Citizen S CharterDocument46 pagesCitizen S CharterEunicaNo ratings yet

- Purchasing Cycle NarrativeDocument1 pagePurchasing Cycle NarrativeSunny MaeNo ratings yet

- Ca Inter C0 Audit Question Bank NewDocument14 pagesCa Inter C0 Audit Question Bank NewDaanish Mittal100% (1)

- Unit 5. Verification and Valuation of Assets and LiabilitiesDocument16 pagesUnit 5. Verification and Valuation of Assets and LiabilitiesAmit PatelNo ratings yet

- Request Letter For Internal AuditDocument1 pageRequest Letter For Internal Auditali100% (1)

- 5.45 Inventory Management ProcedureDocument4 pages5.45 Inventory Management ProcedureRhozeiah LeiahNo ratings yet

- Foreclosure - New York DiscoveryDocument25 pagesForeclosure - New York Discoverywinstons2311100% (2)

- Checklist & Guideline ISO 22000Document14 pagesChecklist & Guideline ISO 22000Documentos Tecnicos75% (4)

- Cert IPSAS BrochureDocument2 pagesCert IPSAS BrochureMù SênNo ratings yet

- Quiz Auditing II Before Midtest Ubakrie April 23, 2021Document9 pagesQuiz Auditing II Before Midtest Ubakrie April 23, 2021Wisnu Aldi WibowoNo ratings yet

- MBA Health and Hospital Management Course StructureDocument2 pagesMBA Health and Hospital Management Course StructureMunir DayaniNo ratings yet

- Qapm Issue 4, Rev 0, March 2016Document284 pagesQapm Issue 4, Rev 0, March 2016Sujoy Ghosh100% (2)

- A Case Study On Fraudulent Financial Reporting Evidence From MalaysiaDocument16 pagesA Case Study On Fraudulent Financial Reporting Evidence From MalaysiaIsmail WardhanaNo ratings yet

- Cost-Effective Stores Management: DR .Saleh Salem GhnaemDocument7 pagesCost-Effective Stores Management: DR .Saleh Salem GhnaemhichamlamNo ratings yet

- Shelf StockerDocument1 pageShelf StockerShirley AribeNo ratings yet

- EDP Auditing SemiFinalDocument4 pagesEDP Auditing SemiFinalErwin Labayog MedinaNo ratings yet