Download as pdf or txt

You might also like

- Basel III Endgame 1682938205Document147 pagesBasel III Endgame 1682938205rpk51088No ratings yet

- Analyzing Banking Risk (Fourth Edition): A Framework for Assessing Corporate Governance and Risk ManagementFrom EverandAnalyzing Banking Risk (Fourth Edition): A Framework for Assessing Corporate Governance and Risk ManagementRating: 5 out of 5 stars5/5 (5)

- Islamic and Conventional Banking Comparative Analysis, Pakistan's PerspectiveDocument91 pagesIslamic and Conventional Banking Comparative Analysis, Pakistan's PerspectiveSaid Ali93% (15)

- ICRRS Guidelines - BB - Version 2.0Document25 pagesICRRS Guidelines - BB - Version 2.0Optimistic EyeNo ratings yet

- The Pious Caliphs: Abdullah, Abu Bakr As-SiddiqDocument4 pagesThe Pious Caliphs: Abdullah, Abu Bakr As-SiddiqMerima100% (2)

- Resolving NPL Report - enDocument61 pagesResolving NPL Report - enlidia012No ratings yet

- Europe Central BankDocument82 pagesEurope Central BankYasmeen KhuhroNo ratings yet

- SSM Assetqualityreviewmanual201806 enDocument295 pagesSSM Assetqualityreviewmanual201806 ensubmarinoaguadulceNo ratings yet

- ICAAP Sllovenia GuidelineDocument44 pagesICAAP Sllovenia GuidelineDritaNo ratings yet

- Guideline On Stress Testing For Nigerian BanksDocument30 pagesGuideline On Stress Testing For Nigerian BanksAgwu Obinna0% (1)

- Final Guidelines On Accounting For Expected Credit Losses (EBA-GL-2017-06)Document88 pagesFinal Guidelines On Accounting For Expected Credit Losses (EBA-GL-2017-06)Alejandro SanchezNo ratings yet

- J12961 GPPC Merged sg3 LKDDocument53 pagesJ12961 GPPC Merged sg3 LKDGab RielNo ratings yet

- Guide To Assessments of Licence ApplicationsDocument36 pagesGuide To Assessments of Licence ApplicationsSupriyo BhattacharjeeNo ratings yet

- Discussion Paper On The Significant Risk Transfer in Securitisation (EBA-DP-2017-03)Document155 pagesDiscussion Paper On The Significant Risk Transfer in Securitisation (EBA-DP-2017-03)Robin MichaelNo ratings yet

- Guidelines On Credit Risk ManagementDocument99 pagesGuidelines On Credit Risk ManagementVallabh Utpat100% (1)

- SSM - NPL Addendum 201803.enDocument12 pagesSSM - NPL Addendum 201803.enPhilippe St-cyrNo ratings yet

- En Improving Internal Control CampionDocument82 pagesEn Improving Internal Control Campionmogemboo100% (1)

- MCOM-I 101 (English Medium)Document264 pagesMCOM-I 101 (English Medium)kousik sadhuNo ratings yet

- CAR18 chpt4Document59 pagesCAR18 chpt4Charles HouedjissiNo ratings yet

- Financial Sector Assessment: Rakesh MohanDocument68 pagesFinancial Sector Assessment: Rakesh MohanbichgatiNo ratings yet

- Rar HDFC Bank 2014Document32 pagesRar HDFC Bank 2014Moneylife Foundation100% (1)

- Final Guidelines On Risk Factors (JC 2017 37)Document108 pagesFinal Guidelines On Risk Factors (JC 2017 37)Georgio RomaniNo ratings yet

- Accounting Theory Ch02Document36 pagesAccounting Theory Ch02Deema JadNo ratings yet

- Guidelines IRRBB 000Document19 pagesGuidelines IRRBB 000Sam SinhaNo ratings yet

- Springerbriefs in Finance: For Further VolumesDocument58 pagesSpringerbriefs in Finance: For Further VolumesdarioNo ratings yet

- SSM Reportrecoveryplans201807 enDocument43 pagesSSM Reportrecoveryplans201807 enmguerra1282No ratings yet

- 20080618b ValuationDocument26 pages20080618b ValuationgrobbebolNo ratings yet

- Coordinated Supervision PDFDocument32 pagesCoordinated Supervision PDFmoidul ISLAMNo ratings yet

- ACCA2 1 Handout No. 1 - Conceptual Framework For Financial ReportingDocument3 pagesACCA2 1 Handout No. 1 - Conceptual Framework For Financial ReportingZia May LauretaNo ratings yet

- FSI Insights: Financial Stability InstituteDocument54 pagesFSI Insights: Financial Stability InstituteKathan RajNo ratings yet

- Tabagari Salome MSC 2015Document44 pagesTabagari Salome MSC 2015George MartinNo ratings yet

- MORBBANKODocument84 pagesMORBBANKOocssantiagoNo ratings yet

- Quiz 1. Conceptual Framework and Accounting Standards: PointsDocument21 pagesQuiz 1. Conceptual Framework and Accounting Standards: PointsMarcus MonocayNo ratings yet

- Basel Committee BCBS Report On 2023 Banking Turmoil 1696540214Document36 pagesBasel Committee BCBS Report On 2023 Banking Turmoil 1696540214basharkhateeb112No ratings yet

- Q323 Shareholders Report-EnDocument92 pagesQ323 Shareholders Report-EndavidbayatNo ratings yet

- Ed Conceptual Framework For Fin ReportingDocument50 pagesEd Conceptual Framework For Fin ReportingMichele VallaroNo ratings yet

- Evaluation of The Effects of Too-Big-To-Fail Reforms: Final ReportDocument160 pagesEvaluation of The Effects of Too-Big-To-Fail Reforms: Final ReportThabiso MtimkuluNo ratings yet

- ICRA Securitisation Rating Methodology PDFDocument32 pagesICRA Securitisation Rating Methodology PDFShivani AgarwalNo ratings yet

- Basel Committee On Banking SupervisionDocument24 pagesBasel Committee On Banking SupervisionAditya BajoriaNo ratings yet

- Financial Sector Advisory Centre (Finsac) : Loan Classification and Provisioning: Current Practices in 26 CountriesDocument42 pagesFinancial Sector Advisory Centre (Finsac) : Loan Classification and Provisioning: Current Practices in 26 CountriesTom, Dick and HarryNo ratings yet

- General Presentation On The New Format of The Audit ReportDocument9 pagesGeneral Presentation On The New Format of The Audit ReportIoana HMNo ratings yet

- Draft Mapping Report - FitchDocument40 pagesDraft Mapping Report - FitchJOAONo ratings yet

- CRM Current PracticesDocument35 pagesCRM Current Practicessh_chandraNo ratings yet

- Examguide PDFDocument1,044 pagesExamguide PDFMāhmõūd ĀhmēdNo ratings yet

- 2021 04 28 Kam Lessons LearnedDocument16 pages2021 04 28 Kam Lessons LearnedSherlyn Chong Yan KayNo ratings yet

- FINAL DECISION NOTICE Sanctions Against UHY Hacker Young and Martin Jones in Relation To Laura Ashley Holdings 13 07 22Document67 pagesFINAL DECISION NOTICE Sanctions Against UHY Hacker Young and Martin Jones in Relation To Laura Ashley Holdings 13 07 22Abdelmadjid djibrineNo ratings yet

- FaC ProjectDocument20 pagesFaC ProjectPaula RamosNo ratings yet

- Guide For Evaluation Procedures For Employment of Consultants Under Japanese Oda LoansDocument44 pagesGuide For Evaluation Procedures For Employment of Consultants Under Japanese Oda LoansMin Chan MoonNo ratings yet

- COMPLAINTS MANAGEMENT STANDARD OPERATING GUIDELINES Updated December 2022 1Document23 pagesCOMPLAINTS MANAGEMENT STANDARD OPERATING GUIDELINES Updated December 2022 1Razbir RayhanNo ratings yet

- 2024 L1 FsaDocument108 pages2024 L1 Fsahamna wahabNo ratings yet

- Regulatory and Supervisory Developments For Non-Performing LoansDocument8 pagesRegulatory and Supervisory Developments For Non-Performing LoansTom, Dick and HarryNo ratings yet

- Exploring Green Finance Incentives in ChinaDocument71 pagesExploring Green Finance Incentives in Chinangocmyduyen3107No ratings yet

- CPAT Reviewer - Key Audit MattersDocument3 pagesCPAT Reviewer - Key Audit MattersZaaavnn VannnnnNo ratings yet

- Design and Testing of Overdraft Disclosures: Phase Two: Board of Governors of The Federal Reserve SystemDocument57 pagesDesign and Testing of Overdraft Disclosures: Phase Two: Board of Governors of The Federal Reserve Systembret10No ratings yet

- Draft RTS On Shadow Banking EntitiesDocument75 pagesDraft RTS On Shadow Banking EntitiesEirini KoufakiNo ratings yet

- Ebook Rating DefDocument65 pagesEbook Rating DefChiara MateraNo ratings yet

- Pillar3 ENGDocument133 pagesPillar3 ENGInternal AuditNo ratings yet

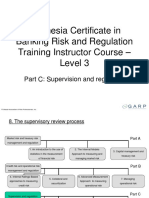

- Indonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3Document46 pagesIndonesia Certificate in Banking Risk and Regulation Training Instructor Course - Level 3endro suendroNo ratings yet

- Icici Bank Rar 2015Document42 pagesIcici Bank Rar 2015Moneylife Foundation0% (1)

- World Development Report 2022: Finance for an Equitable RecoveryFrom EverandWorld Development Report 2022: Finance for an Equitable RecoveryNo ratings yet

- Appendix B IFRS S2 Sample WorksheetDocument2 pagesAppendix B IFRS S2 Sample WorksheetcontactpulkitagarwalNo ratings yet

- IAS 12 PG 87Document1 pageIAS 12 PG 87contactpulkitagarwalNo ratings yet

- Appendix A IFRS S1 Sample WorksheetDocument4 pagesAppendix A IFRS S1 Sample WorksheetcontactpulkitagarwalNo ratings yet

- Pricing Mechanisms - Paul Hastings - PWCDocument8 pagesPricing Mechanisms - Paul Hastings - PWCcontactpulkitagarwalNo ratings yet

- Bank FinTech Online Study Pack 2020Document41 pagesBank FinTech Online Study Pack 2020contactpulkitagarwalNo ratings yet

- @accaleaks F9-BPP PassCardsDocument129 pages@accaleaks F9-BPP PassCardscontactpulkitagarwalNo ratings yet

- 1.2 Walker (Introduction To The City of London)Document13 pages1.2 Walker (Introduction To The City of London)contactpulkitagarwalNo ratings yet

- #MeToo in #MA - Introducing The Weinstein Warranty - Corporate - Commercial Law - AustraliaDocument2 pages#MeToo in #MA - Introducing The Weinstein Warranty - Corporate - Commercial Law - AustraliacontactpulkitagarwalNo ratings yet

- 2.1 Prof G A Walker (International Financial Markets) Summary DiagramDocument3 pages2.1 Prof G A Walker (International Financial Markets) Summary DiagramcontactpulkitagarwalNo ratings yet

- Nineteenth Century Philippines GEC109Document7 pagesNineteenth Century Philippines GEC109Nashebah A. BatuganNo ratings yet

- Annotated BibliographyDocument4 pagesAnnotated Bibliographyapi-340395866No ratings yet

- The Iranian Deep State: Understanding The Politics of Transition in The Islamic RepublicDocument24 pagesThe Iranian Deep State: Understanding The Politics of Transition in The Islamic RepublicHoover InstitutionNo ratings yet

- Water Quality Monitoring in Nigeria Case Study of Nigeria's Industrial CitiesDocument7 pagesWater Quality Monitoring in Nigeria Case Study of Nigeria's Industrial CitiesJaime SalguerroNo ratings yet

- Unfair LabourDocument1 pageUnfair LabourDivya ShekhawatNo ratings yet

- Thailand Visa Application FormDocument1 pageThailand Visa Application FormAjay KumarNo ratings yet

- The PRESIDENT FERDINAND RDocument40 pagesThe PRESIDENT FERDINAND RInes Flordelis RonquilloNo ratings yet

- Reading in The Philippine History Final ExamDocument5 pagesReading in The Philippine History Final ExamMARK 2020No ratings yet

- Revision of The EU Insolvency Regulation What Type of FaceliftDocument14 pagesRevision of The EU Insolvency Regulation What Type of FaceliftCornel TatuNo ratings yet

- Contribution Beneficial Financial Critically Enormously SolutionDocument3 pagesContribution Beneficial Financial Critically Enormously SolutionAnh Quân LêNo ratings yet

- Ra 9175 Chainsaw ActDocument5 pagesRa 9175 Chainsaw ActjayinthelongrunNo ratings yet

- Ballard Partners Opens Office in Ft. Lauderdale, Elite Fundraiser Stephanie Grutman Joins TeamDocument1 pageBallard Partners Opens Office in Ft. Lauderdale, Elite Fundraiser Stephanie Grutman Joins TeamCoreMessageNo ratings yet

- Allan Ignacio L. Sia III Gelitph - Y26 12044261: Short Critical Essay #4Document2 pagesAllan Ignacio L. Sia III Gelitph - Y26 12044261: Short Critical Essay #4Ark TresNo ratings yet

- The National Flag of VNDocument16 pagesThe National Flag of VNdinh son myNo ratings yet

- DZLIFT - Second Instalment CIA Fund Request - TC (Pakokku)Document4 pagesDZLIFT - Second Instalment CIA Fund Request - TC (Pakokku)Zin Min TunNo ratings yet

- MFIT2Document1 pageMFIT2rathiramsha7No ratings yet

- Labor CaseDocument11 pagesLabor CaseAnne AjednemNo ratings yet

- 3rd World Radical Technology 1977Document310 pages3rd World Radical Technology 1977conanjNo ratings yet

- Class 8 Civics Chapter 3 Extra Questions and Answers Why Do We Need A ParliamentDocument7 pagesClass 8 Civics Chapter 3 Extra Questions and Answers Why Do We Need A ParliamentTanuj100% (1)

- Western Political Thought & Political Theory-1Document79 pagesWestern Political Thought & Political Theory-1Nani Chowdary100% (3)

- Atienza Vs BrillantesDocument12 pagesAtienza Vs BrillantesPaolo AdalemNo ratings yet

- 3-Development of Education During British Period in IndiaDocument3 pages3-Development of Education During British Period in IndiaSeharNo ratings yet

- BE 2019 Course Fiber Optics Lab (404195)Document6 pagesBE 2019 Course Fiber Optics Lab (404195)Pratibha KulkarniNo ratings yet

- Unit 15Document24 pagesUnit 15mrsaritrahassanNo ratings yet

- Lecturer Selection Grade For Pre 1986 Retired College ProfessorsDocument3 pagesLecturer Selection Grade For Pre 1986 Retired College ProfessorsVenkatakrishnan IyerNo ratings yet

- Berlin Wall HISTORYDocument1 pageBerlin Wall HISTORYDip PerNo ratings yet

- Sociology Past PaperDocument2 pagesSociology Past PaperAbdul Quadri33% (3)

- Img 0002Document1 pageImg 0002api-338270828No ratings yet

- Certified List of Candidates For Congressional and Local Positions For The May 13, 2013 2013 National, Local and Armm ElectionsDocument2 pagesCertified List of Candidates For Congressional and Local Positions For The May 13, 2013 2013 National, Local and Armm ElectionsSunStar Philippine NewsNo ratings yet