Download as pdf or txt

You might also like

- Sharon Zukin-The Cultures of Cities-Blackwell (1995)Document338 pagesSharon Zukin-The Cultures of Cities-Blackwell (1995)Lilia Nenescu81% (16)

- Contract Review-QMP-MK-01Document5 pagesContract Review-QMP-MK-01Rohit VishwakarmaNo ratings yet

- A STUDY On Industrial RelationsDocument53 pagesA STUDY On Industrial RelationsVenkat66% (29)

- 1 s2.0 S0301479724002160 MainDocument12 pages1 s2.0 S0301479724002160 MainAmna NoorNo ratings yet

- Research Methodology Ciaaa (1) - 1-10Document10 pagesResearch Methodology Ciaaa (1) - 1-10Vanishree senthil kumaranNo ratings yet

- Manage Decis Econ - 2021 - Li - Does Environmental Corporate Social Responsibility ECSR Promote Green Product and ProcessDocument9 pagesManage Decis Econ - 2021 - Li - Does Environmental Corporate Social Responsibility ECSR Promote Green Product and Processhuazhou bushizhouNo ratings yet

- Moderating Effect of Social Uncertainty Between Capital Budgeting Practices and PerformanceDocument17 pagesModerating Effect of Social Uncertainty Between Capital Budgeting Practices and PerformanceBatool HuzaifahNo ratings yet

- Research Methodology CiaaaDocument10 pagesResearch Methodology CiaaaVanishree senthil kumaranNo ratings yet

- Zeyun-Li 2022Document18 pagesZeyun-Li 2022maianoviNo ratings yet

- Research in International Business and Finance: Full Length ArticleDocument9 pagesResearch in International Business and Finance: Full Length ArticleMuhammad RamzanNo ratings yet

- Accepted Manuscript: J. of Multi. Fin. ManagDocument35 pagesAccepted Manuscript: J. of Multi. Fin. ManagRajulut TaqwaNo ratings yet

- ESG Factors by Mutual Funds in South AfricaDocument15 pagesESG Factors by Mutual Funds in South AfricaSimaNo ratings yet

- RM CiaDocument8 pagesRM CiaVanishree senthil kumaranNo ratings yet

- 2023 ESG Performance and Investment Efficiency The Impact of Information AsymmetryDocument55 pages2023 ESG Performance and Investment Efficiency The Impact of Information AsymmetryAhmed EldemiryNo ratings yet

- External and Internal Economic Impacts PDFDocument9 pagesExternal and Internal Economic Impacts PDFDionisius Joachim Marcello Vincent JonathanNo ratings yet

- Esg 11Document22 pagesEsg 11anubha srivastavaNo ratings yet

- Bus Strat Env - 2022 - Zhou - Sustainable Development ESG Performance and Company Market Value Mediating Effect ofDocument17 pagesBus Strat Env - 2022 - Zhou - Sustainable Development ESG Performance and Company Market Value Mediating Effect ofadilNo ratings yet

- 1 s2.0 S014098832400224X MainDocument11 pages1 s2.0 S014098832400224X MainonlyshakilNo ratings yet

- Green Finance PaperDocument18 pagesGreen Finance PaperMeghna PurohitNo ratings yet

- Analysis of The Use of Corporate Social Responsibility Funds On The Profitability of Banks Listed On The Idx For The 2017-2021 PeriodDocument15 pagesAnalysis of The Use of Corporate Social Responsibility Funds On The Profitability of Banks Listed On The Idx For The 2017-2021 Periodindex PubNo ratings yet

- Greenwashing in Environmental, Social and Governance Disclosures From Ellen YuDocument68 pagesGreenwashing in Environmental, Social and Governance Disclosures From Ellen YuJovanaNo ratings yet

- Subsidy Expiration and Greenwashing Decision Is There A Ro - 2023 - Energy EconDocument11 pagesSubsidy Expiration and Greenwashing Decision Is There A Ro - 2023 - Energy Econabdelali ELFAIZNo ratings yet

- Challenges and Trends in Sustainable Corporate Finance: A Bibliometric Systematic ReviewDocument27 pagesChallenges and Trends in Sustainable Corporate Finance: A Bibliometric Systematic ReviewKishan MishraNo ratings yet

- Can The Spending of Corporate Social Responsibility Be Offset? Evidence From Pharmaceutical IndustryDocument26 pagesCan The Spending of Corporate Social Responsibility Be Offset? Evidence From Pharmaceutical IndustryAnirudh bhardwajNo ratings yet

- Do Environmental, Social and Corporate Governance Practices Enhance Malaysian Public-Listed Companies Performance?Document28 pagesDo Environmental, Social and Corporate Governance Practices Enhance Malaysian Public-Listed Companies Performance?Li Chen LeeNo ratings yet

- The Impact of Green Financial Development On Stock Price Crash Risk From The Perspective of Information Asymmetry in Chinese Listed CompaniesDocument16 pagesThe Impact of Green Financial Development On Stock Price Crash Risk From The Perspective of Information Asymmetry in Chinese Listed CompaniesjoglofansNo ratings yet

- 1 s2.0 S2405844023035089 MainDocument12 pages1 s2.0 S2405844023035089 Mainwiem chibaNo ratings yet

- Financial Knowledge, Risk Attitude, Access AttitudeDocument14 pagesFinancial Knowledge, Risk Attitude, Access AttitudeRatnawati AbdullahNo ratings yet

- Fenvs 10 1033868Document14 pagesFenvs 10 1033868atiqNo ratings yet

- ESG Performance and Disclosure A Cross-Country AnalysisDocument45 pagesESG Performance and Disclosure A Cross-Country Analysis111 333No ratings yet

- A Study of The Relationship Between Corporate Social Responsibility Report and TheDocument18 pagesA Study of The Relationship Between Corporate Social Responsibility Report and TheunibooksNo ratings yet

- ESG Performance and Ownership Structure On Cost of Capital and Research & Development InvestmentDocument18 pagesESG Performance and Ownership Structure On Cost of Capital and Research & Development Investmentasri_lutfianiNo ratings yet

- Kinerja Lingkungan Ke Kinerja Keuangan Dengan Corporate Governance Sebagai Variabel ModerasiDocument11 pagesKinerja Lingkungan Ke Kinerja Keuangan Dengan Corporate Governance Sebagai Variabel ModerasiWakis SamuelwijarNo ratings yet

- Sustainability and Firm Performance The Role of Environmental Social and Governance Disclosure and Green InnovationManagement DecisionDocument20 pagesSustainability and Firm Performance The Role of Environmental Social and Governance Disclosure and Green InnovationManagement DecisionsaritaNo ratings yet

- ESG Performance, Capital Financing Decisions, and Audit Quality: Empirical Evidence From Chinese State Owned EnterprisesDocument14 pagesESG Performance, Capital Financing Decisions, and Audit Quality: Empirical Evidence From Chinese State Owned EnterprisesYanto LieNo ratings yet

- Bus Strat Env - 2021 - Singh - Stakeholder Pressure Green Innovation and Performance in Small and Medium SizedDocument15 pagesBus Strat Env - 2021 - Singh - Stakeholder Pressure Green Innovation and Performance in Small and Medium SizedFlying Dutchman2020No ratings yet

- Chen 2019Document22 pagesChen 2019upiNo ratings yet

- The Impact of Green Financial Development On StockDocument17 pagesThe Impact of Green Financial Development On StockNguyễn Hà TrangNo ratings yet

- Corporates Sustainability Disclosures Impact On Cost of Capital and Idisyncratic RiskDocument26 pagesCorporates Sustainability Disclosures Impact On Cost of Capital and Idisyncratic RiskPoly Machinery AccountNo ratings yet

- The Effects of Green Banking Practices On Financial Performance of Listed Banking Companies in BangladeshDocument9 pagesThe Effects of Green Banking Practices On Financial Performance of Listed Banking Companies in BangladeshDebora Evianti Lumban TobingNo ratings yet

- FDI in Emerging Asia and Its Impact On EnvironmentDocument4 pagesFDI in Emerging Asia and Its Impact On Environmentroad_chikenNo ratings yet

- 3 Indian JIntegrated RSCH L1Document11 pages3 Indian JIntegrated RSCH L1hikarunonchessNo ratings yet

- Does Corporate Green Investment Enhance Profitability An Institutional PerspectiveDocument25 pagesDoes Corporate Green Investment Enhance Profitability An Institutional Perspectivemuhamaad.ali.javedNo ratings yet

- The Relationship Between Non-Financial Reporting, Environmental Strategies and Financial Performance. Empirical Evidence From Milano Stock ExchangeDocument9 pagesThe Relationship Between Non-Financial Reporting, Environmental Strategies and Financial Performance. Empirical Evidence From Milano Stock ExchangeRima LaaouinaNo ratings yet

- Ijfs 9020022Document16 pagesIjfs 9020022Abhishree JainNo ratings yet

- Corporate Social ResponsibilityDocument11 pagesCorporate Social ResponsibilityZafir Ullah KhanNo ratings yet

- Case Study ReportDocument7 pagesCase Study ReportabnerrrNo ratings yet

- Does Environmental Social and Governance Performance Affect Financial Risk Disclosure Evidence From European ESG CompaniesDocument20 pagesDoes Environmental Social and Governance Performance Affect Financial Risk Disclosure Evidence From European ESG Companiespranitis gnNo ratings yet

- Research ProposalDocument7 pagesResearch ProposalHassan TariqNo ratings yet

- The Impact of Environmental, Social, Governance (ESG) Factors On Stock Prices and Corporate PerformanceDocument5 pagesThe Impact of Environmental, Social, Governance (ESG) Factors On Stock Prices and Corporate Performancesrivastavakarishma18No ratings yet

- Journal of Economics and BusinessDocument17 pagesJournal of Economics and BusinessFachrul RoziNo ratings yet

- Journal 2022Document12 pagesJournal 2022Khadija YaqoobNo ratings yet

- ESG in Vietnam 2023Document45 pagesESG in Vietnam 2023Kim ÁnhNo ratings yet

- Corporate Responsibility Disclosure, Information Environment and Analysts' Recommendations: Evidence From MalaysiaDocument27 pagesCorporate Responsibility Disclosure, Information Environment and Analysts' Recommendations: Evidence From MalaysiaWan Nordin Wan HussinNo ratings yet

- Strategic Management Journal - 2013 - Cheng - Corporate Social Responsibility and Access To FinanceDocument23 pagesStrategic Management Journal - 2013 - Cheng - Corporate Social Responsibility and Access To FinancetnborgesNo ratings yet

- Formal Finance Usage and Innovative Smes: Evidence From Asean CountriesDocument19 pagesFormal Finance Usage and Innovative Smes: Evidence From Asean Countriesmenchong 123No ratings yet

- Khattak Et Al 2021 The Role of Entrepreneurial Finance in Corporate Social Responsibility and New Venture PerformanceDocument31 pagesKhattak Et Al 2021 The Role of Entrepreneurial Finance in Corporate Social Responsibility and New Venture PerformancediahNo ratings yet

- ESG - Indian MarketDocument6 pagesESG - Indian MarketMarisa LaokulrachNo ratings yet

- Fenvs 11 1127380Document16 pagesFenvs 11 1127380saoussen AGUIR EP BARGAOUINo ratings yet

- Esg or Not Esg? A Benchmarking AnalysisDocument10 pagesEsg or Not Esg? A Benchmarking AnalysisDevaNo ratings yet

- Capital Budgeting As A Tool of Management Decision Making: A Case Study of National Investment Bank LimitedDocument10 pagesCapital Budgeting As A Tool of Management Decision Making: A Case Study of National Investment Bank LimitedKun CupNo ratings yet

- بحث هااااااااااااااااااااااامDocument13 pagesبحث هااااااااااااااااااااااامSherif ElgoharyNo ratings yet

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveFrom EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveNo ratings yet

- Chapter 18Document23 pagesChapter 18LINH NGUYEN NGOC THUYNo ratings yet

- Chapter 7Document21 pagesChapter 7LINH NGUYEN NGOC THUYNo ratings yet

- Investing in The Early Stages of A Company: Venture CapitalDocument12 pagesInvesting in The Early Stages of A Company: Venture CapitalLINH NGUYEN NGOC THUYNo ratings yet

- Trắc nghiệm LTTCDocument269 pagesTrắc nghiệm LTTCLINH NGUYEN NGOC THUYNo ratings yet

- The Underlying Indicators of Good Governance in Vietnam: Review ArticleDocument13 pagesThe Underlying Indicators of Good Governance in Vietnam: Review ArticleLINH NGUYEN NGOC THUYNo ratings yet

- Mishkin Econ13e PPT 13Document41 pagesMishkin Econ13e PPT 13LINH NGUYEN NGOC THUYNo ratings yet

- Letter of Termination Contract: Subject: ( (Subject) )Document3 pagesLetter of Termination Contract: Subject: ( (Subject) )Duyen NguyenNo ratings yet

- INTL-728-Workbook Assignments For Final ReportDocument8 pagesINTL-728-Workbook Assignments For Final ReportDani GhansahNo ratings yet

- Mcdonals SOPM ReportDocument18 pagesMcdonals SOPM ReportAndleeb IrfanNo ratings yet

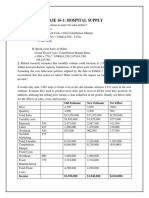

- Case 16-1: Hospital Supply: 1. What Is The Break-Even Volume in Units? in Sales Dollars?Document6 pagesCase 16-1: Hospital Supply: 1. What Is The Break-Even Volume in Units? in Sales Dollars?Lalit SapkaleNo ratings yet

- Asif Ahmed Ayon 1712987630 - Human Resource Management - Alternative Individual AssessmentDocument9 pagesAsif Ahmed Ayon 1712987630 - Human Resource Management - Alternative Individual AssessmentValak100% (1)

- Aslund - Reform TrapDocument21 pagesAslund - Reform TrapSanket ShrivastavaNo ratings yet

- West Meets East Agro Business Proposal DraftDocument16 pagesWest Meets East Agro Business Proposal DraftZarita Abu ZarinNo ratings yet

- STR Rishabh Bambha 089 Final PDFDocument59 pagesSTR Rishabh Bambha 089 Final PDFRishabh bambhaNo ratings yet

- Ar Darma Henwa 31121138Document388 pagesAr Darma Henwa 31121138SintyaNo ratings yet

- BuwevulugodafiwimigatDocument2 pagesBuwevulugodafiwimigatFair PrinceNo ratings yet

- Gopi Inventory-ManagementDocument9 pagesGopi Inventory-Managementvasantawada Gopi krishnaNo ratings yet

- Final Exam MAT1004 Summer Code 1Document3 pagesFinal Exam MAT1004 Summer Code 1Anh NguyễnNo ratings yet

- OGP 2025 Timetables B1 2025Document27 pagesOGP 2025 Timetables B1 2025Vikas KapoorNo ratings yet

- Presentation 1 LDDocument13 pagesPresentation 1 LDMaaz AliNo ratings yet

- Dwnload Full Physics For Scientists and Engineers Foundations and Connections Volume 2 1st Edition Katz Solutions Manual PDFDocument14 pagesDwnload Full Physics For Scientists and Engineers Foundations and Connections Volume 2 1st Edition Katz Solutions Manual PDFnicoledickersonwmncpoyefk100% (15)

- Document-Understanding Deconsolidation in SAP EWMDocument7 pagesDocument-Understanding Deconsolidation in SAP EWMAnonymous u3PhTjWZRNo ratings yet

- Engineering DepartmentDocument4 pagesEngineering DepartmentANKIT SINGHNo ratings yet

- Test Bank For M Finance 3rd Edition by CornettDocument36 pagesTest Bank For M Finance 3rd Edition by Cornettcorinneheroismf19wfo100% (42)

- Contract - RegularDocument5 pagesContract - Regularabanganjm08No ratings yet

- Ultratech Cement Limited Unit: Maihar Cement Works SarlanagarDocument1 pageUltratech Cement Limited Unit: Maihar Cement Works Sarlanagarjogender kumarNo ratings yet

- Assignment 01 Financial AccountingDocument3 pagesAssignment 01 Financial Accountingsehrish kayaniNo ratings yet

- Ecn 1100 Worksheet #3Document6 pagesEcn 1100 Worksheet #3Suraj SomaiNo ratings yet

- Brokers or TREC HoldersDocument8 pagesBrokers or TREC HoldersQamar ZamanNo ratings yet

- Week 4Document43 pagesWeek 4CHUA WEI JINNo ratings yet

- 2023 06 16 - LogDocument4 pages2023 06 16 - LogLuiza CorreaNo ratings yet

- Country Review - Unemployment Rate MidtermsDocument9 pagesCountry Review - Unemployment Rate MidtermsPamela MahinayNo ratings yet

- Week3 Intermediate1 - PracticeDocument12 pagesWeek3 Intermediate1 - PracticeRaj Kothari MNo ratings yet