Download as pdf or txt

You might also like

- Autodesk Invoice #9122128059 1.255,60Document1 pageAutodesk Invoice #9122128059 1.255,60Rambabu kNo ratings yet

- Wealth ManagementDocument14 pagesWealth Managementnikki karma100% (1)

- Determinants of Interest Rates (Revilla & Sanchez)Document12 pagesDeterminants of Interest Rates (Revilla & Sanchez)Kearn CercadoNo ratings yet

- IMS Proschool CFP EbookDocument140 pagesIMS Proschool CFP EbookNielesh AmbreNo ratings yet

- Retirement PlanningDocument11 pagesRetirement PlanningIan Miles TakawiraNo ratings yet

- Chapter 1: IntroductionDocument20 pagesChapter 1: IntroductionAlyn CheongNo ratings yet

- POF Individual AssignmentDocument5 pagesPOF Individual AssignmentMuhammad SaqlainNo ratings yet

- Annuity Sinking FundsDocument4 pagesAnnuity Sinking Fundsapi-645059243No ratings yet

- PFP Retirement Planning Unit 3 Bba IIIDocument13 pagesPFP Retirement Planning Unit 3 Bba IIIRaghuNo ratings yet

- Retirement PlanningDocument18 pagesRetirement PlanningsuryarathiNo ratings yet

- How To Make Your Retirement Kitty LastDocument1 pageHow To Make Your Retirement Kitty LastDurai NaiduNo ratings yet

- Retirement PlanningDocument3 pagesRetirement PlanningAarti GuptaNo ratings yet

- Assignment C - Lucy CookDocument4 pagesAssignment C - Lucy Cookapi-711725782No ratings yet

- CSE K Reading-Morton Niederjohn Thomas-Building WealthDocument17 pagesCSE K Reading-Morton Niederjohn Thomas-Building Wealthgraphicman1060No ratings yet

- BAFI3184 ASM1 s3818425 LyAnhTuan-2Document12 pagesBAFI3184 ASM1 s3818425 LyAnhTuan-2tuan ly100% (1)

- Are You Also Wasting Your Financial Potential?: If Only You Act Fast, You Too Can Surpass Your 'Ambitious' GoalsDocument13 pagesAre You Also Wasting Your Financial Potential?: If Only You Act Fast, You Too Can Surpass Your 'Ambitious' GoalskvijayasokNo ratings yet

- WM Unit 8 Retirement Planning 6th Jan 2022Document32 pagesWM Unit 8 Retirement Planning 6th Jan 2022Aarti GuptaNo ratings yet

- Project For Pension PlanDocument9 pagesProject For Pension PlanLakshmi DlaksNo ratings yet

- Financial: JourneysDocument4 pagesFinancial: Journeysapi-158508989No ratings yet

- Financial. PlanningDocument77 pagesFinancial. PlanningAmrit TejaniNo ratings yet

- Personal Financial PlanningDocument5 pagesPersonal Financial PlanningAyeshaNo ratings yet

- Self-Help Guidebook for Retirement Planning For Couples and Seniors: Ultimate Retirement Planning Book for Life after Paid EmploymentFrom EverandSelf-Help Guidebook for Retirement Planning For Couples and Seniors: Ultimate Retirement Planning Book for Life after Paid EmploymentNo ratings yet

- Retirement Planning for Beginners: A Comprehensive Guide to Building Savings, Maximizing Income, and Achieving Financial Security for Your Golden Years: Financial Planning Essentials, #1From EverandRetirement Planning for Beginners: A Comprehensive Guide to Building Savings, Maximizing Income, and Achieving Financial Security for Your Golden Years: Financial Planning Essentials, #1No ratings yet

- Retirement Planning Guide Book: Steering you Through Crucial Choices to Shape Your Ideal Retirement SuccessFrom EverandRetirement Planning Guide Book: Steering you Through Crucial Choices to Shape Your Ideal Retirement SuccessNo ratings yet

- FM Assignment2orignalDocument6 pagesFM Assignment2orignalHafiz AbdulwahabNo ratings yet

- The Details: 146 - IMAGE - IeDocument1 pageThe Details: 146 - IMAGE - IeJoanneTSmithNo ratings yet

- Full ReportDocument37 pagesFull ReportXiao TianNo ratings yet

- NOW I KNOW ! Cikaldana Newsletter No. 03-2015 (On Retirement Planning)Document5 pagesNOW I KNOW ! Cikaldana Newsletter No. 03-2015 (On Retirement Planning)CikaldanaNo ratings yet

- Retirement Plan 2Document11 pagesRetirement Plan 2Reign Ashley RamizaresNo ratings yet

- Lecture9 - ES301 Engineering EconomicsDocument19 pagesLecture9 - ES301 Engineering EconomicsLory Liza Bulay-ogNo ratings yet

- Module 3 Math1 Ge3Document10 pagesModule 3 Math1 Ge3orogrichchelynNo ratings yet

- Road Map For Investing SuccessDocument44 pagesRoad Map For Investing Successnguyentech100% (1)

- Chap 02Document25 pagesChap 02amatulmateennoorNo ratings yet

- CIA15 Study Guide12 Personal FinanceDocument16 pagesCIA15 Study Guide12 Personal FinanceAngelo SaayoNo ratings yet

- Research Agenda: Section 1. Article 287 of Presidential Decree No. 442, As Amended, Otherwise KnownDocument8 pagesResearch Agenda: Section 1. Article 287 of Presidential Decree No. 442, As Amended, Otherwise KnownFrancine Claire AbesamisNo ratings yet

- Retirement PlanDocument11 pagesRetirement PlanReign Ashley RamizaresNo ratings yet

- TVM & CompoundingDocument8 pagesTVM & CompoundingUday BansalNo ratings yet

- TMVTBDocument17 pagesTMVTBShantam RajanNo ratings yet

- Ifp 23 Estimating Retirement Needs and How Much Do You Need On RetirementDocument9 pagesIfp 23 Estimating Retirement Needs and How Much Do You Need On Retirementsachin_chawlaNo ratings yet

- Civil Engineering Construction and Graphics QUIZ#02 Topic:: Difference Between Simple and Compound InterestDocument14 pagesCivil Engineering Construction and Graphics QUIZ#02 Topic:: Difference Between Simple and Compound InteresttayyabNo ratings yet

- The Story of Rising Against MarketsDocument4 pagesThe Story of Rising Against MarketsDeuterNo ratings yet

- MalaDocument5 pagesMalaAruna MadasamyNo ratings yet

- FM I CH IiiDocument8 pagesFM I CH IiiDùķe HPNo ratings yet

- Middle in Come GroupDocument32 pagesMiddle in Come GroupVirdhi JoshiNo ratings yet

- Business FinanceDocument58 pagesBusiness FinanceCarmina DongcayanNo ratings yet

- The Time Value of MoneyDocument18 pagesThe Time Value of MoneyRaxelle MalubagNo ratings yet

- FP IntroductionDocument4 pagesFP IntroductionStellina JoeshibaNo ratings yet

- WM Unit 8 Retirement PlanningDocument21 pagesWM Unit 8 Retirement PlanningAarti GuptaNo ratings yet

- Math of Investment: Name: Joana Lhyn A. Rudas Gr/Sec: 11 HE (D)Document12 pagesMath of Investment: Name: Joana Lhyn A. Rudas Gr/Sec: 11 HE (D)eunha allaybanNo ratings yet

- JO1 - T Genchar E. Siroma Financial Literacy September 01, 2022 NCR Reflection PaperDocument1 pageJO1 - T Genchar E. Siroma Financial Literacy September 01, 2022 NCR Reflection PaperGenchar SiromaNo ratings yet

- FP Group WorkDocument12 pagesFP Group WorkStellina JoeshibaNo ratings yet

- Finance Chpter 5 Time Value of MoneyDocument11 pagesFinance Chpter 5 Time Value of MoneyOmar Ahmed ElkhalilNo ratings yet

- Chapter 4: Managing Your Money Lecture Notes Math 1030 Section CDocument7 pagesChapter 4: Managing Your Money Lecture Notes Math 1030 Section CChrisSantosNo ratings yet

- Fnce 220: Business Finance: Lecture 3: Time Value of MoneyDocument18 pagesFnce 220: Business Finance: Lecture 3: Time Value of MoneyVincent KamemiaNo ratings yet

- Chapter 12Document45 pagesChapter 12Angelo SaayoNo ratings yet

- The Magic of CompoundingDocument4 pagesThe Magic of Compoundingmaria gomezNo ratings yet

- MMW Financial Mathematics W62nd2021Presentation1Document34 pagesMMW Financial Mathematics W62nd2021Presentation1ILOVE MATURED FANSNo ratings yet

- Retirement PlanningDocument4 pagesRetirement Planningakshaygupta55555411No ratings yet

- Research JournalDocument7 pagesResearch Journalapi-549064431No ratings yet

- Rhetorical AnalysisDocument6 pagesRhetorical Analysisapi-549064431No ratings yet

- Final ReflectionDocument4 pagesFinal Reflectionapi-549064431No ratings yet

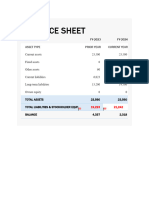

- Personal Balance SheetDocument4 pagesPersonal Balance Sheetapi-549064431No ratings yet

- Personal BudgetDocument1 pagePersonal Budgetapi-549064431No ratings yet

- CashDocument4 pagesCashapi-549064431No ratings yet

- Michael Platt (Financier)Document5 pagesMichael Platt (Financier)evangeliamartini2017No ratings yet

- 1 SMDocument9 pages1 SMReuben RichardNo ratings yet

- Wa0004.Document50 pagesWa0004.pradhanraja05679No ratings yet

- Discussion Forum Unit 1 University of The People BUS 2204-01 Personal Finance - AY2022 - T4 Instructor: Angela Wright 7 April 2022Document2 pagesDiscussion Forum Unit 1 University of The People BUS 2204-01 Personal Finance - AY2022 - T4 Instructor: Angela Wright 7 April 2022Karsa SambasNo ratings yet

- Chapters 20, 22 & 24Document59 pagesChapters 20, 22 & 24Manidipa BoseNo ratings yet

- Summative-TestDocument2 pagesSummative-TestChristian DequilatoNo ratings yet

- Cost Accounting: 6 EditionDocument13 pagesCost Accounting: 6 EditionGiannis SalaNo ratings yet

- 22 1184 ResolutionDocument3 pages22 1184 ResolutionTMJ4 NewsNo ratings yet

- Zimbabwe Banking Swift Codes: Here For AfricaDocument1 pageZimbabwe Banking Swift Codes: Here For AfricaTadiwanashe BurukaiNo ratings yet

- Gec 108 (Zaldivar Lesson 2)Document3 pagesGec 108 (Zaldivar Lesson 2)Drip KartelNo ratings yet

- Statistical Techniques in Business and Economics 16th Edition Lind Solutions ManualDocument19 pagesStatistical Techniques in Business and Economics 16th Edition Lind Solutions Manualsnuggerytamiliana4h2100% (26)

- Financial Markets 1Document8 pagesFinancial Markets 1Nicole Andrea BernabeNo ratings yet

- Day 5Document11 pagesDay 5KM HiềnNo ratings yet

- GHGGVG Data UploadedDocument3 pagesGHGGVG Data Uploadedshriya shettiwarNo ratings yet

- Enslaved African Labour by Andy HigginbottomDocument16 pagesEnslaved African Labour by Andy HigginbottomShih-Yu ChouNo ratings yet

- Uae Pharmacies Network List April 2014Document5 pagesUae Pharmacies Network List April 2014MD ABUL KHAYERNo ratings yet

- BFW2140 Lecture Week 2: Corporate Financial Mathematics IDocument33 pagesBFW2140 Lecture Week 2: Corporate Financial Mathematics Iaa TANNo ratings yet

- Successive Increase/ Decrease: PercentageDocument2 pagesSuccessive Increase/ Decrease: PercentageMadhu Sudhan NayakaNo ratings yet

- Chemical CompaniesDocument120 pagesChemical Companiestarun. crescentindiaNo ratings yet

- Back To The Future: A Review of The Latest Philippine Development Plan For 2023-2028Document17 pagesBack To The Future: A Review of The Latest Philippine Development Plan For 2023-2028Clark Hazel Timogan100% (1)

- Hubli DatabaseDocument20 pagesHubli Databaseshweta_gupta0718444No ratings yet

- Tax Invoice: Excitel Broadband Pvt. LTDDocument1 pageTax Invoice: Excitel Broadband Pvt. LTDMittal GalaxyNo ratings yet

- Practice+Test OverviewDocument2 pagesPractice+Test OverviewJuaymah MarieNo ratings yet

- Englishfor Studentsof EconomicsDocument217 pagesEnglishfor Studentsof EconomicsErkaiym ZhusupovaNo ratings yet

- Garrett RankingDocument14 pagesGarrett RankingCorey Wells88% (25)

- Sample/Pre-Board Paper 19 Class X Term 1 Exam Nov - Dec 2021 English Language and Literature (Code 184)Document5 pagesSample/Pre-Board Paper 19 Class X Term 1 Exam Nov - Dec 2021 English Language and Literature (Code 184)Tamil FutureNo ratings yet

- Uponor Thermo - Varia - 12 - 2012 - UK - 43028Document8 pagesUponor Thermo - Varia - 12 - 2012 - UK - 43028portocala12No ratings yet

- Understand The Submission Process To Local Authorities and External Technical Agencies For Property Development in MalaysiaDocument3 pagesUnderstand The Submission Process To Local Authorities and External Technical Agencies For Property Development in MalaysiastzlkNo ratings yet