Download as pdf or txt

You might also like

- Business Plan - SPECIAL TAHODocument17 pagesBusiness Plan - SPECIAL TAHOMia Casas60% (5)

- Tax 08 Gina OutlineDocument159 pagesTax 08 Gina OutlineCameron SnowdenNo ratings yet

- FINMAN Decision AnalysisDocument5 pagesFINMAN Decision AnalysisTrish GarridoNo ratings yet

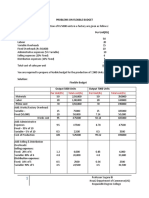

- Flexible BudgetDocument3 pagesFlexible BudgetJasdeep Singh Deepu0% (2)

- Illustration1: For The Production of 10000 Units of A Product, The Following Are The Budgeted ExpensesDocument4 pagesIllustration1: For The Production of 10000 Units of A Product, The Following Are The Budgeted ExpensesGabriel BelmonteNo ratings yet

- EC2101 Practice Problems 10 SolutionDocument3 pagesEC2101 Practice Problems 10 Solutiongravity_coreNo ratings yet

- Chapter 2 - Cost Terms, Concepts and ClassificationsDocument55 pagesChapter 2 - Cost Terms, Concepts and ClassificationsMarriel Fate CullanoNo ratings yet

- Budgetary ControlDocument7 pagesBudgetary ControlKuldeep NNo ratings yet

- MA CHAPTER 2 Budgeting Flexible BudgetDocument29 pagesMA CHAPTER 2 Budgeting Flexible BudgetMohd Zubair KhanNo ratings yet

- Budgetary ControlDocument7 pagesBudgetary ControlChinki ShahNo ratings yet

- Budgetory Control ContinuedDocument4 pagesBudgetory Control ContinuedFalak Falak fatimaNo ratings yet

- Assignment On BudgetingDocument5 pagesAssignment On BudgetingRameshNo ratings yet

- Ch8 PDFDocument11 pagesCh8 PDFGiang NguyenNo ratings yet

- Flexible Budget: ProblemsDocument3 pagesFlexible Budget: ProblemsRenu PoddarNo ratings yet

- Budgets & Budgetary ControlDocument10 pagesBudgets & Budgetary Controlsimranarora2007No ratings yet

- Flexible BudgetsDocument3 pagesFlexible Budgetsmansidalal45No ratings yet

- Budgeting OnlineDocument4 pagesBudgeting OnlineSoumendra RoyNo ratings yet

- Apr 18 Management Acc 2Document4 pagesApr 18 Management Acc 2Harish KapoorNo ratings yet

- Absorption & Marginal Costing-1Document6 pagesAbsorption & Marginal Costing-1田淼No ratings yet

- Budgetary Control NumericalDocument8 pagesBudgetary Control NumericalPuja AgarwalNo ratings yet

- Budgetory Control Flexible Budget With SolutionsDocument6 pagesBudgetory Control Flexible Budget With SolutionsJash SanghviNo ratings yet

- AFM-Session 25Document13 pagesAFM-Session 25abhijit.kundu23-25No ratings yet

- Requirement 1 Hypothetical Data Assumption: Company Name: Super Glass Bangles LLPDocument9 pagesRequirement 1 Hypothetical Data Assumption: Company Name: Super Glass Bangles LLPYahya ZafarNo ratings yet

- Requirement 1 Hypothetical Data Assumption: Company Name: Super Glass Bangles LLPDocument12 pagesRequirement 1 Hypothetical Data Assumption: Company Name: Super Glass Bangles LLPYahya ZafarNo ratings yet

- Unit 7 Budgeting SolutionsDocument15 pagesUnit 7 Budgeting SolutionsYogesh BandiNo ratings yet

- Flexible Budget Practical Problems & Solutions - Explanation & DiscussionDocument14 pagesFlexible Budget Practical Problems & Solutions - Explanation & DiscussionahmedNo ratings yet

- Management Accounting Problem Unit 5Document7 pagesManagement Accounting Problem Unit 5princeNo ratings yet

- Marginal Costing - Flexed BudgetDocument4 pagesMarginal Costing - Flexed BudgetMUSTHARI KHANNo ratings yet

- Measures of Leverage: Abhishek SinhaDocument30 pagesMeasures of Leverage: Abhishek Sinhadev guptaNo ratings yet

- Financial Plan (Illustration)Document6 pagesFinancial Plan (Illustration)Syed ArslanNo ratings yet

- Quiz 2Document2 pagesQuiz 2imagineimfNo ratings yet

- BudgetingDocument11 pagesBudgetingTanuj LalchandaniNo ratings yet

- MA Hasnain Ginwala PGP-21-025Document18 pagesMA Hasnain Ginwala PGP-21-025Shashank AgarwalaNo ratings yet

- Tut 8 - Management AccountingDocument29 pagesTut 8 - Management AccountingTao LoheNo ratings yet

- Solved Prblem of Budget PDFDocument9 pagesSolved Prblem of Budget PDFSweta PandeyNo ratings yet

- Solved Problems: OlutionDocument9 pagesSolved Problems: OlutionSweta PandeyNo ratings yet

- Flexible Budget #3Document2 pagesFlexible Budget #3Likith RNo ratings yet

- Financial Plan (Illustration)Document6 pagesFinancial Plan (Illustration)rana samiNo ratings yet

- Budegetory ControlDocument34 pagesBudegetory ControlDurdana NasserNo ratings yet

- Oroya Corporation - Oroya SegregationDocument8 pagesOroya Corporation - Oroya SegregationJULLIE CARMELLE H. CHATTONo ratings yet

- Slides of Lecture#09 Corporate Finance (FIN-622)Document4 pagesSlides of Lecture#09 Corporate Finance (FIN-622)sukhiesNo ratings yet

- Business Budget - Assignment ProblemsDocument3 pagesBusiness Budget - Assignment ProblemsSHARATH JNo ratings yet

- MAE RevisionDocument57 pagesMAE RevisionsaloniNo ratings yet

- Problem Unit 4Document7 pagesProblem Unit 4meenasaratha100% (1)

- Adobe Scan 01 Jul 2023Document5 pagesAdobe Scan 01 Jul 2023Faisal NawazNo ratings yet

- CVP AnalysisDocument5 pagesCVP AnalysisDwain pinakapogiNo ratings yet

- Sdathn Ripsryd@r@ea@pis - Unit) : - SolutionDocument16 pagesSdathn Ripsryd@r@ea@pis - Unit) : - SolutionAnimesh VoraNo ratings yet

- Responsiblity Accounting IllustrationDocument14 pagesResponsiblity Accounting IllustrationRianne NavidadNo ratings yet

- MGT AC - Prob-NewDocument276 pagesMGT AC - Prob-Newrandom122No ratings yet

- 5 Job CostingDocument22 pages5 Job CostingAbimanyu Shenil0% (1)

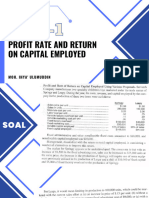

- Profit Rate and Return On Capital Employed: Moh. Ihya' UlumuddinDocument11 pagesProfit Rate and Return On Capital Employed: Moh. Ihya' UlumuddinKKM 37 2023No ratings yet

- Practice Q (Capital Budgeting)Document12 pagesPractice Q (Capital Budgeting)Divyam GargNo ratings yet

- Reggie's BudgetDocument5 pagesReggie's BudgetYazan AdamNo ratings yet

- Relevant CostingDocument23 pagesRelevant CostingEy GuanlaoNo ratings yet

- Marginal Costing - Module 3: Learning ObjectivesDocument111 pagesMarginal Costing - Module 3: Learning Objectives727822TPMB005 ARAVINTHAN.SNo ratings yet

- Chapter 7 and 9 Execises Problems - SolutionsDocument33 pagesChapter 7 and 9 Execises Problems - SolutionsVenus PalmencoNo ratings yet

- Lille Tissage WorksheetDocument19 pagesLille Tissage WorksheetJaouadiNo ratings yet

- DR Rachna Mahalwla - B.Com III Year Management Accounting Flexible BudgetingDocument6 pagesDR Rachna Mahalwla - B.Com III Year Management Accounting Flexible BudgetingSaumya JainNo ratings yet

- Midterms MADocument10 pagesMidterms MAJustz LimNo ratings yet

- Budgetary Control: BY Animesh Kalita 2K10MKT37Document15 pagesBudgetary Control: BY Animesh Kalita 2K10MKT37Animesh KalitaNo ratings yet

- Budget Format Sales Budget: Cash Collection Total Budgeted SalesDocument6 pagesBudget Format Sales Budget: Cash Collection Total Budgeted Salessernhaow_658673991No ratings yet

- Mcom QP Amd 40 MarksDocument2 pagesMcom QP Amd 40 Marksirfanahmed.dbaNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Kanban Change Leadership: Creating a Culture of Continuous ImprovementFrom EverandKanban Change Leadership: Creating a Culture of Continuous ImprovementNo ratings yet

- Azure Bootcamp Syllabus 1Document4 pagesAzure Bootcamp Syllabus 1MOHAIDEEN THARIQ MNo ratings yet

- Unit - 4Document26 pagesUnit - 4MOHAIDEEN THARIQ MNo ratings yet

- BIBLIOGRAPHY1Document11 pagesBIBLIOGRAPHY1MOHAIDEEN THARIQ MNo ratings yet

- 16528/yesvantpur Exp Sleeper Class (SL)Document2 pages16528/yesvantpur Exp Sleeper Class (SL)MOHAIDEEN THARIQ MNo ratings yet

- Health Clinic Template Blank ReportDocument4 pagesHealth Clinic Template Blank ReportMOHAIDEEN THARIQ MNo ratings yet

- Types of Bank AccountsDocument3 pagesTypes of Bank AccountsAkshay BhasinNo ratings yet

- Cash FlowDocument23 pagesCash FlowSundara BalamuruganNo ratings yet

- Doctrine of Lifting of or Piercing The Corporate VeilDocument5 pagesDoctrine of Lifting of or Piercing The Corporate VeilNiraj Dhar DubeyNo ratings yet

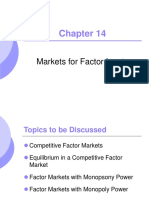

- Markets For Factor InputsDocument87 pagesMarkets For Factor InputsDesiSelviaNo ratings yet

- Compensation ManagementDocument17 pagesCompensation ManagementPooja DhingraNo ratings yet

- Reading List First Semester 2017-2018Document15 pagesReading List First Semester 2017-2018NajjaSheriff007No ratings yet

- BMS FM SDF 2012-13Document127 pagesBMS FM SDF 2012-13Digvijay KakuleNo ratings yet

- 0452 Accounting: MARK SCHEME For The October/November 2012 SeriesDocument10 pages0452 Accounting: MARK SCHEME For The October/November 2012 SeriesJoel GwenereNo ratings yet

- Cost Accounting MethodsDocument26 pagesCost Accounting MethodsshaimaNo ratings yet

- General Technologies Group LTD.: CASE 2.5Document9 pagesGeneral Technologies Group LTD.: CASE 2.5Hana Amalia VirantiNo ratings yet

- Decision Tree AnalysisDocument9 pagesDecision Tree AnalysisRhett SageNo ratings yet

- CHP 5Document5 pagesCHP 5Adeeb Hassannoor0% (1)

- Razelle Ann B. Dapilaga 11 Abm, Peter DruckerDocument3 pagesRazelle Ann B. Dapilaga 11 Abm, Peter DruckerJasmine ActaNo ratings yet

- Chapter 9 Ratio AnalysisDocument65 pagesChapter 9 Ratio AnalysisPoojaNo ratings yet

- Sun and Crocs ValuationDocument7 pagesSun and Crocs ValuationKshitishNo ratings yet

- AVT LawsuitDocument14 pagesAVT LawsuitYTOLeaderNo ratings yet

- Customs Valuation of Imported GoodsDocument2 pagesCustoms Valuation of Imported GoodsjustenjoythelifeNo ratings yet

- Scf-Capital Structure Questions (Tybfm)Document2 pagesScf-Capital Structure Questions (Tybfm)TFM069 -SHIVAM VARMANo ratings yet

- Taxation Mid TermsDocument8 pagesTaxation Mid TermsEppie SeverinoNo ratings yet

- Financial Planning - ForecastingDocument4 pagesFinancial Planning - ForecastingPrathamesh411No ratings yet

- Marketing Management ProjectDocument5 pagesMarketing Management ProjectDebasish SahaNo ratings yet

- Ratio Analysis Comparison Between Beximco & Square by Simon (BUBT)Document16 pagesRatio Analysis Comparison Between Beximco & Square by Simon (BUBT)Simon Haque100% (1)

- Mutual Fund Research PaperDocument22 pagesMutual Fund Research Paperphani100% (1)

- Game Theory MoralityDocument17 pagesGame Theory MoralityHenryNo ratings yet

- RR 2-98Document85 pagesRR 2-98restless11No ratings yet

- Kalyani Investment Co Ltd. AR 2013 14 DDocument28 pagesKalyani Investment Co Ltd. AR 2013 14 DmarinedgeNo ratings yet