Download as pdf or txt

You might also like

- Business Dealings in Emerging Economies, Non-Contractual Relations, and Recourse To Law - An AnalysisDocument12 pagesBusiness Dealings in Emerging Economies, Non-Contractual Relations, and Recourse To Law - An AnalysisAnish GuptaNo ratings yet

- Bajaj Finance - SELL (Taking A Breather) 20211210 1Document81 pagesBajaj Finance - SELL (Taking A Breather) 20211210 1mpjegan90No ratings yet

- Karnataka Bank - Initiating Coverage - 161020Document14 pagesKarnataka Bank - Initiating Coverage - 161020Nihit SandNo ratings yet

- Muthoot Finance - Initiating Coverage - 120221Document13 pagesMuthoot Finance - Initiating Coverage - 120221DeepikaNo ratings yet

- HDFC Securities Sees 24% UPSIDE in IDFC LTDDocument14 pagesHDFC Securities Sees 24% UPSIDE in IDFC LTDTarunNo ratings yet

- Axis Bank - LKP - 29.10.2020 PDFDocument12 pagesAxis Bank - LKP - 29.10.2020 PDFVimal SharmaNo ratings yet

- Indusind Q2FY23 RU LKPDocument12 pagesIndusind Q2FY23 RU LKPPramukNo ratings yet

- Initiating Coverage - Trident LTD - 311020Document21 pagesInitiating Coverage - Trident LTD - 311020V KeshavdevNo ratings yet

- Shriram Transport Finance Company Ltd. - Initiating Coverage - 30032021Document12 pagesShriram Transport Finance Company Ltd. - Initiating Coverage - 30032021Devarsh VakilNo ratings yet

- ICICI Securities Zomato Reinitiating Coverage NoteDocument13 pagesICICI Securities Zomato Reinitiating Coverage NoteClaptrapjackNo ratings yet

- SBI LTD Initiating Coverage 19062020Document8 pagesSBI LTD Initiating Coverage 19062020Devendra rautNo ratings yet

- ICICI - Piramal EnterprisesDocument16 pagesICICI - Piramal EnterprisessehgalgauravNo ratings yet

- SBI - 3QFY19 - HDFC Sec-201902031901526172690Document14 pagesSBI - 3QFY19 - HDFC Sec-201902031901526172690HARDIK SHAHNo ratings yet

- Strategiuc MGMT Session 1 MaterialDocument14 pagesStrategiuc MGMT Session 1 MaterialAPOORVA BALAKRISHNANNo ratings yet

- LIC Housing Finance: Performance HighlightsDocument10 pagesLIC Housing Finance: Performance HighlightsAngel BrokingNo ratings yet

- LIC Housing Ltd. - InitiatingDocument7 pagesLIC Housing Ltd. - InitiatingAnantharaman RamasamyNo ratings yet

- Axis Bank LTDDocument12 pagesAxis Bank LTDMera Birthday 2021No ratings yet

- L&T Finance Holdings - GeojitDocument4 pagesL&T Finance Holdings - GeojitdarshanmadeNo ratings yet

- Initiating Coverage - Orient Cement 171220 PDFDocument16 pagesInitiating Coverage - Orient Cement 171220 PDFJayshree JadhavNo ratings yet

- (Kotak) ICICI Bank, January 31, 2013Document14 pages(Kotak) ICICI Bank, January 31, 2013Chaitanya JagarlapudiNo ratings yet

- AxisCap - PEL - FN - 29 Feb 2024Document6 pagesAxisCap - PEL - FN - 29 Feb 2024Mohammed Israr ShaikhNo ratings yet

- Indostar 20200813 Mosl Ru PG010Document10 pagesIndostar 20200813 Mosl Ru PG010Forall PainNo ratings yet

- REC Ltd. - Re Initiating Coverage - 13082021Document15 pagesREC Ltd. - Re Initiating Coverage - 13082021Rahul RathodNo ratings yet

- HDFC Bank Result UpdatedDocument13 pagesHDFC Bank Result UpdatedAngel BrokingNo ratings yet

- 0 - 3qfy20 - HDFC SecDocument11 pages0 - 3qfy20 - HDFC SecGirish Raj SankunnyNo ratings yet

- Icici Bank: Performance HighlightsDocument15 pagesIcici Bank: Performance HighlightsAngel BrokingNo ratings yet

- ICICI Securities Suryoday Q2FY23 ResultsDocument10 pagesICICI Securities Suryoday Q2FY23 ResultsDivy JainNo ratings yet

- Britannia Industries - Initiating Coverage 281020Document12 pagesBritannia Industries - Initiating Coverage 281020Aniket DhanukaNo ratings yet

- Q1FY22 Result Update City Union Bank LTD: Beat On Operational Front Due To Lower Credit CostDocument12 pagesQ1FY22 Result Update City Union Bank LTD: Beat On Operational Front Due To Lower Credit Costforgi mistyNo ratings yet

- State Bank of India 4 QuarterUpdateDocument6 pagesState Bank of India 4 QuarterUpdatedarshan pNo ratings yet

- Care Ratings - Q4FY19 - Call Closure - 13062019 - 14-06-2019 - 09Document4 pagesCare Ratings - Q4FY19 - Call Closure - 13062019 - 14-06-2019 - 09Jai SinghNo ratings yet

- Bajaj Finance Sell: Result UpdateDocument5 pagesBajaj Finance Sell: Result UpdateJeedula ManasaNo ratings yet

- Dewan Housing Finance Corporation.: Business Background Key DataDocument4 pagesDewan Housing Finance Corporation.: Business Background Key DataKOUSHIKNo ratings yet

- CMP: INR141 TP: INR175 (+24%) Biggest Beneficiary of Improved PricingDocument10 pagesCMP: INR141 TP: INR175 (+24%) Biggest Beneficiary of Improved PricingPratik PatilNo ratings yet

- Press Release Bank of Baroda Announces Financial Results For Q3Fy22Document4 pagesPress Release Bank of Baroda Announces Financial Results For Q3Fy22Abhay SinghNo ratings yet

- Allahabad Bank Result UpdatedDocument11 pagesAllahabad Bank Result UpdatedAngel BrokingNo ratings yet

- Federal Bank: Performance HighlightsDocument11 pagesFederal Bank: Performance HighlightsAngel BrokingNo ratings yet

- State Bank of India LTD.: Result UpdateDocument7 pagesState Bank of India LTD.: Result UpdatedeveshNo ratings yet

- Canara Bank 110522 LKPDocument7 pagesCanara Bank 110522 LKPjazz mohamedNo ratings yet

- HDFC Bank 20072020 IciciDocument15 pagesHDFC Bank 20072020 IciciVipul Braj BhartiaNo ratings yet

- South Indian BankDocument11 pagesSouth Indian BankAngel BrokingNo ratings yet

- Security Valuation Additional Q M19 To J21Document33 pagesSecurity Valuation Additional Q M19 To J21Prazita ShresthaNo ratings yet

- Nykaa - Company Update - Jan23Document8 pagesNykaa - Company Update - Jan23Abhishek MurarkaNo ratings yet

- Investment Idea HDFCLTD Hold 101021001914 Phpapp01Document2 pagesInvestment Idea HDFCLTD Hold 101021001914 Phpapp01yogi3250No ratings yet

- Can Fin Homes Ltd-4QFY23 Result UpdateDocument5 pagesCan Fin Homes Ltd-4QFY23 Result UpdateUjwal KumarNo ratings yet

- ICICI Bank, 4th February, 2013Document16 pagesICICI Bank, 4th February, 2013Angel BrokingNo ratings yet

- LIC Housing FinanceDocument8 pagesLIC Housing FinanceAngel BrokingNo ratings yet

- Initiating Coverage - Sandhar Technologies - 26072021Document18 pagesInitiating Coverage - Sandhar Technologies - 26072021Chandrakumar KumarNo ratings yet

- Shriram City Union Finance 27042018 1Document14 pagesShriram City Union Finance 27042018 1saran21No ratings yet

- Buy Aditya Birla Capital EDEL 9.11.2019 PDFDocument24 pagesBuy Aditya Birla Capital EDEL 9.11.2019 PDFKunalNo ratings yet

- Indian Hotel - Q4FY22 Results - DAMDocument8 pagesIndian Hotel - Q4FY22 Results - DAMRajiv BharatiNo ratings yet

- Reliance Retail - Update - Apr20 - HDFC Sec-202004142249010251722Document27 pagesReliance Retail - Update - Apr20 - HDFC Sec-202004142249010251722hemant pawdeNo ratings yet

- HDFC 2qfy2013ruDocument9 pagesHDFC 2qfy2013ruAngel BrokingNo ratings yet

- LIC Housing Finance Result UpdatedDocument8 pagesLIC Housing Finance Result UpdatedAngel BrokingNo ratings yet

- HDFCDocument2 pagesHDFCshankyagarNo ratings yet

- South Indian Bank, 1Q FY 2014Document12 pagesSouth Indian Bank, 1Q FY 2014Angel BrokingNo ratings yet

- Axis Bank: Performance HighlightsDocument13 pagesAxis Bank: Performance HighlightsAngel BrokingNo ratings yet

- SouthIndianBank 2QFY2013RU NWDocument13 pagesSouthIndianBank 2QFY2013RU NWAngel BrokingNo ratings yet

- CDSL-Stock RessearchDocument13 pagesCDSL-Stock RessearchSarah AliceNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2021 Volume IV: Pilot SME Development Index: Applying Probabilistic Principal Component AnalysisFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2021 Volume IV: Pilot SME Development Index: Applying Probabilistic Principal Component AnalysisNo ratings yet

- Economic Insights from Input–Output Tables for Asia and the PacificFrom EverandEconomic Insights from Input–Output Tables for Asia and the PacificNo ratings yet

- Land Records ModernisationDocument4 pagesLand Records ModernisationRohit GuptaNo ratings yet

- MGI - Thriving Amid Turbulence Imagining The Cities of The FutureDocument16 pagesMGI - Thriving Amid Turbulence Imagining The Cities of The FutureRohit GuptaNo ratings yet

- A Comparative Analysis of The Land Acquisition Laws in India - 1894, 2013 and 2015Document5 pagesA Comparative Analysis of The Land Acquisition Laws in India - 1894, 2013 and 2015Rohit GuptaNo ratings yet

- Reader - CRE Prespective-DeloitteDocument50 pagesReader - CRE Prespective-DeloitteRohit GuptaNo ratings yet

- Viksit BharatDocument8 pagesViksit BharatRohit GuptaNo ratings yet

- Strategic Management - Internal Envt AssessmentDocument35 pagesStrategic Management - Internal Envt AssessmentRohit GuptaNo ratings yet

- PS 9Document4 pagesPS 9Rohit GuptaNo ratings yet

- Roles in A GDDocument6 pagesRoles in A GDRohit GuptaNo ratings yet

- FM - Introduction Scope Lecture 2Document25 pagesFM - Introduction Scope Lecture 2Rohit GuptaNo ratings yet

- Gurgaon City Evolution LMSDocument60 pagesGurgaon City Evolution LMSRohit GuptaNo ratings yet

- PS 5Document3 pagesPS 5Rohit GuptaNo ratings yet

- Mumbai Metropolitan Region (MMR) : The Crown Jewel of IndiaDocument22 pagesMumbai Metropolitan Region (MMR) : The Crown Jewel of IndiaRohit GuptaNo ratings yet

- PS 3Document4 pagesPS 3Rohit GuptaNo ratings yet

- PS 7Document4 pagesPS 7Rohit GuptaNo ratings yet

- PS 6Document3 pagesPS 6Rohit GuptaNo ratings yet

- PS 8Document4 pagesPS 8Rohit GuptaNo ratings yet

- PS 4Document4 pagesPS 4Rohit GuptaNo ratings yet

- 1391506514076brouchers UtopiaDocument1 page1391506514076brouchers UtopiaRohit GuptaNo ratings yet

- PS 2Document4 pagesPS 2Rohit GuptaNo ratings yet

- Golf Course Road - Micro Market Overview Report-READERDocument6 pagesGolf Course Road - Micro Market Overview Report-READERRohit GuptaNo ratings yet

- Final Capstone - Ruchi SawwalakheDocument48 pagesFinal Capstone - Ruchi SawwalakheRohit GuptaNo ratings yet

- WEO DataDocument14 pagesWEO DataPrypiat 0No ratings yet

- Aia Smart Growth BrochureDocument8 pagesAia Smart Growth BrochurebutterNo ratings yet

- Acceptance Letter JKRDocument5 pagesAcceptance Letter JKRNUR HAMIZAH BINTI ISHAK STUDENTNo ratings yet

- A Study On Factors Influencing Consumer's Attitude Towards Mobile Payment Application in BelgaumDocument37 pagesA Study On Factors Influencing Consumer's Attitude Towards Mobile Payment Application in BelgaumPETER MENDONSANo ratings yet

- Accounting For SupermartDocument2 pagesAccounting For SupermartSubscribe PranksNo ratings yet

- (Done) Q2 - GenMath WEEK 11 (M1)Document3 pages(Done) Q2 - GenMath WEEK 11 (M1)aespa karinaNo ratings yet

- Commercial Banking in PakistanDocument24 pagesCommercial Banking in PakistanMuhammad RadeelNo ratings yet

- PHS For Philippine Coast Guard AuxillaryDocument7 pagesPHS For Philippine Coast Guard AuxillaryRj Hush EsguerraNo ratings yet

- SKYZ by Danube - High ResolutionDocument44 pagesSKYZ by Danube - High ResolutionHamza AhmedNo ratings yet

- Fundraiser For Aruna Kumar by Murugesan Guruswamy Viswanathan Family Support FundDocument1 pageFundraiser For Aruna Kumar by Murugesan Guruswamy Viswanathan Family Support FundMadhu YemaniNo ratings yet

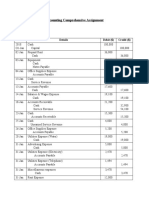

- Accounting Comprehensive AssignmentDocument11 pagesAccounting Comprehensive AssignmentSadia ShithyNo ratings yet

- YL9000P Stellar Labs (MCM Electronics) Product Details: Part Number: Worldway Part: Category: Manufacturer: ApplicationsDocument3 pagesYL9000P Stellar Labs (MCM Electronics) Product Details: Part Number: Worldway Part: Category: Manufacturer: ApplicationsAbdallh MahmoudNo ratings yet

- CIX 2005 Entrepreneurship Essay Covid-19Document8 pagesCIX 2005 Entrepreneurship Essay Covid-19Tan WzzzNo ratings yet

- Data 69Document4 pagesData 69Abhijit BarmanNo ratings yet

- Concepts in Federal Taxation 2013 20th Edition Murphy Test Bank DownloadDocument141 pagesConcepts in Federal Taxation 2013 20th Edition Murphy Test Bank DownloadDavid Clark100% (23)

- ABIR Global Underwriting Report - 2021Document2 pagesABIR Global Underwriting Report - 2021BernewsAdminNo ratings yet

- Mock Scenario - Manufacturing - ERP - UATDocument1 pageMock Scenario - Manufacturing - ERP - UATHtun LinNo ratings yet

- BS 4662Document41 pagesBS 4662hessian123100% (1)

- ASEAN Officially The Association of Southeast Asian Nations Is A Political and Economic Union ofDocument5 pagesASEAN Officially The Association of Southeast Asian Nations Is A Political and Economic Union ofjustineNo ratings yet

- Offsite Construction - Question 1Document6 pagesOffsite Construction - Question 1BarrouzNo ratings yet

- WT Ramsay LTD V Inland Revenue Commissioners (1981) UKHL 1 (12 March 1981)Document19 pagesWT Ramsay LTD V Inland Revenue Commissioners (1981) UKHL 1 (12 March 1981)bharath289No ratings yet

- Chapter 7Document19 pagesChapter 7dylanNo ratings yet

- Contract12 1Document3 pagesContract12 1ghostwriter83No ratings yet

- WEEK 2 3 ExercisesDocument13 pagesWEEK 2 3 ExercisesÁi Ly NguyễnNo ratings yet

- The Unintended Environmental Effect of A Climate Change Adaptation Strategy - Evidence From The Colombian Coffee SectorDocument46 pagesThe Unintended Environmental Effect of A Climate Change Adaptation Strategy - Evidence From The Colombian Coffee SectorrafardzvNo ratings yet

- The State of CPP Purchase Power - Presentation To Utilities Comm 9-29-2020Document35 pagesThe State of CPP Purchase Power - Presentation To Utilities Comm 9-29-2020Sheehan HannanNo ratings yet

- Demonstrativo de Posição: Dayane David Duraes CPF / CNPJ: 582554608Document4 pagesDemonstrativo de Posição: Dayane David Duraes CPF / CNPJ: 582554608Fábio AndreuccettiNo ratings yet

- 4 P's of Bisleri: By-Divay Agarwal PGDM-09-049Document18 pages4 P's of Bisleri: By-Divay Agarwal PGDM-09-049divya_agarwal_8No ratings yet

- China's New Development Strategies Upgrading From Above and From Below in Global Value Chains (Gary Gereffi, Penny Bamber Etc.) (Z-Library)Document303 pagesChina's New Development Strategies Upgrading From Above and From Below in Global Value Chains (Gary Gereffi, Penny Bamber Etc.) (Z-Library)chandrasgudivNo ratings yet