Download as pdf or txt

You might also like

- Tutorial 6Document26 pagesTutorial 6Mya Hmuu KhinNo ratings yet

- 112-Article Text-273-1-10-20211223Document6 pages112-Article Text-273-1-10-20211223junaidiNo ratings yet

- A Study On Financial Performance Analysis of Selected Public and Private Sector BanksDocument7 pagesA Study On Financial Performance Analysis of Selected Public and Private Sector Banksshaik.712239No ratings yet

- The Effect of Bank Soundness Ratio Towards Financial Performance On Commercial Banks Moderated by Good Corporate GovernanceDocument7 pagesThe Effect of Bank Soundness Ratio Towards Financial Performance On Commercial Banks Moderated by Good Corporate GovernanceInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Mburu MwangiandMuathe2020Document14 pagesMburu MwangiandMuathe2020Jr SantiagoNo ratings yet

- Akoi, Andrea 2020Document12 pagesAkoi, Andrea 2020welwencoolNo ratings yet

- Market Risk Management and Financial Performance of Commercial Banks in Mbarara City Evidence of Centenary Bank Mbarara BranchDocument6 pagesMarket Risk Management and Financial Performance of Commercial Banks in Mbarara City Evidence of Centenary Bank Mbarara Branchajmrr editorNo ratings yet

- A Research Report On Cost Efficiency and Credit Management Variables of Banking Industry: A Study On Sunrise Bank and Siddhartha BankDocument16 pagesA Research Report On Cost Efficiency and Credit Management Variables of Banking Industry: A Study On Sunrise Bank and Siddhartha BankBinod thakurNo ratings yet

- Madda Walabu University College of Business and Economics Department of Accounting and FinanceDocument5 pagesMadda Walabu University College of Business and Economics Department of Accounting and FinancehabtamuNo ratings yet

- Artikel Publikasi - Dhiya, Alex, GraceDocument15 pagesArtikel Publikasi - Dhiya, Alex, Graceh2qkh9pvsbNo ratings yet

- Impact of Credit Risk On Profitability ADocument7 pagesImpact of Credit Risk On Profitability ANikeladam JNo ratings yet

- Influence of Financial Depth On Financial Performance of Commercial Banks in RwandaDocument12 pagesInfluence of Financial Depth On Financial Performance of Commercial Banks in RwandaJohn PaulNo ratings yet

- Impact of Npa (Non-Performing Assets) On The Profitability Performance of The Selected Public and Private Sector BankDocument7 pagesImpact of Npa (Non-Performing Assets) On The Profitability Performance of The Selected Public and Private Sector BankIJAR JOURNALNo ratings yet

- 15 - Chapter 6 PDFDocument30 pages15 - Chapter 6 PDFRukminiNo ratings yet

- Ijrbm - Effect of Macro-Economic and Banks Specific Determinants of Credit Risk of Select Public Sector Banks in The Post Financial Crisis Period Evidence From IndiaDocument11 pagesIjrbm - Effect of Macro-Economic and Banks Specific Determinants of Credit Risk of Select Public Sector Banks in The Post Financial Crisis Period Evidence From IndiaImpact JournalsNo ratings yet

- Relationship Between Credit Risk Management and Financial Performance: Empirical Evidence From Microfinance Banks in KenyaDocument28 pagesRelationship Between Credit Risk Management and Financial Performance: Empirical Evidence From Microfinance Banks in KenyaCatherine AteNo ratings yet

- Developing A Predictive Model About Bankruptcy in The Rural Areas of IndonesiaDocument7 pagesDeveloping A Predictive Model About Bankruptcy in The Rural Areas of IndonesiaOka WidanaNo ratings yet

- Mahmud Rani FriendDocument25 pagesMahmud Rani FriendMOHAMMED ABDULMALIKNo ratings yet

- A Proposal on Mortage Financing of AdblDocument7 pagesA Proposal on Mortage Financing of Adblkamal KharelNo ratings yet

- Research Paper On BankingDocument7 pagesResearch Paper On BankingHunny Pal100% (1)

- Research Papers On Risk Management in Indian BanksDocument5 pagesResearch Papers On Risk Management in Indian BanksafnkjuvgzjzrglNo ratings yet

- 347-Article Text-704-1-10-20230619Document13 pages347-Article Text-704-1-10-20230619WISNU SUKMANEGARANo ratings yet

- LDR To ROADocument10 pagesLDR To ROAJennifer WijayaNo ratings yet

- Reinforcing Indonesian Banks' Earnings Stability: A Gcg-Moderated Analysis of Risk Profile, Bank Digitalization, and Fintech P2P LendingDocument14 pagesReinforcing Indonesian Banks' Earnings Stability: A Gcg-Moderated Analysis of Risk Profile, Bank Digitalization, and Fintech P2P Lendingindex PubNo ratings yet

- Credit Risk, Liquidity Risk and Profitability in Nepalese Commercial BanksDocument9 pagesCredit Risk, Liquidity Risk and Profitability in Nepalese Commercial BanksKarim FarjallahNo ratings yet

- Published ManuscriptDocument13 pagesPublished ManuscriptmdhsohailNo ratings yet

- The Effect of Bank Efficiency, Industry Specification, and Macroeconomic On Banking Profitability in IndonesiaDocument9 pagesThe Effect of Bank Efficiency, Industry Specification, and Macroeconomic On Banking Profitability in Indonesiakinhdoanh282No ratings yet

- Bank Maturity, Income Diversification, and Bank StabilityDocument20 pagesBank Maturity, Income Diversification, and Bank Stabilitymah-e-alam rashidNo ratings yet

- Term Paper On Banking IndustryDocument4 pagesTerm Paper On Banking Industryc5rc7ppr100% (1)

- Management of Non-Performing Assets in Public Banks:: Evidence From IndiaDocument14 pagesManagement of Non-Performing Assets in Public Banks:: Evidence From Indiasidhusherry35No ratings yet

- 1 PBDocument8 pages1 PBGizachewNo ratings yet

- Impact of Asset Liability ManagementDocument8 pagesImpact of Asset Liability ManagementsajeerfimNo ratings yet

- A Study of Credit Risk ManagementDocument60 pagesA Study of Credit Risk ManagementPrince Satish Reddy100% (2)

- A Case Study On Conceptual Framework of Lending Technologies For Financing of Small and Medium Enterprises by Indian Overseas Bank PDFDocument19 pagesA Case Study On Conceptual Framework of Lending Technologies For Financing of Small and Medium Enterprises by Indian Overseas Bank PDFkannan sunilNo ratings yet

- CREDIT RISK AND COMMERCIAL BANKS' PERFORMANCE IN NIGERIA: A PANEL Model APPROACHDocument8 pagesCREDIT RISK AND COMMERCIAL BANKS' PERFORMANCE IN NIGERIA: A PANEL Model APPROACHdarkniightNo ratings yet

- Methodology To Predict NPA in Indian Banking System: Gourav Vallabh, Digvijay Singh, Ruchir Prasoon, Abhimanyu SinghDocument10 pagesMethodology To Predict NPA in Indian Banking System: Gourav Vallabh, Digvijay Singh, Ruchir Prasoon, Abhimanyu SinghBiswajit DasNo ratings yet

- Research Paper Banking SectorDocument5 pagesResearch Paper Banking Sectormwjhkmrif100% (1)

- Impact of Financial Risk Management Practices On Financial Performance: Evidence From Commercial Banks in BotswanaDocument15 pagesImpact of Financial Risk Management Practices On Financial Performance: Evidence From Commercial Banks in Botswanavandv printsNo ratings yet

- Research Paper On Indian BanksDocument8 pagesResearch Paper On Indian Banksc9sj0n70100% (1)

- Research in International Business and Finance: Irwan Trinugroho, Wimboh Santoso, Rakianto Irawanto, Putra PamungkasDocument19 pagesResearch in International Business and Finance: Irwan Trinugroho, Wimboh Santoso, Rakianto Irawanto, Putra PamungkasZella Qaulan QarimahNo ratings yet

- Literature Review Banking SectorDocument7 pagesLiterature Review Banking Sectoreubvhsvkg100% (1)

- Bank Capital, Deposits and Size Effects Onprofitability of Commercial Banks in NepalDocument74 pagesBank Capital, Deposits and Size Effects Onprofitability of Commercial Banks in NepalRajendra LamsalNo ratings yet

- Credit Risk AnalysisDocument10 pagesCredit Risk AnalysisThiruvenkadam SrinivasanNo ratings yet

- Banking Health Assessment Using CAMELS and RGEC Methods (Jurnal Internasional)Document11 pagesBanking Health Assessment Using CAMELS and RGEC Methods (Jurnal Internasional)Ryan AlvarezyNo ratings yet

- Review of Literature On Credit Risk ManagementDocument12 pagesReview of Literature On Credit Risk ManagementMaryletIlagan67% (3)

- Van Dan LangDocument12 pagesVan Dan Langप्रज्वल थापाNo ratings yet

- Literature Review: 2.1 Industry OverviewDocument14 pagesLiterature Review: 2.1 Industry OverviewRashmi LekamgeNo ratings yet

- Updated Complete ProjectDocument67 pagesUpdated Complete Projectvictor wizvikNo ratings yet

- Nexus Between Marketing of Financial Services and Banks' Profitability in Nigeria: Study of United Bank For Africa PLC (Uba)Document13 pagesNexus Between Marketing of Financial Services and Banks' Profitability in Nigeria: Study of United Bank For Africa PLC (Uba)Ellastrous Gogo NathanNo ratings yet

- SSRN Id3525666Document17 pagesSSRN Id3525666v1v1subrotoNo ratings yet

- Performance and Financial Ratios of Commercial Banks in Malaysia and ChinaDocument12 pagesPerformance and Financial Ratios of Commercial Banks in Malaysia and Chinatedy hermawanNo ratings yet

- Is There Financial Accelerator in Indonesian Banking?: Dadang Lesmana, Felisitas Defung, Wirasmi WardhaniDocument9 pagesIs There Financial Accelerator in Indonesian Banking?: Dadang Lesmana, Felisitas Defung, Wirasmi WardhaniJeremy GunturNo ratings yet

- Final ThesisDocument61 pagesFinal ThesisKeshav KafleNo ratings yet

- Risk Management in Indian Banks Research PapersDocument4 pagesRisk Management in Indian Banks Research PapersafeaudffuNo ratings yet

- 1960 7446 1 PBDocument18 pages1960 7446 1 PBkinhdoanh282No ratings yet

- Proposal On SOCBsDocument15 pagesProposal On SOCBsRipa AkterNo ratings yet

- Impact of Liquidity On Profitability of Joint Venture Commercial Banks in Nepal (With Reference To EBL, HBL and NBB)Document16 pagesImpact of Liquidity On Profitability of Joint Venture Commercial Banks in Nepal (With Reference To EBL, HBL and NBB)Welcome BgNo ratings yet

- Sugianto Et Al. (2020)Document11 pagesSugianto Et Al. (2020)heprieka wulandariNo ratings yet

- Research Paper On Indian Banking IndustryDocument4 pagesResearch Paper On Indian Banking Industrygazqaacnd100% (1)

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- EIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptFrom EverandEIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptNo ratings yet

- ACC221 Exam-ReviewerDocument6 pagesACC221 Exam-ReviewerRianell Andrea AsumbradoNo ratings yet

- AE 24 Module 1 BudgetingDocument14 pagesAE 24 Module 1 BudgetingShamae Duma-anNo ratings yet

- Financial Accounting Problem SetDocument3 pagesFinancial Accounting Problem SetLohraine DyNo ratings yet

- Fabm 4 PDFDocument2 pagesFabm 4 PDFgk concepcionNo ratings yet

- CH06Document80 pagesCH06shelategosongNo ratings yet

- Investor Presentation - 2303 - ENG PDFDocument25 pagesInvestor Presentation - 2303 - ENG PDFJoseph ChoiNo ratings yet

- Solution Manual Advanced Accounting by Guerrero Peralta Chapter 2 PDFDocument24 pagesSolution Manual Advanced Accounting by Guerrero Peralta Chapter 2 PDFAndry John PerialdeNo ratings yet

- One Page Summary Millionaire FastLaneDocument9 pagesOne Page Summary Millionaire FastLaneHisfan NaziefNo ratings yet

- Microeconomics Group Assignment (Report Writing)Document9 pagesMicroeconomics Group Assignment (Report Writing)Abdirizak AhmedNo ratings yet

- 7169 - Noncurrent Asset Held For Sale and Discountinued OperationDocument2 pages7169 - Noncurrent Asset Held For Sale and Discountinued Operationjsmozol3434qcNo ratings yet

- Kunci Jawaban Uts - Pengantar Akuntansi - s1 AkuntansiDocument18 pagesKunci Jawaban Uts - Pengantar Akuntansi - s1 AkuntansiAll AboutNo ratings yet

- AEON - AR2021 (Part 4)Document66 pagesAEON - AR2021 (Part 4)SITI NAJIBAH BINTI MOHD NORNo ratings yet

- Solution Chapter 12 Advanced Accounting II 2014 by Dayag PDFDocument20 pagesSolution Chapter 12 Advanced Accounting II 2014 by Dayag PDFAurcus JumskieNo ratings yet

- Formulas and Sample CalculationsDocument8 pagesFormulas and Sample CalculationsBrave KingNo ratings yet

- Provisional: Provisional Income Tax CalculationDocument1 pageProvisional: Provisional Income Tax CalculationM. A Hossain & Associates Tax ConsultantsNo ratings yet

- Revolving Loan Application FormDocument1 pageRevolving Loan Application FormJames LangNo ratings yet

- Vita Construction LTD Payslip: Description Days/Hrs Rate Amount Description Days/Hrs Rate AmountDocument15 pagesVita Construction LTD Payslip: Description Days/Hrs Rate Amount Description Days/Hrs Rate AmountAmanzeNo ratings yet

- Industrial Arts - 6 - PowerpointDocument21 pagesIndustrial Arts - 6 - PowerpointGerard Adrian C. CastilloNo ratings yet

- National IncomeDocument4 pagesNational IncomeLawrenceNo ratings yet

- Lecture Cases On Consolidation With Intercompany Sale of InventoryDocument2 pagesLecture Cases On Consolidation With Intercompany Sale of InventoryRedNo ratings yet

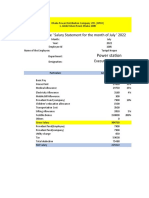

- Tariqul Hoque ' Salary Statement For The Month of July ' 2022Document6 pagesTariqul Hoque ' Salary Statement For The Month of July ' 2022Sadman Rafid FardeenNo ratings yet

- Abft1024 L7 - LtyDocument9 pagesAbft1024 L7 - Ltylfc778No ratings yet

- COMEX1 TAX REVIEW Canvas-1Document18 pagesCOMEX1 TAX REVIEW Canvas-1Angel RosalesNo ratings yet

- PFRS 10 Consolidated Financial Statement - : (Elimination Entries)Document11 pagesPFRS 10 Consolidated Financial Statement - : (Elimination Entries)Banana QNo ratings yet

- Chapter 24 Homework SolutionsDocument18 pagesChapter 24 Homework Solutionslenovot61No ratings yet

- Cash So Swiftly. Company Presentation - pptx-5Document23 pagesCash So Swiftly. Company Presentation - pptx-5brane.milcheskiNo ratings yet

- Act 122 Final Exam 2021 NoneDocument13 pagesAct 122 Final Exam 2021 Nonemax pNo ratings yet

- Ipsas 18 Segment Reporting 1Document31 pagesIpsas 18 Segment Reporting 1Rutuja KaleNo ratings yet

- Week3 The Marketing EnvironmentDocument29 pagesWeek3 The Marketing EnvironmentCHZE CHZI CHUAHNo ratings yet