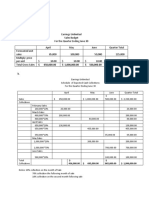

Nhóm ABC Bakery 2 - CA 3

Nhóm ABC Bakery 2 - CA 3

You might also like

- Retail Standard Operating ProceduresDocument55 pagesRetail Standard Operating ProceduresGurmeet Kaur Simmy83% (12)

- Ceres Gardening Company - Spreadsheet For StudentsDocument1 pageCeres Gardening Company - Spreadsheet For Studentsandres felipe restrepo arango0% (1)

- Budget Exercises - Part II (Model Answers)Document7 pagesBudget Exercises - Part II (Model Answers)Menna AssemNo ratings yet

- Strat Cost 8-24Document4 pagesStrat Cost 8-24Vivienne Rozenn LaytoNo ratings yet

- BudgetingDocument5 pagesBudgetingKevin James Sedurifa Oledan100% (1)

- Quiz 3.1 BudgetingDocument6 pagesQuiz 3.1 BudgetingMaxine ConstantinoNo ratings yet

- Cash Budget - Payal Plastics CompanyDocument4 pagesCash Budget - Payal Plastics Companysukesh86% (7)

- Master Budgeting (Sample Problems With Answers)Document11 pagesMaster Budgeting (Sample Problems With Answers)Jonalyn TaboNo ratings yet

- Cost Accounting 1Document2 pagesCost Accounting 1Anntoinette BendalNo ratings yet

- Solution For C. Alvarez ManufacturingDocument12 pagesSolution For C. Alvarez Manufacturingrei gbivNo ratings yet

- Proj 2Document15 pagesProj 2Shahan AsifNo ratings yet

- Chapter Two: Master Budget and Responsibility AccountingDocument25 pagesChapter Two: Master Budget and Responsibility Accountingweyn deguNo ratings yet

- Master Budget IllustrationDocument15 pagesMaster Budget IllustrationMaeNo ratings yet

- Group Managerial AccountingDocument9 pagesGroup Managerial AccountingSlamet SalimNo ratings yet

- Chapter Two Master Budget and Responsibility Accounting What Is Budget?Document12 pagesChapter Two Master Budget and Responsibility Accounting What Is Budget?kirosNo ratings yet

- 17 - Ni Putu Cherline Berliana - Problem 11.1 & 11.8Document6 pages17 - Ni Putu Cherline Berliana - Problem 11.1 & 11.8putu cherline21No ratings yet

- Financial Accounting - Final Case StudyDocument13 pagesFinancial Accounting - Final Case StudyAhmad ZakariaNo ratings yet

- Corp-Bgt#IUP-X#Sept21#Aldira Jasmine R A#12010119190284Document4 pagesCorp-Bgt#IUP-X#Sept21#Aldira Jasmine R A#12010119190284aldira jasmineNo ratings yet

- Earrings UnlimitedDocument6 pagesEarrings Unlimitedabigail franciscoNo ratings yet

- April May June Quarter Product: 1 Budgeted Sales (Units) Selling Price Per Unit Total RevenueDocument18 pagesApril May June Quarter Product: 1 Budgeted Sales (Units) Selling Price Per Unit Total Revenueyonna anggrelinaNo ratings yet

- Earrings UnlimitedDocument7 pagesEarrings Unlimitedabigail franciscoNo ratings yet

- Solution For C. Alvarez ManufacturingDocument12 pagesSolution For C. Alvarez ManufacturingHarvey AguilarNo ratings yet

- 08 TP 1-ArgDocument3 pages08 TP 1-ArgAlthea ObinaNo ratings yet

- Master Budget TemplateDocument19 pagesMaster Budget TemplateSanie Hizkia Hendrik MendeNo ratings yet

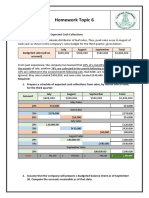

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- 08 TP - Evangelista Angela - 501PDocument9 pages08 TP - Evangelista Angela - 501PBetchang AquinoNo ratings yet

- Capital Budgeting Group 6Document31 pagesCapital Budgeting Group 6Uyên TrangNo ratings yet

- 1-3 Assignments in BudgettingDocument4 pages1-3 Assignments in BudgettingUlugbek SayfiddinovNo ratings yet

- Quiz 3.1 BudgetingDocument6 pagesQuiz 3.1 BudgetingMaxine ConstantinoNo ratings yet

- Budgeting - ExamplesDocument2 pagesBudgeting - Examplessunil.ctNo ratings yet

- Ex and P-BudgetingDocument10 pagesEx and P-BudgetingJessa Swing Dela CruzNo ratings yet

- BudgetDocument8 pagesBudgetvaibhavpratapsingh910No ratings yet

- Total Cash Inflow: PaymentsDocument12 pagesTotal Cash Inflow: PaymentsLikith RNo ratings yet

- Master BudgetingDocument20 pagesMaster Budgetingjoinme2dayNo ratings yet

- Schedule 1: Sales BudgetDocument9 pagesSchedule 1: Sales BudgetAndrea Lyn Salonga CacayNo ratings yet

- Earrings Suggested SolutionsDocument4 pagesEarrings Suggested Solutions9ry5gsghybNo ratings yet

- AE323 Prelim Long Quiz AY 23 24 Answer KeyDocument1 pageAE323 Prelim Long Quiz AY 23 24 Answer KeyElla janeNo ratings yet

- Melly Yanti - Case Study Master BudgetingDocument4 pagesMelly Yanti - Case Study Master BudgetingNatasha HerlianaNo ratings yet

- LB53 Case MA Graviela Charleen 2502001574Document4 pagesLB53 Case MA Graviela Charleen 2502001574Natasha HerlianaNo ratings yet

- Final Exam - Sent StudentsDocument6 pagesFinal Exam - Sent StudentsYến Hoàng HảiNo ratings yet

- Final Exam - Sent StudentsDocument5 pagesFinal Exam - Sent StudentsTrần Nguyễn Tuệ MinhNo ratings yet

- PA2 - Master Budget and Its ComponentsDocument10 pagesPA2 - Master Budget and Its ComponentsSunil N PunjabiNo ratings yet

- Master BudgetDocument36 pagesMaster BudgetRafols AnnabelleNo ratings yet

- Budgetary ControlDocument5 pagesBudgetary ControlJasdeep Singh DeepuNo ratings yet

- Corminal TPDocument7 pagesCorminal TPBetchang AquinoNo ratings yet

- Budget RIZZA PIZZA - Luan GonzagaDocument15 pagesBudget RIZZA PIZZA - Luan GonzagaLuan Allama GonzagaNo ratings yet

- Strat CostDocument2 pagesStrat CostTINDOY, Darlyn Joyce O.No ratings yet

- Treasury Management Vs Cash Management Answer To Warm Up ExercisesDocument8 pagesTreasury Management Vs Cash Management Answer To Warm Up Exercisesephraim0% (1)

- Case Analysis (1 30)Document3 pagesCase Analysis (1 30)manishadaaNo ratings yet

- Purposes of Budgeting Systems: BudgetDocument42 pagesPurposes of Budgeting Systems: BudgetJohn Joseph CambaNo ratings yet

- Budgeting - Planning: A325 Discussion - March 19, 2012Document8 pagesBudgeting - Planning: A325 Discussion - March 19, 2012alfaNo ratings yet

- Master BudgetDocument12 pagesMaster Budgetshi shiiisshhNo ratings yet

- (Jennifer / 1901469555 / LA53) : GSLC Assignment Profit PlanningDocument5 pages(Jennifer / 1901469555 / LA53) : GSLC Assignment Profit PlanningJennifer GunawanNo ratings yet

- Imanuel Xaverdino - 01804220010 - Homework 06Document3 pagesImanuel Xaverdino - 01804220010 - Homework 06Imanuel XaverdinoNo ratings yet

- CHƯƠNG 1 - 10đ - 4Document5 pagesCHƯƠNG 1 - 10đ - 4Trần Khánh VyNo ratings yet

- Healthy Bread DelightDocument11 pagesHealthy Bread DelightSetty HakeemaNo ratings yet

- Management Accounting Monday 3-6 Sir Fahim QaziDocument21 pagesManagement Accounting Monday 3-6 Sir Fahim QaziMuhammad Hamza AijaziNo ratings yet

- ADFM Cash BudgetDocument5 pagesADFM Cash BudgetNidheena K SNo ratings yet

- A. Sales Budget (4items)Document3 pagesA. Sales Budget (4items)Nin JahNo ratings yet

- Cash BudgetingDocument3 pagesCash Budgetingsunil.ctNo ratings yet

- Receipts: Closing Balance (A-B) 33,000 27,000 34,750Document6 pagesReceipts: Closing Balance (A-B) 33,000 27,000 34,750rajyalakshmiNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- O P Jindal Modern School, Hisar: Worksheet No. 3 Subject-Evs NAME: ................... ROLL NO. . Class 5Document2 pagesO P Jindal Modern School, Hisar: Worksheet No. 3 Subject-Evs NAME: ................... ROLL NO. . Class 5Raghav BansalNo ratings yet

- The Legend of Lake TobaDocument4 pagesThe Legend of Lake TobaLilis MahmudatunNo ratings yet

- PRED Dharwad Circle 2018-19 SRDocument111 pagesPRED Dharwad Circle 2018-19 SRRameshkumar Hugar54% (13)

- LIT 1 FOOTNOTE TO YOUTH With ASSIGNMENTDocument6 pagesLIT 1 FOOTNOTE TO YOUTH With ASSIGNMENTAiel Legaspi EstepaNo ratings yet

- Electro AdhesionDocument2 pagesElectro AdhesiongremlinglitchNo ratings yet

- Editing EssayDocument7 pagesEditing Essayapi-581857550No ratings yet

- Title ProposalDocument6 pagesTitle ProposalChanNo ratings yet

- Baby - Assessing The 21ST Century Skill of Learners in Multigrade ClassesDocument22 pagesBaby - Assessing The 21ST Century Skill of Learners in Multigrade ClassesHiezl Ness GonzagaNo ratings yet

- Phytoremediation 150123100305 Conversion Gate02Document49 pagesPhytoremediation 150123100305 Conversion Gate02Kumar MadhuNo ratings yet

- Table SettingDocument4 pagesTable SettingBianca FormantesNo ratings yet

- Trimestral LogicDocument4 pagesTrimestral LogicGabriel FigueroaNo ratings yet

- Sustainable DevelopmentDocument5 pagesSustainable DevelopmentMeera NairNo ratings yet

- Chapter 1 EdDocument6 pagesChapter 1 EdReffisa JiruNo ratings yet

- Weekly Home Learning Plan: Carmen National High School Carmen, San Agustin, RomblonDocument2 pagesWeekly Home Learning Plan: Carmen National High School Carmen, San Agustin, RomblonVina Verdadero TomeNo ratings yet

- Sun City Biker - November 2011Document24 pagesSun City Biker - November 2011Spotlight EP NewsNo ratings yet

- Comparative Report On Fast Food Study in Thailand, Indonesia and Vietnam in 2015Document48 pagesComparative Report On Fast Food Study in Thailand, Indonesia and Vietnam in 2015Daksh SetiaNo ratings yet

- MRCPCH DhanDocument26 pagesMRCPCH DhanRajiv KabadNo ratings yet

- Steps Involved in Business Process ReengineeringDocument2 pagesSteps Involved in Business Process ReengineeringHarrison NchoeNo ratings yet

- Experimental Study On Use of Hypo Sludge and Nylon Fibre in Paver BlockDocument6 pagesExperimental Study On Use of Hypo Sludge and Nylon Fibre in Paver BlockIJRASETPublicationsNo ratings yet

- Saleem Sinai The 1st Among 1001Document8 pagesSaleem Sinai The 1st Among 1001Sonom RahnumaNo ratings yet

- Future Simple Tense - InterrogativeDocument5 pagesFuture Simple Tense - InterrogativeanthonyleonNo ratings yet

- Hollywood Theatre Redevelopment Plan 9-12-08Document12 pagesHollywood Theatre Redevelopment Plan 9-12-08Matthew HendricksNo ratings yet

- Fundamentals of PM SZABISTDocument20 pagesFundamentals of PM SZABISTSalah Ud DinNo ratings yet

- Along Came Love by Cheryl ZeeDocument787 pagesAlong Came Love by Cheryl ZeeFungai Wise MukaratiNo ratings yet

- Lecture Notes On Software Configuration Management: Zia Syed Carnegie Mellon UniversityDocument58 pagesLecture Notes On Software Configuration Management: Zia Syed Carnegie Mellon Universityvarsha reddyNo ratings yet

- G.R. No. 122807 July 5, 1996 ROGELIO P. MENDIOLA, Petitioner, Court of Appeals and Philippine National Bank, RespondentsDocument5 pagesG.R. No. 122807 July 5, 1996 ROGELIO P. MENDIOLA, Petitioner, Court of Appeals and Philippine National Bank, RespondentsSamantha BaricauaNo ratings yet

- Sundays With YouDocument2 pagesSundays With YouLlana Claire CatudioNo ratings yet

- Immaculate Conception Academy: West CampusDocument25 pagesImmaculate Conception Academy: West CampusCrystal SnowNo ratings yet

Download as docx, pdf, or txt

You might also like

- Retail Standard Operating ProceduresDocument55 pagesRetail Standard Operating ProceduresGurmeet Kaur Simmy83% (12)

- Ceres Gardening Company - Spreadsheet For StudentsDocument1 pageCeres Gardening Company - Spreadsheet For Studentsandres felipe restrepo arango0% (1)

- Budget Exercises - Part II (Model Answers)Document7 pagesBudget Exercises - Part II (Model Answers)Menna AssemNo ratings yet

- Strat Cost 8-24Document4 pagesStrat Cost 8-24Vivienne Rozenn LaytoNo ratings yet

- BudgetingDocument5 pagesBudgetingKevin James Sedurifa Oledan100% (1)

- Quiz 3.1 BudgetingDocument6 pagesQuiz 3.1 BudgetingMaxine ConstantinoNo ratings yet

- Cash Budget - Payal Plastics CompanyDocument4 pagesCash Budget - Payal Plastics Companysukesh86% (7)

- Master Budgeting (Sample Problems With Answers)Document11 pagesMaster Budgeting (Sample Problems With Answers)Jonalyn TaboNo ratings yet

- Cost Accounting 1Document2 pagesCost Accounting 1Anntoinette BendalNo ratings yet

- Solution For C. Alvarez ManufacturingDocument12 pagesSolution For C. Alvarez Manufacturingrei gbivNo ratings yet

- Proj 2Document15 pagesProj 2Shahan AsifNo ratings yet

- Chapter Two: Master Budget and Responsibility AccountingDocument25 pagesChapter Two: Master Budget and Responsibility Accountingweyn deguNo ratings yet

- Master Budget IllustrationDocument15 pagesMaster Budget IllustrationMaeNo ratings yet

- Group Managerial AccountingDocument9 pagesGroup Managerial AccountingSlamet SalimNo ratings yet

- Chapter Two Master Budget and Responsibility Accounting What Is Budget?Document12 pagesChapter Two Master Budget and Responsibility Accounting What Is Budget?kirosNo ratings yet

- 17 - Ni Putu Cherline Berliana - Problem 11.1 & 11.8Document6 pages17 - Ni Putu Cherline Berliana - Problem 11.1 & 11.8putu cherline21No ratings yet

- Financial Accounting - Final Case StudyDocument13 pagesFinancial Accounting - Final Case StudyAhmad ZakariaNo ratings yet

- Corp-Bgt#IUP-X#Sept21#Aldira Jasmine R A#12010119190284Document4 pagesCorp-Bgt#IUP-X#Sept21#Aldira Jasmine R A#12010119190284aldira jasmineNo ratings yet

- Earrings UnlimitedDocument6 pagesEarrings Unlimitedabigail franciscoNo ratings yet

- April May June Quarter Product: 1 Budgeted Sales (Units) Selling Price Per Unit Total RevenueDocument18 pagesApril May June Quarter Product: 1 Budgeted Sales (Units) Selling Price Per Unit Total Revenueyonna anggrelinaNo ratings yet

- Earrings UnlimitedDocument7 pagesEarrings Unlimitedabigail franciscoNo ratings yet

- Solution For C. Alvarez ManufacturingDocument12 pagesSolution For C. Alvarez ManufacturingHarvey AguilarNo ratings yet

- 08 TP 1-ArgDocument3 pages08 TP 1-ArgAlthea ObinaNo ratings yet

- Master Budget TemplateDocument19 pagesMaster Budget TemplateSanie Hizkia Hendrik MendeNo ratings yet

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- 08 TP - Evangelista Angela - 501PDocument9 pages08 TP - Evangelista Angela - 501PBetchang AquinoNo ratings yet

- Capital Budgeting Group 6Document31 pagesCapital Budgeting Group 6Uyên TrangNo ratings yet

- 1-3 Assignments in BudgettingDocument4 pages1-3 Assignments in BudgettingUlugbek SayfiddinovNo ratings yet

- Quiz 3.1 BudgetingDocument6 pagesQuiz 3.1 BudgetingMaxine ConstantinoNo ratings yet

- Budgeting - ExamplesDocument2 pagesBudgeting - Examplessunil.ctNo ratings yet

- Ex and P-BudgetingDocument10 pagesEx and P-BudgetingJessa Swing Dela CruzNo ratings yet

- BudgetDocument8 pagesBudgetvaibhavpratapsingh910No ratings yet

- Total Cash Inflow: PaymentsDocument12 pagesTotal Cash Inflow: PaymentsLikith RNo ratings yet

- Master BudgetingDocument20 pagesMaster Budgetingjoinme2dayNo ratings yet

- Schedule 1: Sales BudgetDocument9 pagesSchedule 1: Sales BudgetAndrea Lyn Salonga CacayNo ratings yet

- Earrings Suggested SolutionsDocument4 pagesEarrings Suggested Solutions9ry5gsghybNo ratings yet

- AE323 Prelim Long Quiz AY 23 24 Answer KeyDocument1 pageAE323 Prelim Long Quiz AY 23 24 Answer KeyElla janeNo ratings yet

- Melly Yanti - Case Study Master BudgetingDocument4 pagesMelly Yanti - Case Study Master BudgetingNatasha HerlianaNo ratings yet

- LB53 Case MA Graviela Charleen 2502001574Document4 pagesLB53 Case MA Graviela Charleen 2502001574Natasha HerlianaNo ratings yet

- Final Exam - Sent StudentsDocument6 pagesFinal Exam - Sent StudentsYến Hoàng HảiNo ratings yet

- Final Exam - Sent StudentsDocument5 pagesFinal Exam - Sent StudentsTrần Nguyễn Tuệ MinhNo ratings yet

- PA2 - Master Budget and Its ComponentsDocument10 pagesPA2 - Master Budget and Its ComponentsSunil N PunjabiNo ratings yet

- Master BudgetDocument36 pagesMaster BudgetRafols AnnabelleNo ratings yet

- Budgetary ControlDocument5 pagesBudgetary ControlJasdeep Singh DeepuNo ratings yet

- Corminal TPDocument7 pagesCorminal TPBetchang AquinoNo ratings yet

- Budget RIZZA PIZZA - Luan GonzagaDocument15 pagesBudget RIZZA PIZZA - Luan GonzagaLuan Allama GonzagaNo ratings yet

- Strat CostDocument2 pagesStrat CostTINDOY, Darlyn Joyce O.No ratings yet

- Treasury Management Vs Cash Management Answer To Warm Up ExercisesDocument8 pagesTreasury Management Vs Cash Management Answer To Warm Up Exercisesephraim0% (1)

- Case Analysis (1 30)Document3 pagesCase Analysis (1 30)manishadaaNo ratings yet

- Purposes of Budgeting Systems: BudgetDocument42 pagesPurposes of Budgeting Systems: BudgetJohn Joseph CambaNo ratings yet

- Budgeting - Planning: A325 Discussion - March 19, 2012Document8 pagesBudgeting - Planning: A325 Discussion - March 19, 2012alfaNo ratings yet

- Master BudgetDocument12 pagesMaster Budgetshi shiiisshhNo ratings yet

- (Jennifer / 1901469555 / LA53) : GSLC Assignment Profit PlanningDocument5 pages(Jennifer / 1901469555 / LA53) : GSLC Assignment Profit PlanningJennifer GunawanNo ratings yet

- Imanuel Xaverdino - 01804220010 - Homework 06Document3 pagesImanuel Xaverdino - 01804220010 - Homework 06Imanuel XaverdinoNo ratings yet

- CHƯƠNG 1 - 10đ - 4Document5 pagesCHƯƠNG 1 - 10đ - 4Trần Khánh VyNo ratings yet

- Healthy Bread DelightDocument11 pagesHealthy Bread DelightSetty HakeemaNo ratings yet

- Management Accounting Monday 3-6 Sir Fahim QaziDocument21 pagesManagement Accounting Monday 3-6 Sir Fahim QaziMuhammad Hamza AijaziNo ratings yet

- ADFM Cash BudgetDocument5 pagesADFM Cash BudgetNidheena K SNo ratings yet

- A. Sales Budget (4items)Document3 pagesA. Sales Budget (4items)Nin JahNo ratings yet

- Cash BudgetingDocument3 pagesCash Budgetingsunil.ctNo ratings yet

- Receipts: Closing Balance (A-B) 33,000 27,000 34,750Document6 pagesReceipts: Closing Balance (A-B) 33,000 27,000 34,750rajyalakshmiNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- O P Jindal Modern School, Hisar: Worksheet No. 3 Subject-Evs NAME: ................... ROLL NO. . Class 5Document2 pagesO P Jindal Modern School, Hisar: Worksheet No. 3 Subject-Evs NAME: ................... ROLL NO. . Class 5Raghav BansalNo ratings yet

- The Legend of Lake TobaDocument4 pagesThe Legend of Lake TobaLilis MahmudatunNo ratings yet

- PRED Dharwad Circle 2018-19 SRDocument111 pagesPRED Dharwad Circle 2018-19 SRRameshkumar Hugar54% (13)

- LIT 1 FOOTNOTE TO YOUTH With ASSIGNMENTDocument6 pagesLIT 1 FOOTNOTE TO YOUTH With ASSIGNMENTAiel Legaspi EstepaNo ratings yet

- Electro AdhesionDocument2 pagesElectro AdhesiongremlinglitchNo ratings yet

- Editing EssayDocument7 pagesEditing Essayapi-581857550No ratings yet

- Title ProposalDocument6 pagesTitle ProposalChanNo ratings yet

- Baby - Assessing The 21ST Century Skill of Learners in Multigrade ClassesDocument22 pagesBaby - Assessing The 21ST Century Skill of Learners in Multigrade ClassesHiezl Ness GonzagaNo ratings yet

- Phytoremediation 150123100305 Conversion Gate02Document49 pagesPhytoremediation 150123100305 Conversion Gate02Kumar MadhuNo ratings yet

- Table SettingDocument4 pagesTable SettingBianca FormantesNo ratings yet

- Trimestral LogicDocument4 pagesTrimestral LogicGabriel FigueroaNo ratings yet

- Sustainable DevelopmentDocument5 pagesSustainable DevelopmentMeera NairNo ratings yet

- Chapter 1 EdDocument6 pagesChapter 1 EdReffisa JiruNo ratings yet

- Weekly Home Learning Plan: Carmen National High School Carmen, San Agustin, RomblonDocument2 pagesWeekly Home Learning Plan: Carmen National High School Carmen, San Agustin, RomblonVina Verdadero TomeNo ratings yet

- Sun City Biker - November 2011Document24 pagesSun City Biker - November 2011Spotlight EP NewsNo ratings yet

- Comparative Report On Fast Food Study in Thailand, Indonesia and Vietnam in 2015Document48 pagesComparative Report On Fast Food Study in Thailand, Indonesia and Vietnam in 2015Daksh SetiaNo ratings yet

- MRCPCH DhanDocument26 pagesMRCPCH DhanRajiv KabadNo ratings yet

- Steps Involved in Business Process ReengineeringDocument2 pagesSteps Involved in Business Process ReengineeringHarrison NchoeNo ratings yet

- Experimental Study On Use of Hypo Sludge and Nylon Fibre in Paver BlockDocument6 pagesExperimental Study On Use of Hypo Sludge and Nylon Fibre in Paver BlockIJRASETPublicationsNo ratings yet

- Saleem Sinai The 1st Among 1001Document8 pagesSaleem Sinai The 1st Among 1001Sonom RahnumaNo ratings yet

- Future Simple Tense - InterrogativeDocument5 pagesFuture Simple Tense - InterrogativeanthonyleonNo ratings yet

- Hollywood Theatre Redevelopment Plan 9-12-08Document12 pagesHollywood Theatre Redevelopment Plan 9-12-08Matthew HendricksNo ratings yet

- Fundamentals of PM SZABISTDocument20 pagesFundamentals of PM SZABISTSalah Ud DinNo ratings yet

- Along Came Love by Cheryl ZeeDocument787 pagesAlong Came Love by Cheryl ZeeFungai Wise MukaratiNo ratings yet

- Lecture Notes On Software Configuration Management: Zia Syed Carnegie Mellon UniversityDocument58 pagesLecture Notes On Software Configuration Management: Zia Syed Carnegie Mellon Universityvarsha reddyNo ratings yet

- G.R. No. 122807 July 5, 1996 ROGELIO P. MENDIOLA, Petitioner, Court of Appeals and Philippine National Bank, RespondentsDocument5 pagesG.R. No. 122807 July 5, 1996 ROGELIO P. MENDIOLA, Petitioner, Court of Appeals and Philippine National Bank, RespondentsSamantha BaricauaNo ratings yet

- Sundays With YouDocument2 pagesSundays With YouLlana Claire CatudioNo ratings yet

- Immaculate Conception Academy: West CampusDocument25 pagesImmaculate Conception Academy: West CampusCrystal SnowNo ratings yet