Download as pdf or txt

You might also like

- Affidavit of Damage To VehicleDocument2 pagesAffidavit of Damage To VehicleJ Ph Selrahc92% (96)

- Equity and Adequacy in Alabama Schools and DistrictsDocument96 pagesEquity and Adequacy in Alabama Schools and DistrictsTrisha Powell Crain100% (1)

- Lenovo Thinkpad E495 E595 LCFC PICASSO EX95 JINN - DOOKU 2.0 FE495 - FE595 NM-C061 Rev 1.0 (0.1)Document65 pagesLenovo Thinkpad E495 E595 LCFC PICASSO EX95 JINN - DOOKU 2.0 FE495 - FE595 NM-C061 Rev 1.0 (0.1)Jose Mauro de SouzaNo ratings yet

- AgriPinay Simple Business PlanDocument6 pagesAgriPinay Simple Business PlanKristy Dela PeñaNo ratings yet

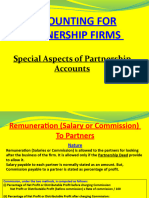

- Fundamental: Accounting For PartnershipDocument7 pagesFundamental: Accounting For PartnershipNeeraj PoddarNo ratings yet

- Chapter 6: Appropriation of Profits: Rohit AgarwalDocument4 pagesChapter 6: Appropriation of Profits: Rohit AgarwalbcomNo ratings yet

- Introduction To Ratio AnalysisDocument17 pagesIntroduction To Ratio AnalysisArnav JangidNo ratings yet

- Study Material CH.-1 Fundamentals of Partnership 2023-24Document28 pagesStudy Material CH.-1 Fundamentals of Partnership 2023-24vsy9926No ratings yet

- Accounting For Partnership Firms - Fundamentals 2021Document183 pagesAccounting For Partnership Firms - Fundamentals 2021JPS J100% (1)

- Course Materials BADVAC2X Week2Document8 pagesCourse Materials BADVAC2X Week2Mitchie FaustinoNo ratings yet

- Partnership Firms Part 2 Appropriation of ProfitDocument14 pagesPartnership Firms Part 2 Appropriation of ProfitDeepti BistNo ratings yet

- Partnership OperationDocument24 pagesPartnership OperationCASALJAY, KENT FRANCES P.No ratings yet

- Partnership OperationDocument34 pagesPartnership OperationejcapolinarNo ratings yet

- Partnership Firms - Part5 Guarantee and Past AdjustmentDocument15 pagesPartnership Firms - Part5 Guarantee and Past AdjustmentDeepti BistNo ratings yet

- Ahmadhiyya International School Syllabus: Subject: ACCOUNTING-Gr-11-Unit: Partnership Accounts-NotesDocument4 pagesAhmadhiyya International School Syllabus: Subject: ACCOUNTING-Gr-11-Unit: Partnership Accounts-NotesMohamed MuizNo ratings yet

- Ahmadhiyya International School Syllabus: Subject: ACCOUNTING-Gr-11-Unit: Partnership Accounts-NotesDocument4 pagesAhmadhiyya International School Syllabus: Subject: ACCOUNTING-Gr-11-Unit: Partnership Accounts-NotesMohamed MuizNo ratings yet

- Work Sheet On Accounting For Partnership FundamentalsDocument19 pagesWork Sheet On Accounting For Partnership Fundamentals8qk77kkhwbNo ratings yet

- Unit 5Document37 pagesUnit 5Rej HaanNo ratings yet

- Class Notes: Class: XII Topic: Accounting of Partnership Firm: Fundamentals Subject: ACCOUNTANCYDocument4 pagesClass Notes: Class: XII Topic: Accounting of Partnership Firm: Fundamentals Subject: ACCOUNTANCYDilip ChenaniNo ratings yet

- Partnership OperationDocument10 pagesPartnership OperationchristineNo ratings yet

- Partnership OperationsDocument12 pagesPartnership Operationsninny ragayNo ratings yet

- Module 3 Partnership OperationsDocument17 pagesModule 3 Partnership OperationsClaire CastrenceNo ratings yet

- CH - 2 Accounting For Partnership Firms: Fundamentals: According To Section 4 of The Partnership Act 1932Document12 pagesCH - 2 Accounting For Partnership Firms: Fundamentals: According To Section 4 of The Partnership Act 1932Laksh KhannaNo ratings yet

- Partners Hi P Operations: Lesson 4 of Financial Accounting andDocument32 pagesPartners Hi P Operations: Lesson 4 of Financial Accounting andMonicaNo ratings yet

- Partnership Operations: Accounting Cycle of A PartnershipDocument13 pagesPartnership Operations: Accounting Cycle of A Partnershipred100% (1)

- Partnership Operation 2 PDF FreeDocument12 pagesPartnership Operation 2 PDF Freehustice freedNo ratings yet

- Dissolution of PartnershipDocument17 pagesDissolution of PartnershipJASKARANNo ratings yet

- Chapter 5Document8 pagesChapter 5Gautam KumarNo ratings yet

- Class: XII Subject: Accountancy Notes On Partnership-FundamentalsDocument11 pagesClass: XII Subject: Accountancy Notes On Partnership-FundamentalsSurbhi DevnaniNo ratings yet

- Kentcoc 2Document1 pageKentcoc 2Starilazation KDNo ratings yet

- Partnership Operations - Learning MaterialDocument5 pagesPartnership Operations - Learning MaterialFaith CastroNo ratings yet

- WK 1 Intro 2 PartnershipDocument6 pagesWK 1 Intro 2 PartnershipkehindeadeniyiNo ratings yet

- Reserve and ProvisionDocument19 pagesReserve and ProvisionRojesh BasnetNo ratings yet

- Libro de AprendizajeDocument3 pagesLibro de AprendizajeElioenai SerranoNo ratings yet

- 12 AccountancyDocument4 pages12 AccountancyAbhishek DhillonNo ratings yet

- Changes in A PartnershipDocument18 pagesChanges in A PartnershipHadi HarizNo ratings yet

- Block 5 ECO 02 Unit 2Document9 pagesBlock 5 ECO 02 Unit 2HozefadahodNo ratings yet

- Last-Minute Tips For Qualifying Exam (Nov. Batch)Document7 pagesLast-Minute Tips For Qualifying Exam (Nov. Batch)aldrin casioNo ratings yet

- Partnership Operations P1Document7 pagesPartnership Operations P1Kyut KoNo ratings yet

- Chapter - 2: 14 15 Accounts-XII Quick Revision 14 15 Accounts-XII Quick RevisionDocument4 pagesChapter - 2: 14 15 Accounts-XII Quick Revision 14 15 Accounts-XII Quick RevisionIqra MughalNo ratings yet

- Partnership Firms - Part 4 Special AspectsDocument20 pagesPartnership Firms - Part 4 Special AspectsDeepti BistNo ratings yet

- Fundamental of PatnershipDocument21 pagesFundamental of PatnershipHamza RiyazNo ratings yet

- Partnership Operations PDFDocument5 pagesPartnership Operations PDFSameer Hussain67% (3)

- PartnershipDocument6 pagesPartnershipabhishekanandsingh123goNo ratings yet

- AccountancyDocument6 pagesAccountancyManu BabuNo ratings yet

- Partnership AccountingDocument7 pagesPartnership AccountingZaid ZubairiNo ratings yet

- Profit & Loss Appropriation Account, Admission, Retirement and Death of A Partner, and Dissolution of A Partnership FirmDocument10 pagesProfit & Loss Appropriation Account, Admission, Retirement and Death of A Partner, and Dissolution of A Partnership Firmd-fbuser-65596417No ratings yet

- Accounting For Partnership - Basic ConceptsDocument19 pagesAccounting For Partnership - Basic ConceptsAashutosh PatodiaNo ratings yet

- C Apre6 Spectrans Module 2 PDFDocument11 pagesC Apre6 Spectrans Module 2 PDFSittie Ainna Acmed UnteNo ratings yet

- Accounts Foundation RevisionDocument66 pagesAccounts Foundation RevisionABHISHEK SINGH 2124600No ratings yet

- 23 PartnershiptheoryDocument10 pages23 PartnershiptheorySanjeev MiglaniNo ratings yet

- Simplified Business Plan On Swine Production: By: Jourly C. RanqueDocument7 pagesSimplified Business Plan On Swine Production: By: Jourly C. RanqueJOURLY RANQUENo ratings yet

- CH 19-Notes 1025242961Document7 pagesCH 19-Notes 1025242961ayten.ayman.elerakyNo ratings yet

- Notes On Depreciation Class-11Document5 pagesNotes On Depreciation Class-11Suresh Kumar100% (1)

- SYJC AccountsDocument6 pagesSYJC Accountsprabodhcms0% (1)

- POA Section 8 PartnershipsDocument26 pagesPOA Section 8 Partnershipskxng ultimateNo ratings yet

- Partnership Operations ReviewDocument37 pagesPartnership Operations ReviewShin Shan JeonNo ratings yet

- Accounting For PartnershipDocument15 pagesAccounting For Partnershipnagesh dashNo ratings yet

- Chapter 8 Partnership AccountingDocument16 pagesChapter 8 Partnership Accountingk.muhammed aaqibNo ratings yet

- PC2 AnswerSheetDocument3 pagesPC2 AnswerSheetLuWiz DiazNo ratings yet

- 02, Accounting & Financial Analysis: 13, Preparation of Profit and Loss Accounts Loss AccountDocument14 pages02, Accounting & Financial Analysis: 13, Preparation of Profit and Loss Accounts Loss AccountHOD Dept of BBA Vels UniversityNo ratings yet

- Non Trading by MeDocument23 pagesNon Trading by MeQuality Assurance ManagerNo ratings yet

- Teacher's RoutineDocument16 pagesTeacher's RoutineNeerajNo ratings yet

- Rouitne VI To XIIDocument10 pagesRouitne VI To XIINeerajNo ratings yet

- 11 Economics Imp Vsa ch3Document2 pages11 Economics Imp Vsa ch3NeerajNo ratings yet

- Cbse Training: ReceiptDocument1 pageCbse Training: ReceiptNeerajNo ratings yet

- Cbse Training: ReceiptDocument1 pageCbse Training: ReceiptNeerajNo ratings yet

- CBSE Class 12 Economics Sample Question Paper 2020Document12 pagesCBSE Class 12 Economics Sample Question Paper 2020NeerajNo ratings yet

- JRU Prospectus 2022Document38 pagesJRU Prospectus 2022NeerajNo ratings yet

- Class 11 Sample Papers Economics 2023 3Document4 pagesClass 11 Sample Papers Economics 2023 3NeerajNo ratings yet

- Subject Verb Agreement ExcercisesDocument14 pagesSubject Verb Agreement ExcercisesEmilyn Mata CastilloNo ratings yet

- Mlaw Past Papers Since 2019-1Document107 pagesMlaw Past Papers Since 2019-1JawadNo ratings yet

- Breakdown of ExpensesDocument6 pagesBreakdown of ExpensesKim SablayanNo ratings yet

- GOPAL JAGDISH KULKARNI (1042190088) 2019-2020 Semester I Fy, MGMT, Mba, En, Revised - CDocument1 pageGOPAL JAGDISH KULKARNI (1042190088) 2019-2020 Semester I Fy, MGMT, Mba, En, Revised - CGopal KulkarniNo ratings yet

- Erp. ReportingDocument67 pagesErp. ReportingKenneth Roy MatuguinaNo ratings yet

- Q2 Week 8 - ADM ModuleDocument4 pagesQ2 Week 8 - ADM ModuleCathleenbeth MorialNo ratings yet

- Astm C0969 - 1 (En)Document3 pagesAstm C0969 - 1 (En)Dinesh Sai100% (1)

- 1571200894498vXFbvpGvTzdbgeN8 PDFDocument3 pages1571200894498vXFbvpGvTzdbgeN8 PDFBazidpur GsssNo ratings yet

- Mathematics of Finance HandoutDocument10 pagesMathematics of Finance Handoutleandro2620010% (2)

- Criminal Procedure Code Project: Rajesh Ranjan Yadav Vs - CBI and OthersDocument8 pagesCriminal Procedure Code Project: Rajesh Ranjan Yadav Vs - CBI and OthersRahul MuthuNo ratings yet

- Meiji Japan and East Asia HandoutDocument4 pagesMeiji Japan and East Asia HandoutgozappariNo ratings yet

- Case Note Judgment of The Supreme Court in The Essar Steel CaseDocument9 pagesCase Note Judgment of The Supreme Court in The Essar Steel CaseSakthi NathanNo ratings yet

- Preliminary Program IPSADocument261 pagesPreliminary Program IPSApics3441100% (1)

- HSBC Rewards and Cashback Sales Deck A4 Digital Final Q1Document15 pagesHSBC Rewards and Cashback Sales Deck A4 Digital Final Q1Madhuritha RajapakseNo ratings yet

- Know Your Vessel Case Studies in Steering Clear of Sanctions EvasionDocument15 pagesKnow Your Vessel Case Studies in Steering Clear of Sanctions EvasionAlly Hassan AliNo ratings yet

- Flag and Class RequirementsDocument4 pagesFlag and Class RequirementsAlexPredaNo ratings yet

- Maharashtra State PoliticsDocument2 pagesMaharashtra State Politicsvedanti shindeNo ratings yet

- PTA (TGT) Contract 13012015 RamanDocument15 pagesPTA (TGT) Contract 13012015 Ramanसबका बापNo ratings yet

- Impres Battery Fleet Management Troubleshooting Guide: JANUARY 2021Document10 pagesImpres Battery Fleet Management Troubleshooting Guide: JANUARY 2021Alfonso Garcia LozanoNo ratings yet

- RousseauDocument3 pagesRousseauपुष्कर मिश्रNo ratings yet

- DirectoryDocument3 pagesDirectoryfem-femNo ratings yet

- Quotation For Food Stall For Mr. Abdullah Hamed Rev. 00Document2 pagesQuotation For Food Stall For Mr. Abdullah Hamed Rev. 00anwar surNo ratings yet

- R131S2 (B) - SANTOS VS NSODocument17 pagesR131S2 (B) - SANTOS VS NSOAllyza SantosNo ratings yet

- Item5 Malaysia 1 Main 0Document10 pagesItem5 Malaysia 1 Main 0veiathishvaarimurugan100% (1)

- Purchase-To-Pay Process Map: Inventory DepartmentDocument2 pagesPurchase-To-Pay Process Map: Inventory DepartmentDanielle MarundanNo ratings yet

- Esguerra v. Trinidad, G.R. No. 169890, Mar. 12, 2007Document12 pagesEsguerra v. Trinidad, G.R. No. 169890, Mar. 12, 2007idko2wNo ratings yet

- Asme PTC-1-2011Document28 pagesAsme PTC-1-2011andhucaosNo ratings yet