Download as pdf or txt

You might also like

- MT700Document3 pagesMT700Mikol Be50% (2)

- VerbiageDocument5 pagesVerbiageTuan Ku Rao100% (1)

- LC From Cambodia 2018-12-26Document3 pagesLC From Cambodia 2018-12-26Derek ChiuNo ratings yet

- Via Hans - SBLC SCB HK 73%+2%Document28 pagesVia Hans - SBLC SCB HK 73%+2%Raja RoyNo ratings yet

- 4-5 - Draft Agreement GPI AUTOMATIC Conditional Bank Endorse PGLDocument13 pages4-5 - Draft Agreement GPI AUTOMATIC Conditional Bank Endorse PGLhford5734_638722150No ratings yet

- Group 6 Group Assignment Chapter 3Document6 pagesGroup 6 Group Assignment Chapter 3CatnipNo ratings yet

- Yêu Cầu Phát Hành Thư Tín DụngDocument4 pagesYêu Cầu Phát Hành Thư Tín DụngtranbqbNo ratings yet

- 1241209/G786L/BGAG/234: Sender Bank Details - First PartyDocument15 pages1241209/G786L/BGAG/234: Sender Bank Details - First PartyRian Hidayat100% (1)

- Firmwide One Pager - Michigan (1) JP MorganDocument2 pagesFirmwide One Pager - Michigan (1) JP MorganRamisa RobNo ratings yet

- Barcode MGDocument16 pagesBarcode MGarjunachu81100% (1)

- Review Questions On Documents and Payment MethodsDocument10 pagesReview Questions On Documents and Payment Methodsgdragon7012No ratings yet

- Contract Correcting and Drafting FinalDocument7 pagesContract Correcting and Drafting FinalVân Anh LêNo ratings yet

- FakeDocument8 pagesFakePhương LinhNo ratings yet

- UntitledDocument13 pagesUntitledNguyễn Võ Bảo NgaNo ratings yet

- Hop Dong Xuat LCDocument5 pagesHop Dong Xuat LCBình Đỗ ThanhNo ratings yet

- Loi - 44+2 - BG - Uk V.2 DPDocument17 pagesLoi - 44+2 - BG - Uk V.2 DPAtthippattu Srinivasan MuralitharanNo ratings yet

- ELLI - N46 UREA - FCO - DFN Global Network Pte LTDDocument13 pagesELLI - N46 UREA - FCO - DFN Global Network Pte LTDChandan Jst100% (1)

- Gold Format For Client-PdffillerDocument4 pagesGold Format For Client-PdffillerkarismaqdotNo ratings yet

- Screenshot 2021-06-25 at 05.38.49Document24 pagesScreenshot 2021-06-25 at 05.38.49gentot yulianto100% (1)

- 6-HD Ztdx18-11-0588qp-Yb + BCTDocument22 pages6-HD Ztdx18-11-0588qp-Yb + BCTThi Hồng nguyễnNo ratings yet

- Review Exercise 2023Document4 pagesReview Exercise 2023Nguyễn Phạm Quỳnh NhưNo ratings yet

- - Nguyễn Thị Ngân (ttqt)Document3 pages- Nguyễn Thị Ngân (ttqt)NgânNo ratings yet

- 1NMG Cifscouniversald HuangDocument3 pages1NMG Cifscouniversald HuangGrigory Vladimirovich TishkinNo ratings yet

- Group Assignment Chapter 5Document2 pagesGroup Assignment Chapter 5Thuong Nguyen100% (1)

- Giấy Đề Nghị Mở LC Trả Ngay .Do CDocument3 pagesGiấy Đề Nghị Mở LC Trả Ngay .Do CHuy ThaiNo ratings yet

- Hoàng Thu Hương - 31211025044 - Individual Assignment C3Document3 pagesHoàng Thu Hương - 31211025044 - Individual Assignment C3Hương HoàngNo ratings yet

- Parties Involved in Transaction: Exporter (Drawer)Document6 pagesParties Involved in Transaction: Exporter (Drawer)Farooq Sajjad AlamNo ratings yet

- Shipping and Customs Formalities For Import & Export ConsignmentsDocument4 pagesShipping and Customs Formalities For Import & Export ConsignmentsMM. HasanNo ratings yet

- Import & Expo PresentationDocument20 pagesImport & Expo PresentationsNo ratings yet

- Solución Dinamica Interpretacion de Carta de Credito S10Document8 pagesSolución Dinamica Interpretacion de Carta de Credito S10Carlos AssenNo ratings yet

- Import - LC DraftDocument2 pagesImport - LC DraftPandi RajaNo ratings yet

- Draft LC 700Document5 pagesDraft LC 700Panda NababanNo ratings yet

- Company Letter Head: Letter of Request (Lor)Document28 pagesCompany Letter Head: Letter of Request (Lor)Thomas HiggsNo ratings yet

- Unit 4 - Exercises to sts tiếng anh chuyên ngành 3 FTUDocument6 pagesUnit 4 - Exercises to sts tiếng anh chuyên ngành 3 FTUvunguyenvankhanh171104No ratings yet

- Requirement: You Are The Importer, Fill in The Documentary Credit Application Form For Missing Information As FollowsDocument1 pageRequirement: You Are The Importer, Fill in The Documentary Credit Application Form For Missing Information As FollowsMai ChiNo ratings yet

- Letter of Credit NKDocument4 pagesLetter of Credit NKChâu PhạmNo ratings yet

- Bai Tap HPDocument3 pagesBai Tap HPĐỗ Tấn QuốcNo ratings yet

- Lc-Draft: SUISSE BANK PLC, Trojan House, Top Floor, 34 Arcadia Avenue, London N3 2JU, United Kingdom 1Document3 pagesLc-Draft: SUISSE BANK PLC, Trojan House, Top Floor, 34 Arcadia Avenue, London N3 2JU, United Kingdom 1Chandan JstNo ratings yet

- Draft LC ChesHkDocument2 pagesDraft LC ChesHkputratea810% (1)

- Howtoopenletterofcredit 150219123447 Conversion Gate01Document13 pagesHowtoopenletterofcredit 150219123447 Conversion Gate01Mrzovic Oil and Gas Oil and GasNo ratings yet

- 103 M D 1 (2) PrimoDocument14 pages103 M D 1 (2) PrimoAnonymous qfl2Gqbkt100% (2)

- Gold 2Document4 pagesGold 2amarsdeo100% (1)

- LC ApplicationDocument2 pagesLC ApplicationShruti BudhirajaNo ratings yet

- Bài Tập Unit 4Document7 pagesBài Tập Unit 4Nguyễn Lanh AnhNo ratings yet

- Pon Sanger ExportsDocument11 pagesPon Sanger ExportsTaruna BhadanaNo ratings yet

- LC Draft - (Client) - SCBDocument3 pagesLC Draft - (Client) - SCBDima RajaNo ratings yet

- LCD79741Document3 pagesLCD79741donglaiduyNo ratings yet

- mẫu đơn xin mở tín dụng thưDocument3 pagesmẫu đơn xin mở tín dụng thưhungNo ratings yet

- Universitatea Bucuresti Marketing Anul I: Ciocan Maria LucianaDocument15 pagesUniversitatea Bucuresti Marketing Anul I: Ciocan Maria LucianaJianu Florin-SilviuNo ratings yet

- Hridoy MD Jahid Hossain (2016006704)Document3 pagesHridoy MD Jahid Hossain (2016006704)Jh HridoyNo ratings yet

- Answer To The Question of Part-1Document3 pagesAnswer To The Question of Part-1Jh HridoyNo ratings yet

- SB Draft LCDocument3 pagesSB Draft LCsyedibrahimmuazzamNo ratings yet

- Viet Hoi PhieuDocument9 pagesViet Hoi Phieuthaiquangsang92No ratings yet

- Urea 46% KazahDocument5 pagesUrea 46% Kazahkurbatov11No ratings yet

- Hoi Phieu - Giai Bai TapDocument6 pagesHoi Phieu - Giai Bai TapBảo Lâm Nguyễn NgọcNo ratings yet

- Wa0016Document6 pagesWa0016trustcompanyNo ratings yet

- Sight Via MT 700 - 701Document5 pagesSight Via MT 700 - 701nghity22409No ratings yet

- Unclaimed Money - Step by Step Guide how you claim your moneyFrom EverandUnclaimed Money - Step by Step Guide how you claim your moneyNo ratings yet

- Letters of Credit and Documentary Collections: An Export and Import GuideFrom EverandLetters of Credit and Documentary Collections: An Export and Import GuideRating: 1 out of 5 stars1/5 (1)

- Repairing Your Identity and Credit: A Comprehensive Easy to Follow Instruction GuideFrom EverandRepairing Your Identity and Credit: A Comprehensive Easy to Follow Instruction GuideNo ratings yet

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Front Page FormatDocument7 pagesFront Page FormatArunKumarNo ratings yet

- Retroactive Price in Procurement CloudDocument14 pagesRetroactive Price in Procurement CloudranvijayNo ratings yet

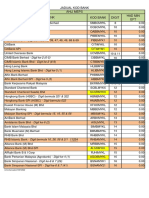

- JADUAL KOD BANK TERKINI (Kemaskini 10012022)Document1 pageJADUAL KOD BANK TERKINI (Kemaskini 10012022)DygKuNormarzuraNo ratings yet

- "Why Perfion Gives You The Highest ROI of All... ": Product Information ManagementDocument8 pages"Why Perfion Gives You The Highest ROI of All... ": Product Information ManagementpttaNo ratings yet

- Hunter Insurance PolicyDocument10 pagesHunter Insurance PolicyAli AbdullahNo ratings yet

- Credit ManagementDocument20 pagesCredit ManagementNausheen Ahmed NobaNo ratings yet

- Poriazis Fruits Business PlanDocument6 pagesPoriazis Fruits Business PlanDimitri Poriazis50% (2)

- Strategic Development at Virgin 2013: About The Virgin GroupDocument6 pagesStrategic Development at Virgin 2013: About The Virgin GrouphjNo ratings yet

- Amsteel CatalogueDocument45 pagesAmsteel CatalogueSyafiq KamaluddinNo ratings yet

- COA PresentationDocument19 pagesCOA PresentationJim B Punz100% (1)

- Jessica Chong CV - Sep 2018Document1 pageJessica Chong CV - Sep 2018Anonymous H5Ru4rvuHNo ratings yet

- Strategic Decision Making and Functional Decision MakingDocument11 pagesStrategic Decision Making and Functional Decision Makingajo arveniaNo ratings yet

- International Trade TestDocument2 pagesInternational Trade TestFifi FifilacheNo ratings yet

- IDEX Magazine, December 2012Document72 pagesIDEX Magazine, December 2012New Acropolis Mumbai100% (1)

- Tilapia Farm Business Management and Economics: A Training ManualDocument43 pagesTilapia Farm Business Management and Economics: A Training ManualAquaponics100% (1)

- Startup Funding StagesDocument4 pagesStartup Funding StagesSachin KhuranaNo ratings yet

- Authorized Causes, Resignation, and Retirement-1Document86 pagesAuthorized Causes, Resignation, and Retirement-1patricia guillermo0% (1)

- Bank Chain Testing ProcessDocument5 pagesBank Chain Testing ProcessdurjaymNo ratings yet

- Local TaxDocument68 pagesLocal Taxambonulan100% (1)

- Finland National Innovation StrategyDocument50 pagesFinland National Innovation Strategya1b2c3z1No ratings yet

- Enterprise Applications: Case 1Document42 pagesEnterprise Applications: Case 1will willNo ratings yet

- Whittle OptimiseDocument0 pagesWhittle OptimiseGegedukNo ratings yet

- Mohammad Abu Taher: Apply For: QA/QC (Senior Piping Welding Inspector) Personal DetailsDocument10 pagesMohammad Abu Taher: Apply For: QA/QC (Senior Piping Welding Inspector) Personal DetailsRajkumar ANo ratings yet

- Creating A Statement of Purpose An Essential New Action Tool For Small and Medium Size Organizations by Francis P. PandolfiDocument16 pagesCreating A Statement of Purpose An Essential New Action Tool For Small and Medium Size Organizations by Francis P. PandolfiGaurav TyagiNo ratings yet

- Corporate Social Responsibility: Doing The Most Good For Your Company and Your CauseDocument69 pagesCorporate Social Responsibility: Doing The Most Good For Your Company and Your CauseNabilaNo ratings yet

- Sales Order - 010224 - Teras Angkasa (Unsigned)Document1 pageSales Order - 010224 - Teras Angkasa (Unsigned)Fachry RasyidinNo ratings yet

- Practice Problem - LeasesDocument2 pagesPractice Problem - LeasesNitinNo ratings yet