Chapter 5

Chapter 5

You might also like

- Simplified Invoice: Invoice Number Date of Transaction Date of IssueDocument1 pageSimplified Invoice: Invoice Number Date of Transaction Date of IssueradhoinezerellyNo ratings yet

- 2412 Payslip JunDocument1 page2412 Payslip JunAnonymous 68rvpJvvNo ratings yet

- Income From HP PDFDocument14 pagesIncome From HP PDFNanda NanduNo ratings yet

- Income From House Property 12th July 23Document39 pagesIncome From House Property 12th July 23Ashish KumarNo ratings yet

- Income From House PropertyDocument6 pagesIncome From House Propertypardeep bainsNo ratings yet

- Unit 2 (Income From House Property)Document13 pagesUnit 2 (Income From House Property)Vijay GiriNo ratings yet

- Chapter-4b Income From House Property PDFDocument6 pagesChapter-4b Income From House Property PDFBrinda RNo ratings yet

- Income From House Property: Section/Rule Subject MatterDocument21 pagesIncome From House Property: Section/Rule Subject Matterphanidhar varanasiNo ratings yet

- Tax ProjectDocument12 pagesTax ProjectUtkarsh SinghNo ratings yet

- Chapter 5 Income From House Property PMDocument14 pagesChapter 5 Income From House Property PMMohammad Yusuf NabeelNo ratings yet

- Income From House PropertyDocument23 pagesIncome From House PropertySahil14JNo ratings yet

- Income From House Property: Chapter - 4 Unit - 3Document24 pagesIncome From House Property: Chapter - 4 Unit - 3srinidhivrNo ratings yet

- Income From House PropertyDocument31 pagesIncome From House PropertyAarti SainiNo ratings yet

- Income From House PropertyDocument74 pagesIncome From House PropertyHarshit YNo ratings yet

- Short Notes of House PropertyDocument3 pagesShort Notes of House PropertyutsavNo ratings yet

- House Property - Summary (PY 2020-21 AY 2021-22)Document5 pagesHouse Property - Summary (PY 2020-21 AY 2021-22)Aruna RajappaNo ratings yet

- Chapter 5 Income From House PropertyDocument19 pagesChapter 5 Income From House PropertysagarNo ratings yet

- Tax ProjectDocument40 pagesTax ProjectGunaNo ratings yet

- Income From House PropertyDocument5 pagesIncome From House PropertyParas SinghNo ratings yet

- House PropertyDocument7 pagesHouse Propertyatul.maurya0290No ratings yet

- Income From House Property: After Studying This Chapter, You Would Be Able ToDocument38 pagesIncome From House Property: After Studying This Chapter, You Would Be Able ToAnkitaNo ratings yet

- House Property ChapterDocument64 pagesHouse Property ChapterManohar LalNo ratings yet

- Session 11-12 Income From House PropertyDocument7 pagesSession 11-12 Income From House PropertyNoob GamerNo ratings yet

- House PropertyDocument33 pagesHouse PropertypriyaNo ratings yet

- Assignment - 1 1. What Do You Mean by "Gross Annual Value"? How To Calculate The Income Under The Head "Income From House Property"?Document11 pagesAssignment - 1 1. What Do You Mean by "Gross Annual Value"? How To Calculate The Income Under The Head "Income From House Property"?Khushi ChadhaNo ratings yet

- Income From Bnvvbhouse Property SakshamDocument25 pagesIncome From Bnvvbhouse Property SakshamRohit KumarNo ratings yet

- PDF Document AB2D94598B09 1Document28 pagesPDF Document AB2D94598B09 120BRM051 Sukant SNo ratings yet

- Income From House Property: After Studying This Chapter, You Would Be Able ToDocument35 pagesIncome From House Property: After Studying This Chapter, You Would Be Able ToLilyNo ratings yet

- Tax HandoutDocument6 pagesTax Handoutshekharsuhani5No ratings yet

- Heads of Income: Unit - 2: Income From House PropertyDocument40 pagesHeads of Income: Unit - 2: Income From House PropertyMaheswar SethiNo ratings yet

- Direct Taxation - 1582Document21 pagesDirect Taxation - 1582Maneesh ReddyNo ratings yet

- House Property IncomeDocument4 pagesHouse Property IncomeOnkar BandichhodeNo ratings yet

- Income From House Property PracticalDocument52 pagesIncome From House Property PracticalShreekanta DattaNo ratings yet

- Income From House Property: Prepared By: Mandeep KaurDocument69 pagesIncome From House Property: Prepared By: Mandeep KaurSresth VermaNo ratings yet

- Income From House Property: After Studying This Chapter, You Would Be Able ToDocument40 pagesIncome From House Property: After Studying This Chapter, You Would Be Able ToManoj GNo ratings yet

- 62289bos50449 Mod1 cp5Document41 pages62289bos50449 Mod1 cp5monicabhat96No ratings yet

- 56465bos45796cp4u2 PDFDocument49 pages56465bos45796cp4u2 PDFNarendra VasavanNo ratings yet

- House ProDocument7 pagesHouse Prosb_jainNo ratings yet

- Income From House Property-6Document9 pagesIncome From House Property-6s4sahithNo ratings yet

- Income From House PropertyDocument6 pagesIncome From House PropertyKamini PawarNo ratings yet

- Vacancy & Unrealised RentDocument7 pagesVacancy & Unrealised RentKiran ChristyNo ratings yet

- Income From House PropertyDocument12 pagesIncome From House PropertydipxxxNo ratings yet

- Incomefromhouse Property JeevithaDocument22 pagesIncomefromhouse Property Jeevitharyanraj008No ratings yet

- Income From House PropertyDocument14 pagesIncome From House Propertyjack2529007No ratings yet

- 02 House Property Notes 23Document14 pages02 House Property Notes 23Hritik HarlalkaNo ratings yet

- Income From House PropertyDocument7 pagesIncome From House Propertyrhrishad1No ratings yet

- Unit - 2: Income From House Property: After Studying This Chapter, You Would Be Able ToDocument47 pagesUnit - 2: Income From House Property: After Studying This Chapter, You Would Be Able Toadityaraj purohitNo ratings yet

- Income From House PropertyDocument35 pagesIncome From House PropertyroopamNo ratings yet

- Income Under The Head "Income From House Property": Quick Review of The ChapterDocument5 pagesIncome Under The Head "Income From House Property": Quick Review of The ChapterKaustubh BasuNo ratings yet

- Income From House PropertyDocument15 pagesIncome From House PropertyMansi DabasNo ratings yet

- II. Income Under The House Properties :: Basis of Charge Section 22Document4 pagesII. Income Under The House Properties :: Basis of Charge Section 22Akash Singh RajputNo ratings yet

- Study Note: 8 Income From House Property: 8.1 Basis of Charge (Section 22)Document19 pagesStudy Note: 8 Income From House Property: 8.1 Basis of Charge (Section 22)T.S.G RamaraoNo ratings yet

- Unit 3 (Income From House Property) - 1Document5 pagesUnit 3 (Income From House Property) - 1Vijay GiriNo ratings yet

- House Property IncomeDocument21 pagesHouse Property IncomekhNo ratings yet

- House Property TaxationDocument13 pagesHouse Property TaxationAnupam BaliNo ratings yet

- Computation of Income From House PropertDocument20 pagesComputation of Income From House PropertSIDDHART BHANSALINo ratings yet

- Income From House Property: Ms. Harmanpreet Kaur Assistant Professor Shivaji College University of DelhiDocument40 pagesIncome From House Property: Ms. Harmanpreet Kaur Assistant Professor Shivaji College University of DelhiRAKESH KUMAR GOUTAMNo ratings yet

- Income From House PropertyDocument14 pagesIncome From House PropertyshivNo ratings yet

- 07 Income From Property (50 59)Document11 pages07 Income From Property (50 59)jafferyasim100% (2)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Nov 23 StrategyDocument25 pagesNov 23 StrategyCA Mohit SharmaNo ratings yet

- Financial Reporting Strategy For May 23Document3 pagesFinancial Reporting Strategy For May 23CA Mohit SharmaNo ratings yet

- IBC Part - 1 PDFDocument12 pagesIBC Part - 1 PDFCA Mohit SharmaNo ratings yet

- PIRP Summary Notes by CA Mohit SharmaDocument7 pagesPIRP Summary Notes by CA Mohit SharmaCA Mohit SharmaNo ratings yet

- Chapter 2Document13 pagesChapter 2CA Mohit SharmaNo ratings yet

- Chapter 3 Corporate & Economic LawDocument7 pagesChapter 3 Corporate & Economic LawCA Mohit SharmaNo ratings yet

- Audit Strategy For May 23Document3 pagesAudit Strategy For May 23CA Mohit SharmaNo ratings yet

- Chapter 1 SCMPE Theory Keyword NotesDocument6 pagesChapter 1 SCMPE Theory Keyword NotesCA Mohit SharmaNo ratings yet

- Chapter 1Document5 pagesChapter 1CA Mohit SharmaNo ratings yet

- Chapter 2 Corporate & Economic LawDocument13 pagesChapter 2 Corporate & Economic LawCA Mohit SharmaNo ratings yet

- Chapter 1 SFM (Theory)Document5 pagesChapter 1 SFM (Theory)CA Mohit SharmaNo ratings yet

- Formats For Consolidation Group StructureDocument4 pagesFormats For Consolidation Group StructureMuhammad3588No ratings yet

- BIR Ruling 359-17Document5 pagesBIR Ruling 359-17Bobby Olavides SebastianNo ratings yet

- JL3 Electric Bill 2Document2 pagesJL3 Electric Bill 2jointariqaslamNo ratings yet

- 558 /5 Sanghrajka House Adenwala Road Near Five Garden Matunga MUMBAI - 400019 Maharashtra, IndiaDocument2 pages558 /5 Sanghrajka House Adenwala Road Near Five Garden Matunga MUMBAI - 400019 Maharashtra, IndiaPankaj GuptaNo ratings yet

- After-Tax Economic Analysis: Engineering EconomyDocument16 pagesAfter-Tax Economic Analysis: Engineering EconomyTUẤN TRẦN MINHNo ratings yet

- VAT Booklet F.Y.2012-13Document20 pagesVAT Booklet F.Y.2012-13ankur2706No ratings yet

- Fesco Online BillDocument2 pagesFesco Online BillSaqLain AliNo ratings yet

- GST CHALLAnDocument1 pageGST CHALLAnVibhav AnasaneNo ratings yet

- Systra Philippines vs. Cir G.R. No. 176290 September 21, 2007Document2 pagesSystra Philippines vs. Cir G.R. No. 176290 September 21, 2007Armstrong BosantogNo ratings yet

- Solved Firm L Has 500 000 To Invest and Is Considering TwoDocument1 pageSolved Firm L Has 500 000 To Invest and Is Considering TwoAnbu jaromiaNo ratings yet

- Income Tax Proj Nov09Document530 pagesIncome Tax Proj Nov09nilesh_jain27No ratings yet

- AAT ITAX LRP Assessment FA2015 - Questions 2015-16Document8 pagesAAT ITAX LRP Assessment FA2015 - Questions 2015-16LindaBakóNo ratings yet

- Property LedgerDocument2 pagesProperty LedgerHemant ChaudhariNo ratings yet

- Intermediate Accounting Solutions To Exercises 11Document38 pagesIntermediate Accounting Solutions To Exercises 11Hira Farooq100% (1)

- W-9 FormDocument2 pagesW-9 FormTrish HitNo ratings yet

- Swimming Membership Receipt-MulundDocument1 pageSwimming Membership Receipt-Mulundchithur DevarajNo ratings yet

- Final ReitDocument5 pagesFinal Reitchris_yvonneNo ratings yet

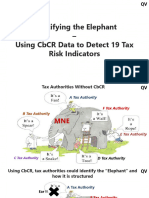

- 19 Tax Risk Indicators in CBCRDocument22 pages19 Tax Risk Indicators in CBCRidan28No ratings yet

- Bir RequirmentsDocument4 pagesBir RequirmentsMa Therese MontessoriNo ratings yet

- CBK Power Co LTD Vs CirDocument1 pageCBK Power Co LTD Vs CirlacbayenNo ratings yet

- Income Tax For Partnerships Chapter W AnswersDocument4 pagesIncome Tax For Partnerships Chapter W AnswersPrince Carl Lepiten SilvaNo ratings yet

- Black Book Final Project - GST: Manish TiwariDocument28 pagesBlack Book Final Project - GST: Manish TiwariJatin PoojariNo ratings yet

- 434 Absolute LajpatDocument2 pages434 Absolute LajpatNandu SumalNo ratings yet

- 084 CIR v. Citytrust (Potian)Document3 pages084 CIR v. Citytrust (Potian)Erika Potian100% (1)

- Van Buren May Elections - ProposalsDocument4 pagesVan Buren May Elections - ProposalsWXMINo ratings yet

- Assess The Economic Effects of A Significant Increase in Taxation On The UK EconomyDocument3 pagesAssess The Economic Effects of A Significant Increase in Taxation On The UK EconomyCalebP12No ratings yet

- 2 - CIR vs. de LaraDocument9 pages2 - CIR vs. de LaraJeanne CalalinNo ratings yet

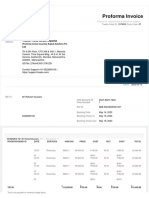

- Invoice FormatDocument3 pagesInvoice FormatNishant ChaudharyNo ratings yet

Download as pdf or txt

You might also like

- Simplified Invoice: Invoice Number Date of Transaction Date of IssueDocument1 pageSimplified Invoice: Invoice Number Date of Transaction Date of IssueradhoinezerellyNo ratings yet

- 2412 Payslip JunDocument1 page2412 Payslip JunAnonymous 68rvpJvvNo ratings yet

- Income From HP PDFDocument14 pagesIncome From HP PDFNanda NanduNo ratings yet

- Income From House Property 12th July 23Document39 pagesIncome From House Property 12th July 23Ashish KumarNo ratings yet

- Income From House PropertyDocument6 pagesIncome From House Propertypardeep bainsNo ratings yet

- Unit 2 (Income From House Property)Document13 pagesUnit 2 (Income From House Property)Vijay GiriNo ratings yet

- Chapter-4b Income From House Property PDFDocument6 pagesChapter-4b Income From House Property PDFBrinda RNo ratings yet

- Income From House Property: Section/Rule Subject MatterDocument21 pagesIncome From House Property: Section/Rule Subject Matterphanidhar varanasiNo ratings yet

- Tax ProjectDocument12 pagesTax ProjectUtkarsh SinghNo ratings yet

- Chapter 5 Income From House Property PMDocument14 pagesChapter 5 Income From House Property PMMohammad Yusuf NabeelNo ratings yet

- Income From House PropertyDocument23 pagesIncome From House PropertySahil14JNo ratings yet

- Income From House Property: Chapter - 4 Unit - 3Document24 pagesIncome From House Property: Chapter - 4 Unit - 3srinidhivrNo ratings yet

- Income From House PropertyDocument31 pagesIncome From House PropertyAarti SainiNo ratings yet

- Income From House PropertyDocument74 pagesIncome From House PropertyHarshit YNo ratings yet

- Short Notes of House PropertyDocument3 pagesShort Notes of House PropertyutsavNo ratings yet

- House Property - Summary (PY 2020-21 AY 2021-22)Document5 pagesHouse Property - Summary (PY 2020-21 AY 2021-22)Aruna RajappaNo ratings yet

- Chapter 5 Income From House PropertyDocument19 pagesChapter 5 Income From House PropertysagarNo ratings yet

- Tax ProjectDocument40 pagesTax ProjectGunaNo ratings yet

- Income From House PropertyDocument5 pagesIncome From House PropertyParas SinghNo ratings yet

- House PropertyDocument7 pagesHouse Propertyatul.maurya0290No ratings yet

- Income From House Property: After Studying This Chapter, You Would Be Able ToDocument38 pagesIncome From House Property: After Studying This Chapter, You Would Be Able ToAnkitaNo ratings yet

- House Property ChapterDocument64 pagesHouse Property ChapterManohar LalNo ratings yet

- Session 11-12 Income From House PropertyDocument7 pagesSession 11-12 Income From House PropertyNoob GamerNo ratings yet

- House PropertyDocument33 pagesHouse PropertypriyaNo ratings yet

- Assignment - 1 1. What Do You Mean by "Gross Annual Value"? How To Calculate The Income Under The Head "Income From House Property"?Document11 pagesAssignment - 1 1. What Do You Mean by "Gross Annual Value"? How To Calculate The Income Under The Head "Income From House Property"?Khushi ChadhaNo ratings yet

- Income From Bnvvbhouse Property SakshamDocument25 pagesIncome From Bnvvbhouse Property SakshamRohit KumarNo ratings yet

- PDF Document AB2D94598B09 1Document28 pagesPDF Document AB2D94598B09 120BRM051 Sukant SNo ratings yet

- Income From House Property: After Studying This Chapter, You Would Be Able ToDocument35 pagesIncome From House Property: After Studying This Chapter, You Would Be Able ToLilyNo ratings yet

- Tax HandoutDocument6 pagesTax Handoutshekharsuhani5No ratings yet

- Heads of Income: Unit - 2: Income From House PropertyDocument40 pagesHeads of Income: Unit - 2: Income From House PropertyMaheswar SethiNo ratings yet

- Direct Taxation - 1582Document21 pagesDirect Taxation - 1582Maneesh ReddyNo ratings yet

- House Property IncomeDocument4 pagesHouse Property IncomeOnkar BandichhodeNo ratings yet

- Income From House Property PracticalDocument52 pagesIncome From House Property PracticalShreekanta DattaNo ratings yet

- Income From House Property: Prepared By: Mandeep KaurDocument69 pagesIncome From House Property: Prepared By: Mandeep KaurSresth VermaNo ratings yet

- Income From House Property: After Studying This Chapter, You Would Be Able ToDocument40 pagesIncome From House Property: After Studying This Chapter, You Would Be Able ToManoj GNo ratings yet

- 62289bos50449 Mod1 cp5Document41 pages62289bos50449 Mod1 cp5monicabhat96No ratings yet

- 56465bos45796cp4u2 PDFDocument49 pages56465bos45796cp4u2 PDFNarendra VasavanNo ratings yet

- House ProDocument7 pagesHouse Prosb_jainNo ratings yet

- Income From House Property-6Document9 pagesIncome From House Property-6s4sahithNo ratings yet

- Income From House PropertyDocument6 pagesIncome From House PropertyKamini PawarNo ratings yet

- Vacancy & Unrealised RentDocument7 pagesVacancy & Unrealised RentKiran ChristyNo ratings yet

- Income From House PropertyDocument12 pagesIncome From House PropertydipxxxNo ratings yet

- Incomefromhouse Property JeevithaDocument22 pagesIncomefromhouse Property Jeevitharyanraj008No ratings yet

- Income From House PropertyDocument14 pagesIncome From House Propertyjack2529007No ratings yet

- 02 House Property Notes 23Document14 pages02 House Property Notes 23Hritik HarlalkaNo ratings yet

- Income From House PropertyDocument7 pagesIncome From House Propertyrhrishad1No ratings yet

- Unit - 2: Income From House Property: After Studying This Chapter, You Would Be Able ToDocument47 pagesUnit - 2: Income From House Property: After Studying This Chapter, You Would Be Able Toadityaraj purohitNo ratings yet

- Income From House PropertyDocument35 pagesIncome From House PropertyroopamNo ratings yet

- Income Under The Head "Income From House Property": Quick Review of The ChapterDocument5 pagesIncome Under The Head "Income From House Property": Quick Review of The ChapterKaustubh BasuNo ratings yet

- Income From House PropertyDocument15 pagesIncome From House PropertyMansi DabasNo ratings yet

- II. Income Under The House Properties :: Basis of Charge Section 22Document4 pagesII. Income Under The House Properties :: Basis of Charge Section 22Akash Singh RajputNo ratings yet

- Study Note: 8 Income From House Property: 8.1 Basis of Charge (Section 22)Document19 pagesStudy Note: 8 Income From House Property: 8.1 Basis of Charge (Section 22)T.S.G RamaraoNo ratings yet

- Unit 3 (Income From House Property) - 1Document5 pagesUnit 3 (Income From House Property) - 1Vijay GiriNo ratings yet

- House Property IncomeDocument21 pagesHouse Property IncomekhNo ratings yet

- House Property TaxationDocument13 pagesHouse Property TaxationAnupam BaliNo ratings yet

- Computation of Income From House PropertDocument20 pagesComputation of Income From House PropertSIDDHART BHANSALINo ratings yet

- Income From House Property: Ms. Harmanpreet Kaur Assistant Professor Shivaji College University of DelhiDocument40 pagesIncome From House Property: Ms. Harmanpreet Kaur Assistant Professor Shivaji College University of DelhiRAKESH KUMAR GOUTAMNo ratings yet

- Income From House PropertyDocument14 pagesIncome From House PropertyshivNo ratings yet

- 07 Income From Property (50 59)Document11 pages07 Income From Property (50 59)jafferyasim100% (2)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Nov 23 StrategyDocument25 pagesNov 23 StrategyCA Mohit SharmaNo ratings yet

- Financial Reporting Strategy For May 23Document3 pagesFinancial Reporting Strategy For May 23CA Mohit SharmaNo ratings yet

- IBC Part - 1 PDFDocument12 pagesIBC Part - 1 PDFCA Mohit SharmaNo ratings yet

- PIRP Summary Notes by CA Mohit SharmaDocument7 pagesPIRP Summary Notes by CA Mohit SharmaCA Mohit SharmaNo ratings yet

- Chapter 2Document13 pagesChapter 2CA Mohit SharmaNo ratings yet

- Chapter 3 Corporate & Economic LawDocument7 pagesChapter 3 Corporate & Economic LawCA Mohit SharmaNo ratings yet

- Audit Strategy For May 23Document3 pagesAudit Strategy For May 23CA Mohit SharmaNo ratings yet

- Chapter 1 SCMPE Theory Keyword NotesDocument6 pagesChapter 1 SCMPE Theory Keyword NotesCA Mohit SharmaNo ratings yet

- Chapter 1Document5 pagesChapter 1CA Mohit SharmaNo ratings yet

- Chapter 2 Corporate & Economic LawDocument13 pagesChapter 2 Corporate & Economic LawCA Mohit SharmaNo ratings yet

- Chapter 1 SFM (Theory)Document5 pagesChapter 1 SFM (Theory)CA Mohit SharmaNo ratings yet

- Formats For Consolidation Group StructureDocument4 pagesFormats For Consolidation Group StructureMuhammad3588No ratings yet

- BIR Ruling 359-17Document5 pagesBIR Ruling 359-17Bobby Olavides SebastianNo ratings yet

- JL3 Electric Bill 2Document2 pagesJL3 Electric Bill 2jointariqaslamNo ratings yet

- 558 /5 Sanghrajka House Adenwala Road Near Five Garden Matunga MUMBAI - 400019 Maharashtra, IndiaDocument2 pages558 /5 Sanghrajka House Adenwala Road Near Five Garden Matunga MUMBAI - 400019 Maharashtra, IndiaPankaj GuptaNo ratings yet

- After-Tax Economic Analysis: Engineering EconomyDocument16 pagesAfter-Tax Economic Analysis: Engineering EconomyTUẤN TRẦN MINHNo ratings yet

- VAT Booklet F.Y.2012-13Document20 pagesVAT Booklet F.Y.2012-13ankur2706No ratings yet

- Fesco Online BillDocument2 pagesFesco Online BillSaqLain AliNo ratings yet

- GST CHALLAnDocument1 pageGST CHALLAnVibhav AnasaneNo ratings yet

- Systra Philippines vs. Cir G.R. No. 176290 September 21, 2007Document2 pagesSystra Philippines vs. Cir G.R. No. 176290 September 21, 2007Armstrong BosantogNo ratings yet

- Solved Firm L Has 500 000 To Invest and Is Considering TwoDocument1 pageSolved Firm L Has 500 000 To Invest and Is Considering TwoAnbu jaromiaNo ratings yet

- Income Tax Proj Nov09Document530 pagesIncome Tax Proj Nov09nilesh_jain27No ratings yet

- AAT ITAX LRP Assessment FA2015 - Questions 2015-16Document8 pagesAAT ITAX LRP Assessment FA2015 - Questions 2015-16LindaBakóNo ratings yet

- Property LedgerDocument2 pagesProperty LedgerHemant ChaudhariNo ratings yet

- Intermediate Accounting Solutions To Exercises 11Document38 pagesIntermediate Accounting Solutions To Exercises 11Hira Farooq100% (1)

- W-9 FormDocument2 pagesW-9 FormTrish HitNo ratings yet

- Swimming Membership Receipt-MulundDocument1 pageSwimming Membership Receipt-Mulundchithur DevarajNo ratings yet

- Final ReitDocument5 pagesFinal Reitchris_yvonneNo ratings yet

- 19 Tax Risk Indicators in CBCRDocument22 pages19 Tax Risk Indicators in CBCRidan28No ratings yet

- Bir RequirmentsDocument4 pagesBir RequirmentsMa Therese MontessoriNo ratings yet

- CBK Power Co LTD Vs CirDocument1 pageCBK Power Co LTD Vs CirlacbayenNo ratings yet

- Income Tax For Partnerships Chapter W AnswersDocument4 pagesIncome Tax For Partnerships Chapter W AnswersPrince Carl Lepiten SilvaNo ratings yet

- Black Book Final Project - GST: Manish TiwariDocument28 pagesBlack Book Final Project - GST: Manish TiwariJatin PoojariNo ratings yet

- 434 Absolute LajpatDocument2 pages434 Absolute LajpatNandu SumalNo ratings yet

- 084 CIR v. Citytrust (Potian)Document3 pages084 CIR v. Citytrust (Potian)Erika Potian100% (1)

- Van Buren May Elections - ProposalsDocument4 pagesVan Buren May Elections - ProposalsWXMINo ratings yet

- Assess The Economic Effects of A Significant Increase in Taxation On The UK EconomyDocument3 pagesAssess The Economic Effects of A Significant Increase in Taxation On The UK EconomyCalebP12No ratings yet

- 2 - CIR vs. de LaraDocument9 pages2 - CIR vs. de LaraJeanne CalalinNo ratings yet

- Invoice FormatDocument3 pagesInvoice FormatNishant ChaudharyNo ratings yet