Download as pdf or txt

You might also like

- Accounts Manual J ZowaDocument78 pagesAccounts Manual J ZowaPassmore RulensoNo ratings yet

- Security Analysis Chapter 34 The Relation of Depreciation and Similar Charges To Earning PowerDocument3 pagesSecurity Analysis Chapter 34 The Relation of Depreciation and Similar Charges To Earning PowerTheodor Tonca0% (1)

- Solutions of The Audit Process. Principles, Practice and CasesDocument71 pagesSolutions of The Audit Process. Principles, Practice and Casesletuan221290% (10)

- ch01 Introduction Acounting & BusinessDocument37 pagesch01 Introduction Acounting & Businesskuncoroooo100% (1)

- Questions: Liabilities, and Equity. These ElementsDocument38 pagesQuestions: Liabilities, and Equity. These ElementssiaaswanNo ratings yet

- Financial Accounting NotesDocument14 pagesFinancial Accounting NotesLex XuNo ratings yet

- ACC - ACF1200 Topic 3 SOLUTIONS To Questions For Self-StudyDocument3 pagesACC - ACF1200 Topic 3 SOLUTIONS To Questions For Self-StudyChuangjia MaNo ratings yet

- Accounting AssignmentDocument6 pagesAccounting AssignmentOmer NasirNo ratings yet

- The Matching PrincipleDocument4 pagesThe Matching Principlesegayna100% (1)

- Chap 013Document45 pagesChap 013Hemali MehtaNo ratings yet

- Basic FinanceDocument67 pagesBasic Financesoref49920No ratings yet

- Topic 3 SolutionsDocument13 pagesTopic 3 SolutionsLiang BochengNo ratings yet

- Study and Briefly Explain On: Accounting Concepts AssumptionsDocument4 pagesStudy and Briefly Explain On: Accounting Concepts AssumptionsAziz AhmadNo ratings yet

- Accounting Concepts: 1. Business Entity Concept or Separate Entity ConceptDocument4 pagesAccounting Concepts: 1. Business Entity Concept or Separate Entity ConceptTawanda Tatenda HerbertNo ratings yet

- (Analisis Laporan Keuangan) Soal Dan Jawaban Chapter 2 EnglishDocument4 pages(Analisis Laporan Keuangan) Soal Dan Jawaban Chapter 2 EnglishAdinda SabeliaNo ratings yet

- Acc Project VANSHDocument12 pagesAcc Project VANSHVansh SehgalNo ratings yet

- HK MA: The Hong Kong Management Association Hong Kong Polytechnic Joint Diploma in Management StudiesDocument12 pagesHK MA: The Hong Kong Management Association Hong Kong Polytechnic Joint Diploma in Management StudiesSinoNo ratings yet

- Materiality Is A Relativity: Example: A Large Company Has A Building in The Hurricane Zone During HurricaneDocument4 pagesMateriality Is A Relativity: Example: A Large Company Has A Building in The Hurricane Zone During HurricaneDonita BinayNo ratings yet

- Owner Earnings and CapexDocument11 pagesOwner Earnings and CapexJohn Aldridge ChewNo ratings yet

- John K Peter-PGEMP58-A-39 Assignment 09 FA Week 3Document4 pagesJohn K Peter-PGEMP58-A-39 Assignment 09 FA Week 3dineshNo ratings yet

- CH 13 - Current LiabilitiesDocument85 pagesCH 13 - Current LiabilitiesViviane Tavares60% (5)

- Session 3Document13 pagesSession 3officialwork684No ratings yet

- What Is A Plant AssetDocument23 pagesWhat Is A Plant AssetMiton AlamNo ratings yet

- Fa-May-June 2011Document16 pagesFa-May-June 2011xodic49847No ratings yet

- Cost Concept of AccountingDocument3 pagesCost Concept of AccountingVidya ShaniaNo ratings yet

- Since A Long Time AgoDocument5 pagesSince A Long Time AgoPatrisia CibisovNo ratings yet

- Csec Poa Handout 3Document32 pagesCsec Poa Handout 3Taariq Abdul-MajeedNo ratings yet

- Accounting Period Shareholders DividendsDocument3 pagesAccounting Period Shareholders DividendsAmaranathreddy YgNo ratings yet

- Accounting For Non-Accounting Students - Summary Chapter 4Document4 pagesAccounting For Non-Accounting Students - Summary Chapter 4Megan Joye100% (1)

- Ans Chapter 4Document34 pagesAns Chapter 4thaovdt22414No ratings yet

- AFM Model Test PaperDocument16 pagesAFM Model Test PaperNeelu AhluwaliaNo ratings yet

- Double EntryDocument6 pagesDouble EntryViknesvaran PillaiNo ratings yet

- Accounting Principles: (Cheat Sheet)Document4 pagesAccounting Principles: (Cheat Sheet)Bony ThomasNo ratings yet

- MCQ AccountungDocument30 pagesMCQ AccountungNilimonBanerjeeNo ratings yet

- Financial AccountingDocument8 pagesFinancial AccountingKeshav AgarwalNo ratings yet

- Answer 210Document6 pagesAnswer 210Hazel F.No ratings yet

- Aulab Case 8Document6 pagesAulab Case 8sulthanhakimNo ratings yet

- Chapter 3 HW SolutionsDocument41 pagesChapter 3 HW SolutionsemailericNo ratings yet

- EXAM1 Jfor WebDocument16 pagesEXAM1 Jfor WebtimothyandrewssNo ratings yet

- Balance Sheet ExplanationDocument11 pagesBalance Sheet Explanationdario.ramirezNo ratings yet

- Accounting For Decision Making: Unit-Iii Accounting Principles & ConventionsDocument24 pagesAccounting For Decision Making: Unit-Iii Accounting Principles & ConventionsVishal ChandakNo ratings yet

- Basic Structure of Accounting 1: Chapter OneDocument15 pagesBasic Structure of Accounting 1: Chapter OneSeid KassawNo ratings yet

- Audit Risk 1Document2 pagesAudit Risk 1Sanjay PradhanNo ratings yet

- 4 Accounting PrinciplesDocument3 pages4 Accounting Principlesapi-299265916No ratings yet

- What Is A Balance Sheet AuditDocument6 pagesWhat Is A Balance Sheet AuditSOMOSCONo ratings yet

- Bva 3Document7 pagesBva 3najaneNo ratings yet

- 5 6172302118171443575 PDFDocument6 pages5 6172302118171443575 PDFPavan RaiNo ratings yet

- A Well-Balanced Equation: Andrew HarringtonDocument2 pagesA Well-Balanced Equation: Andrew HarringtonLegogie Moses Anoghena100% (1)

- Test Bank For Financial and Managerial Accounting For Mbas 4th Edition EastonDocument36 pagesTest Bank For Financial and Managerial Accounting For Mbas 4th Edition Eastonuprightteel.rpe20h100% (51)

- Fixed Asset: Fixed Assets, Also Known As A Non-Current Asset or As Property, Plant, and Equipment (PP&E), Is ADocument7 pagesFixed Asset: Fixed Assets, Also Known As A Non-Current Asset or As Property, Plant, and Equipment (PP&E), Is ARandal SchroederNo ratings yet

- Acct Principles and Assumption - Week1Document10 pagesAcct Principles and Assumption - Week1Linh KhánhNo ratings yet

- Chapter 2 Accounting Concepts and Principles PDFDocument12 pagesChapter 2 Accounting Concepts and Principles PDFAnonymous F9lLWExNNo ratings yet

- Sample of Asset-Office Land, Equiptment, Cash, MachinesDocument29 pagesSample of Asset-Office Land, Equiptment, Cash, MachinesMaria Cludet NayveNo ratings yet

- Chapter 8Document44 pagesChapter 8Rifki OksantikaNo ratings yet

- Introduction To Balance SheetDocument10 pagesIntroduction To Balance SheetJodie Ann PajacNo ratings yet

- The Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveFrom EverandThe Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveNo ratings yet

- Balance Sheet Management: Squeezing Extra Profits and Cash from Your BusinessFrom EverandBalance Sheet Management: Squeezing Extra Profits and Cash from Your BusinessNo ratings yet

- Icmi,+4.+selvi 1 (+tahun2022) +-+Document11 pagesIcmi,+4.+selvi 1 (+tahun2022) +-+gmsstaffoperationsNo ratings yet

- Exam Calendar2020Document8 pagesExam Calendar2020gmsstaffoperationsNo ratings yet

- Ecb 3aaae739e5.fsrbox201905 09Document4 pagesEcb 3aaae739e5.fsrbox201905 09gmsstaffoperationsNo ratings yet

- Fulltext01 11Document29 pagesFulltext01 11gmsstaffoperationsNo ratings yet

- Travel Guide Kyoto enDocument8 pagesTravel Guide Kyoto engmsstaffoperationsNo ratings yet

- Project: Integration ManagementDocument71 pagesProject: Integration ManagementMustefa MohammedNo ratings yet

- 231 Everyday Vocabulary Going Shopping TestDocument6 pages231 Everyday Vocabulary Going Shopping TestHouda HiroufNo ratings yet

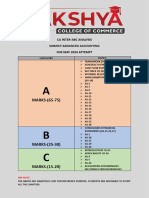

- Abc Analysis-Adv Accounts May 2024Document1 pageAbc Analysis-Adv Accounts May 2024Looney ApacheNo ratings yet

- Ayu Nurfitriadi-4111711020Document1,375 pagesAyu Nurfitriadi-4111711020Ayu NurfitriadiNo ratings yet

- Sabon NG KalantogDocument2 pagesSabon NG Kalantogjanice ocolNo ratings yet

- TDA Delivery Lead Job Description V1.0Document3 pagesTDA Delivery Lead Job Description V1.0Boobalan SuppiahNo ratings yet

- RA 9485 Anti Red Tape Act of 2007Document3 pagesRA 9485 Anti Red Tape Act of 2007lejigeNo ratings yet

- Liquidation 1Document28 pagesLiquidation 1Noemi T. LiberatoNo ratings yet

- Managerial Economics 8th Edition Samuelson Solutions Manual 1Document36 pagesManagerial Economics 8th Edition Samuelson Solutions Manual 1terrencejonesrseywdxbcf100% (30)

- JRC Assessment Framework Final v2Document26 pagesJRC Assessment Framework Final v2Jerome PercepiedNo ratings yet

- Chapter 6 - ProblemsDocument6 pagesChapter 6 - ProblemsDeanna GicaleNo ratings yet

- Lean Basics: Training ScriptDocument18 pagesLean Basics: Training ScriptmagudeeshNo ratings yet

- SBR-INT S24-J25 Syllabus and Study Guide - FinalDocument17 pagesSBR-INT S24-J25 Syllabus and Study Guide - FinalMyo NaingNo ratings yet

- How To Humanize Your AI ContentDocument12 pagesHow To Humanize Your AI ContentUmm AbdullahNo ratings yet

- Img 20150623 0002Document1 pageImg 20150623 0002Hein MaungNo ratings yet

- Zara Business Canvas ModelDocument3 pagesZara Business Canvas Modelkoko.keeganNo ratings yet

- Problem 10.2 Siam CementDocument17 pagesProblem 10.2 Siam CementRimpy SondhNo ratings yet

- Service Process RedesignDocument9 pagesService Process RedesignUnsolved MistryNo ratings yet

- Bata Store Manager JD 2019Document2 pagesBata Store Manager JD 2019asgari sheikhNo ratings yet

- Digital Communications & Customer EngagementDocument9 pagesDigital Communications & Customer EngagementAlexander Frahm-FetherstonNo ratings yet

- Elearning-Chapter 3-Carriage of Goods in Container - RVDocument77 pagesElearning-Chapter 3-Carriage of Goods in Container - RVDương Thị Kim HiềnNo ratings yet

- Publisher Version (Open Access)Document67 pagesPublisher Version (Open Access)spiconsultantdaNo ratings yet

- Stock in Transit (GR - IR Regrouping - Reclassification) - SAP BlogsDocument7 pagesStock in Transit (GR - IR Regrouping - Reclassification) - SAP BlogsusamaNo ratings yet

- W. W. Grainger: Maintenance, Repair and Operations (MRO) ProductsDocument33 pagesW. W. Grainger: Maintenance, Repair and Operations (MRO) ProductsHitisha agrawalNo ratings yet

- E-Commerce Presentation Plan - CreativeDocument15 pagesE-Commerce Presentation Plan - CreativeMUKUL DOBHALNo ratings yet

- MNC & TNCDocument1 pageMNC & TNCumang24100% (1)

- BlackRock 2020-2021 Investments Job DescriptionDocument13 pagesBlackRock 2020-2021 Investments Job DescriptionNora PetruțaNo ratings yet

- Loan Application Form Please Complete in BLOCK LETTERS.: Office UseDocument4 pagesLoan Application Form Please Complete in BLOCK LETTERS.: Office UseKennedy SimumbaNo ratings yet

- Consumer Perception Towards LIC in Rewa CityDocument64 pagesConsumer Perception Towards LIC in Rewa CityAbhay JainNo ratings yet

- Recycling Business Plan ExampleDocument49 pagesRecycling Business Plan ExampleJoseph QuillNo ratings yet