Download as pdf or txt

You might also like

- Financial Modeling Handbook 3rd EditionDocument93 pagesFinancial Modeling Handbook 3rd EditionMaunik ParikhNo ratings yet

- L1 - JN - Economics 2024 V1Document55 pagesL1 - JN - Economics 2024 V1Rohan ShekarNo ratings yet

- L1 - JN - Derivatives 2024 V1Document27 pagesL1 - JN - Derivatives 2024 V1Rohan ShekarNo ratings yet

- Balance Sheet of AMULDocument7 pagesBalance Sheet of AMULPriyanka Kotian59% (66)

- 14 - Net Profit Example 1Document2 pages14 - Net Profit Example 1balajiNo ratings yet

- Indigo Income STMT 1Document1 pageIndigo Income STMT 1deepzNo ratings yet

- 17 - Net Cash Accrual ExampleDocument3 pages17 - Net Cash Accrual ExamplebalajiNo ratings yet

- Impce Bs m23 For SignDocument15 pagesImpce Bs m23 For SignauditNo ratings yet

- Investor Presentation May 20 2022Document19 pagesInvestor Presentation May 20 2022Shwetta BajpaiNo ratings yet

- Consolidated Profit LossDocument1 pageConsolidated Profit LossPooja SoniNo ratings yet

- FinalDocument20 pagesFinalMuhammad Aminul HoqueNo ratings yet

- Statement of Profit and Loss For The Year Ended 31 March 2020Document1 pageStatement of Profit and Loss For The Year Ended 31 March 2020Prathi KarthikNo ratings yet

- Profit and LossDocument1 pageProfit and LossYagika Jagnani100% (1)

- BFS Standalone P&L2022Document1 pageBFS Standalone P&L2022manoj mahantaNo ratings yet

- Asian Paints ProjectDocument3 pagesAsian Paints ProjectRahul SinghNo ratings yet

- UntitledDocument357 pagesUntitledAlexNo ratings yet

- AFM Project Sec J Group 10Document32 pagesAFM Project Sec J Group 10J40Santhosh KrishnaNo ratings yet

- Axis Bank AR 2021-22 - Consolidated Financial StatementsDocument50 pagesAxis Bank AR 2021-22 - Consolidated Financial StatementsPooja SoniNo ratings yet

- Board'S Report: Summarised Financial ResultsDocument15 pagesBoard'S Report: Summarised Financial Resultsirisha guptaNo ratings yet

- RadheDocument8 pagesRadheMohitNo ratings yet

- Directors Report FY20Document49 pagesDirectors Report FY20Rajeshwari ShuklaNo ratings yet

- Audited Consolidated-Statements - PAL 2022Document10 pagesAudited Consolidated-Statements - PAL 2022P patelNo ratings yet

- Consolidated Balance Sheet (Contd.)Document40 pagesConsolidated Balance Sheet (Contd.)Sehajpal SanghuNo ratings yet

- Financial-Statements (1) - Pages-1-2,4Document3 pagesFinancial-Statements (1) - Pages-1-2,4Harshita KalwaniNo ratings yet

- Asian Paints 2021-2022Document2 pagesAsian Paints 2021-2022aguptakochi314No ratings yet

- Statement of Profit and Loss: Particulars Notes For The Year Ending On 31st March 2020Document11 pagesStatement of Profit and Loss: Particulars Notes For The Year Ending On 31st March 2020dineshkumar1234No ratings yet

- InfoEdge Annual Report 2023 1Document1 pageInfoEdge Annual Report 2023 1Aditya RoyNo ratings yet

- Mint Delhi 21-10-2022Document20 pagesMint Delhi 21-10-2022sushilpal161No ratings yet

- 200 500 Imo Result 20230215Document30 pages200 500 Imo Result 20230215Contra Value BetsNo ratings yet

- Britannia ExcelDocument7 pagesBritannia ExcelParth MalikNo ratings yet

- Choo Bee Metal Industries Berhad (10587-A)Document18 pagesChoo Bee Metal Industries Berhad (10587-A)Iqbal YusufNo ratings yet

- Good Hope PLC: Annual ReportDocument11 pagesGood Hope PLC: Annual ReporthvalolaNo ratings yet

- Pursuant To Regulation 33 of The SEBI (Listing Obligations and Disclosure Requirements)Document19 pagesPursuant To Regulation 33 of The SEBI (Listing Obligations and Disclosure Requirements)pvs12684No ratings yet

- Beneish M ScoreDocument45 pagesBeneish M ScoreAnshu RaiNo ratings yet

- Axis Bank - AR21 - DRDocument17 pagesAxis Bank - AR21 - DRRakeshNo ratings yet

- Incredible EngineeringDocument4 pagesIncredible EngineeringAnirudha SharmaNo ratings yet

- Notes To Consolidated Financial Statements: Note 36: Segment Information For The Year Ended 31 March, 2016Document2 pagesNotes To Consolidated Financial Statements: Note 36: Segment Information For The Year Ended 31 March, 2016Gaurang GroverNo ratings yet

- Statement of Profit and LossDocument1 pageStatement of Profit and LossAjit singhNo ratings yet

- Bata India Limited: Statement of Profit and Loss For The Fifteen Month Period Ended 31St March, 2015Document1 pageBata India Limited: Statement of Profit and Loss For The Fifteen Month Period Ended 31St March, 2015Viswateja KrottapalliNo ratings yet

- GK Audited Financial 31-Dec-2010Document97 pagesGK Audited Financial 31-Dec-2010Dante GillespieNo ratings yet

- ITC-Profit-Loss 2017 PDFDocument1 pageITC-Profit-Loss 2017 PDFShristi GutgutiaNo ratings yet

- Profit / Loss Staement of Asian PaintsDocument3 pagesProfit / Loss Staement of Asian PaintsShivangi Gupta Student, Jaipuria LucknowNo ratings yet

- Assignment-2 FA PDFDocument3 pagesAssignment-2 FA PDFrajNo ratings yet

- ACAPL - Outcome of BM - Finnancials - Asset Cover CertificateDocument23 pagesACAPL - Outcome of BM - Finnancials - Asset Cover CertificateShashi Bhushan PrinceNo ratings yet

- EV Annual Report 2021 22Document69 pagesEV Annual Report 2021 22deepakturi2002No ratings yet

- 234invuf AnnualReport2021-22Document169 pages234invuf AnnualReport2021-22Pathan IkhlaqueNo ratings yet

- Statement of Profit and Loss For The Year Ended 31St March 2017Document1 pageStatement of Profit and Loss For The Year Ended 31St March 2017Himanshu DuttaNo ratings yet

- a237f07e-0946-42cc-93d1-998fc61372d7Document20 pagesa237f07e-0946-42cc-93d1-998fc61372d7sonu.k.gupta9No ratings yet

- Financial Results EWM 1Q 2024Document18 pagesFinancial Results EWM 1Q 2024Najib SaadNo ratings yet

- Financial White Lotus Motors PVT - LTD - For The FY 2078-79Document117 pagesFinancial White Lotus Motors PVT - LTD - For The FY 2078-79Roshan PoudelNo ratings yet

- AnnexureDocument1 pageAnnexureAdv Anand JhaNo ratings yet

- CHAPTER 5 - RPRC NewDocument60 pagesCHAPTER 5 - RPRC NewCMHNo ratings yet

- NTPC - Annual Report - 20-21-423-431Document9 pagesNTPC - Annual Report - 20-21-423-431devrishabhNo ratings yet

- Directors Report (Interim 2)Document14 pagesDirectors Report (Interim 2)DILIP KUMARNo ratings yet

- AFM Project Report FinalDocument19 pagesAFM Project Report FinalRitu KumariNo ratings yet

- Bajaj Auto International Holdings B.V.: Balance SheetDocument22 pagesBajaj Auto International Holdings B.V.: Balance SheetPhani TejaNo ratings yet

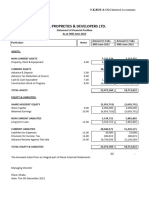

- RTCL Properties & Developers LIMITED-2022Document15 pagesRTCL Properties & Developers LIMITED-2022Asad RanaNo ratings yet

- HomeDepot F22 SolutionDocument4 pagesHomeDepot F22 SolutionFalguni ShomeNo ratings yet

- Annual Report 2019 3Document77 pagesAnnual Report 2019 3andreileonard.asigurariNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Annual Report 2022 23Document77 pagesAnnual Report 2022 23Rohan ShekarNo ratings yet

- 03regression ClassDocument2 pages03regression ClassRohan ShekarNo ratings yet

- Session03 - Common Size BS - IS - CFS WorksheetDocument8 pagesSession03 - Common Size BS - IS - CFS WorksheetRohan ShekarNo ratings yet

- Fa ClassDocument2 pagesFa ClassRohan ShekarNo ratings yet

- Session 12.06.2024 ClassDocument9 pagesSession 12.06.2024 ClassRohan ShekarNo ratings yet

- Afm Concept Diary 2023Document6 pagesAfm Concept Diary 2023Rohan ShekarNo ratings yet

- Business Cycles and UnemploymentDocument60 pagesBusiness Cycles and UnemploymentRohan ShekarNo ratings yet

- Fixed Income-IDocument110 pagesFixed Income-IRohan ShekarNo ratings yet

- CorpFin 2Document76 pagesCorpFin 2Rohan ShekarNo ratings yet

- CorpFin 1Document125 pagesCorpFin 1Rohan ShekarNo ratings yet

- Equity 2Document122 pagesEquity 2Rohan ShekarNo ratings yet

- Equity 1Document126 pagesEquity 1Rohan ShekarNo ratings yet

- Proposal InternshipDocument2 pagesProposal InternshipRohan ShekarNo ratings yet

- CH 9 SummaryDocument1 pageCH 9 SummaryRohan ShekarNo ratings yet

- L1 - JN - Ethical and Professional Standards 2024 V1Document44 pagesL1 - JN - Ethical and Professional Standards 2024 V1Rohan Shekar0% (1)

- Topics Related To Tata Steel IBMDDocument4 pagesTopics Related To Tata Steel IBMDRohan ShekarNo ratings yet

- ISM 4 To 7 PPTDocument44 pagesISM 4 To 7 PPTRohan ShekarNo ratings yet

- Ism 1 2 3 PPT 2024Document45 pagesIsm 1 2 3 PPT 2024Rohan ShekarNo ratings yet

- QUIZDocument3 pagesQUIZIris FenelleNo ratings yet

- e-StatementBRImo 479601031479508 Aug2023 20240206 095000-2Document6 pagese-StatementBRImo 479601031479508 Aug2023 20240206 095000-2lesehan selerakuNo ratings yet

- Thesis of ManagementDocument12 pagesThesis of Managementsangamsapkota0007No ratings yet

- Corporate Finance PPT 1Document58 pagesCorporate Finance PPT 1Major SehrawatNo ratings yet

- Mudarabah and Its Application in Islamic BankingDocument26 pagesMudarabah and Its Application in Islamic Bankingsaif khanNo ratings yet

- ABC Discussion - Business CombinationDocument7 pagesABC Discussion - Business CombinationJohn Cesar PaunatNo ratings yet

- CASE STUDY INSTRUCTIONS 2019 T5 NewDocument10 pagesCASE STUDY INSTRUCTIONS 2019 T5 NewSunil SharmaNo ratings yet

- Consolidated Financial StatementsDocument29 pagesConsolidated Financial StatementsPramad BhattacharjeeNo ratings yet

- Dabur IndiaDocument336 pagesDabur IndiakjNo ratings yet

- CR - MA-2023 - Suggested - AnswersDocument15 pagesCR - MA-2023 - Suggested - AnswersfahadsarkerNo ratings yet

- GDV: TDC:: Per PeriodDocument9 pagesGDV: TDC:: Per PeriodM. HfizzNo ratings yet

- M6-CGBLE (Updated Syllabus)Document2 pagesM6-CGBLE (Updated Syllabus)Amna Bi biNo ratings yet

- TaxationDocument8 pagesTaxationArlyn VicenteNo ratings yet

- FM DC Lecture 5 Capital Budgeting PDFDocument7 pagesFM DC Lecture 5 Capital Budgeting PDFRitesh KumarNo ratings yet

- DG Khan Cement Financial StatementsDocument8 pagesDG Khan Cement Financial StatementsAsad BumbiaNo ratings yet

- Financial Accounting 9Th Edition Libby Test Bank Full Chapter PDFDocument36 pagesFinancial Accounting 9Th Edition Libby Test Bank Full Chapter PDFnancy.lee736100% (11)

- (SEC. 17-37) BUS LAW - For April 17, 2023 RECITATIONDocument32 pages(SEC. 17-37) BUS LAW - For April 17, 2023 RECITATIONEleina BernardoNo ratings yet

- CID 20231122201002378796 777900 CIDROC IpayccDocument6 pagesCID 20231122201002378796 777900 CIDROC Ipayccnvm creativeNo ratings yet

- Suggested Answer CAP II (Dec 2018) All Subjects PDFDocument123 pagesSuggested Answer CAP II (Dec 2018) All Subjects PDFDipendra kumar MehtaNo ratings yet

- Avenue Supermarts-Investment ThesisDocument1 pageAvenue Supermarts-Investment Thesisnageswar.pattipatiNo ratings yet

- DownloadDocument3 pagesDownloadChristina SalliNo ratings yet

- Mutual Fund SWP Calculator Plan 1Document8 pagesMutual Fund SWP Calculator Plan 1Yada GiriNo ratings yet

- 3.0 Final Project - InternationalCorporateTax - EditedDocument17 pages3.0 Final Project - InternationalCorporateTax - Editedkevin kipkemoiNo ratings yet

- Kering Case QuestionsDocument24 pagesKering Case Questionsadelaida.cerveraestebanNo ratings yet

- Revision Test 2 Accountancy XiiDocument2 pagesRevision Test 2 Accountancy Xiisakshamagnihotri0No ratings yet

- Bank StatementDocument2 pagesBank Statementrosmainy0% (1)

- Accounting For Special TransactionsDocument1 pageAccounting For Special TransactionsKc SevillaNo ratings yet

- InventoryDocument36 pagesInventorydhruvbhartiya2420No ratings yet

- Current and Deferred Tax Slides Tax Training 27.02.2020Document55 pagesCurrent and Deferred Tax Slides Tax Training 27.02.2020Amal P TomyNo ratings yet