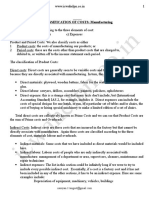

Cost Sheet

Cost Sheet

You might also like

- Research MethodologyDocument46 pagesResearch Methodologyنور شهبره فانوت100% (6)

- Engineering Economy 3Document37 pagesEngineering Economy 3Steven SengNo ratings yet

- 74749bos60489 cp6Document34 pages74749bos60489 cp6tempNo ratings yet

- Cost SheetDocument19 pagesCost SheetpraphullmadaneNo ratings yet

- COST ACCOUNTING I Module VDocument4 pagesCOST ACCOUNTING I Module VEmil E. ANo ratings yet

- Cost Sheet: Learning OutcomesDocument26 pagesCost Sheet: Learning OutcomesSusovan SirNo ratings yet

- Cost SheetDocument26 pagesCost SheetPankaj SahaniNo ratings yet

- Cost SheetDocument5 pagesCost Sheetgaurav gauravNo ratings yet

- Cost Sheet: Learning OutcomesDocument15 pagesCost Sheet: Learning OutcomesshubNo ratings yet

- Cost Sheet SummaryDocument8 pagesCost Sheet SummaryBahi Khata CommerceNo ratings yet

- CHP 6. Cost Sheet - CapranavDocument14 pagesCHP 6. Cost Sheet - CapranavMonikaNo ratings yet

- Course Title: Cost Accounting Course Code:441 BBA Program Lecture-2Document14 pagesCourse Title: Cost Accounting Course Code:441 BBA Program Lecture-2Tanvir Ahmed ChowdhuryNo ratings yet

- RR Cost SheetDocument4 pagesRR Cost SheetRamiz SiddiquiNo ratings yet

- Dr. (CA) Ankita Jain: Unit - IiiDocument11 pagesDr. (CA) Ankita Jain: Unit - IiiBHAVYA SHARMANo ratings yet

- Costs - Concepts and ClassificationsDocument5 pagesCosts - Concepts and ClassificationsCarlo B CagampangNo ratings yet

- 103 Sample Chapter PDFDocument28 pages103 Sample Chapter PDFKomal MusaleNo ratings yet

- 103 Sample ChapterDocument28 pages103 Sample ChapterRithik VisuNo ratings yet

- 110-W2-3-Cost concept-chp02-STDocument85 pages110-W2-3-Cost concept-chp02-STmargaret mariaNo ratings yet

- COST Lesson 2Document4 pagesCOST Lesson 2Christian Clyde Zacal Ching0% (1)

- 1 Introduction To Cost Accounting (2017)Document62 pages1 Introduction To Cost Accounting (2017)kilogek124No ratings yet

- Session 3 - MAC - ConceptsDocument18 pagesSession 3 - MAC - ConceptsABHASH JHANo ratings yet

- Cost ClassificationDocument6 pagesCost ClassificationAnonymous yy8In96j0r100% (1)

- Cost Accounting With More Illustrations-2Document21 pagesCost Accounting With More Illustrations-2Rohit KashyapNo ratings yet

- Classification of CostsDocument84 pagesClassification of CostsRoyal ProjectsNo ratings yet

- Cost Classification Theory and Practice QuestionsDocument9 pagesCost Classification Theory and Practice QuestionsBilal Rauf100% (1)

- Manufacturing AccountsDocument10 pagesManufacturing Accountsamosoundo59No ratings yet

- Cost 1 CH-twoDocument10 pagesCost 1 CH-twoDebela AbidhuNo ratings yet

- Cost ManagementDocument23 pagesCost ManagementEswara ReddyNo ratings yet

- Overheads - Absorption Costing Method: Learning OutcomesDocument89 pagesOverheads - Absorption Costing Method: Learning Outcomessamyak bafnaNo ratings yet

- Cost Sheet P&SDocument41 pagesCost Sheet P&SJishnuPatilNo ratings yet

- Full Download Managerial Accounting Creating Value in A Dynamic Business Environment Hilton 10th Edition Solutions Manual PDF Full ChapterDocument36 pagesFull Download Managerial Accounting Creating Value in A Dynamic Business Environment Hilton 10th Edition Solutions Manual PDF Full Chapterdrearingpuncheonrpeal100% (21)

- Costing Formulae Topic WiseDocument81 pagesCosting Formulae Topic WiseSuresh SharmaNo ratings yet

- Accounting 2Document5 pagesAccounting 2jessicaong2403No ratings yet

- Notes in Strategic Cost Management (SLPO)Document7 pagesNotes in Strategic Cost Management (SLPO)Laila OlpindoNo ratings yet

- Chapter 12 Cost Sheet or Statement of CostDocument16 pagesChapter 12 Cost Sheet or Statement of CostNeelesh MishraNo ratings yet

- Basic Cost Term and Concepts - An Inrodution 13.12.22Document36 pagesBasic Cost Term and Concepts - An Inrodution 13.12.22JayaNo ratings yet

- Basic Cost Management ConceptsDocument7 pagesBasic Cost Management ConceptsImadNo ratings yet

- Managerial Accounting and Cost Concepts: Solutions To QuestionsDocument13 pagesManagerial Accounting and Cost Concepts: Solutions To QuestionsGera MatsNo ratings yet

- A.3. Cost ClassificationsDocument57 pagesA.3. Cost ClassificationsTiyas KurniaNo ratings yet

- Chapter TwoDocument33 pagesChapter TwoTerefe DubeNo ratings yet

- Cost and Management Accounting and Quandative TechniqueDocument86 pagesCost and Management Accounting and Quandative TechniquesaiyuvatechNo ratings yet

- Managerial Accounting Creating Value in A Dynamic Business Environment Hilton 10th Edition Solutions ManualDocument11 pagesManagerial Accounting Creating Value in A Dynamic Business Environment Hilton 10th Edition Solutions Manualbarrenlywale1ibn8No ratings yet

- Costing Formulae Topic WiseDocument83 pagesCosting Formulae Topic WiseViswanathan SrkNo ratings yet

- CostingDocument10 pagesCostingd.pagkatoytoyNo ratings yet

- Manufacturing Account-Ref - Material: SyllabusDocument5 pagesManufacturing Account-Ref - Material: SyllabusMohamed MuizNo ratings yet

- Manufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesFrom EverandManufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesRating: 4.5 out of 5 stars4.5/5 (3)

- Creating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowFrom EverandCreating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowRating: 4 out of 5 stars4/5 (1)

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Practical Guide To Production Planning & Control [Revised Edition]From EverandPractical Guide To Production Planning & Control [Revised Edition]Rating: 1 out of 5 stars1/5 (1)

- Lean-based Production Management: Practical Lean ManufacturingFrom EverandLean-based Production Management: Practical Lean ManufacturingNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Kanban the Toyota Way: An Inventory Buffering System to Eliminate InventoryFrom EverandKanban the Toyota Way: An Inventory Buffering System to Eliminate InventoryRating: 5 out of 5 stars5/5 (1)

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Total Plant Performance Management:: A Profit-Building Plan to Promote, Implement, and Maintain Optimum Performance Throughout Your PlantFrom EverandTotal Plant Performance Management:: A Profit-Building Plan to Promote, Implement, and Maintain Optimum Performance Throughout Your PlantNo ratings yet

- Identifying Mura-Muri-Muda in the Manufacturing Stream: Toyota Production System ConceptsFrom EverandIdentifying Mura-Muri-Muda in the Manufacturing Stream: Toyota Production System ConceptsRating: 5 out of 5 stars5/5 (1)

- Integrated Design and Construction - Single Responsibility: A Code of PracticeFrom EverandIntegrated Design and Construction - Single Responsibility: A Code of PracticeNo ratings yet

- Chapter 1 - Introduction - IE 112Document12 pagesChapter 1 - Introduction - IE 112leojhunNo ratings yet

- (Economy) Liquidity Adjustment Facility (LAF), Marginal Standing Facility (MSF), Repo, Reverse Repo, SLR, CRR, NEFT, RTGS, NDTL: Meaning ExplainedDocument14 pages(Economy) Liquidity Adjustment Facility (LAF), Marginal Standing Facility (MSF), Repo, Reverse Repo, SLR, CRR, NEFT, RTGS, NDTL: Meaning Explainedsameer bakshiNo ratings yet

- O Uco Bank: Rnictj/Date: 19.08.2019Document3 pagesO Uco Bank: Rnictj/Date: 19.08.2019Satya KarNo ratings yet

- Chapter 4 MC QuestionsDocument5 pagesChapter 4 MC QuestionsjessicaNo ratings yet

- B&K Wealth Management Introduction & CapabilitiesDocument18 pagesB&K Wealth Management Introduction & Capabilitiesiifl dataNo ratings yet

- Cornerstone Exercises Cornerstone Exercise 17.1Document30 pagesCornerstone Exercises Cornerstone Exercise 17.1Nirwana PuriNo ratings yet

- Admas University School of Postgraduate Studies MBA Financial Management AssignmentDocument17 pagesAdmas University School of Postgraduate Studies MBA Financial Management AssignmentAbnet BeleteNo ratings yet

- Chapter 06 Test Bank - Static - Version1Document26 pagesChapter 06 Test Bank - Static - Version1Veronica MargotNo ratings yet

- Accelerating Capital Markets Development in Emerging EconomiesDocument26 pagesAccelerating Capital Markets Development in Emerging EconomiesIchbin BinNo ratings yet

- EconDocument4 pagesEconKianna SabalaNo ratings yet

- STR Op BB OkDocument18 pagesSTR Op BB OkriddhmarketingNo ratings yet

- Case Study On Executive CompensationDocument2 pagesCase Study On Executive CompensationanathomsanNo ratings yet

- MBA 530 GROW ModelDocument5 pagesMBA 530 GROW ModelSchool Purposes OnlyNo ratings yet

- Flat No. 2 Iesco BillDocument1 pageFlat No. 2 Iesco BillGamers CrewNo ratings yet

- Ch6.Strategy in Global EnvironmentDocument17 pagesCh6.Strategy in Global EnvironmentDian MaulanaNo ratings yet

- Tata Steel 2015 16 PDFDocument300 pagesTata Steel 2015 16 PDFAman PrasasdNo ratings yet

- BÀI TẬP TÀI CHÍNH QUỐC TẾDocument2 pagesBÀI TẬP TÀI CHÍNH QUỐC TẾXuan KimNo ratings yet

- TAPMI Placement Brochure 2010-11Document48 pagesTAPMI Placement Brochure 2010-11tapmiblogsNo ratings yet

- MastekDocument27 pagesMastekcsheth3650No ratings yet

- HO Inventory-EstimationDocument1 pageHO Inventory-EstimationAl Francis GuillermoNo ratings yet

- NABARD ESI Summary SheetsDocument692 pagesNABARD ESI Summary SheetsGoutham RajasekaranNo ratings yet

- Amendment in Itb and GCC: Amend - ITBGCC 1Document2 pagesAmendment in Itb and GCC: Amend - ITBGCC 1Mayank SharmaNo ratings yet

- A Framework of Sustainable Supply Chain Management - Moving Toward New TheoryDocument78 pagesA Framework of Sustainable Supply Chain Management - Moving Toward New TheoryjulienfolquetNo ratings yet

- 2) Instructions For Playing The GameDocument7 pages2) Instructions For Playing The GameAna MariaNo ratings yet

- Lego StudentDocument7 pagesLego StudentPookguy100% (1)

- Struktur Organisasi: Organization StructureDocument2 pagesStruktur Organisasi: Organization StructureRalila SejahteraNo ratings yet

- Social Structure TheoryDocument16 pagesSocial Structure TheorySalman AtherNo ratings yet

- Lecture 36Document14 pagesLecture 36praneix100% (1)

![Practical Guide To Production Planning & Control [Revised Edition]](https://imgv2-1-f.scribdassets.com/img/word_document/235162742/149x198/2a816df8c8/1709920378?v=1)

Download as pdf or txt

You might also like

- Research MethodologyDocument46 pagesResearch Methodologyنور شهبره فانوت100% (6)

- Engineering Economy 3Document37 pagesEngineering Economy 3Steven SengNo ratings yet

- 74749bos60489 cp6Document34 pages74749bos60489 cp6tempNo ratings yet

- Cost SheetDocument19 pagesCost SheetpraphullmadaneNo ratings yet

- COST ACCOUNTING I Module VDocument4 pagesCOST ACCOUNTING I Module VEmil E. ANo ratings yet

- Cost Sheet: Learning OutcomesDocument26 pagesCost Sheet: Learning OutcomesSusovan SirNo ratings yet

- Cost SheetDocument26 pagesCost SheetPankaj SahaniNo ratings yet

- Cost SheetDocument5 pagesCost Sheetgaurav gauravNo ratings yet

- Cost Sheet: Learning OutcomesDocument15 pagesCost Sheet: Learning OutcomesshubNo ratings yet

- Cost Sheet SummaryDocument8 pagesCost Sheet SummaryBahi Khata CommerceNo ratings yet

- CHP 6. Cost Sheet - CapranavDocument14 pagesCHP 6. Cost Sheet - CapranavMonikaNo ratings yet

- Course Title: Cost Accounting Course Code:441 BBA Program Lecture-2Document14 pagesCourse Title: Cost Accounting Course Code:441 BBA Program Lecture-2Tanvir Ahmed ChowdhuryNo ratings yet

- RR Cost SheetDocument4 pagesRR Cost SheetRamiz SiddiquiNo ratings yet

- Dr. (CA) Ankita Jain: Unit - IiiDocument11 pagesDr. (CA) Ankita Jain: Unit - IiiBHAVYA SHARMANo ratings yet

- Costs - Concepts and ClassificationsDocument5 pagesCosts - Concepts and ClassificationsCarlo B CagampangNo ratings yet

- 103 Sample Chapter PDFDocument28 pages103 Sample Chapter PDFKomal MusaleNo ratings yet

- 103 Sample ChapterDocument28 pages103 Sample ChapterRithik VisuNo ratings yet

- 110-W2-3-Cost concept-chp02-STDocument85 pages110-W2-3-Cost concept-chp02-STmargaret mariaNo ratings yet

- COST Lesson 2Document4 pagesCOST Lesson 2Christian Clyde Zacal Ching0% (1)

- 1 Introduction To Cost Accounting (2017)Document62 pages1 Introduction To Cost Accounting (2017)kilogek124No ratings yet

- Session 3 - MAC - ConceptsDocument18 pagesSession 3 - MAC - ConceptsABHASH JHANo ratings yet

- Cost ClassificationDocument6 pagesCost ClassificationAnonymous yy8In96j0r100% (1)

- Cost Accounting With More Illustrations-2Document21 pagesCost Accounting With More Illustrations-2Rohit KashyapNo ratings yet

- Classification of CostsDocument84 pagesClassification of CostsRoyal ProjectsNo ratings yet

- Cost Classification Theory and Practice QuestionsDocument9 pagesCost Classification Theory and Practice QuestionsBilal Rauf100% (1)

- Manufacturing AccountsDocument10 pagesManufacturing Accountsamosoundo59No ratings yet

- Cost 1 CH-twoDocument10 pagesCost 1 CH-twoDebela AbidhuNo ratings yet

- Cost ManagementDocument23 pagesCost ManagementEswara ReddyNo ratings yet

- Overheads - Absorption Costing Method: Learning OutcomesDocument89 pagesOverheads - Absorption Costing Method: Learning Outcomessamyak bafnaNo ratings yet

- Cost Sheet P&SDocument41 pagesCost Sheet P&SJishnuPatilNo ratings yet

- Full Download Managerial Accounting Creating Value in A Dynamic Business Environment Hilton 10th Edition Solutions Manual PDF Full ChapterDocument36 pagesFull Download Managerial Accounting Creating Value in A Dynamic Business Environment Hilton 10th Edition Solutions Manual PDF Full Chapterdrearingpuncheonrpeal100% (21)

- Costing Formulae Topic WiseDocument81 pagesCosting Formulae Topic WiseSuresh SharmaNo ratings yet

- Accounting 2Document5 pagesAccounting 2jessicaong2403No ratings yet

- Notes in Strategic Cost Management (SLPO)Document7 pagesNotes in Strategic Cost Management (SLPO)Laila OlpindoNo ratings yet

- Chapter 12 Cost Sheet or Statement of CostDocument16 pagesChapter 12 Cost Sheet or Statement of CostNeelesh MishraNo ratings yet

- Basic Cost Term and Concepts - An Inrodution 13.12.22Document36 pagesBasic Cost Term and Concepts - An Inrodution 13.12.22JayaNo ratings yet

- Basic Cost Management ConceptsDocument7 pagesBasic Cost Management ConceptsImadNo ratings yet

- Managerial Accounting and Cost Concepts: Solutions To QuestionsDocument13 pagesManagerial Accounting and Cost Concepts: Solutions To QuestionsGera MatsNo ratings yet

- A.3. Cost ClassificationsDocument57 pagesA.3. Cost ClassificationsTiyas KurniaNo ratings yet

- Chapter TwoDocument33 pagesChapter TwoTerefe DubeNo ratings yet

- Cost and Management Accounting and Quandative TechniqueDocument86 pagesCost and Management Accounting and Quandative TechniquesaiyuvatechNo ratings yet

- Managerial Accounting Creating Value in A Dynamic Business Environment Hilton 10th Edition Solutions ManualDocument11 pagesManagerial Accounting Creating Value in A Dynamic Business Environment Hilton 10th Edition Solutions Manualbarrenlywale1ibn8No ratings yet

- Costing Formulae Topic WiseDocument83 pagesCosting Formulae Topic WiseViswanathan SrkNo ratings yet

- CostingDocument10 pagesCostingd.pagkatoytoyNo ratings yet

- Manufacturing Account-Ref - Material: SyllabusDocument5 pagesManufacturing Account-Ref - Material: SyllabusMohamed MuizNo ratings yet

- Manufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesFrom EverandManufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesRating: 4.5 out of 5 stars4.5/5 (3)

- Creating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowFrom EverandCreating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowRating: 4 out of 5 stars4/5 (1)

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Practical Guide To Production Planning & Control [Revised Edition]From EverandPractical Guide To Production Planning & Control [Revised Edition]Rating: 1 out of 5 stars1/5 (1)

- Lean-based Production Management: Practical Lean ManufacturingFrom EverandLean-based Production Management: Practical Lean ManufacturingNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Kanban the Toyota Way: An Inventory Buffering System to Eliminate InventoryFrom EverandKanban the Toyota Way: An Inventory Buffering System to Eliminate InventoryRating: 5 out of 5 stars5/5 (1)

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Total Plant Performance Management:: A Profit-Building Plan to Promote, Implement, and Maintain Optimum Performance Throughout Your PlantFrom EverandTotal Plant Performance Management:: A Profit-Building Plan to Promote, Implement, and Maintain Optimum Performance Throughout Your PlantNo ratings yet

- Identifying Mura-Muri-Muda in the Manufacturing Stream: Toyota Production System ConceptsFrom EverandIdentifying Mura-Muri-Muda in the Manufacturing Stream: Toyota Production System ConceptsRating: 5 out of 5 stars5/5 (1)

- Integrated Design and Construction - Single Responsibility: A Code of PracticeFrom EverandIntegrated Design and Construction - Single Responsibility: A Code of PracticeNo ratings yet

- Chapter 1 - Introduction - IE 112Document12 pagesChapter 1 - Introduction - IE 112leojhunNo ratings yet

- (Economy) Liquidity Adjustment Facility (LAF), Marginal Standing Facility (MSF), Repo, Reverse Repo, SLR, CRR, NEFT, RTGS, NDTL: Meaning ExplainedDocument14 pages(Economy) Liquidity Adjustment Facility (LAF), Marginal Standing Facility (MSF), Repo, Reverse Repo, SLR, CRR, NEFT, RTGS, NDTL: Meaning Explainedsameer bakshiNo ratings yet

- O Uco Bank: Rnictj/Date: 19.08.2019Document3 pagesO Uco Bank: Rnictj/Date: 19.08.2019Satya KarNo ratings yet

- Chapter 4 MC QuestionsDocument5 pagesChapter 4 MC QuestionsjessicaNo ratings yet

- B&K Wealth Management Introduction & CapabilitiesDocument18 pagesB&K Wealth Management Introduction & Capabilitiesiifl dataNo ratings yet

- Cornerstone Exercises Cornerstone Exercise 17.1Document30 pagesCornerstone Exercises Cornerstone Exercise 17.1Nirwana PuriNo ratings yet

- Admas University School of Postgraduate Studies MBA Financial Management AssignmentDocument17 pagesAdmas University School of Postgraduate Studies MBA Financial Management AssignmentAbnet BeleteNo ratings yet

- Chapter 06 Test Bank - Static - Version1Document26 pagesChapter 06 Test Bank - Static - Version1Veronica MargotNo ratings yet

- Accelerating Capital Markets Development in Emerging EconomiesDocument26 pagesAccelerating Capital Markets Development in Emerging EconomiesIchbin BinNo ratings yet

- EconDocument4 pagesEconKianna SabalaNo ratings yet

- STR Op BB OkDocument18 pagesSTR Op BB OkriddhmarketingNo ratings yet

- Case Study On Executive CompensationDocument2 pagesCase Study On Executive CompensationanathomsanNo ratings yet

- MBA 530 GROW ModelDocument5 pagesMBA 530 GROW ModelSchool Purposes OnlyNo ratings yet

- Flat No. 2 Iesco BillDocument1 pageFlat No. 2 Iesco BillGamers CrewNo ratings yet

- Ch6.Strategy in Global EnvironmentDocument17 pagesCh6.Strategy in Global EnvironmentDian MaulanaNo ratings yet

- Tata Steel 2015 16 PDFDocument300 pagesTata Steel 2015 16 PDFAman PrasasdNo ratings yet

- BÀI TẬP TÀI CHÍNH QUỐC TẾDocument2 pagesBÀI TẬP TÀI CHÍNH QUỐC TẾXuan KimNo ratings yet

- TAPMI Placement Brochure 2010-11Document48 pagesTAPMI Placement Brochure 2010-11tapmiblogsNo ratings yet

- MastekDocument27 pagesMastekcsheth3650No ratings yet

- HO Inventory-EstimationDocument1 pageHO Inventory-EstimationAl Francis GuillermoNo ratings yet

- NABARD ESI Summary SheetsDocument692 pagesNABARD ESI Summary SheetsGoutham RajasekaranNo ratings yet

- Amendment in Itb and GCC: Amend - ITBGCC 1Document2 pagesAmendment in Itb and GCC: Amend - ITBGCC 1Mayank SharmaNo ratings yet

- A Framework of Sustainable Supply Chain Management - Moving Toward New TheoryDocument78 pagesA Framework of Sustainable Supply Chain Management - Moving Toward New TheoryjulienfolquetNo ratings yet

- 2) Instructions For Playing The GameDocument7 pages2) Instructions For Playing The GameAna MariaNo ratings yet

- Lego StudentDocument7 pagesLego StudentPookguy100% (1)

- Struktur Organisasi: Organization StructureDocument2 pagesStruktur Organisasi: Organization StructureRalila SejahteraNo ratings yet

- Social Structure TheoryDocument16 pagesSocial Structure TheorySalman AtherNo ratings yet

- Lecture 36Document14 pagesLecture 36praneix100% (1)