Download as pdf or txt

You might also like

- Hanoi Marketview Q4 2017Document7 pagesHanoi Marketview Q4 2017Lui AnsonNo ratings yet

- Kantar Worldpanel Division FMCG Monitor Full Year 2020 EN FinalDocument10 pagesKantar Worldpanel Division FMCG Monitor Full Year 2020 EN FinalvinhtamledangNo ratings yet

- Uncle CheffyDocument8 pagesUncle CheffyKaly Rie100% (1)

- India@2030 - Mohandas Pai (Final) PDFDocument52 pagesIndia@2030 - Mohandas Pai (Final) PDFSunil KumarNo ratings yet

- Affordable Housing & Housing FinanceDocument11 pagesAffordable Housing & Housing FinanceUmang PanchalNo ratings yet

- State Budget Analysis KA 2020-21 FinalDocument7 pagesState Budget Analysis KA 2020-21 Finalmohdahmed12345No ratings yet

- WTTC 23 EIR2023 - Global - Factsheet - 190423Document1 pageWTTC 23 EIR2023 - Global - Factsheet - 190423Nathalia GamboaNo ratings yet

- 2022 Asset Wealth ManagementDocument22 pages2022 Asset Wealth ManagementSankaty LightNo ratings yet

- Q4 2018Document56 pagesQ4 2018Mcke YapNo ratings yet

- State Budget Analysis 2021-22-HimachalDocument9 pagesState Budget Analysis 2021-22-HimachalHarsh Kr. SharmaNo ratings yet

- Retail Industry Retail Industry Retail IndustryDocument8 pagesRetail Industry Retail Industry Retail IndustryTanmay PokaleNo ratings yet

- Property Valuation & Tax Reform: Package 3Document14 pagesProperty Valuation & Tax Reform: Package 3April EspirituNo ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- Study Id117047 Nbfcs in IndiaDocument14 pagesStudy Id117047 Nbfcs in IndiaankitNo ratings yet

- Vietnam Market Insights - HSCDocument36 pagesVietnam Market Insights - HSCAGIS .,JSCNo ratings yet

- Uttar Pradesh Budget Analysis 2019-20Document6 pagesUttar Pradesh Budget Analysis 2019-20AdNo ratings yet

- WTTC-travel and TourismDocument1 pageWTTC-travel and TourismAli KhavariNo ratings yet

- FD RD ERD PD Except Revenue Expenditure All Other Have Increased ConsistentlyDocument31 pagesFD RD ERD PD Except Revenue Expenditure All Other Have Increased ConsistentlyKODURI SAI UTTEJ ed16b015No ratings yet

- India International Trade Investment Website June 2022Document18 pagesIndia International Trade Investment Website June 2022vinay jodNo ratings yet

- ReQ Real Estate Quarterly HighlightsDocument8 pagesReQ Real Estate Quarterly HighlightsVaibhav RaghuvanshiNo ratings yet

- 2020 Targets - 050818 - v11 PDFDocument7 pages2020 Targets - 050818 - v11 PDFZerohedgeNo ratings yet

- ABB Analyst Meet 2013Document26 pagesABB Analyst Meet 2013Paurav LakhaniNo ratings yet

- FY 2017 PresentationDocument30 pagesFY 2017 PresentationtheredcornerNo ratings yet

- 7-Year Asset Class Real Return Forecasts : As of August 31, 2020Document1 page7-Year Asset Class Real Return Forecasts : As of August 31, 2020Stanley MunodawafaNo ratings yet

- HTTPS:/WWW - Pnbmetlife.com/documents/met Invest - ULIP - Aug18 - tcm47-66816 PDFDocument33 pagesHTTPS:/WWW - Pnbmetlife.com/documents/met Invest - ULIP - Aug18 - tcm47-66816 PDFAbhinav VermaNo ratings yet

- Karnataka Budget Analysis 2017-18Document5 pagesKarnataka Budget Analysis 2017-18Raghavendra PrabhuNo ratings yet

- Study Id117047 Nbfcs-In-IndiaDocument28 pagesStudy Id117047 Nbfcs-In-IndiavishnuNo ratings yet

- Macroeconomic Analysis Key Economic VariablesDocument6 pagesMacroeconomic Analysis Key Economic VariablesShaikh Saifullah KhalidNo ratings yet

- NBP Riba Free Savings Fund (NRFSF)Document1 pageNBP Riba Free Savings Fund (NRFSF)HIRA -No ratings yet

- NWPCap PrivateDebt Q2-2023Document2 pagesNWPCap PrivateDebt Q2-2023zackzyp98No ratings yet

- Research Pulse: February 2020Document14 pagesResearch Pulse: February 2020JeetuNo ratings yet

- NIOF-Dec 2020Document1 pageNIOF-Dec 2020chqaiserNo ratings yet

- CS Lviii 24 17062023Document3 pagesCS Lviii 24 17062023leo lokeshNo ratings yet

- Qatar - Food & Beverage Sector Overview & Forecast: Thought Leadership SeriesDocument16 pagesQatar - Food & Beverage Sector Overview & Forecast: Thought Leadership SeriesShashank Hanuman JainNo ratings yet

- Monthly Bulletin July 2023 EnglishDocument13 pagesMonthly Bulletin July 2023 EnglishNirmal MenonNo ratings yet

- Statistic - Id263617 - Gross Domestic Product GDP Growth Rate in India 2025Document8 pagesStatistic - Id263617 - Gross Domestic Product GDP Growth Rate in India 2025Sarvagya GopalNo ratings yet

- Assam Budget Analysis 2024-25Document7 pagesAssam Budget Analysis 2024-25Vnvg BnffhNo ratings yet

- State - Budget - Analysis - 2023-24 PSIRDocument7 pagesState - Budget - Analysis - 2023-24 PSIReranilvrmaNo ratings yet

- Fortnightly Banking Update: Deposit Growth Moderated But Bank Credit Growth Moderates Even MoreDocument3 pagesFortnightly Banking Update: Deposit Growth Moderated But Bank Credit Growth Moderates Even Morekumar ganeshNo ratings yet

- Roanoke Americas Alliance MarketBeat Industrial Q1 2021Document1 pageRoanoke Americas Alliance MarketBeat Industrial Q1 2021Kevin ParkerNo ratings yet

- India Market Strategy: FY23 Budget: The Struggle To Spend ProductivelyDocument34 pagesIndia Market Strategy: FY23 Budget: The Struggle To Spend ProductivelyVi KiNo ratings yet

- Cushman & Wakefield Global Cities Retail GuideDocument9 pagesCushman & Wakefield Global Cities Retail GuideFiolenzaNo ratings yet

- Jakarta Retail 2q17Document2 pagesJakarta Retail 2q17ainia putriNo ratings yet

- Essential Guide To Digital Signage Trends 2018 and BeyondDocument15 pagesEssential Guide To Digital Signage Trends 2018 and BeyondAntonio MUÑOZNo ratings yet

- (For Distribution) JLL 4Q23 Property Market OverviewDocument36 pages(For Distribution) JLL 4Q23 Property Market OverviewLouie CoNo ratings yet

- West Bengal Budget Analysis 2021-22Document9 pagesWest Bengal Budget Analysis 2021-22Ronit SahaNo ratings yet

- Uttar Pradesh Budget Analysis 2018-19Document6 pagesUttar Pradesh Budget Analysis 2018-19vaibhav gargNo ratings yet

- YES Bank Presentation Q42018Document32 pagesYES Bank Presentation Q42018sanjeev7777No ratings yet

- Commercial Real Estate - Case Study Apr 2020Document2 pagesCommercial Real Estate - Case Study Apr 2020alim shaikhNo ratings yet

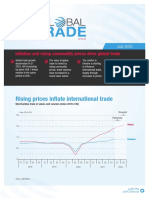

- GL Bal: Rising Prices Inflate International TradeDocument11 pagesGL Bal: Rising Prices Inflate International TradeBekele Guta GemeneNo ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- Generaciones Perú. Todas para Una y Cada Una Con Lo SuyoDocument35 pagesGeneraciones Perú. Todas para Una y Cada Una Con Lo SuyoKaren ChavezNo ratings yet

- Analyst Presentation Q2 2017 FinalDocument13 pagesAnalyst Presentation Q2 2017 FinalRamakanth GiriNo ratings yet

- Quang Ninh Research Report 2020Document26 pagesQuang Ninh Research Report 2020Architecte UrbanisteNo ratings yet

- NBP Income Opportunity Fund (Niof)Document1 pageNBP Income Opportunity Fund (Niof)HIRA -No ratings yet

- Beijing Enterprise Water Research Report 05.22.21Document4 pagesBeijing Enterprise Water Research Report 05.22.21Ralph SuarezNo ratings yet

- Rhizome Partners Q2 2020 Investor Letter FinalDocument12 pagesRhizome Partners Q2 2020 Investor Letter FinalAndy HuffNo ratings yet

- West Bengal Budget Analysis 2022-23 PDFDocument7 pagesWest Bengal Budget Analysis 2022-23 PDFSubhajit BhattacharjeeNo ratings yet

- CBRE Vietnam Market Insights Q3 2023 ENDocument55 pagesCBRE Vietnam Market Insights Q3 2023 ENTRAN QUYNH TRANG H3050No ratings yet

- Bhutan and the Asian Development Bank: Partnership for Inclusive GrowthFrom EverandBhutan and the Asian Development Bank: Partnership for Inclusive GrowthNo ratings yet

- Automatic Blackboard CleanerDocument4 pagesAutomatic Blackboard Cleanerharmanhoney_singh100% (1)

- Tectonic Evolution of Mogok Metamorphic BeltDocument21 pagesTectonic Evolution of Mogok Metamorphic BeltOak KarNo ratings yet

- Brian Cooksey - An Introduction To APIs-Zapier Inc (2014)Document100 pagesBrian Cooksey - An Introduction To APIs-Zapier Inc (2014)zakaria abbadiNo ratings yet

- Data Sheet For Pressure Gauge and DP GaugeDocument1 pageData Sheet For Pressure Gauge and DP Gaugeanand patelNo ratings yet

- Setting and Hardening of ConcreteDocument30 pagesSetting and Hardening of ConcreteManjer123No ratings yet

- Manual Bluetti Eb150Document12 pagesManual Bluetti Eb150Rafa Lozoya AlbacarNo ratings yet

- Repsol Oil Operations: Nc-115 Field DevelopmentDocument11 pagesRepsol Oil Operations: Nc-115 Field DevelopmentYangui AliNo ratings yet

- AADE 05 NTCE 52 - PatilDocument8 pagesAADE 05 NTCE 52 - PatilAhmad Reza FarokhiNo ratings yet

- 0650-EDW-00009-02 - Seaking DST Parts List - Customer Parts ListDocument11 pages0650-EDW-00009-02 - Seaking DST Parts List - Customer Parts ListJosianeMacielNo ratings yet

- OPT B1plus U09 Grammar HigherDocument1 pageOPT B1plus U09 Grammar HigherJacobo GutierrezNo ratings yet

- MGT 534 Organizational Behavior2Document3 pagesMGT 534 Organizational Behavior2Phattyin ZaharahNo ratings yet

- Name: Waguma Leticia: Jomo Kenyatta University of Agriculture and Technology Nakuru CampusDocument9 pagesName: Waguma Leticia: Jomo Kenyatta University of Agriculture and Technology Nakuru CampusWaguma LeticiaNo ratings yet

- Dr. Wifanto-Management Liver Metastasis CRCDocument46 pagesDr. Wifanto-Management Liver Metastasis CRCAfkar30No ratings yet

- Problem Set 1 - Review On Basic Soil Mech FormulasDocument2 pagesProblem Set 1 - Review On Basic Soil Mech FormulasKenny SiludNo ratings yet

- CP7211 Advanced Databases Laboratory ManualDocument63 pagesCP7211 Advanced Databases Laboratory Manualashaheer75% (4)

- SANTOS VsDocument12 pagesSANTOS VsKristel YeenNo ratings yet

- FFC New Imp FormatDocument1 pageFFC New Imp FormatMalik Zaryab babarNo ratings yet

- The Vivago Watch A Telecare Solution For Cost-Efficient CareDocument1 pageThe Vivago Watch A Telecare Solution For Cost-Efficient CareGeronTechnoPlatformNo ratings yet

- XI Theories and Schools of Modern LinguisticsDocument62 pagesXI Theories and Schools of Modern LinguisticsDjallelBoulmaizNo ratings yet

- Daftar Pustaka: Thrombosis: Basic Principles and Clinical Practice. 6 Ed. Philadelphia, PADocument3 pagesDaftar Pustaka: Thrombosis: Basic Principles and Clinical Practice. 6 Ed. Philadelphia, PAAhmad Agus PurwantoNo ratings yet

- Ravi LE ROCHUS - ResumeDocument1 pageRavi LE ROCHUS - ResumeRavi Le RochusNo ratings yet

- Swot NBPDocument8 pagesSwot NBPWajahat SufianNo ratings yet

- Well ViewDocument1 pageWell Viewoa3740523No ratings yet

- Democratic Life Skill 1Document1 pageDemocratic Life Skill 1andinurzamzamNo ratings yet

- Lisa Olle Declaration in SupportDocument5 pagesLisa Olle Declaration in SupportMikey CampbellNo ratings yet

- Smart Battery Data Specification Revision 1.1 ErrataDocument5 pagesSmart Battery Data Specification Revision 1.1 ErrataredmsbatteryNo ratings yet

- The Language of Legal DocumentsDocument15 pagesThe Language of Legal DocumentsAldo CokaNo ratings yet

- 6 - Telephone and Cable Networks For Data TransmissionDocument31 pages6 - Telephone and Cable Networks For Data TransmissionpranjalcrackuNo ratings yet

- Homework 13.3.2024Document2 pagesHomework 13.3.2024vothaibinh2004No ratings yet