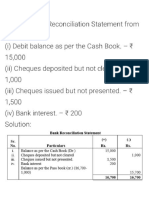

01-11-2023 - 08.00pm - Accounts - Bank Reconciliation Statement Assignment

01-11-2023 - 08.00pm - Accounts - Bank Reconciliation Statement Assignment

You might also like

- GMCVB Marketing Plan Y 2023Document95 pagesGMCVB Marketing Plan Y 2023avinaauthoringtools3No ratings yet

- Auditing Concept Problems Cash and Cash EquivalentDocument7 pagesAuditing Concept Problems Cash and Cash EquivalentJoanah TayamenNo ratings yet

- Additional Practical Problems-13-1Document5 pagesAdditional Practical Problems-13-1sharmaarmaan103No ratings yet

- Practice With MT - BRSDocument6 pagesPractice With MT - BRSsrushtibhawsar07No ratings yet

- CA Foundation Accounts Q MTP 1 June 2024 Castudynotes ComDocument8 pagesCA Foundation Accounts Q MTP 1 June 2024 Castudynotes Comgokulthilagam362No ratings yet

- Navyug Commerce Institute Lakhanpur Kanpur Topic-B.R.SDocument2 pagesNavyug Commerce Institute Lakhanpur Kanpur Topic-B.R.SparthNo ratings yet

- BRS PDFDocument14 pagesBRS PDFGautam KhanwaniNo ratings yet

- 39759Document3 pages39759MonikaNo ratings yet

- Accounts June 2024Document8 pagesAccounts June 2024rajdjpurohitNo ratings yet

- Tsgrewal BRSDocument11 pagesTsgrewal BRSDhruvNo ratings yet

- Q-10 Prepare Bank Reconciliation Statement As On 31Document2 pagesQ-10 Prepare Bank Reconciliation Statement As On 31krish mehtaNo ratings yet

- Business Acoounting (2020)Document4 pagesBusiness Acoounting (2020)harshdeepgarg5No ratings yet

- BRS WSDocument2 pagesBRS WSShrajith A NatarajanNo ratings yet

- Chapter 9 - Bank Reconciliation StatementDocument15 pagesChapter 9 - Bank Reconciliation StatementSaurabh GohanNo ratings yet

- Bank Reconciliation StatementDocument12 pagesBank Reconciliation StatementBhuvan PrajapatiNo ratings yet

- Adobe Scan 05 Jan 2024Document2 pagesAdobe Scan 05 Jan 2024Harshit GargNo ratings yet

- Ca Foundation Accounts Test Paper: Maximum Marks: 40 Time Allowed: 1hr. Allowed: 1hr. 15 MinutesDocument3 pagesCa Foundation Accounts Test Paper: Maximum Marks: 40 Time Allowed: 1hr. Allowed: 1hr. 15 Minutesvanshikha.agarwal345No ratings yet

- B.R.S. Test 3Document5 pagesB.R.S. Test 3Sudhir SinhaNo ratings yet

- 21Document10 pages21aroranavdishNo ratings yet

- 0c26dbank Reconciliation Statement Practice QuestionsDocument2 pages0c26dbank Reconciliation Statement Practice QuestionsRahul AgarwalNo ratings yet

- CA Foundation Accounts Q MTP 2 Nov23 Castudynotes ComDocument6 pagesCA Foundation Accounts Q MTP 2 Nov23 Castudynotes Comhariniharini03904No ratings yet

- BRS RevisionDocument2 pagesBRS RevisionHarsh ModiNo ratings yet

- Accountancy XI: Pankaj Rajan 9810194206Document4 pagesAccountancy XI: Pankaj Rajan 9810194206A4S ARMY Akshdeep singhNo ratings yet

- Assignment BRSDocument2 pagesAssignment BRSveydantsharma42No ratings yet

- BRS Ca FoundationDocument9 pagesBRS Ca FoundationJunaid Iqbal MastoiNo ratings yet

- Dkgoel BRS 11Document15 pagesDkgoel BRS 11DhruvNo ratings yet

- 3.CA Foundation Test 3Document5 pages3.CA Foundation Test 3Nived Narayan PNo ratings yet

- CA F BRS WithDocument10 pagesCA F BRS WithG. DhanyaNo ratings yet

- 6 BRS 08-2023 RegularDocument7 pages6 BRS 08-2023 RegularjahnaviNo ratings yet

- Prepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookDocument10 pagesPrepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookPragya ShuklaNo ratings yet

- Bank Reconciliation Statement Practice ProblemsDocument2 pagesBank Reconciliation Statement Practice ProblemsHaya DanishNo ratings yet

- BRS Class 11Document1 pageBRS Class 11tarun aroraNo ratings yet

- Exam Type Question of Accountancy, Class XiDocument3 pagesExam Type Question of Accountancy, Class Xirobinghimire100% (7)

- Ts Grewal Solutions For Class 11 Accountancy Chapter 9 BankDocument34 pagesTs Grewal Solutions For Class 11 Accountancy Chapter 9 Bankmyankjindal9No ratings yet

- Practical - Bank Reconciliation StatementDocument5 pagesPractical - Bank Reconciliation StatementUniversal SoldierNo ratings yet

- Adobe Scan Apr 10, 2023Document12 pagesAdobe Scan Apr 10, 2023ineshbanerjee80No ratings yet

- Bank Reconcilaition Statement Problems PDF 1 4 PDFDocument4 pagesBank Reconcilaition Statement Problems PDF 1 4 PDFHakim JanNo ratings yet

- BRS SCANNER by Nahta PDFDocument24 pagesBRS SCANNER by Nahta PDFVaidika JainNo ratings yet

- Brs Practical QuestionsDocument5 pagesBrs Practical QuestionsSwarupa VNo ratings yet

- WS - Xi BRS - 2Document5 pagesWS - Xi BRS - 2richshivamshahNo ratings yet

- Test 4Document6 pagesTest 4Jayant MittalNo ratings yet

- BRS WorksheetDocument8 pagesBRS WorksheetMayank VermaNo ratings yet

- CA Foundation BRS Practice Questions - DRS - CTC ClassesDocument2 pagesCA Foundation BRS Practice Questions - DRS - CTC ClassesAnas AzeemNo ratings yet

- Mid Term Accounts - SubjectiveDocument4 pagesMid Term Accounts - Subjectivekarishma prabagaranNo ratings yet

- BRS 2Document2 pagesBRS 2Aarnav SharmaNo ratings yet

- Bank Reconciliation Statement Problems and Solutions I BRS I AK PDFDocument12 pagesBank Reconciliation Statement Problems and Solutions I BRS I AK PDFAdvance Knowledge88% (8)

- Test Series: May, 2022 Mock Test Paper 2 Foundation Course Paper - 1: Principles and Practice of AccountingDocument5 pagesTest Series: May, 2022 Mock Test Paper 2 Foundation Course Paper - 1: Principles and Practice of AccountingGayathiri RNo ratings yet

- Quiz 1 - Audit of CashDocument4 pagesQuiz 1 - Audit of CashmillescaasiNo ratings yet

- SET B 11th Acc BRS N RECT.Document2 pagesSET B 11th Acc BRS N RECT.Mohammad Tariq AnsariNo ratings yet

- Worksheet BRSDocument2 pagesWorksheet BRSCA Chhavi Gupta100% (1)

- Bank Reconciliation StatementDocument13 pagesBank Reconciliation Statement20232024s5r14leungjacobNo ratings yet

- Bank Reconciliation Statement AssignmentDocument3 pagesBank Reconciliation Statement AssignmentDev KumarNo ratings yet

- 06 BRS - Practice QuestionsDocument1 page06 BRS - Practice QuestionsNeelanjana RayNo ratings yet

- Test Aldine FinalDocument3 pagesTest Aldine FinalAkshay TulshyanNo ratings yet

- Foundation Accounts Suggested Nov20Document25 pagesFoundation Accounts Suggested Nov20dhanushd0613No ratings yet

- BRS Statement IllustrationsDocument3 pagesBRS Statement Illustrationssurekha khandebharadNo ratings yet

- 5664accountancy XIDocument9 pages5664accountancy XIAryan VishwakarmaNo ratings yet

- Bank Reconciliation StatementDocument33 pagesBank Reconciliation StatementMd TahirNo ratings yet

- F005 Test 5 StudentsDocument6 pagesF005 Test 5 StudentsbhumikaaNo ratings yet

- QuestionsDocument5 pagesQuestionsmonster gamerNo ratings yet

- Ill-Gotten Money and the Economy: Experiences from Malawi and NamibiaFrom EverandIll-Gotten Money and the Economy: Experiences from Malawi and NamibiaNo ratings yet

- Nes D2188Document6 pagesNes D2188prasannaNo ratings yet

- HP Scanjet Pro 2500 F1 Flatbed Scanner: DatasheetDocument2 pagesHP Scanjet Pro 2500 F1 Flatbed Scanner: DatasheetKarkittykatNo ratings yet

- Recognition, Signaling, and Repair of DNA Double-Strand Breaks Produced by Ionizing Radiation in Mammalian Cells - The Molecular ChoreographyDocument89 pagesRecognition, Signaling, and Repair of DNA Double-Strand Breaks Produced by Ionizing Radiation in Mammalian Cells - The Molecular ChoreographyMaria ClaraNo ratings yet

- Assessment of Digestive and GI FunctionDocument23 pagesAssessment of Digestive and GI FunctionSandeepNo ratings yet

- Before Reading: An Encyclopedia EntryDocument6 pagesBefore Reading: An Encyclopedia EntryĐào Nguyễn Duy TùngNo ratings yet

- Synopsis Car Showroom ManagementDocument18 pagesSynopsis Car Showroom ManagementRaj Bangalore50% (4)

- Martin Luther King Jr. - A True Historical Examination. (N.D.) - Retrieved OctoberDocument5 pagesMartin Luther King Jr. - A True Historical Examination. (N.D.) - Retrieved Octoberapi-336574490No ratings yet

- The Russian Military Today and Tomorrow: Essays in Memory of Mary FitzgeraldDocument474 pagesThe Russian Military Today and Tomorrow: Essays in Memory of Mary FitzgeraldSSI-Strategic Studies Institute-US Army War College100% (1)

- Crim Pro 2004-2010 Bar QuestionsDocument4 pagesCrim Pro 2004-2010 Bar QuestionsDennie Vieve IdeaNo ratings yet

- Kapandji TrunkDocument245 pagesKapandji TrunkVTZIOTZIAS90% (10)

- Resource AllocationDocument10 pagesResource AllocationZoe NyadziNo ratings yet

- Trades About To Happen - David Weiss - Notes FromDocument3 pagesTrades About To Happen - David Weiss - Notes FromUma Maheshwaran100% (1)

- Chem 26.1 Lab Manual 2017 Edition (2019) PDFDocument63 pagesChem 26.1 Lab Manual 2017 Edition (2019) PDFBea JacintoNo ratings yet

- Uperpowered Estiary: Boleth To YclopsDocument6 pagesUperpowered Estiary: Boleth To YclopsMatheusEnder172No ratings yet

- The Wexford Carol (Arr Victor C Johnson)Document13 pagesThe Wexford Carol (Arr Victor C Johnson)Macdara de BurcaNo ratings yet

- Rev JSRR 45765Document2 pagesRev JSRR 45765Amit BNo ratings yet

- Hispanic Tradition in Philippine ArtsDocument14 pagesHispanic Tradition in Philippine ArtsRoger Pascual Cuaresma100% (1)

- Prince Ganai NuclearDocument30 pagesPrince Ganai Nuclearprince_ganaiNo ratings yet

- The Madmullah of Somaliland 1916 1921Document386 pagesThe Madmullah of Somaliland 1916 1921Khadar Hayaan Freelancer100% (1)

- Squirrels of Indian SubcontinentDocument14 pagesSquirrels of Indian SubcontinentAkshay MotiNo ratings yet

- Final Artifact Management Theory IIDocument11 pagesFinal Artifact Management Theory IIapi-651643566No ratings yet

- CAN LIN ProtocolDocument60 pagesCAN LIN ProtocolBrady BriffaNo ratings yet

- Student Assesment PDFDocument1 pageStudent Assesment PDFBelaNo ratings yet

- Industry ProfileDocument9 pagesIndustry ProfilesarathNo ratings yet

- MSP432 Chapter2 v1Document59 pagesMSP432 Chapter2 v1Akshat TulsaniNo ratings yet

- Neuromusic IIIDocument3 pagesNeuromusic IIIJudit VallejoNo ratings yet

- Palm Oil MillDocument52 pagesPalm Oil MillengrsurifNo ratings yet

- Architecture in EthDocument4 pagesArchitecture in Ethmelakumikias2No ratings yet

- Skullcandy Case Study - Part OneDocument8 pagesSkullcandy Case Study - Part OneUthmanNo ratings yet

Download as pdf or txt

You might also like

- GMCVB Marketing Plan Y 2023Document95 pagesGMCVB Marketing Plan Y 2023avinaauthoringtools3No ratings yet

- Auditing Concept Problems Cash and Cash EquivalentDocument7 pagesAuditing Concept Problems Cash and Cash EquivalentJoanah TayamenNo ratings yet

- Additional Practical Problems-13-1Document5 pagesAdditional Practical Problems-13-1sharmaarmaan103No ratings yet

- Practice With MT - BRSDocument6 pagesPractice With MT - BRSsrushtibhawsar07No ratings yet

- CA Foundation Accounts Q MTP 1 June 2024 Castudynotes ComDocument8 pagesCA Foundation Accounts Q MTP 1 June 2024 Castudynotes Comgokulthilagam362No ratings yet

- Navyug Commerce Institute Lakhanpur Kanpur Topic-B.R.SDocument2 pagesNavyug Commerce Institute Lakhanpur Kanpur Topic-B.R.SparthNo ratings yet

- BRS PDFDocument14 pagesBRS PDFGautam KhanwaniNo ratings yet

- 39759Document3 pages39759MonikaNo ratings yet

- Accounts June 2024Document8 pagesAccounts June 2024rajdjpurohitNo ratings yet

- Tsgrewal BRSDocument11 pagesTsgrewal BRSDhruvNo ratings yet

- Q-10 Prepare Bank Reconciliation Statement As On 31Document2 pagesQ-10 Prepare Bank Reconciliation Statement As On 31krish mehtaNo ratings yet

- Business Acoounting (2020)Document4 pagesBusiness Acoounting (2020)harshdeepgarg5No ratings yet

- BRS WSDocument2 pagesBRS WSShrajith A NatarajanNo ratings yet

- Chapter 9 - Bank Reconciliation StatementDocument15 pagesChapter 9 - Bank Reconciliation StatementSaurabh GohanNo ratings yet

- Bank Reconciliation StatementDocument12 pagesBank Reconciliation StatementBhuvan PrajapatiNo ratings yet

- Adobe Scan 05 Jan 2024Document2 pagesAdobe Scan 05 Jan 2024Harshit GargNo ratings yet

- Ca Foundation Accounts Test Paper: Maximum Marks: 40 Time Allowed: 1hr. Allowed: 1hr. 15 MinutesDocument3 pagesCa Foundation Accounts Test Paper: Maximum Marks: 40 Time Allowed: 1hr. Allowed: 1hr. 15 Minutesvanshikha.agarwal345No ratings yet

- B.R.S. Test 3Document5 pagesB.R.S. Test 3Sudhir SinhaNo ratings yet

- 21Document10 pages21aroranavdishNo ratings yet

- 0c26dbank Reconciliation Statement Practice QuestionsDocument2 pages0c26dbank Reconciliation Statement Practice QuestionsRahul AgarwalNo ratings yet

- CA Foundation Accounts Q MTP 2 Nov23 Castudynotes ComDocument6 pagesCA Foundation Accounts Q MTP 2 Nov23 Castudynotes Comhariniharini03904No ratings yet

- BRS RevisionDocument2 pagesBRS RevisionHarsh ModiNo ratings yet

- Accountancy XI: Pankaj Rajan 9810194206Document4 pagesAccountancy XI: Pankaj Rajan 9810194206A4S ARMY Akshdeep singhNo ratings yet

- Assignment BRSDocument2 pagesAssignment BRSveydantsharma42No ratings yet

- BRS Ca FoundationDocument9 pagesBRS Ca FoundationJunaid Iqbal MastoiNo ratings yet

- Dkgoel BRS 11Document15 pagesDkgoel BRS 11DhruvNo ratings yet

- 3.CA Foundation Test 3Document5 pages3.CA Foundation Test 3Nived Narayan PNo ratings yet

- CA F BRS WithDocument10 pagesCA F BRS WithG. DhanyaNo ratings yet

- 6 BRS 08-2023 RegularDocument7 pages6 BRS 08-2023 RegularjahnaviNo ratings yet

- Prepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookDocument10 pagesPrepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookPragya ShuklaNo ratings yet

- Bank Reconciliation Statement Practice ProblemsDocument2 pagesBank Reconciliation Statement Practice ProblemsHaya DanishNo ratings yet

- BRS Class 11Document1 pageBRS Class 11tarun aroraNo ratings yet

- Exam Type Question of Accountancy, Class XiDocument3 pagesExam Type Question of Accountancy, Class Xirobinghimire100% (7)

- Ts Grewal Solutions For Class 11 Accountancy Chapter 9 BankDocument34 pagesTs Grewal Solutions For Class 11 Accountancy Chapter 9 Bankmyankjindal9No ratings yet

- Practical - Bank Reconciliation StatementDocument5 pagesPractical - Bank Reconciliation StatementUniversal SoldierNo ratings yet

- Adobe Scan Apr 10, 2023Document12 pagesAdobe Scan Apr 10, 2023ineshbanerjee80No ratings yet

- Bank Reconcilaition Statement Problems PDF 1 4 PDFDocument4 pagesBank Reconcilaition Statement Problems PDF 1 4 PDFHakim JanNo ratings yet

- BRS SCANNER by Nahta PDFDocument24 pagesBRS SCANNER by Nahta PDFVaidika JainNo ratings yet

- Brs Practical QuestionsDocument5 pagesBrs Practical QuestionsSwarupa VNo ratings yet

- WS - Xi BRS - 2Document5 pagesWS - Xi BRS - 2richshivamshahNo ratings yet

- Test 4Document6 pagesTest 4Jayant MittalNo ratings yet

- BRS WorksheetDocument8 pagesBRS WorksheetMayank VermaNo ratings yet

- CA Foundation BRS Practice Questions - DRS - CTC ClassesDocument2 pagesCA Foundation BRS Practice Questions - DRS - CTC ClassesAnas AzeemNo ratings yet

- Mid Term Accounts - SubjectiveDocument4 pagesMid Term Accounts - Subjectivekarishma prabagaranNo ratings yet

- BRS 2Document2 pagesBRS 2Aarnav SharmaNo ratings yet

- Bank Reconciliation Statement Problems and Solutions I BRS I AK PDFDocument12 pagesBank Reconciliation Statement Problems and Solutions I BRS I AK PDFAdvance Knowledge88% (8)

- Test Series: May, 2022 Mock Test Paper 2 Foundation Course Paper - 1: Principles and Practice of AccountingDocument5 pagesTest Series: May, 2022 Mock Test Paper 2 Foundation Course Paper - 1: Principles and Practice of AccountingGayathiri RNo ratings yet

- Quiz 1 - Audit of CashDocument4 pagesQuiz 1 - Audit of CashmillescaasiNo ratings yet

- SET B 11th Acc BRS N RECT.Document2 pagesSET B 11th Acc BRS N RECT.Mohammad Tariq AnsariNo ratings yet

- Worksheet BRSDocument2 pagesWorksheet BRSCA Chhavi Gupta100% (1)

- Bank Reconciliation StatementDocument13 pagesBank Reconciliation Statement20232024s5r14leungjacobNo ratings yet

- Bank Reconciliation Statement AssignmentDocument3 pagesBank Reconciliation Statement AssignmentDev KumarNo ratings yet

- 06 BRS - Practice QuestionsDocument1 page06 BRS - Practice QuestionsNeelanjana RayNo ratings yet

- Test Aldine FinalDocument3 pagesTest Aldine FinalAkshay TulshyanNo ratings yet

- Foundation Accounts Suggested Nov20Document25 pagesFoundation Accounts Suggested Nov20dhanushd0613No ratings yet

- BRS Statement IllustrationsDocument3 pagesBRS Statement Illustrationssurekha khandebharadNo ratings yet

- 5664accountancy XIDocument9 pages5664accountancy XIAryan VishwakarmaNo ratings yet

- Bank Reconciliation StatementDocument33 pagesBank Reconciliation StatementMd TahirNo ratings yet

- F005 Test 5 StudentsDocument6 pagesF005 Test 5 StudentsbhumikaaNo ratings yet

- QuestionsDocument5 pagesQuestionsmonster gamerNo ratings yet

- Ill-Gotten Money and the Economy: Experiences from Malawi and NamibiaFrom EverandIll-Gotten Money and the Economy: Experiences from Malawi and NamibiaNo ratings yet

- Nes D2188Document6 pagesNes D2188prasannaNo ratings yet

- HP Scanjet Pro 2500 F1 Flatbed Scanner: DatasheetDocument2 pagesHP Scanjet Pro 2500 F1 Flatbed Scanner: DatasheetKarkittykatNo ratings yet

- Recognition, Signaling, and Repair of DNA Double-Strand Breaks Produced by Ionizing Radiation in Mammalian Cells - The Molecular ChoreographyDocument89 pagesRecognition, Signaling, and Repair of DNA Double-Strand Breaks Produced by Ionizing Radiation in Mammalian Cells - The Molecular ChoreographyMaria ClaraNo ratings yet

- Assessment of Digestive and GI FunctionDocument23 pagesAssessment of Digestive and GI FunctionSandeepNo ratings yet

- Before Reading: An Encyclopedia EntryDocument6 pagesBefore Reading: An Encyclopedia EntryĐào Nguyễn Duy TùngNo ratings yet

- Synopsis Car Showroom ManagementDocument18 pagesSynopsis Car Showroom ManagementRaj Bangalore50% (4)

- Martin Luther King Jr. - A True Historical Examination. (N.D.) - Retrieved OctoberDocument5 pagesMartin Luther King Jr. - A True Historical Examination. (N.D.) - Retrieved Octoberapi-336574490No ratings yet

- The Russian Military Today and Tomorrow: Essays in Memory of Mary FitzgeraldDocument474 pagesThe Russian Military Today and Tomorrow: Essays in Memory of Mary FitzgeraldSSI-Strategic Studies Institute-US Army War College100% (1)

- Crim Pro 2004-2010 Bar QuestionsDocument4 pagesCrim Pro 2004-2010 Bar QuestionsDennie Vieve IdeaNo ratings yet

- Kapandji TrunkDocument245 pagesKapandji TrunkVTZIOTZIAS90% (10)

- Resource AllocationDocument10 pagesResource AllocationZoe NyadziNo ratings yet

- Trades About To Happen - David Weiss - Notes FromDocument3 pagesTrades About To Happen - David Weiss - Notes FromUma Maheshwaran100% (1)

- Chem 26.1 Lab Manual 2017 Edition (2019) PDFDocument63 pagesChem 26.1 Lab Manual 2017 Edition (2019) PDFBea JacintoNo ratings yet

- Uperpowered Estiary: Boleth To YclopsDocument6 pagesUperpowered Estiary: Boleth To YclopsMatheusEnder172No ratings yet

- The Wexford Carol (Arr Victor C Johnson)Document13 pagesThe Wexford Carol (Arr Victor C Johnson)Macdara de BurcaNo ratings yet

- Rev JSRR 45765Document2 pagesRev JSRR 45765Amit BNo ratings yet

- Hispanic Tradition in Philippine ArtsDocument14 pagesHispanic Tradition in Philippine ArtsRoger Pascual Cuaresma100% (1)

- Prince Ganai NuclearDocument30 pagesPrince Ganai Nuclearprince_ganaiNo ratings yet

- The Madmullah of Somaliland 1916 1921Document386 pagesThe Madmullah of Somaliland 1916 1921Khadar Hayaan Freelancer100% (1)

- Squirrels of Indian SubcontinentDocument14 pagesSquirrels of Indian SubcontinentAkshay MotiNo ratings yet

- Final Artifact Management Theory IIDocument11 pagesFinal Artifact Management Theory IIapi-651643566No ratings yet

- CAN LIN ProtocolDocument60 pagesCAN LIN ProtocolBrady BriffaNo ratings yet

- Student Assesment PDFDocument1 pageStudent Assesment PDFBelaNo ratings yet

- Industry ProfileDocument9 pagesIndustry ProfilesarathNo ratings yet

- MSP432 Chapter2 v1Document59 pagesMSP432 Chapter2 v1Akshat TulsaniNo ratings yet

- Neuromusic IIIDocument3 pagesNeuromusic IIIJudit VallejoNo ratings yet

- Palm Oil MillDocument52 pagesPalm Oil MillengrsurifNo ratings yet

- Architecture in EthDocument4 pagesArchitecture in Ethmelakumikias2No ratings yet

- Skullcandy Case Study - Part OneDocument8 pagesSkullcandy Case Study - Part OneUthmanNo ratings yet