Download as docx, pdf, or txt

You might also like

- ABC Internal Controls PDFDocument2 pagesABC Internal Controls PDFice manga100% (3)

- Auditing Accounts ReceivableDocument5 pagesAuditing Accounts ReceivableVivien NaigNo ratings yet

- Subdivision, Partition, Amalgamation (Land Development) AssignmentDocument14 pagesSubdivision, Partition, Amalgamation (Land Development) AssignmentYingling NgNo ratings yet

- Session 3 - Practice Exercise 1 - Check Co - Audit Risks Respones - Question AnsDocument4 pagesSession 3 - Practice Exercise 1 - Check Co - Audit Risks Respones - Question AnsKim NgânNo ratings yet

- Auditing Part 3Document10 pagesAuditing Part 3Trisha BanzonNo ratings yet

- Internal Control and EvidenceDocument12 pagesInternal Control and EvidenceSanaNo ratings yet

- Fundamentals Level - Skills Module, F8 (INT) Audit and AssuranceDocument12 pagesFundamentals Level - Skills Module, F8 (INT) Audit and AssurancekhengmaiNo ratings yet

- Adv. Aud. CH 6 Auditor Resp.Document5 pagesAdv. Aud. CH 6 Auditor Resp.HagarMahmoudNo ratings yet

- Audit ProceduresDocument4 pagesAudit Proceduresakhil.ng6No ratings yet

- Kaplan Audit Procedures GuidanceDocument18 pagesKaplan Audit Procedures Guidancebasit ovaisiNo ratings yet

- Cfo Advisory CmaasDocument27 pagesCfo Advisory Cmaasanjali aggarwalNo ratings yet

- Auditing 1 Final Chapter 10Document7 pagesAuditing 1 Final Chapter 10PaupauNo ratings yet

- Article: Home About Resources Sample Questions StoreDocument62 pagesArticle: Home About Resources Sample Questions StorejojinjulieNo ratings yet

- Auditng CIA-1Document5 pagesAuditng CIA-1Hitesh ohlyanNo ratings yet

- Audit and Assuranc1Document5 pagesAudit and Assuranc1shaazNo ratings yet

- ARIBA, Fretzyl Bless A. - Chapter 9 - Substantive Test of Receivables and Sales - ReflectionDocument3 pagesARIBA, Fretzyl Bless A. - Chapter 9 - Substantive Test of Receivables and Sales - ReflectionFretzyl JulyNo ratings yet

- What Are Some of The Limitations of Periodic, Manual, and Sample-Based Audits?Document2 pagesWhat Are Some of The Limitations of Periodic, Manual, and Sample-Based Audits?Laiza Joyce SalesNo ratings yet

- Audit ReportDocument10 pagesAudit Report03fl22bcl033No ratings yet

- Paper Tech IndustriesDocument20 pagesPaper Tech IndustriesMargaret TaylorNo ratings yet

- 153Document1 page153Swapnil MahantaNo ratings yet

- Types of Audit EvidenceDocument10 pagesTypes of Audit EvidenceEDELYN PoblacionNo ratings yet

- Pederson CPA Review AUD Study Notes Audit PlanningDocument10 pagesPederson CPA Review AUD Study Notes Audit PlanningRyanMosMckoyNo ratings yet

- Chapter2Document4 pagesChapter2Keanne ArmstrongNo ratings yet

- ACCT 555 Audit Week 7Document5 pagesACCT 555 Audit Week 7Natasha DeclanNo ratings yet

- AuditingCorporateGovernance - BasicInt - An Overview of The Audit ProcessDocument4 pagesAuditingCorporateGovernance - BasicInt - An Overview of The Audit ProcessIsmaaeel Essay KotwalNo ratings yet

- Audit ProceduresDocument4 pagesAudit Procedureschristien tshikaNo ratings yet

- IA of OTC 1678120325Document16 pagesIA of OTC 1678120325Bachir LoukiliNo ratings yet

- Exam Kit Specimen (Cases)Document6 pagesExam Kit Specimen (Cases)Mayurika DassaniNo ratings yet

- Audit ReportDocument10 pagesAudit Report03fl22bcl033No ratings yet

- Detection Risks NotesDocument2 pagesDetection Risks NotesMoeer razaNo ratings yet

- TheProcure To PayCyclebyChristineDoxeyDocument6 pagesTheProcure To PayCyclebyChristineDoxeyrajus_cisa6423No ratings yet

- The Purpose of Audit TestsDocument2 pagesThe Purpose of Audit TestsOsemwegie PaulNo ratings yet

- ACCO 30043 Assignment No.3Document8 pagesACCO 30043 Assignment No.3RoseanneNo ratings yet

- Chapter 10-OA AssignDocument2 pagesChapter 10-OA AssignJeane Mae BooNo ratings yet

- Oliveros, Mark M. ACTYCY32S1-3 Year Accountancy ACCTG 026 - Auditing and Assurance: Specialized IndustriesDocument6 pagesOliveros, Mark M. ACTYCY32S1-3 Year Accountancy ACCTG 026 - Auditing and Assurance: Specialized IndustriesJessalyn DaneNo ratings yet

- Solution Manual For Auditing and Assurance Services An Applied Approach Stuart 1st EditionDocument13 pagesSolution Manual For Auditing and Assurance Services An Applied Approach Stuart 1st EditionMeredithFleminggztayNo ratings yet

- Answer 1Document3 pagesAnswer 1Ansika ChoudharyNo ratings yet

- Audit Risk NotesDocument8 pagesAudit Risk NotesAditya KanabarNo ratings yet

- CA Inter (QB) - Chapter 5Document85 pagesCA Inter (QB) - Chapter 5Aishu SivadasanNo ratings yet

- Auditing Ass1Document14 pagesAuditing Ass1Azlinda JonathanNo ratings yet

- 2RAC - Revision 2019 Lecture 11Document7 pages2RAC - Revision 2019 Lecture 11Jia YinNo ratings yet

- ACC701Sem - Mid Sem Revision Questions - SolutionsDocument4 pagesACC701Sem - Mid Sem Revision Questions - SolutionsUshra KhanNo ratings yet

- Chapter 8 Systems and ControlsDocument4 pagesChapter 8 Systems and Controlsrishi kareliaNo ratings yet

- Reviewer 4 - Audit of ReceivablesDocument2 pagesReviewer 4 - Audit of ReceivablesCASAMAYOR JOVELYN B.No ratings yet

- Substantive Tests123Document3 pagesSubstantive Tests123Ryan TamondongNo ratings yet

- Vouching and VerificationDocument26 pagesVouching and VerificationmfranciskishushuNo ratings yet

- Kit - Q - 229 - Pear - International Deficiencies Recommendations Test of ControlsDocument2 pagesKit - Q - 229 - Pear - International Deficiencies Recommendations Test of ControlsEwe PieNo ratings yet

- ReceivablesDocument9 pagesReceivablesThinagari JevataranNo ratings yet

- Fraud Auditing Dr. Sanjib Basu Department of Commerce, ST - Xavier's CollegeDocument6 pagesFraud Auditing Dr. Sanjib Basu Department of Commerce, ST - Xavier's CollegeKunal ChauhanNo ratings yet

- 1.1. Background-Wps OfficeDocument7 pages1.1. Background-Wps OfficeFrederick AgyemangNo ratings yet

- OpAudCh10-CBET-01-501E-Toralde, Ma - Kristine E.Document6 pagesOpAudCh10-CBET-01-501E-Toralde, Ma - Kristine E.Kristine Esplana ToraldeNo ratings yet

- Notes in Audit Acn001 (Prelim)Document3 pagesNotes in Audit Acn001 (Prelim)Josephine YenNo ratings yet

- Auditing Notes.Document55 pagesAuditing Notes.Viraja Guru50% (2)

- 5 PlanningDocument20 pages5 PlanningSayraj Siddiki AnikNo ratings yet

- Auditing and Assurance - Concepts and Applications - Lecture AidDocument30 pagesAuditing and Assurance - Concepts and Applications - Lecture AidBrithney ButalidNo ratings yet

- ACFrOgD1sYm56PHRPgCcMMl5ZVdZLplwetgPn9flkODr97nA1JvYCzGRaEUz4Y3uoPI icInXbPlRHbeN0ATMBgRZTh3 u5zHfN9cnxYzQARZvphHUjGpIFt2rLeiuIjnfdH0F1Wsja-UxIdWVcODocument5 pagesACFrOgD1sYm56PHRPgCcMMl5ZVdZLplwetgPn9flkODr97nA1JvYCzGRaEUz4Y3uoPI icInXbPlRHbeN0ATMBgRZTh3 u5zHfN9cnxYzQARZvphHUjGpIFt2rLeiuIjnfdH0F1Wsja-UxIdWVcOclara san miguelNo ratings yet

- Essay On AuditingDocument7 pagesEssay On AuditingAndy Rdz0% (1)

- Forensic Accounting ReportDocument11 pagesForensic Accounting ReportNike ColeNo ratings yet

- Tinkerbell: Key Control Test of ControlDocument2 pagesTinkerbell: Key Control Test of ControlIanNo ratings yet

- Substantive ProceduresDocument10 pagesSubstantive ProceduresfyzaaaanNo ratings yet

- English 9 Q1 1 - Modals Used in Expressing Permission, Obligation, and ProhibitionDocument33 pagesEnglish 9 Q1 1 - Modals Used in Expressing Permission, Obligation, and ProhibitionMarilyn GuillermoNo ratings yet

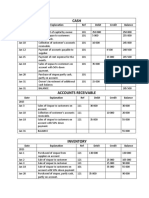

- Date Explanation Ref Debit Credit BalanceDocument6 pagesDate Explanation Ref Debit Credit BalanceKissedNo ratings yet

- 2018 09 03 220829 LawDocument12 pages2018 09 03 220829 LawNelson JordanNo ratings yet

- Facts.: Donoghue V Stevenson (1932) AC 562Document5 pagesFacts.: Donoghue V Stevenson (1932) AC 562MerlynNo ratings yet

- Reaction Paper On Never AgainDocument2 pagesReaction Paper On Never AgainJohn Wilbert R. AretanoNo ratings yet

- Lecture 1Document19 pagesLecture 1abdirahmanNo ratings yet

- Executive Order No. 542Document2 pagesExecutive Order No. 542Jey RhyNo ratings yet

- 008 Republic v. BagtasDocument2 pages008 Republic v. BagtasLoren Bea TulalianNo ratings yet

- D 2749 - 92 R99 - Rdi3ndktotjsotlfmq - PDFDocument5 pagesD 2749 - 92 R99 - Rdi3ndktotjsotlfmq - PDFAndre CasteloNo ratings yet

- Team 6-PetitionerDocument20 pagesTeam 6-PetitionerSwetha JoscoNo ratings yet

- Civ1 4SCDE1920 Doctrines PersonsDocument47 pagesCiv1 4SCDE1920 Doctrines PersonsSpartansNo ratings yet

- BDC EoDocument6 pagesBDC EoVanessa Maravilla TabaneraNo ratings yet

- Faq Bulk Payment Via M2u BizDocument5 pagesFaq Bulk Payment Via M2u BizkavsabirNo ratings yet

- Globalization PuzzleDocument5 pagesGlobalization PuzzleMILDRED GAYADENNo ratings yet

- Cinematography ActDocument4 pagesCinematography Actvedanshasinghal -No ratings yet

- Ban Seng V Yap Pek Soo, (1967) 2 MLJ 156Document4 pagesBan Seng V Yap Pek Soo, (1967) 2 MLJ 156nroshaNo ratings yet

- Art 1 To 20 RPCDocument9 pagesArt 1 To 20 RPCAtty Ed Gibson BelarminoNo ratings yet

- Jemaa CircumstancesDocument32 pagesJemaa CircumstancesPheeb Hoggang0% (1)

- Chapter 3 - Legal, Ethical, and Professional Issues in Information SecurityDocument7 pagesChapter 3 - Legal, Ethical, and Professional Issues in Information SecurityAshura OsipNo ratings yet

- Hawk Company: Coy Commander - CDT 1C CorpuzDocument1 pageHawk Company: Coy Commander - CDT 1C CorpuzErnie PadernillaNo ratings yet

- 6 Privity of ContractDocument23 pages6 Privity of ContractCHUA JIATIENNo ratings yet

- SINDH Qaim Ali Shah AND SON IN LAW (DAMAD)Document2 pagesSINDH Qaim Ali Shah AND SON IN LAW (DAMAD)abad bookNo ratings yet

- Philtread Workers Union vs. ConfessorDocument2 pagesPhiltread Workers Union vs. Confessorjovani emaNo ratings yet

- Has The Advocate A Lien For His Fees On The Litigation Papers Entrusted To Him by His ClientDocument7 pagesHas The Advocate A Lien For His Fees On The Litigation Papers Entrusted To Him by His ClientprachiNo ratings yet

- Memorandum of Agreement SampleDocument3 pagesMemorandum of Agreement SampleFatMan87No ratings yet

- Payment of Gratuity Act, 1972 MCQDocument4 pagesPayment of Gratuity Act, 1972 MCQPratikNo ratings yet

- MCB ChallanDocument4 pagesMCB ChallanMuhammad Ilyas Shafiq71% (7)

- 03 - Bardillon v. Barangay Masili of Calamba, LagunaDocument2 pages03 - Bardillon v. Barangay Masili of Calamba, LagunaAngelicaNo ratings yet

- EITAI Lithium Battery Warranty File1Document6 pagesEITAI Lithium Battery Warranty File1Evan KaungMyatNo ratings yet