Download as pdf or txt

You might also like

- MAES London Pricing Sheet Lets Make It HereDocument3 pagesMAES London Pricing Sheet Lets Make It HereNimesh DesaiNo ratings yet

- Corporate Finance ModuleDocument153 pagesCorporate Finance ModuleKaso Muse100% (1)

- Differential Cost AnalysisDocument15 pagesDifferential Cost AnalysisIndu GuptaNo ratings yet

- Solution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 11Document44 pagesSolution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 11jasperkennedy089% (28)

- Objectives of Cost-Volume-Profit AnalysisDocument7 pagesObjectives of Cost-Volume-Profit AnalysisAnonNo ratings yet

- Solution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 10Document26 pagesSolution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 10jasperkennedy083% (36)

- CHAPTER 8 AnswerDocument14 pagesCHAPTER 8 AnswerKenncyNo ratings yet

- Chap 021Document19 pagesChap 021Neetu Rajaraman100% (1)

- CHAPTER FOUR Cost and MGMT ACCTDocument12 pagesCHAPTER FOUR Cost and MGMT ACCTFeleke TerefeNo ratings yet

- Corporate Finance Foundations Global Edition 15th Edition Block Solutions Manual 1Document60 pagesCorporate Finance Foundations Global Edition 15th Edition Block Solutions Manual 1janice100% (40)

- Solution Manual Managerial Accounting Hansen Mowen 8th Editions CH 11Document44 pagesSolution Manual Managerial Accounting Hansen Mowen 8th Editions CH 11kkamjonginnNo ratings yet

- UNIT Two CAMIIDocument10 pagesUNIT Two CAMIIMilkias MuseNo ratings yet

- Chapter 4 AnswerDocument23 pagesChapter 4 AnswerMethly Moreno100% (1)

- Cost-Volume-Profit Relationships: MANAGEMENT ACCOUNTING - Solutions ManualDocument36 pagesCost-Volume-Profit Relationships: MANAGEMENT ACCOUNTING - Solutions ManualStephanie LeeNo ratings yet

- Acct 620 Chapter 10Document42 pagesAcct 620 Chapter 10teddyh2oNo ratings yet

- Report CVP AnalysisDocument25 pagesReport CVP AnalysisSaief Dip100% (1)

- CHAPTER 14 - AnswerDocument17 pagesCHAPTER 14 - Answernash0% (2)

- CH 2Document16 pagesCH 2melat felekeNo ratings yet

- CM231. MAC (IL-II) Solution CMA May-2023 Exam.Document5 pagesCM231. MAC (IL-II) Solution CMA May-2023 Exam.Md FahadNo ratings yet

- Cost Ii CH 3Document8 pagesCost Ii CH 3TESFAY GEBRECHERKOSNo ratings yet

- Assignment Nos.3 Optimal Decision Using Marginal AnalysisDocument4 pagesAssignment Nos.3 Optimal Decision Using Marginal AnalysisKeziaNo ratings yet

- Cost Classification For Decision MakingDocument4 pagesCost Classification For Decision Makingkhurrams603572No ratings yet

- 3a Overheads Marginal CostingDocument19 pages3a Overheads Marginal Costingsylviekasembe4No ratings yet

- Flexible BudgetDocument15 pagesFlexible BudgetDawit AmahaNo ratings yet

- Cost-Volume-Profit Analysis (CVP) : Names of Sub-UnitsDocument12 pagesCost-Volume-Profit Analysis (CVP) : Names of Sub-Unitsmakouapenda2000No ratings yet

- Chapter 7: Cost-Volume-Profit Analysis Questions: Solutions ManualDocument49 pagesChapter 7: Cost-Volume-Profit Analysis Questions: Solutions ManualdarraNo ratings yet

- Introduction To Managerial Accounting Canadian Canadian 4th Edition Brewer Solutions ManualDocument72 pagesIntroduction To Managerial Accounting Canadian Canadian 4th Edition Brewer Solutions Manualcarlhawkinsjgwzqxabyt100% (24)

- Cost Profit Volume AnalysisDocument28 pagesCost Profit Volume AnalysisClarice LangitNo ratings yet

- 21decentralized Operations and Segment ReportingDocument130 pages21decentralized Operations and Segment ReportingAilene QuintoNo ratings yet

- Cost Analysis and EstimationDocument58 pagesCost Analysis and EstimationÖzge UzerNo ratings yet

- Chapter TwoDocument16 pagesChapter TwofiraolmosisabonkeNo ratings yet

- Manecon Chapter 6Document52 pagesManecon Chapter 6Allyssa GabrizaNo ratings yet

- Introduction To Managerial Accounting Canadian Canadian 4Th Edition Brewer Solutions Manual Full Chapter PDFDocument68 pagesIntroduction To Managerial Accounting Canadian Canadian 4Th Edition Brewer Solutions Manual Full Chapter PDFotisfarrerfjh2100% (11)

- 8 Marginal CostingDocument50 pages8 Marginal CostingBhagaban DasNo ratings yet

- Chapter 006Document75 pagesChapter 006Md. Abul HasnatNo ratings yet

- Flexible BudgetDocument15 pagesFlexible BudgetDawit AmahaNo ratings yet

- Profit Planning and Cost-Volume-Profit AnalysisDocument24 pagesProfit Planning and Cost-Volume-Profit AnalysisFallen Hieronymus50% (2)

- LNDefferencial AnalysisDocument13 pagesLNDefferencial AnalysiskajaleNo ratings yet

- CH - 6 - Relevant Costs and Decision MakingDocument44 pagesCH - 6 - Relevant Costs and Decision MakingNitish KhatanaNo ratings yet

- Informe FinanzasDocument8 pagesInforme FinanzasAlessandro SSJNo ratings yet

- Bilu Chap 3Document16 pagesBilu Chap 3borena extensionNo ratings yet

- Cost and Management Mod.Document111 pagesCost and Management Mod.Taresa AdugnaNo ratings yet

- Contribution Margin Definition - InvestopediaDocument6 pagesContribution Margin Definition - InvestopediaBob KaneNo ratings yet

- D23 PM Examiner's ReportDocument17 pagesD23 PM Examiner's ReportamayrablahblahNo ratings yet

- Unit 3 Acct312-UnlockedDocument21 pagesUnit 3 Acct312-UnlockedTilahun GirmaNo ratings yet

- Decision Making TechniquesDocument16 pagesDecision Making TechniquesKathlynJoySalazarNo ratings yet

- Module 2 Cost-Volume-Profit AnalysisDocument73 pagesModule 2 Cost-Volume-Profit Analysiscurly030125No ratings yet

- Chapter IVDocument10 pagesChapter IVeyasuNo ratings yet

- Cost II Chapter-OneDocument10 pagesCost II Chapter-OneSemiraNo ratings yet

- Differential Cost AnalysisDocument37 pagesDifferential Cost AnalysisJr RendonNo ratings yet

- Chapter 4 Answer Cost AccountingDocument19 pagesChapter 4 Answer Cost AccountingJuline Ashley A CarballoNo ratings yet

- Differential Cost and Differential RevenueDocument4 pagesDifferential Cost and Differential RevenueasadshakirNo ratings yet

- Module 5 (Chapter 24) - Managing Productivity & MKTG EffectivenessDocument28 pagesModule 5 (Chapter 24) - Managing Productivity & MKTG Effectivenessdakis cherishjoyfNo ratings yet

- 012 CAMIST CH10 Amndd 2 HS PP 247-276 Branded BW SecDocument31 pages012 CAMIST CH10 Amndd 2 HS PP 247-276 Branded BW Secsumaiazerin101No ratings yet

- 006 Camist Ch04 Amndd Hs PP 79-102 Branded BW RP SecDocument25 pages006 Camist Ch04 Amndd Hs PP 79-102 Branded BW RP SecMd Salahuddin HowladerNo ratings yet

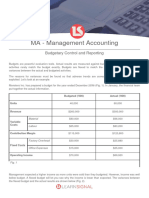

- 69 Budgetary Control and Reporting NotesDocument7 pages69 Budgetary Control and Reporting Notesgetcultured69No ratings yet

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- BofA Global Research-Commodity Strategist Year Ahead 2023 Commodity Outlook-99278411Document96 pagesBofA Global Research-Commodity Strategist Year Ahead 2023 Commodity Outlook-99278411杨舒No ratings yet

- MCI Steel Price Projections ReportDocument29 pagesMCI Steel Price Projections ReportAndrzej M Kotas100% (1)

- What Is A Resort?: The Impact of Pricing To Tourism of Resorts in Santiago CityDocument66 pagesWhat Is A Resort?: The Impact of Pricing To Tourism of Resorts in Santiago CityMaureen Li GuingabNo ratings yet

- Ass 1Document6 pagesAss 1Shubham PathakNo ratings yet

- India Pesticides Limited: An ISO 9001:2015, 1 2015,45001 2018 and 10002:2018 CIN No. U24112 UP1984PLC006894Document20 pagesIndia Pesticides Limited: An ISO 9001:2015, 1 2015,45001 2018 and 10002:2018 CIN No. U24112 UP1984PLC006894Pãräs PhútélàNo ratings yet

- Fin254 Chapter 6Document18 pagesFin254 Chapter 6Wasif KhanNo ratings yet

- Chapter Six: Social Cost Benefit Analysis (Scba)Document47 pagesChapter Six: Social Cost Benefit Analysis (Scba)yimer100% (1)

- SELF CHECK ACTIVITY QD and QSDocument3 pagesSELF CHECK ACTIVITY QD and QSJohn Jerome BasmayorNo ratings yet

- Chapter 13 Dimensions of Marketing Strategy: ObjectivesDocument23 pagesChapter 13 Dimensions of Marketing Strategy: ObjectivesAhmad ArdiansyahNo ratings yet

- Blue BK Manc PDFDocument300 pagesBlue BK Manc PDFNyemwerai MuterereNo ratings yet

- THREE Bonds and Stock Valuation.. STOCKDocument19 pagesTHREE Bonds and Stock Valuation.. STOCKRaasu KuttyNo ratings yet

- Fundamental Analysis Models in Financial Markets: Review of PaperDocument3 pagesFundamental Analysis Models in Financial Markets: Review of PaperKhushboo NagpalNo ratings yet

- Solved TS Police SI Mains 2018 Arithmetic and Reasoning Paper With SolutionsDocument54 pagesSolved TS Police SI Mains 2018 Arithmetic and Reasoning Paper With SolutionsNare ChallagondlaNo ratings yet

- EY&AuraArt ArtValuationDocument12 pagesEY&AuraArt ArtValuationRishiraj SethiNo ratings yet

- Operation Management Chapter 2: Product DesignDocument2 pagesOperation Management Chapter 2: Product DesignSyahira RamliNo ratings yet

- Marketing Project Tarang: Company: Engro Foods LimitedDocument19 pagesMarketing Project Tarang: Company: Engro Foods LimitedMuhammad MudassarNo ratings yet

- BHMH2002 - QP - V1 - B (Formatted) (Signed)Document9 pagesBHMH2002 - QP - V1 - B (Formatted) (Signed)andy wongNo ratings yet

- Candelario The Pricing of ServicesDocument5 pagesCandelario The Pricing of ServicesGrace MarasiganNo ratings yet

- MGT 368 Final ExamDocument12 pagesMGT 368 Final ExamNaushin Fariha Jalal 1821146630No ratings yet

- 1.5 WorksheetDocument5 pages1.5 WorksheetZid RangerNo ratings yet

- Introduction To DerivativesDocument34 pagesIntroduction To Derivativessalil1285100% (2)

- CB - Assignment 2Document4 pagesCB - Assignment 2Jaison JosephNo ratings yet

- MQ 1 Inventories Ak PDFDocument4 pagesMQ 1 Inventories Ak PDFJuliana ChengNo ratings yet

- How Can Samsung Compete With Companies Like Apple and Google in The Phone MarketDocument3 pagesHow Can Samsung Compete With Companies Like Apple and Google in The Phone MarketPamela SantosNo ratings yet

- DividendsDocument3 pagesDividendsClaudia ChoiNo ratings yet

- Assignment 5Document4 pagesAssignment 5Shin SobejanaNo ratings yet

- Disadvantages of Cause MarketingDocument3 pagesDisadvantages of Cause MarketingTusharNo ratings yet

- Option Valuation - DamodaranDocument82 pagesOption Valuation - DamodaranIA M.No ratings yet