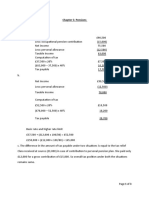

Week 3 - Extension Questions (Solutions)

Week 3 - Extension Questions (Solutions)

You might also like

- ACC 3013 - FWA - Revision - 202110Document14 pagesACC 3013 - FWA - Revision - 202110falnuaimi001No ratings yet

- Indoor Soccer Facility Business Plan1 2Document29 pagesIndoor Soccer Facility Business Plan1 2Ihsan QolbuNo ratings yet

- Rules Governing Redeemable and Treasury SharesDocument2 pagesRules Governing Redeemable and Treasury SharesTosca Mansujeto50% (2)

- SwissBorg Pitch Deck (English)Document19 pagesSwissBorg Pitch Deck (English)Suzie EvansNo ratings yet

- Chapter 2 - SolutionDocument12 pagesChapter 2 - SolutionAk AlNo ratings yet

- TXUK 2019 MarJun ADocument11 pagesTXUK 2019 MarJun AmdNo ratings yet

- Atxuk Sample Marjun 2019 ADocument10 pagesAtxuk Sample Marjun 2019 AAdam KhanNo ratings yet

- MJ17 - Hybrids - P6UK - AMENDED AnswersDocument12 pagesMJ17 - Hybrids - P6UK - AMENDED AnswersHassan jalilNo ratings yet

- f6 ANSDocument14 pagesf6 ANSSarad KharelNo ratings yet

- CGT 1Document25 pagesCGT 1Donald HollistNo ratings yet

- F6 Qbda PDFDocument36 pagesF6 Qbda PDFqqqNo ratings yet

- Capital Gains Tax - AnswersDocument10 pagesCapital Gains Tax - AnswersRai Ali WafaNo ratings yet

- F6mys 2015 Dec ADocument8 pagesF6mys 2015 Dec ABryan EngNo ratings yet

- ACC 3013 Taxation Revision - TEST 2Document4 pagesACC 3013 Taxation Revision - TEST 2falnuaimi001No ratings yet

- P6uk 2018 Jun ADocument11 pagesP6uk 2018 Jun ADilawar HayatNo ratings yet

- Ronald - Answer (TX UK)Document2 pagesRonald - Answer (TX UK)ysaneechar29No ratings yet

- Week 4 - Extension Question SolutionsDocument10 pagesWeek 4 - Extension Question Solutionsichika20010201No ratings yet

- Acc 3013 - Fwa Revision AnswersDocument15 pagesAcc 3013 - Fwa Revision Answersfalnuaimi001No ratings yet

- F6mys 2016 Jun A Hybrid PDFDocument9 pagesF6mys 2016 Jun A Hybrid PDFsahrasaqsdNo ratings yet

- Chapter 5: Pensions Question 5.1-AnswerDocument3 pagesChapter 5: Pensions Question 5.1-AnswerAk AlNo ratings yet

- R2. TAX ML Solution CMA January 2022 ExaminationDocument6 pagesR2. TAX ML Solution CMA January 2022 ExaminationPavel DhakaNo ratings yet

- Answers: Tuition (Course) ExaminationDocument16 pagesAnswers: Tuition (Course) ExaminationHussein SeetalNo ratings yet

- Initial Plc-Jasons Employment Income For The Tax Year 22/23Document9 pagesInitial Plc-Jasons Employment Income For The Tax Year 22/23akramkiller0No ratings yet

- IFRS Week 6Document4 pagesIFRS Week 6AleksandraNo ratings yet

- Higher SkillsDocument14 pagesHigher SkillsArun ThomasNo ratings yet

- Finance Act 2020 - ACCA GlobalDocument65 pagesFinance Act 2020 - ACCA GlobalRaza AliNo ratings yet

- Model Solution: Page 1 of 6Document6 pagesModel Solution: Page 1 of 6ShuvonathNo ratings yet

- F6 AnsDocument9 pagesF6 AnsRaza AliNo ratings yet

- MAAC 502 Question Bank 2019Document32 pagesMAAC 502 Question Bank 2019Stephen NdambakuwaNo ratings yet

- Taxation AccountingDocument10 pagesTaxation Accountingjanahh.omNo ratings yet

- APT Tax AssignmentDocument11 pagesAPT Tax AssignmentMalik JavidNo ratings yet

- F2 Past Paper - Ans12-2006Document8 pagesF2 Past Paper - Ans12-2006ArsalanACCANo ratings yet

- The Difference in Future Taxable AmountsDocument2 pagesThe Difference in Future Taxable AmountsThư LuyệnNo ratings yet

- Txmys 2022 Dec ADocument10 pagesTxmys 2022 Dec Amuhammadafifi126No ratings yet

- 1 2 2006 Jun ADocument8 pages1 2 2006 Jun AcyoteditorNo ratings yet

- INCOME TAX AssignmentDocument5 pagesINCOME TAX AssignmentShakib studentNo ratings yet

- R2.TAXML Solution CMA September 2022 Exam.Document5 pagesR2.TAXML Solution CMA September 2022 Exam.Raziur RahmanNo ratings yet

- Chapter 19Document4 pagesChapter 19Bella RonahNo ratings yet

- ICAEW - Tax - Mini Test 3 - STDDocument6 pagesICAEW - Tax - Mini Test 3 - STDlinhdinhphuong02No ratings yet

- Trick TradersDocument2 pagesTrick Tradersrethaxaba82No ratings yet

- Week 3 - Extension QuestionsDocument1 pageWeek 3 - Extension Questionsichika20010201No ratings yet

- Finance Act 2020 - ACCA GlobalDocument62 pagesFinance Act 2020 - ACCA GlobalhfdghdhNo ratings yet

- F6 - IPRO - 2021 - Mock 1 - AnswersDocument16 pagesF6 - IPRO - 2021 - Mock 1 - AnswersHussein SeetalNo ratings yet

- Tax-week12 test bankDocument3 pagesTax-week12 test bankzeinab.iaems.researchNo ratings yet

- S20 TX ROM Sample AnswersDocument8 pagesS20 TX ROM Sample AnswersKAH MENG KAMNo ratings yet

- AC3097 Management Accounting - Preliminary Paper 2015 - AnswersDocument10 pagesAC3097 Management Accounting - Preliminary Paper 2015 - AnswersPei TingNo ratings yet

- CT Qs Day5Document4 pagesCT Qs Day5Jonas KareraNo ratings yet

- Estate ExercisesDocument12 pagesEstate ExercisesAmira SyahiraNo ratings yet

- ACC708 - L1 Class AcctivityDocument3 pagesACC708 - L1 Class AcctivityJake LukmistNo ratings yet

- December 2010 TC10BADocument12 pagesDecember 2010 TC10BAkalowekamoNo ratings yet

- F6RUS AnsDocument9 pagesF6RUS AnsСветлана КозловаNo ratings yet

- Andiam: January 2, 2019Document5 pagesAndiam: January 2, 2019Avox EverdeenNo ratings yet

- Past Exam QuestionDocument3 pagesPast Exam QuestionYến Hoàng HảiNo ratings yet

- STT - Mock - Test - S-24 - Suggested AnswersDocument8 pagesSTT - Mock - Test - S-24 - Suggested AnswersabdullahNo ratings yet

- SolutionDocument4 pagesSolutionIGO SAUCENo ratings yet

- Txmwi 2018 Dec ADocument7 pagesTxmwi 2018 Dec AangaNo ratings yet

- AnswersDocument5 pagesAnswershfdghdhNo ratings yet

- Atxuk m20 ADocument10 pagesAtxuk m20 Apaul sagudaNo ratings yet

- TX-CYP Dec 21 AnswersDocument8 pagesTX-CYP Dec 21 AnswersKAM JIA LINGNo ratings yet

- ENG Salary CalculatorDocument4 pagesENG Salary CalculatorPankaj MittalNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Finding Balance 2023: Benchmarking Performance and Building Climate Resilience in Pacific State-Owned EnterprisesFrom EverandFinding Balance 2023: Benchmarking Performance and Building Climate Resilience in Pacific State-Owned EnterprisesNo ratings yet

- Week 3 - Lecture Illustration SolutionDocument2 pagesWeek 3 - Lecture Illustration Solutionichika20010201No ratings yet

- Week 4 - Extension Question SolutionsDocument10 pagesWeek 4 - Extension Question Solutionsichika20010201No ratings yet

- Week 3 - Lecture IllustrationDocument2 pagesWeek 3 - Lecture Illustrationichika20010201No ratings yet

- Week 3 - Extension QuestionsDocument1 pageWeek 3 - Extension Questionsichika20010201No ratings yet

- Mary The Queen College (Pampanga), Inc.: JASA, San Matias, Guagua, PampangaDocument11 pagesMary The Queen College (Pampanga), Inc.: JASA, San Matias, Guagua, PampangaAllain GuanlaoNo ratings yet

- FCCB in IndiaDocument24 pagesFCCB in IndiaSana Riyaz KhalifeNo ratings yet

- Methodology of The Moscow Exchange Equity Indices CalculationDocument30 pagesMethodology of The Moscow Exchange Equity Indices CalculationJimmyNo ratings yet

- Stone Arch CapitalDocument15 pagesStone Arch CapitalPerty24No ratings yet

- Manvendra Singh - Bajaj FinanceDocument3 pagesManvendra Singh - Bajaj FinanceManvendra SinghNo ratings yet

- Harish Mba ProjectDocument72 pagesHarish Mba ProjectchaluvadiinNo ratings yet

- Lec 02 - Organisational StructuresDocument3 pagesLec 02 - Organisational StructuresRamesh BabuNo ratings yet

- Accounting Concepts and ConventionsDocument5 pagesAccounting Concepts and ConventionsAMIN BUHARI ABDUL KHADERNo ratings yet

- Financial StatementsDocument2 pagesFinancial StatementsRjoshua PlaylistNo ratings yet

- Account Title PR Trial Balance Dr. CRDocument15 pagesAccount Title PR Trial Balance Dr. CRJEERAPA KHANPHETNo ratings yet

- For Session DTD 5th Sep by CA Alok Garg PDFDocument46 pagesFor Session DTD 5th Sep by CA Alok Garg PDFLakshmi Narayana Murthy KapavarapuNo ratings yet

- Detailed Project Report On Establishment of Rural Home-Stay Tourism For A Tourism Cooperative SocietyDocument20 pagesDetailed Project Report On Establishment of Rural Home-Stay Tourism For A Tourism Cooperative SocietysauravNo ratings yet

- Presentation On CIBN (Group One)Document6 pagesPresentation On CIBN (Group One)chinonyebeatrice9No ratings yet

- Stock ValuationDocument17 pagesStock Valuationsankha80No ratings yet

- Consent Letter From SBADocument1 pageConsent Letter From SBAArindom Ray ChaudhuriNo ratings yet

- Postal Submission ListDocument1 pagePostal Submission ListBibekananda RoyNo ratings yet

- Practice Questions - Cost of Capital - 2Document11 pagesPractice Questions - Cost of Capital - 2arun babuNo ratings yet

- We Buy Houses ST PetersburgDocument5 pagesWe Buy Houses ST Petersburglaravel421No ratings yet

- Marshall - Framework For Assessing Risk MarginsDocument43 pagesMarshall - Framework For Assessing Risk MarginsGagan SawhneyNo ratings yet

- Dwnload Full Company Accounting Australia New Zealand 5th Edition Jubb Test Bank PDFDocument11 pagesDwnload Full Company Accounting Australia New Zealand 5th Edition Jubb Test Bank PDFnevahonyumptewa683100% (19)

- Benefits of Post Office Savings AccountsDocument7 pagesBenefits of Post Office Savings Accounts2K22/BAE/79 KESHAV GARGNo ratings yet

- Mock 01 001Document28 pagesMock 01 001masud khanNo ratings yet

- K&E Draft 01/26/2023 Privileged and Confidential Attorney Work ProductDocument14 pagesK&E Draft 01/26/2023 Privileged and Confidential Attorney Work ProductsperlingreichNo ratings yet

- ECON 203 - Midterm - 2010F - AncaAlecsandru - Solution PDFDocument6 pagesECON 203 - Midterm - 2010F - AncaAlecsandru - Solution PDFexamkillerNo ratings yet

- Tax Return ScribdDocument5 pagesTax Return ScribdYvonne TanNo ratings yet

- Income From House PropertyDocument3 pagesIncome From House PropertySneha PotekarNo ratings yet

- Laporan Keuangan UnileverDocument92 pagesLaporan Keuangan UnileverRESTA SUJONONo ratings yet

Download as docx, pdf, or txt

You might also like

- ACC 3013 - FWA - Revision - 202110Document14 pagesACC 3013 - FWA - Revision - 202110falnuaimi001No ratings yet

- Indoor Soccer Facility Business Plan1 2Document29 pagesIndoor Soccer Facility Business Plan1 2Ihsan QolbuNo ratings yet

- Rules Governing Redeemable and Treasury SharesDocument2 pagesRules Governing Redeemable and Treasury SharesTosca Mansujeto50% (2)

- SwissBorg Pitch Deck (English)Document19 pagesSwissBorg Pitch Deck (English)Suzie EvansNo ratings yet

- Chapter 2 - SolutionDocument12 pagesChapter 2 - SolutionAk AlNo ratings yet

- TXUK 2019 MarJun ADocument11 pagesTXUK 2019 MarJun AmdNo ratings yet

- Atxuk Sample Marjun 2019 ADocument10 pagesAtxuk Sample Marjun 2019 AAdam KhanNo ratings yet

- MJ17 - Hybrids - P6UK - AMENDED AnswersDocument12 pagesMJ17 - Hybrids - P6UK - AMENDED AnswersHassan jalilNo ratings yet

- f6 ANSDocument14 pagesf6 ANSSarad KharelNo ratings yet

- CGT 1Document25 pagesCGT 1Donald HollistNo ratings yet

- F6 Qbda PDFDocument36 pagesF6 Qbda PDFqqqNo ratings yet

- Capital Gains Tax - AnswersDocument10 pagesCapital Gains Tax - AnswersRai Ali WafaNo ratings yet

- F6mys 2015 Dec ADocument8 pagesF6mys 2015 Dec ABryan EngNo ratings yet

- ACC 3013 Taxation Revision - TEST 2Document4 pagesACC 3013 Taxation Revision - TEST 2falnuaimi001No ratings yet

- P6uk 2018 Jun ADocument11 pagesP6uk 2018 Jun ADilawar HayatNo ratings yet

- Ronald - Answer (TX UK)Document2 pagesRonald - Answer (TX UK)ysaneechar29No ratings yet

- Week 4 - Extension Question SolutionsDocument10 pagesWeek 4 - Extension Question Solutionsichika20010201No ratings yet

- Acc 3013 - Fwa Revision AnswersDocument15 pagesAcc 3013 - Fwa Revision Answersfalnuaimi001No ratings yet

- F6mys 2016 Jun A Hybrid PDFDocument9 pagesF6mys 2016 Jun A Hybrid PDFsahrasaqsdNo ratings yet

- Chapter 5: Pensions Question 5.1-AnswerDocument3 pagesChapter 5: Pensions Question 5.1-AnswerAk AlNo ratings yet

- R2. TAX ML Solution CMA January 2022 ExaminationDocument6 pagesR2. TAX ML Solution CMA January 2022 ExaminationPavel DhakaNo ratings yet

- Answers: Tuition (Course) ExaminationDocument16 pagesAnswers: Tuition (Course) ExaminationHussein SeetalNo ratings yet

- Initial Plc-Jasons Employment Income For The Tax Year 22/23Document9 pagesInitial Plc-Jasons Employment Income For The Tax Year 22/23akramkiller0No ratings yet

- IFRS Week 6Document4 pagesIFRS Week 6AleksandraNo ratings yet

- Higher SkillsDocument14 pagesHigher SkillsArun ThomasNo ratings yet

- Finance Act 2020 - ACCA GlobalDocument65 pagesFinance Act 2020 - ACCA GlobalRaza AliNo ratings yet

- Model Solution: Page 1 of 6Document6 pagesModel Solution: Page 1 of 6ShuvonathNo ratings yet

- F6 AnsDocument9 pagesF6 AnsRaza AliNo ratings yet

- MAAC 502 Question Bank 2019Document32 pagesMAAC 502 Question Bank 2019Stephen NdambakuwaNo ratings yet

- Taxation AccountingDocument10 pagesTaxation Accountingjanahh.omNo ratings yet

- APT Tax AssignmentDocument11 pagesAPT Tax AssignmentMalik JavidNo ratings yet

- F2 Past Paper - Ans12-2006Document8 pagesF2 Past Paper - Ans12-2006ArsalanACCANo ratings yet

- The Difference in Future Taxable AmountsDocument2 pagesThe Difference in Future Taxable AmountsThư LuyệnNo ratings yet

- Txmys 2022 Dec ADocument10 pagesTxmys 2022 Dec Amuhammadafifi126No ratings yet

- 1 2 2006 Jun ADocument8 pages1 2 2006 Jun AcyoteditorNo ratings yet

- INCOME TAX AssignmentDocument5 pagesINCOME TAX AssignmentShakib studentNo ratings yet

- R2.TAXML Solution CMA September 2022 Exam.Document5 pagesR2.TAXML Solution CMA September 2022 Exam.Raziur RahmanNo ratings yet

- Chapter 19Document4 pagesChapter 19Bella RonahNo ratings yet

- ICAEW - Tax - Mini Test 3 - STDDocument6 pagesICAEW - Tax - Mini Test 3 - STDlinhdinhphuong02No ratings yet

- Trick TradersDocument2 pagesTrick Tradersrethaxaba82No ratings yet

- Week 3 - Extension QuestionsDocument1 pageWeek 3 - Extension Questionsichika20010201No ratings yet

- Finance Act 2020 - ACCA GlobalDocument62 pagesFinance Act 2020 - ACCA GlobalhfdghdhNo ratings yet

- F6 - IPRO - 2021 - Mock 1 - AnswersDocument16 pagesF6 - IPRO - 2021 - Mock 1 - AnswersHussein SeetalNo ratings yet

- Tax-week12 test bankDocument3 pagesTax-week12 test bankzeinab.iaems.researchNo ratings yet

- S20 TX ROM Sample AnswersDocument8 pagesS20 TX ROM Sample AnswersKAH MENG KAMNo ratings yet

- AC3097 Management Accounting - Preliminary Paper 2015 - AnswersDocument10 pagesAC3097 Management Accounting - Preliminary Paper 2015 - AnswersPei TingNo ratings yet

- CT Qs Day5Document4 pagesCT Qs Day5Jonas KareraNo ratings yet

- Estate ExercisesDocument12 pagesEstate ExercisesAmira SyahiraNo ratings yet

- ACC708 - L1 Class AcctivityDocument3 pagesACC708 - L1 Class AcctivityJake LukmistNo ratings yet

- December 2010 TC10BADocument12 pagesDecember 2010 TC10BAkalowekamoNo ratings yet

- F6RUS AnsDocument9 pagesF6RUS AnsСветлана КозловаNo ratings yet

- Andiam: January 2, 2019Document5 pagesAndiam: January 2, 2019Avox EverdeenNo ratings yet

- Past Exam QuestionDocument3 pagesPast Exam QuestionYến Hoàng HảiNo ratings yet

- STT - Mock - Test - S-24 - Suggested AnswersDocument8 pagesSTT - Mock - Test - S-24 - Suggested AnswersabdullahNo ratings yet

- SolutionDocument4 pagesSolutionIGO SAUCENo ratings yet

- Txmwi 2018 Dec ADocument7 pagesTxmwi 2018 Dec AangaNo ratings yet

- AnswersDocument5 pagesAnswershfdghdhNo ratings yet

- Atxuk m20 ADocument10 pagesAtxuk m20 Apaul sagudaNo ratings yet

- TX-CYP Dec 21 AnswersDocument8 pagesTX-CYP Dec 21 AnswersKAM JIA LINGNo ratings yet

- ENG Salary CalculatorDocument4 pagesENG Salary CalculatorPankaj MittalNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Finding Balance 2023: Benchmarking Performance and Building Climate Resilience in Pacific State-Owned EnterprisesFrom EverandFinding Balance 2023: Benchmarking Performance and Building Climate Resilience in Pacific State-Owned EnterprisesNo ratings yet

- Week 3 - Lecture Illustration SolutionDocument2 pagesWeek 3 - Lecture Illustration Solutionichika20010201No ratings yet

- Week 4 - Extension Question SolutionsDocument10 pagesWeek 4 - Extension Question Solutionsichika20010201No ratings yet

- Week 3 - Lecture IllustrationDocument2 pagesWeek 3 - Lecture Illustrationichika20010201No ratings yet

- Week 3 - Extension QuestionsDocument1 pageWeek 3 - Extension Questionsichika20010201No ratings yet

- Mary The Queen College (Pampanga), Inc.: JASA, San Matias, Guagua, PampangaDocument11 pagesMary The Queen College (Pampanga), Inc.: JASA, San Matias, Guagua, PampangaAllain GuanlaoNo ratings yet

- FCCB in IndiaDocument24 pagesFCCB in IndiaSana Riyaz KhalifeNo ratings yet

- Methodology of The Moscow Exchange Equity Indices CalculationDocument30 pagesMethodology of The Moscow Exchange Equity Indices CalculationJimmyNo ratings yet

- Stone Arch CapitalDocument15 pagesStone Arch CapitalPerty24No ratings yet

- Manvendra Singh - Bajaj FinanceDocument3 pagesManvendra Singh - Bajaj FinanceManvendra SinghNo ratings yet

- Harish Mba ProjectDocument72 pagesHarish Mba ProjectchaluvadiinNo ratings yet

- Lec 02 - Organisational StructuresDocument3 pagesLec 02 - Organisational StructuresRamesh BabuNo ratings yet

- Accounting Concepts and ConventionsDocument5 pagesAccounting Concepts and ConventionsAMIN BUHARI ABDUL KHADERNo ratings yet

- Financial StatementsDocument2 pagesFinancial StatementsRjoshua PlaylistNo ratings yet

- Account Title PR Trial Balance Dr. CRDocument15 pagesAccount Title PR Trial Balance Dr. CRJEERAPA KHANPHETNo ratings yet

- For Session DTD 5th Sep by CA Alok Garg PDFDocument46 pagesFor Session DTD 5th Sep by CA Alok Garg PDFLakshmi Narayana Murthy KapavarapuNo ratings yet

- Detailed Project Report On Establishment of Rural Home-Stay Tourism For A Tourism Cooperative SocietyDocument20 pagesDetailed Project Report On Establishment of Rural Home-Stay Tourism For A Tourism Cooperative SocietysauravNo ratings yet

- Presentation On CIBN (Group One)Document6 pagesPresentation On CIBN (Group One)chinonyebeatrice9No ratings yet

- Stock ValuationDocument17 pagesStock Valuationsankha80No ratings yet

- Consent Letter From SBADocument1 pageConsent Letter From SBAArindom Ray ChaudhuriNo ratings yet

- Postal Submission ListDocument1 pagePostal Submission ListBibekananda RoyNo ratings yet

- Practice Questions - Cost of Capital - 2Document11 pagesPractice Questions - Cost of Capital - 2arun babuNo ratings yet

- We Buy Houses ST PetersburgDocument5 pagesWe Buy Houses ST Petersburglaravel421No ratings yet

- Marshall - Framework For Assessing Risk MarginsDocument43 pagesMarshall - Framework For Assessing Risk MarginsGagan SawhneyNo ratings yet

- Dwnload Full Company Accounting Australia New Zealand 5th Edition Jubb Test Bank PDFDocument11 pagesDwnload Full Company Accounting Australia New Zealand 5th Edition Jubb Test Bank PDFnevahonyumptewa683100% (19)

- Benefits of Post Office Savings AccountsDocument7 pagesBenefits of Post Office Savings Accounts2K22/BAE/79 KESHAV GARGNo ratings yet

- Mock 01 001Document28 pagesMock 01 001masud khanNo ratings yet

- K&E Draft 01/26/2023 Privileged and Confidential Attorney Work ProductDocument14 pagesK&E Draft 01/26/2023 Privileged and Confidential Attorney Work ProductsperlingreichNo ratings yet

- ECON 203 - Midterm - 2010F - AncaAlecsandru - Solution PDFDocument6 pagesECON 203 - Midterm - 2010F - AncaAlecsandru - Solution PDFexamkillerNo ratings yet

- Tax Return ScribdDocument5 pagesTax Return ScribdYvonne TanNo ratings yet

- Income From House PropertyDocument3 pagesIncome From House PropertySneha PotekarNo ratings yet

- Laporan Keuangan UnileverDocument92 pagesLaporan Keuangan UnileverRESTA SUJONONo ratings yet