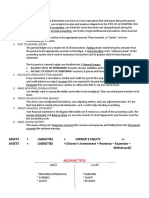

Accounts Receivable

Accounts Receivable

You might also like

- Understanding Financial Statements Solutions Chapter 2Document30 pagesUnderstanding Financial Statements Solutions Chapter 2adam_garcia_81100% (3)

- IM - Updates in Financial Reporting Standards (ACCO 40023) - Cash To AccrualDocument13 pagesIM - Updates in Financial Reporting Standards (ACCO 40023) - Cash To AccrualJasmine100% (2)

- Chapter 10 Income From Business or ProfessionDocument14 pagesChapter 10 Income From Business or ProfessionMd. Rayhanul IslamNo ratings yet

- Chap7 Notes Intermediate Accounting KiesoDocument8 pagesChap7 Notes Intermediate Accounting Kiesoangelbear2577100% (1)

- Tax Test Bank TheoryDocument6 pagesTax Test Bank TheoryXtian de Vera100% (1)

- Chapter 4 Lecture Trade and Non Trade Receivables Part 1 StudentDocument3 pagesChapter 4 Lecture Trade and Non Trade Receivables Part 1 StudentAshlene CruzNo ratings yet

- XFARDocument14 pagesXFARRIZA SAMPAGANo ratings yet

- Audit On ReceivablesDocument19 pagesAudit On ReceivablesPaupauNo ratings yet

- AR AR FinancingDocument34 pagesAR AR FinancingDannis Anne RegajalNo ratings yet

- CKSIAN-Accounting Cycle Hacks pt2Document5 pagesCKSIAN-Accounting Cycle Hacks pt2fhfdhNo ratings yet

- Receivable Financing: Quick Review!Document9 pagesReceivable Financing: Quick Review!Barbie BleuNo ratings yet

- Adjusting Entries. Bad Debts and DepreciationDocument7 pagesAdjusting Entries. Bad Debts and DepreciationShiela LanadoNo ratings yet

- Accounting 471: Class 11Document66 pagesAccounting 471: Class 11CORES LYRICSNo ratings yet

- Notes On Week 3Document11 pagesNotes On Week 3Christy CaneteNo ratings yet

- CH 9 - Intermediate AccountingDocument28 pagesCH 9 - Intermediate Accountinghana osmanNo ratings yet

- Receivables: Created By: Origen, Janiene / Palma, Jennelyn, Cabi Gting, Ela. Artiza, EmmanDocument44 pagesReceivables: Created By: Origen, Janiene / Palma, Jennelyn, Cabi Gting, Ela. Artiza, Emmandeleonjaniene bsaNo ratings yet

- Chapter 5 Estimation of Doubtful AccountsDocument5 pagesChapter 5 Estimation of Doubtful AccountsPam LlanetaNo ratings yet

- 04 Trade Accounts ReceivableDocument7 pages04 Trade Accounts Receivablesharielles /No ratings yet

- IA 1 - 4 ReceivablesDocument9 pagesIA 1 - 4 ReceivablesVJ MacaspacNo ratings yet

- CMA Part 1 Unit 2 (2021)Document116 pagesCMA Part 1 Unit 2 (2021)athul16203682No ratings yet

- Accounting Cycle HacksDocument14 pagesAccounting Cycle HacksAnonymous mnAAXLkYQCNo ratings yet

- Accounts Receivable and Estimating Doubtful AccountsDocument7 pagesAccounts Receivable and Estimating Doubtful AccountsMiles SantosNo ratings yet

- ReceivablesDocument20 pagesReceivablesGemmalyn FolguerasNo ratings yet

- Activity 5 1Document13 pagesActivity 5 1Trice DomingoNo ratings yet

- POA Topic 12Document3 pagesPOA Topic 12Ian ChanNo ratings yet

- Sales Order ProcessingDocument9 pagesSales Order ProcessingKRIS ANNE SAMUDIONo ratings yet

- Quiz 10Document2 pagesQuiz 10andreajade.cawaya10No ratings yet

- Accounting For Receivables: Learning ObjectivesDocument68 pagesAccounting For Receivables: Learning ObjectivesDeeb. DeebNo ratings yet

- Adjusting Entries and Merchandising BusinessDocument5 pagesAdjusting Entries and Merchandising BusinessLing lingNo ratings yet

- 04 Trade Accounts ReceivableDocument7 pages04 Trade Accounts ReceivableKhen HannaNo ratings yet

- Handout 04 Trade ARDocument7 pagesHandout 04 Trade ARMARY GRACE VARGASNo ratings yet

- Control Account Revision NotesDocument30 pagesControl Account Revision NotesOckouri BarnesNo ratings yet

- INTACC 1 - REVIEWER - MIDTERMS (Receivables)Document3 pagesINTACC 1 - REVIEWER - MIDTERMS (Receivables)olerianaryzzsc.56No ratings yet

- CH.8 Notes - Accounting For ReceivablesDocument19 pagesCH.8 Notes - Accounting For ReceivablesLEEN hashemNo ratings yet

- Sample - Monetary Current Assets and LiabilitiesDocument2 pagesSample - Monetary Current Assets and LiabilitiesAdmin - At Least Know ThisNo ratings yet

- Section 7 CONTROL SYSTEMDocument42 pagesSection 7 CONTROL SYSTEMWilliNo ratings yet

- Ffa W12343Document22 pagesFfa W12343DaddyNo ratings yet

- Accounting and Finance BankersDocument68 pagesAccounting and Finance BankersNamita SharmaNo ratings yet

- AR and Doubtful Accounts - NotesDocument5 pagesAR and Doubtful Accounts - NotesTEOPE, EMERLIZA DE CASTRONo ratings yet

- AT Least: CPA Exam Review 2018Document6 pagesAT Least: CPA Exam Review 2018At Least Know This CPANo ratings yet

- RECEIVABLE - Are Financial Assets That Represent A Contractual Right To Receive Cash or AnotherDocument22 pagesRECEIVABLE - Are Financial Assets That Represent A Contractual Right To Receive Cash or AnotherSB19 ChicKENNo ratings yet

- Page 51 From Audit Akm CompreDocument1 pagePage 51 From Audit Akm CompreGaby VionidyaNo ratings yet

- Page 51 From Audit Akm CompreDocument1 pagePage 51 From Audit Akm CompreGaby VionidyaNo ratings yet

- TOPIC 4 Principle - Of.double - EntryDocument4 pagesTOPIC 4 Principle - Of.double - EntryNurul Ain Binti Abd RahimNo ratings yet

- Z Chapter 4 The Revenue Cycle TamanoDocument4 pagesZ Chapter 4 The Revenue Cycle TamanoBrylle TamanoNo ratings yet

- Accounts ReceivableDocument23 pagesAccounts ReceivableAbby MendozaNo ratings yet

- BUSI 2001 Int. AccountingDocument3 pagesBUSI 2001 Int. AccountingJoshNo ratings yet

- Receivable FinancingDocument15 pagesReceivable FinancingArt EezyNo ratings yet

- 04 Accounts Receivable Answer KeyDocument9 pages04 Accounts Receivable Answer Keywheein aegiNo ratings yet

- Accounting Igcse Chapter 1Document11 pagesAccounting Igcse Chapter 1Emily Goodge100% (1)

- Accounts Receivable: Financial AccountingDocument27 pagesAccounts Receivable: Financial AccountingHassan AliNo ratings yet

- Ho4 - Accounts ReceivableDocument10 pagesHo4 - Accounts ReceivableJanesa CamallaNo ratings yet

- Chapter 2 ReceivablesDocument14 pagesChapter 2 Receivablespapajesus papaNo ratings yet

- Which Method Is Best To Use?Document11 pagesWhich Method Is Best To Use?SSSNIPDNo ratings yet

- 11 ReceivablesDocument4 pages11 ReceivablesuncianojhezrhyllemhaeNo ratings yet

- C4 Accounts ReceivableDocument33 pagesC4 Accounts ReceivableShergie GozumNo ratings yet

- Account Receivables NotesDocument6 pagesAccount Receivables NotesABIGAIL DAYOTNo ratings yet

- Identify Transactions: Accounting CycleDocument6 pagesIdentify Transactions: Accounting CycleNezhreen MaruhomNo ratings yet

- Revenue Recognition and Receivables: Financial Accounting - Lecture 5Document30 pagesRevenue Recognition and Receivables: Financial Accounting - Lecture 5Peter ShangNo ratings yet

- 2 Adjusting Journal EntriesDocument6 pages2 Adjusting Journal EntriesJerric CristobalNo ratings yet

- RECEIVABLESDocument3 pagesRECEIVABLESTrazy Jam BagsicNo ratings yet

- Intermediate AccountingDocument2 pagesIntermediate AccountingKylie CortezNo ratings yet

- ch05 ReceivablesDocument51 pagesch05 ReceivableszedingelNo ratings yet

- Module2 ReceivablesDocument21 pagesModule2 ReceivablesClarence Allen MasicatNo ratings yet

- Enbanc: Republic of The Philippines Court Oft Ax Appeals Quezon CityDocument28 pagesEnbanc: Republic of The Philippines Court Oft Ax Appeals Quezon CityAemie JordanNo ratings yet

- Drill-Receivables CompressDocument7 pagesDrill-Receivables CompressHannahbea LindoNo ratings yet

- 2.1 Assessment Test 2.2: Receivables Prelim Exam Intermediate AccountingDocument9 pages2.1 Assessment Test 2.2: Receivables Prelim Exam Intermediate AccountingWinoah HubaldeNo ratings yet

- ENGM401-LectureSlides 03a Income StatementsDocument34 pagesENGM401-LectureSlides 03a Income StatementsThedudeNo ratings yet

- Xii Acc Retirement Ws With AnsDocument3 pagesXii Acc Retirement Ws With AnsKalrav BhansariNo ratings yet

- Ch09 WRD25e InstructorDocument62 pagesCh09 WRD25e InstructorTan IrisNo ratings yet

- ACCTG W09 Chapter 8Document15 pagesACCTG W09 Chapter 8kayla tsoiNo ratings yet

- Prov For Bad Debts and Bad Debts RecoverDocument9 pagesProv For Bad Debts and Bad Debts RecoverGodfreyFrankMwakalingaNo ratings yet

- CPAR TOA Pre-Board FinalDocument10 pagesCPAR TOA Pre-Board FinalJericho Pedragosa100% (1)

- BC 304 PI Past PapersDocument29 pagesBC 304 PI Past PapersBilal AhmadNo ratings yet

- To Record Estimate of Uncollectible AccountsDocument2 pagesTo Record Estimate of Uncollectible AccountssaraNo ratings yet

- Allowable Deductions - Personal ExemptionsDocument163 pagesAllowable Deductions - Personal ExemptionsMari Erika Joi BancualNo ratings yet

- Unit 2 Measurements, Valuation and Disclosure of Investments and Short-Term ItemsDocument30 pagesUnit 2 Measurements, Valuation and Disclosure of Investments and Short-Term Itemsestihdaf استهدافNo ratings yet

- CAF1 IntorductiontoAccounting2016 QBDocument173 pagesCAF1 IntorductiontoAccounting2016 QBMuhammad Talha0% (1)

- PWC Worldwide Tax Summaries Corporate Taxes 2018 19 2 PDFDocument2,839 pagesPWC Worldwide Tax Summaries Corporate Taxes 2018 19 2 PDFJansen SinagaNo ratings yet

- Topic TwoDocument67 pagesTopic TwoMerediths KrisKringleNo ratings yet

- AUDITINGDocument11 pagesAUDITINGMaud Julie May FagyanNo ratings yet

- 11 Accountancy t2 Sp01Document19 pages11 Accountancy t2 Sp01Lakshy BishtNo ratings yet

- Taxation 2023 QuestionsDocument5 pagesTaxation 2023 QuestionsjanaNo ratings yet

- 2 - Principles of Accounting 101Document22 pages2 - Principles of Accounting 101Robinson Bars0% (1)

- Adjusting Entries - Uncollectible AccountsDocument2 pagesAdjusting Entries - Uncollectible AccountsCharish ImaysayNo ratings yet

- Financial AccountingDocument24 pagesFinancial AccountingGiang PhungNo ratings yet

- Ia1 ReviewerDocument10 pagesIa1 ReviewerVeronica SarmientoNo ratings yet

- Loans and Receivables - StudentDocument3 pagesLoans and Receivables - StudentJerome_JadeNo ratings yet

- Chapter 4 - Deductions From Gross Estate2013Document9 pagesChapter 4 - Deductions From Gross Estate2013Rozel Joy Labasano100% (1)

Download as docx, pdf, or txt

You might also like

- Understanding Financial Statements Solutions Chapter 2Document30 pagesUnderstanding Financial Statements Solutions Chapter 2adam_garcia_81100% (3)

- IM - Updates in Financial Reporting Standards (ACCO 40023) - Cash To AccrualDocument13 pagesIM - Updates in Financial Reporting Standards (ACCO 40023) - Cash To AccrualJasmine100% (2)

- Chapter 10 Income From Business or ProfessionDocument14 pagesChapter 10 Income From Business or ProfessionMd. Rayhanul IslamNo ratings yet

- Chap7 Notes Intermediate Accounting KiesoDocument8 pagesChap7 Notes Intermediate Accounting Kiesoangelbear2577100% (1)

- Tax Test Bank TheoryDocument6 pagesTax Test Bank TheoryXtian de Vera100% (1)

- Chapter 4 Lecture Trade and Non Trade Receivables Part 1 StudentDocument3 pagesChapter 4 Lecture Trade and Non Trade Receivables Part 1 StudentAshlene CruzNo ratings yet

- XFARDocument14 pagesXFARRIZA SAMPAGANo ratings yet

- Audit On ReceivablesDocument19 pagesAudit On ReceivablesPaupauNo ratings yet

- AR AR FinancingDocument34 pagesAR AR FinancingDannis Anne RegajalNo ratings yet

- CKSIAN-Accounting Cycle Hacks pt2Document5 pagesCKSIAN-Accounting Cycle Hacks pt2fhfdhNo ratings yet

- Receivable Financing: Quick Review!Document9 pagesReceivable Financing: Quick Review!Barbie BleuNo ratings yet

- Adjusting Entries. Bad Debts and DepreciationDocument7 pagesAdjusting Entries. Bad Debts and DepreciationShiela LanadoNo ratings yet

- Accounting 471: Class 11Document66 pagesAccounting 471: Class 11CORES LYRICSNo ratings yet

- Notes On Week 3Document11 pagesNotes On Week 3Christy CaneteNo ratings yet

- CH 9 - Intermediate AccountingDocument28 pagesCH 9 - Intermediate Accountinghana osmanNo ratings yet

- Receivables: Created By: Origen, Janiene / Palma, Jennelyn, Cabi Gting, Ela. Artiza, EmmanDocument44 pagesReceivables: Created By: Origen, Janiene / Palma, Jennelyn, Cabi Gting, Ela. Artiza, Emmandeleonjaniene bsaNo ratings yet

- Chapter 5 Estimation of Doubtful AccountsDocument5 pagesChapter 5 Estimation of Doubtful AccountsPam LlanetaNo ratings yet

- 04 Trade Accounts ReceivableDocument7 pages04 Trade Accounts Receivablesharielles /No ratings yet

- IA 1 - 4 ReceivablesDocument9 pagesIA 1 - 4 ReceivablesVJ MacaspacNo ratings yet

- CMA Part 1 Unit 2 (2021)Document116 pagesCMA Part 1 Unit 2 (2021)athul16203682No ratings yet

- Accounting Cycle HacksDocument14 pagesAccounting Cycle HacksAnonymous mnAAXLkYQCNo ratings yet

- Accounts Receivable and Estimating Doubtful AccountsDocument7 pagesAccounts Receivable and Estimating Doubtful AccountsMiles SantosNo ratings yet

- ReceivablesDocument20 pagesReceivablesGemmalyn FolguerasNo ratings yet

- Activity 5 1Document13 pagesActivity 5 1Trice DomingoNo ratings yet

- POA Topic 12Document3 pagesPOA Topic 12Ian ChanNo ratings yet

- Sales Order ProcessingDocument9 pagesSales Order ProcessingKRIS ANNE SAMUDIONo ratings yet

- Quiz 10Document2 pagesQuiz 10andreajade.cawaya10No ratings yet

- Accounting For Receivables: Learning ObjectivesDocument68 pagesAccounting For Receivables: Learning ObjectivesDeeb. DeebNo ratings yet

- Adjusting Entries and Merchandising BusinessDocument5 pagesAdjusting Entries and Merchandising BusinessLing lingNo ratings yet

- 04 Trade Accounts ReceivableDocument7 pages04 Trade Accounts ReceivableKhen HannaNo ratings yet

- Handout 04 Trade ARDocument7 pagesHandout 04 Trade ARMARY GRACE VARGASNo ratings yet

- Control Account Revision NotesDocument30 pagesControl Account Revision NotesOckouri BarnesNo ratings yet

- INTACC 1 - REVIEWER - MIDTERMS (Receivables)Document3 pagesINTACC 1 - REVIEWER - MIDTERMS (Receivables)olerianaryzzsc.56No ratings yet

- CH.8 Notes - Accounting For ReceivablesDocument19 pagesCH.8 Notes - Accounting For ReceivablesLEEN hashemNo ratings yet

- Sample - Monetary Current Assets and LiabilitiesDocument2 pagesSample - Monetary Current Assets and LiabilitiesAdmin - At Least Know ThisNo ratings yet

- Section 7 CONTROL SYSTEMDocument42 pagesSection 7 CONTROL SYSTEMWilliNo ratings yet

- Ffa W12343Document22 pagesFfa W12343DaddyNo ratings yet

- Accounting and Finance BankersDocument68 pagesAccounting and Finance BankersNamita SharmaNo ratings yet

- AR and Doubtful Accounts - NotesDocument5 pagesAR and Doubtful Accounts - NotesTEOPE, EMERLIZA DE CASTRONo ratings yet

- AT Least: CPA Exam Review 2018Document6 pagesAT Least: CPA Exam Review 2018At Least Know This CPANo ratings yet

- RECEIVABLE - Are Financial Assets That Represent A Contractual Right To Receive Cash or AnotherDocument22 pagesRECEIVABLE - Are Financial Assets That Represent A Contractual Right To Receive Cash or AnotherSB19 ChicKENNo ratings yet

- Page 51 From Audit Akm CompreDocument1 pagePage 51 From Audit Akm CompreGaby VionidyaNo ratings yet

- Page 51 From Audit Akm CompreDocument1 pagePage 51 From Audit Akm CompreGaby VionidyaNo ratings yet

- TOPIC 4 Principle - Of.double - EntryDocument4 pagesTOPIC 4 Principle - Of.double - EntryNurul Ain Binti Abd RahimNo ratings yet

- Z Chapter 4 The Revenue Cycle TamanoDocument4 pagesZ Chapter 4 The Revenue Cycle TamanoBrylle TamanoNo ratings yet

- Accounts ReceivableDocument23 pagesAccounts ReceivableAbby MendozaNo ratings yet

- BUSI 2001 Int. AccountingDocument3 pagesBUSI 2001 Int. AccountingJoshNo ratings yet

- Receivable FinancingDocument15 pagesReceivable FinancingArt EezyNo ratings yet

- 04 Accounts Receivable Answer KeyDocument9 pages04 Accounts Receivable Answer Keywheein aegiNo ratings yet

- Accounting Igcse Chapter 1Document11 pagesAccounting Igcse Chapter 1Emily Goodge100% (1)

- Accounts Receivable: Financial AccountingDocument27 pagesAccounts Receivable: Financial AccountingHassan AliNo ratings yet

- Ho4 - Accounts ReceivableDocument10 pagesHo4 - Accounts ReceivableJanesa CamallaNo ratings yet

- Chapter 2 ReceivablesDocument14 pagesChapter 2 Receivablespapajesus papaNo ratings yet

- Which Method Is Best To Use?Document11 pagesWhich Method Is Best To Use?SSSNIPDNo ratings yet

- 11 ReceivablesDocument4 pages11 ReceivablesuncianojhezrhyllemhaeNo ratings yet

- C4 Accounts ReceivableDocument33 pagesC4 Accounts ReceivableShergie GozumNo ratings yet

- Account Receivables NotesDocument6 pagesAccount Receivables NotesABIGAIL DAYOTNo ratings yet

- Identify Transactions: Accounting CycleDocument6 pagesIdentify Transactions: Accounting CycleNezhreen MaruhomNo ratings yet

- Revenue Recognition and Receivables: Financial Accounting - Lecture 5Document30 pagesRevenue Recognition and Receivables: Financial Accounting - Lecture 5Peter ShangNo ratings yet

- 2 Adjusting Journal EntriesDocument6 pages2 Adjusting Journal EntriesJerric CristobalNo ratings yet

- RECEIVABLESDocument3 pagesRECEIVABLESTrazy Jam BagsicNo ratings yet

- Intermediate AccountingDocument2 pagesIntermediate AccountingKylie CortezNo ratings yet

- ch05 ReceivablesDocument51 pagesch05 ReceivableszedingelNo ratings yet

- Module2 ReceivablesDocument21 pagesModule2 ReceivablesClarence Allen MasicatNo ratings yet

- Enbanc: Republic of The Philippines Court Oft Ax Appeals Quezon CityDocument28 pagesEnbanc: Republic of The Philippines Court Oft Ax Appeals Quezon CityAemie JordanNo ratings yet

- Drill-Receivables CompressDocument7 pagesDrill-Receivables CompressHannahbea LindoNo ratings yet

- 2.1 Assessment Test 2.2: Receivables Prelim Exam Intermediate AccountingDocument9 pages2.1 Assessment Test 2.2: Receivables Prelim Exam Intermediate AccountingWinoah HubaldeNo ratings yet

- ENGM401-LectureSlides 03a Income StatementsDocument34 pagesENGM401-LectureSlides 03a Income StatementsThedudeNo ratings yet

- Xii Acc Retirement Ws With AnsDocument3 pagesXii Acc Retirement Ws With AnsKalrav BhansariNo ratings yet

- Ch09 WRD25e InstructorDocument62 pagesCh09 WRD25e InstructorTan IrisNo ratings yet

- ACCTG W09 Chapter 8Document15 pagesACCTG W09 Chapter 8kayla tsoiNo ratings yet

- Prov For Bad Debts and Bad Debts RecoverDocument9 pagesProv For Bad Debts and Bad Debts RecoverGodfreyFrankMwakalingaNo ratings yet

- CPAR TOA Pre-Board FinalDocument10 pagesCPAR TOA Pre-Board FinalJericho Pedragosa100% (1)

- BC 304 PI Past PapersDocument29 pagesBC 304 PI Past PapersBilal AhmadNo ratings yet

- To Record Estimate of Uncollectible AccountsDocument2 pagesTo Record Estimate of Uncollectible AccountssaraNo ratings yet

- Allowable Deductions - Personal ExemptionsDocument163 pagesAllowable Deductions - Personal ExemptionsMari Erika Joi BancualNo ratings yet

- Unit 2 Measurements, Valuation and Disclosure of Investments and Short-Term ItemsDocument30 pagesUnit 2 Measurements, Valuation and Disclosure of Investments and Short-Term Itemsestihdaf استهدافNo ratings yet

- CAF1 IntorductiontoAccounting2016 QBDocument173 pagesCAF1 IntorductiontoAccounting2016 QBMuhammad Talha0% (1)

- PWC Worldwide Tax Summaries Corporate Taxes 2018 19 2 PDFDocument2,839 pagesPWC Worldwide Tax Summaries Corporate Taxes 2018 19 2 PDFJansen SinagaNo ratings yet

- Topic TwoDocument67 pagesTopic TwoMerediths KrisKringleNo ratings yet

- AUDITINGDocument11 pagesAUDITINGMaud Julie May FagyanNo ratings yet

- 11 Accountancy t2 Sp01Document19 pages11 Accountancy t2 Sp01Lakshy BishtNo ratings yet

- Taxation 2023 QuestionsDocument5 pagesTaxation 2023 QuestionsjanaNo ratings yet

- 2 - Principles of Accounting 101Document22 pages2 - Principles of Accounting 101Robinson Bars0% (1)

- Adjusting Entries - Uncollectible AccountsDocument2 pagesAdjusting Entries - Uncollectible AccountsCharish ImaysayNo ratings yet

- Financial AccountingDocument24 pagesFinancial AccountingGiang PhungNo ratings yet

- Ia1 ReviewerDocument10 pagesIa1 ReviewerVeronica SarmientoNo ratings yet

- Loans and Receivables - StudentDocument3 pagesLoans and Receivables - StudentJerome_JadeNo ratings yet

- Chapter 4 - Deductions From Gross Estate2013Document9 pagesChapter 4 - Deductions From Gross Estate2013Rozel Joy Labasano100% (1)