Download as docx, pdf, or txt

You might also like

- Financial Accounting Chapter 3Document5 pagesFinancial Accounting Chapter 3NiraniyaNo ratings yet

- Facebook Advertising Guide by Shopify and Adespresso PDFDocument87 pagesFacebook Advertising Guide by Shopify and Adespresso PDFFerdouse OmarNo ratings yet

- Master NoteDocument9 pagesMaster NoteCA Paramesh HemanathNo ratings yet

- Section 4 IDocument22 pagesSection 4 ISatish Ranjan PradhanNo ratings yet

- Fama AssignmentDocument7 pagesFama AssignmentAdityaNo ratings yet

- FRA - Accounting PoliciesDocument4 pagesFRA - Accounting PoliciesGarima SharmaNo ratings yet

- Maruti Suzuki India LTD Is The Name of The CompanyDocument2 pagesMaruti Suzuki India LTD Is The Name of The CompanyPulkitNo ratings yet

- ASSIGNMENTDocument7 pagesASSIGNMENTRahulNo ratings yet

- Nykaa E Retail Mar 19Document23 pagesNykaa E Retail Mar 19NatNo ratings yet

- Accounting Policies - Study Group 4IDocument24 pagesAccounting Policies - Study Group 4ISatish Ranjan PradhanNo ratings yet

- Consolidated Financials 2020 21Document116 pagesConsolidated Financials 2020 21Tuhin SenNo ratings yet

- Standalone Notes To AccountsDocument31 pagesStandalone Notes To AccountsJP Jeya PrasannaNo ratings yet

- Term Paper Internal Assessment Programme: Mba Semester: 3 Course: Cost and Management AccountingDocument11 pagesTerm Paper Internal Assessment Programme: Mba Semester: 3 Course: Cost and Management AccountingRACHITNo ratings yet

- Financial Accounting Assignment Final SubmissionDocument7 pagesFinancial Accounting Assignment Final SubmissionAbhishekNo ratings yet

- Significant Accounting Policies TVS MotorsDocument12 pagesSignificant Accounting Policies TVS MotorsArjun Singh Omkar100% (1)

- Financial Staements Duly Authenticated As Per Section 134 (Including Boards Report, Auditors Report and Other Documents) - 29102023Document28 pagesFinancial Staements Duly Authenticated As Per Section 134 (Including Boards Report, Auditors Report and Other Documents) - 29102023mnbvcxzqwerNo ratings yet

- Narsee Monjee Institute of Management StudiesDocument7 pagesNarsee Monjee Institute of Management StudiesRishabh MishraNo ratings yet

- Probiotec Annual Report 2022 6Document8 pagesProbiotec Annual Report 2022 6楊敬宇No ratings yet

- Major Accounting PoliciesDocument8 pagesMajor Accounting Policies325KAIVALYAPAINo ratings yet

- The Evocative Essential Oil and Scented Candles: 2.1 Basis of Preparation of Financial StatementsDocument12 pagesThe Evocative Essential Oil and Scented Candles: 2.1 Basis of Preparation of Financial StatementsExequiel AmbasingNo ratings yet

- Impact of Ind AS 115 On Emami LTDDocument4 pagesImpact of Ind AS 115 On Emami LTDTanishq VarmaNo ratings yet

- Applicability: Business Organisation Types of IncomeDocument3 pagesApplicability: Business Organisation Types of Incomegaurav069No ratings yet

- TataDocument56 pagesTataAndreea GeorgianaNo ratings yet

- 9 Notes To The Financial Statments NotesDocument36 pages9 Notes To The Financial Statments NotesmohammedaliyyeNo ratings yet

- CK Foods Significant Accounting PoliciesDocument9 pagesCK Foods Significant Accounting PoliciesA YoungNo ratings yet

- IFRS Financials Jun 2014Document25 pagesIFRS Financials Jun 2014Navin KumarNo ratings yet

- Ar-18 9Document5 pagesAr-18 9jawad anwarNo ratings yet

- IND As SummaryDocument41 pagesIND As SummaryAishwarya RajeshNo ratings yet

- Notes To The Financial Statements SampleDocument6 pagesNotes To The Financial Statements SampleKielRinonNo ratings yet

- Financial Accounting and Management Accounting: Individual Assignment (Ind AS)Document6 pagesFinancial Accounting and Management Accounting: Individual Assignment (Ind AS)gauravpalgarimapalNo ratings yet

- Financial Accounting Final Project - Toyota Indus MotorsDocument10 pagesFinancial Accounting Final Project - Toyota Indus Motorsstd34537No ratings yet

- Tata Technologies Inc.Document16 pagesTata Technologies Inc.sanjit kadneNo ratings yet

- Policies - 09Document2 pagesPolicies - 09Ayeman AnwarNo ratings yet

- Technical Interview Questions Prepared by Fahad Irfan - PDF Version 1Document4 pagesTechnical Interview Questions Prepared by Fahad Irfan - PDF Version 1Muhammad Khizzar KhanNo ratings yet

- Significant Accounting PoliciesDocument4 pagesSignificant Accounting PoliciesVenkat Sai Kumar KothalaNo ratings yet

- Individual Project: Financial and Managerial Accounting Assignment Submitted By: Gaurav Pal, A037Document3 pagesIndividual Project: Financial and Managerial Accounting Assignment Submitted By: Gaurav Pal, A037gauravpalgarimapalNo ratings yet

- Consolidated Financial Statements Indian GAAP Dec07Document15 pagesConsolidated Financial Statements Indian GAAP Dec07martynmvNo ratings yet

- Accounting Policies and Notes Final 14.09.2016Document10 pagesAccounting Policies and Notes Final 14.09.2016ramaiahNo ratings yet

- Consolidated Financials 2021 22Document142 pagesConsolidated Financials 2021 22sairaj bhatkarNo ratings yet

- ACC ASSIGNMENT - Abhilash ChaudharyDocument17 pagesACC ASSIGNMENT - Abhilash ChaudharyAbhilash ChaudharyNo ratings yet

- Continous Assignment 2: Mittal School of BusinessDocument8 pagesContinous Assignment 2: Mittal School of BusinessMd UjaleNo ratings yet

- Indian Accounting Standards: Manish B TardejaDocument45 pagesIndian Accounting Standards: Manish B TardejaManish TardejaNo ratings yet

- Almarai AR2018 8mb Final EnglishDocument19 pagesAlmarai AR2018 8mb Final EnglishtahirfaridNo ratings yet

- IND AS FAQsDocument21 pagesIND AS FAQsbhavana40pashamNo ratings yet

- Mary Joy L. Amigos Rice Store Notes To The Financial StatementsDocument5 pagesMary Joy L. Amigos Rice Store Notes To The Financial StatementsLizanne GauranaNo ratings yet

- Accounting Standard of Mahindra and Mahindra LTDDocument9 pagesAccounting Standard of Mahindra and Mahindra LTDDheeraj shettyNo ratings yet

- FAMA OldDocument4 pagesFAMA OldVarun RNo ratings yet

- EFU Accounting PoliciesDocument9 pagesEFU Accounting PoliciesJaved AkramNo ratings yet

- Introduction To Social MediaDocument176 pagesIntroduction To Social MediaLiiNo ratings yet

- XXXXXXXXXXXXXXX, Inc.: Notes To Financial Statements DECEMBER 31, 2018 1.) Corporate InformationDocument7 pagesXXXXXXXXXXXXXXX, Inc.: Notes To Financial Statements DECEMBER 31, 2018 1.) Corporate InformationJmei AfflieriNo ratings yet

- Individual Assignment (Financial Accounting Module)Document4 pagesIndividual Assignment (Financial Accounting Module)Heisenberg008No ratings yet

- 9 Framework For Preparation - Presentation of Financial StatementsDocument13 pages9 Framework For Preparation - Presentation of Financial StatementssmartshivenduNo ratings yet

- Accounting StandardsDocument10 pagesAccounting StandardsSakshi JaiswalNo ratings yet

- Ca IfrsDocument7 pagesCa IfrsyogeshNo ratings yet

- Mohammed Bilal Choudhary (Ju2021Mba14574) Activity - 1 Fsra 1Document4 pagesMohammed Bilal Choudhary (Ju2021Mba14574) Activity - 1 Fsra 1Md BilalNo ratings yet

- Ind-AS PDFDocument4 pagesInd-AS PDFManish MalikNo ratings yet

- Analysis of Financial Reporting by Dr. Reddy's Laboratories Ltd.Document9 pagesAnalysis of Financial Reporting by Dr. Reddy's Laboratories Ltd.Soumya ChakrabortyNo ratings yet

- SARHAD OpinionDocument2 pagesSARHAD OpinionExtra KhanNo ratings yet

- Accounting For Managers.: Assignment 2 by Group 13Document12 pagesAccounting For Managers.: Assignment 2 by Group 13Rutvik RavalNo ratings yet

- Introduction To IFRSDocument33 pagesIntroduction To IFRSmikirichaNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Executive Project SummaryDocument2 pagesExecutive Project SummaryNave2n adventurism & art works.No ratings yet

- Marketing of ServiceDocument11 pagesMarketing of ServiceNave2n adventurism & art works.No ratings yet

- Companies Act 2013 and Consumer Protection ActDocument13 pagesCompanies Act 2013 and Consumer Protection ActNave2n adventurism & art works.No ratings yet

- What Is Inflatoion IssueDocument2 pagesWhat Is Inflatoion IssueNave2n adventurism & art works.No ratings yet

- Sale of Goods Act and Negotiable Instrument ActDocument14 pagesSale of Goods Act and Negotiable Instrument ActNave2n adventurism & art works.No ratings yet

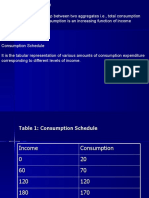

- Answer 2 Consumption FunctionDocument4 pagesAnswer 2 Consumption FunctionNave2n adventurism & art works.No ratings yet

- Consumption FunctionDocument15 pagesConsumption FunctionNave2n adventurism & art works.No ratings yet

- Bkash Limited 2015 (Signed Financials)Document40 pagesBkash Limited 2015 (Signed Financials)Onamika AktherNo ratings yet

- Anand mAHIN PDFDocument1 pageAnand mAHIN PDFABHILASH M VNo ratings yet

- Template FMEA5Document5 pagesTemplate FMEA5Puneet SharmaNo ratings yet

- DMart Case Study - Group 06Document3 pagesDMart Case Study - Group 06Siddhi GodeNo ratings yet

- ? Set Up Sales Cloud Einstein ?Document27 pages? Set Up Sales Cloud Einstein ?bhadec05No ratings yet

- Roles in Project ManagementDocument18 pagesRoles in Project Managementአረጋዊ ሐይለማርያም100% (1)

- Impact of Training and Development Programmes On Indian BanksDocument7 pagesImpact of Training and Development Programmes On Indian BanksaaaNo ratings yet

- WWW Indiabix Com PDFDocument4 pagesWWW Indiabix Com PDFAnil Kumar Gorantala100% (1)

- STP/EHTP SchemeDocument2 pagesSTP/EHTP SchemeHồ ThànhNo ratings yet

- Sanyo RefrigeratorsDocument3 pagesSanyo Refrigeratorspratikhire9No ratings yet

- Learner GuideDocument172 pagesLearner GuideMarius BuysNo ratings yet

- Types of ProposalDocument3 pagesTypes of ProposalSubhash DhungelNo ratings yet

- Semrush Toolkit For Seo SampleDocument23 pagesSemrush Toolkit For Seo SamplePraveen SivaNo ratings yet

- SO253411B Test Report VRTM TouchupDocument11 pagesSO253411B Test Report VRTM Touchupmpedraza-1No ratings yet

- Afar Partnerships Ms. Ellery D. de Leon: True or FalseDocument6 pagesAfar Partnerships Ms. Ellery D. de Leon: True or FalsePat DrezaNo ratings yet

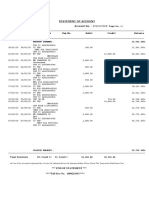

- Statement of Account PDFDocument3 pagesStatement of Account PDFPradyumn MangalNo ratings yet

- Intermediate Reading Yr 2Document3 pagesIntermediate Reading Yr 2Leri KharatiNo ratings yet

- Labor Rights - Textile Industry in KarachiDocument15 pagesLabor Rights - Textile Industry in KarachimusabNo ratings yet

- JpmorganDocument4 pagesJpmorganSabri MaggiNo ratings yet

- ( (Dœmr' Boimßh$Z Ho$ (G'M V Edß Ï'Dhma)Document19 pages( (Dœmr' Boimßh$Z Ho$ (G'M V Edß Ï'Dhma)Satyam MishraNo ratings yet

- Chapter 2 - Intro To ITDocument12 pagesChapter 2 - Intro To ITMakiri Sajili IINo ratings yet

- Introduction To Knowledge Management in Theory and Practice: Kimiz DalkirDocument10 pagesIntroduction To Knowledge Management in Theory and Practice: Kimiz Dalkiravinash bNo ratings yet

- BSBTEC501 CBSA Business Plan V1Document10 pagesBSBTEC501 CBSA Business Plan V1Lis FalisNo ratings yet

- Final Exam With AnswerDocument8 pagesFinal Exam With Answerg409863No ratings yet

- Prem Amul PaneerDocument57 pagesPrem Amul PaneerShailesh KumarNo ratings yet

- Kotler Brand PositioningDocument22 pagesKotler Brand PositioningcarloNo ratings yet

- Employee Engagement PDFDocument1 pageEmployee Engagement PDFEnrique Ignacio PastenetNo ratings yet

- STLCDocument5 pagesSTLCmanoharNo ratings yet

- Comparative Vs Competitive AdvantageDocument19 pagesComparative Vs Competitive AdvantageSuntari CakSoenNo ratings yet