Download as pdf or txt

You might also like

- Study Master Accounting Grade 10 Teacher S GuideDocument356 pagesStudy Master Accounting Grade 10 Teacher S GuideSweetness MakaLuthando Leocardia100% (2)

- Correction of ErrorsDocument119 pagesCorrection of ErrorsKevin James Sedurifa Oledan100% (1)

- Level 5 Assessment Specification: Appendix Ga36BDocument10 pagesLevel 5 Assessment Specification: Appendix Ga36BcsolutionNo ratings yet

- Final Industrial Training Report SignedDocument66 pagesFinal Industrial Training Report SignedJannah AhmadNo ratings yet

- 0450 Specimen Paper Answers Paper 1 For Examination From 2020Document12 pages0450 Specimen Paper Answers Paper 1 For Examination From 2020TinaYuNo ratings yet

- Act1111 Final ExamDocument7 pagesAct1111 Final ExamHaidee Flavier SabidoNo ratings yet

- Auditing Problem - Preweek: Cordillera Career Development College College of AccountancyDocument42 pagesAuditing Problem - Preweek: Cordillera Career Development College College of AccountancyGi Ne VaNo ratings yet

- Four Seasons PMS - FinalDocument24 pagesFour Seasons PMS - FinalnjbitsNo ratings yet

- Edutech Business Plan FinalizedDocument13 pagesEdutech Business Plan FinalizedBun Hourng TanNo ratings yet

- FAR SYLLABUS FinalDocument13 pagesFAR SYLLABUS FinalUchiha WarrenNo ratings yet

- FAR SYLLABUS FinalDocument13 pagesFAR SYLLABUS FinalUchiha WarrenNo ratings yet

- Assignment_DBB2203_BBA 4_SET 1&2_April 2024Document4 pagesAssignment_DBB2203_BBA 4_SET 1&2_April 2024hazilmohamed990No ratings yet

- TDR Kawasaki Pra SuhDocument17 pagesTDR Kawasaki Pra SuhS Suhas Kumar ShettyNo ratings yet

- ACCT 2015 Mona WJC 2022 Course OutlineDocument10 pagesACCT 2015 Mona WJC 2022 Course OutlineChristina StephensonNo ratings yet

- Curriculum: 2016-18 (Batch) Faculty of Commerce and ManagementDocument72 pagesCurriculum: 2016-18 (Batch) Faculty of Commerce and ManagementDeepak PaulNo ratings yet

- Fundamentals of Accountancy 1 SyllabusDocument8 pagesFundamentals of Accountancy 1 SyllabusronNo ratings yet

- Training Proposal Confidence GroupDocument3 pagesTraining Proposal Confidence GroupSharif Abu Nasser ShahinNo ratings yet

- Course Information Summer Semester 2019/2020Document4 pagesCourse Information Summer Semester 2019/2020mmNo ratings yet

- BMM 4442 Final Exam January 2021Document6 pagesBMM 4442 Final Exam January 2021adydinamo1992No ratings yet

- General Guidelines:: ©IAS Placement Office DocumentDocument6 pagesGeneral Guidelines:: ©IAS Placement Office DocumentIqrä QurëshìNo ratings yet

- FAR SYLLABUS FinalDocument13 pagesFAR SYLLABUS FinalUchiha WarrenNo ratings yet

- Conceptual FrameworkDocument13 pagesConceptual FrameworkUchiha WarrenNo ratings yet

- SoaluasakuntansiDocument4 pagesSoaluasakuntansiAlia FardaniNo ratings yet

- Sem 1, 2009 AnnotatedDocument6 pagesSem 1, 2009 Annotatedmoksiuwai100% (2)

- BINUS University: Academic Career: Class ProgramDocument3 pagesBINUS University: Academic Career: Class ProgramJohan fetoNo ratings yet

- 1. Major Accountancy and Financial Management – III 1Document5 pages1. Major Accountancy and Financial Management – III 1anonymous0unNo ratings yet

- BSBFIM601 Learner Workbook-FinalDocument53 pagesBSBFIM601 Learner Workbook-Finalpurva020% (1)

- Assignment Brief MAPE 6AG523 Jan 2024Document16 pagesAssignment Brief MAPE 6AG523 Jan 2024tabonemoira88No ratings yet

- Techno Computer Training CenterDocument11 pagesTechno Computer Training CenterAlemnew SisayNo ratings yet

- Financial Accounting and Analysis AssignmentDocument3 pagesFinancial Accounting and Analysis AssignmentaarhaNo ratings yet

- Financial Accounting and Analysis - Assignment Dec 2021 - Set 1 GvzfOVqGMUDocument3 pagesFinancial Accounting and Analysis - Assignment Dec 2021 - Set 1 GvzfOVqGMUTanmay KothariNo ratings yet

- ACC10007 - Financial Information For Decision Making & HBC110N - Accounting For Managers Outline Semester 1, 2016Document10 pagesACC10007 - Financial Information For Decision Making & HBC110N - Accounting For Managers Outline Semester 1, 2016LeoniMeirisNo ratings yet

- STVEP Entrepreneurship 10 Q1 LAS4 FINALDocument16 pagesSTVEP Entrepreneurship 10 Q1 LAS4 FINALSun Shine OalnacarasNo ratings yet

- Intermediate Accountig AkuntansiDocument46 pagesIntermediate Accountig AkuntansiRika LerianiNo ratings yet

- ACCT6008 - Semester 2, 2021Document9 pagesACCT6008 - Semester 2, 2021Zhang RickNo ratings yet

- Welcome To The B124 Introductory TutorialDocument35 pagesWelcome To The B124 Introductory TutorialFlavio Leal Jovchelevitch0% (1)

- ABM - BF12 IIIb 8Document4 pagesABM - BF12 IIIb 8Raffy Jade SalazarNo ratings yet

- Free Basic School Business Plan TemplateDocument8 pagesFree Basic School Business Plan TemplateADEBAYO TAJUDEENNo ratings yet

- ACC201 PA - UEH-ISB - S1 2019 - Unit Guide - Sent To LecturerDocument9 pagesACC201 PA - UEH-ISB - S1 2019 - Unit Guide - Sent To LecturerHa TranNo ratings yet

- Accounting For BusinessDocument25 pagesAccounting For Businesstheonesmk01No ratings yet

- Assessment 2: InstructionsDocument5 pagesAssessment 2: InstructionsThiago FlorianoNo ratings yet

- August 8,2017Document3 pagesAugust 8,2017April Joy Lascuña - CailoNo ratings yet

- FINA 3710 SyllabusDocument4 pagesFINA 3710 SyllabusroBinNo ratings yet

- ACC202 - Managerial Accounting - Trimester 1 2024Document13 pagesACC202 - Managerial Accounting - Trimester 1 2024Huong Nguyen Thi XuanNo ratings yet

- SyllabusDocument19 pagesSyllabusanonymousNo ratings yet

- MAF 551 - Exercise 2 - Answer Question 1 - Seri Melur Institution - Ridzuan Bin Saharun 2017700141Document3 pagesMAF 551 - Exercise 2 - Answer Question 1 - Seri Melur Institution - Ridzuan Bin Saharun 2017700141RIDZUAN SAHARUNNo ratings yet

- Work Experience Guide - MKT2054Document23 pagesWork Experience Guide - MKT2054PopescuLaurentiuNo ratings yet

- Unit Outline: MKT20031 Marketing and InnovationDocument8 pagesUnit Outline: MKT20031 Marketing and InnovationShehry Vibes100% (1)

- Workshop On Finance For Non-FinanceDocument9 pagesWorkshop On Finance For Non-FinanceShruti SinghalNo ratings yet

- Christ (Deemed To Be University) School of Business and Management Assignment BriefDocument5 pagesChrist (Deemed To Be University) School of Business and Management Assignment BriefLatha JosephNo ratings yet

- Technopreneurship Course OutlineDocument9 pagesTechnopreneurship Course OutlineDino Dizon100% (1)

- Muhammad Ilham R - 201650584 - UTSDocument6 pagesMuhammad Ilham R - 201650584 - UTSIvonie NursalimNo ratings yet

- BU 100: Introduction To Business: Course DescriptionDocument14 pagesBU 100: Introduction To Business: Course DescriptionscribdlertooNo ratings yet

- ACG4940 - Spring 2020Document9 pagesACG4940 - Spring 2020Ryan NguyenNo ratings yet

- Sunny Side Up: Jury PresentationDocument27 pagesSunny Side Up: Jury PresentationSivakrishna MhNo ratings yet

- Session 8 L&D Metrics and Analytics 25th June 2020 For StudentsDocument44 pagesSession 8 L&D Metrics and Analytics 25th June 2020 For StudentsKishore KumarNo ratings yet

- Ugb 253Document6 pagesUgb 253Abdumalik KakhkhorovNo ratings yet

- Research 2 SyllabusDocument5 pagesResearch 2 SyllabusMaricar Pepito RellonNo ratings yet

- Ukam3043 Management Accounting IiiDocument9 pagesUkam3043 Management Accounting IiiBay Jing TingNo ratings yet

- Learning: Fundamentals of Accounting, Business and Management 1Document13 pagesLearning: Fundamentals of Accounting, Business and Management 1MTECH ASIANo ratings yet

- BCOM Syllabus Sem and 2Document28 pagesBCOM Syllabus Sem and 2anuprakash0812No ratings yet

- Syllabus BCOM 14102021Document15 pagesSyllabus BCOM 14102021Shreya MNo ratings yet

- BSBI422 Final Special Project V5Document10 pagesBSBI422 Final Special Project V5hamzaNo ratings yet

- Achievements and Skills Showcase Made Easy: The Made Easy Series Collection, #4From EverandAchievements and Skills Showcase Made Easy: The Made Easy Series Collection, #4No ratings yet

- Ias 36 - Impairment of Assets ObjectiveDocument9 pagesIas 36 - Impairment of Assets ObjectiveAbdullah Al Amin MubinNo ratings yet

- Financial Plan / Strategy / Analysis: 1.1 Project Implementation Cost ScheduleDocument11 pagesFinancial Plan / Strategy / Analysis: 1.1 Project Implementation Cost ScheduleNadrahNo ratings yet

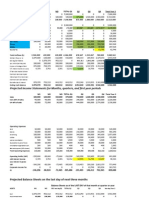

- Projected Income Statements For Months, Quarters, and First Year PeriodsDocument5 pagesProjected Income Statements For Months, Quarters, and First Year Periodssarakhan0622No ratings yet

- SAP Asset Accounting Interview QuestionsDocument3 pagesSAP Asset Accounting Interview QuestionsManas Kumar SahooNo ratings yet

- Chap 8Document13 pagesChap 8MichelleLeeNo ratings yet

- MOCKBOARD With AnswersDocument12 pagesMOCKBOARD With AnswersAnonymous IFu8Wi1gHINo ratings yet

- Sebi Grade A 2020 Costing Methods of CostingDocument12 pagesSebi Grade A 2020 Costing Methods of Costing45satishNo ratings yet

- Problem 1: The Accounts of Marissa Babilonia Health Store Selected From The December 31, 2019 TrialDocument2 pagesProblem 1: The Accounts of Marissa Babilonia Health Store Selected From The December 31, 2019 TrialKimberly G. EtangNo ratings yet

- The Companies Audit of Cost Accounts Regulations 2020 CompressedDocument116 pagesThe Companies Audit of Cost Accounts Regulations 2020 CompressedMuhammad WaqarNo ratings yet

- Week 5 NotesDocument9 pagesWeek 5 NotescalebNo ratings yet

- Assignment Budgeting 1 WorksheetDocument9 pagesAssignment Budgeting 1 WorksheetSultan Bin OboodNo ratings yet

- Exemplu Big BathDocument16 pagesExemplu Big BathValentin BurcaNo ratings yet

- Solution Jan 2018Document8 pagesSolution Jan 2018anis izzatiNo ratings yet

- Advanced Tax Laws Practice PDFDocument188 pagesAdvanced Tax Laws Practice PDFavsharika100% (1)

- Dessert Bakery Business PlanDocument15 pagesDessert Bakery Business PlanPrakash BabuNo ratings yet

- 10 31 Fabm QS 2Document10 pages10 31 Fabm QS 2Fat AjummaNo ratings yet

- 41 DepletionDocument5 pages41 DepletionjsemlpzNo ratings yet

- BUSINESS PLAN-template-ent300 - Mac2018Document41 pagesBUSINESS PLAN-template-ent300 - Mac2018illya amyraNo ratings yet

- Accounting Theory PDFDocument14 pagesAccounting Theory PDFConnor McCarraNo ratings yet

- Cadila Health (Version 1)Document12 pagesCadila Health (Version 1)Sahitya sinhaNo ratings yet

- Accounting For FOHDocument23 pagesAccounting For FOHjoint accountNo ratings yet

- Chapter (2) : Financial Feasibility StudyDocument52 pagesChapter (2) : Financial Feasibility StudyDing RarugalNo ratings yet

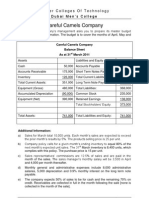

- Color-Coding:: Step 1 - Enter Info About Your Company in Yellow Shaded Boxes BelowDocument26 pagesColor-Coding:: Step 1 - Enter Info About Your Company in Yellow Shaded Boxes BelowBangesweNo ratings yet

- Conceptual Issues by CA. Naveen ND GuptaDocument23 pagesConceptual Issues by CA. Naveen ND GuptaTapas PurwarNo ratings yet

- 2023 IPA Annual ReportDocument90 pages2023 IPA Annual ReportDaniel PandapotanNo ratings yet

- Cash Flow and Working Capital Management - Module 2 - Comprehensive Liquidity Index, Cash Conversion CycleDocument63 pagesCash Flow and Working Capital Management - Module 2 - Comprehensive Liquidity Index, Cash Conversion CyclecarlofgarciaNo ratings yet