2021 Gilbert Case Student Course V4 (Version 1)

2021 Gilbert Case Student Course V4 (Version 1)

You might also like

- Final Solution - New Heritage Doll CompanyDocument6 pagesFinal Solution - New Heritage Doll CompanyRehan Tyagi100% (2)

- Anandam Case Study - AFSDocument20 pagesAnandam Case Study - AFSSiddhesh Mahadik67% (3)

- Group6 - Heritage Doll CaseDocument6 pagesGroup6 - Heritage Doll Casesanket vermaNo ratings yet

- Simple LBODocument16 pagesSimple LBOsingh0001No ratings yet

- Corporate Finance Mini CaseDocument6 pagesCorporate Finance Mini CaseMashaal FNo ratings yet

- New Heritage Doll CompanDocument9 pagesNew Heritage Doll CompanArima ChatterjeeNo ratings yet

- Houzit Pty LTD: 1st Quarter Ended Sept - 2012 Actual Results Budget Q1 Actual Q1 $ VarianceDocument4 pagesHouzit Pty LTD: 1st Quarter Ended Sept - 2012 Actual Results Budget Q1 Actual Q1 $ VarianceHamza Anees100% (1)

- CFI 3 Statement Model Complete in ClassDocument10 pagesCFI 3 Statement Model Complete in ClassThiện NhânNo ratings yet

- Financials at GlanceDocument1 pageFinancials at GlanceSrikanth Marriboyanna MNo ratings yet

- gLLjeluWEem7ixL - 6m9HFg - PolyPanel TO DO Before WEEK 1Document2 pagesgLLjeluWEem7ixL - 6m9HFg - PolyPanel TO DO Before WEEK 1Mohammed Soliman MasliNo ratings yet

- Assignment - 1Document2 pagesAssignment - 1asfandyarkhaliq0% (1)

- Chapter 3. Exhibits y AnexosDocument24 pagesChapter 3. Exhibits y AnexosJulio Arroyo GilNo ratings yet

- CFM Lbo ModelDocument3 pagesCFM Lbo ModelReusNo ratings yet

- Demo File On ValuationDocument3 pagesDemo File On Valuationamaan khanNo ratings yet

- Financials at GlanceDocument1 pageFinancials at Glancekanwal23No ratings yet

- Balance Sheet: Total Equity and LiabilitiesDocument11 pagesBalance Sheet: Total Equity and LiabilitiesSamarth LahotiNo ratings yet

- A - Case Study: Dreaming Corp.: The Financial Statements of Dreaming Corp. Are The Following (In K )Document7 pagesA - Case Study: Dreaming Corp.: The Financial Statements of Dreaming Corp. Are The Following (In K )Mohamed Lamine SanohNo ratings yet

- Five Years' Financial Summary: REPORT 2015Document2 pagesFive Years' Financial Summary: REPORT 2015Rizwan ZisanNo ratings yet

- Key Figures (Euros, Thousands) - Source: Annual Reports 2005-2013Document10 pagesKey Figures (Euros, Thousands) - Source: Annual Reports 2005-2013Wassi Ademola MoudachirouNo ratings yet

- $ Million 2013 2012: Balance SheetDocument3 pages$ Million 2013 2012: Balance Sheetyash sarohaNo ratings yet

- Balance Sheet: Fast Sparrow IncDocument7 pagesBalance Sheet: Fast Sparrow Incmudassir rehmanNo ratings yet

- FM Assignment 02Document1 pageFM Assignment 02Sufyan SarwarNo ratings yet

- Mock Exam FRPM SolutionDocument45 pagesMock Exam FRPM SolutionangelitayosecasetiawanNo ratings yet

- S BqFC2 - T5KgahQtv8 SXQ - Module 3 7 iMBA Example LBO TypeDocument8 pagesS BqFC2 - T5KgahQtv8 SXQ - Module 3 7 iMBA Example LBO TypeharshNo ratings yet

- Lang - Culculate Case StudyDocument6 pagesLang - Culculate Case StudyTrang ĐàiNo ratings yet

- Module-10 Additional Material FSA Template - Session-11 vrTcbcH4leDocument6 pagesModule-10 Additional Material FSA Template - Session-11 vrTcbcH4leBhavya PatelNo ratings yet

- TajvirDocument53 pagesTajvirTajbir Singh GillNo ratings yet

- Case StudyDocument6 pagesCase Studyrajan mishraNo ratings yet

- Ford FS PaiDocument13 pagesFord FS PaiAna Felna R. MirallesNo ratings yet

- Lecture - 5 - CFI-3-statement-model-completeDocument37 pagesLecture - 5 - CFI-3-statement-model-completeshreyasNo ratings yet

- Copia de Caso Healthy Bear 2022Document4 pagesCopia de Caso Healthy Bear 2022rataNo ratings yet

- AnandamDocument12 pagesAnandamNarinderNo ratings yet

- Ilovepdf MergedDocument4 pagesIlovepdf Mergedpahala edwardNo ratings yet

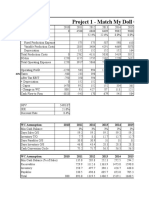

- Project 1 - Match My Doll Clothing Line: WC Assumption: 2010 2011 2012 2013 2014 2015Document4 pagesProject 1 - Match My Doll Clothing Line: WC Assumption: 2010 2011 2012 2013 2014 2015rohitNo ratings yet

- Airthread Acquisition: Income StatementDocument31 pagesAirthread Acquisition: Income StatementnidhidNo ratings yet

- Facts Given in The CaseDocument14 pagesFacts Given in The CaseYashasvi -No ratings yet

- Valuation PracticeDocument19 pagesValuation PracticeAkash PatilNo ratings yet

- AVIS CarsDocument10 pagesAVIS CarsSheikhFaizanUl-HaqueNo ratings yet

- Cost AssignmentDocument16 pagesCost Assignmentmuhammad salmanNo ratings yet

- Stock Analysis Excel Sheet MBPDocument69 pagesStock Analysis Excel Sheet MBPlakeshbeheraaaNo ratings yet

- Particulars 2021: Net SalesDocument17 pagesParticulars 2021: Net SalesSaloni Jain 1820343No ratings yet

- Atlas Honda: Financial ModellingDocument19 pagesAtlas Honda: Financial ModellingSaqib NasirNo ratings yet

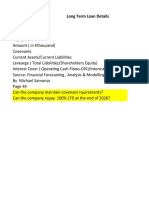

- Long Term Loan Details TermDocument67 pagesLong Term Loan Details TermPranjal GuptaNo ratings yet

- Session 11Document5 pagesSession 11samay gargNo ratings yet

- Bcel 2019Q1Document1 pageBcel 2019Q1Dương NguyễnNo ratings yet

- Apple RatiosDocument19 pagesApple RatiosJims Leñar CezarNo ratings yet

- New Heritage Doll Company Capital BudgetDocument10 pagesNew Heritage Doll Company Capital BudgetIris Belen Medina OrozcoNo ratings yet

- Results Results: in Millions of CHF (Except For Data Per Share and Employees)Document1 pageResults Results: in Millions of CHF (Except For Data Per Share and Employees)SibghaNo ratings yet

- IS, SOFP, SCE My WorkDocument6 pagesIS, SOFP, SCE My WorkoluwapelumiotunNo ratings yet

- Accounts AssignsmentDocument8 pagesAccounts Assignsmentadityatiwari8303No ratings yet

- Brief About The Co Brands Competitive Positioning of The Co / Advantages Tracking Points Financials Incl Shareholding Pattern Valuation Rational SwotDocument42 pagesBrief About The Co Brands Competitive Positioning of The Co / Advantages Tracking Points Financials Incl Shareholding Pattern Valuation Rational SwotMitesh PatilNo ratings yet

- Lecture 6 (05-10-2020) 1-10 To 2-30Document2 pagesLecture 6 (05-10-2020) 1-10 To 2-30Mahmood AhmadNo ratings yet

- K10 SFMDocument6 pagesK10 SFMSrijan AgarwalNo ratings yet

- Go Rural FM AssignmentDocument31 pagesGo Rural FM AssignmentHumphrey OsaigbeNo ratings yet

- 7 Ezeebuy SolutionDocument10 pages7 Ezeebuy SolutionRohan JindalNo ratings yet

- Project 1Document5 pagesProject 1Avengers HeroesNo ratings yet

- Taj Power TechDocument12 pagesTaj Power TechNujhat SharminNo ratings yet

- Chapter 2. Exhibits y AnexosDocument20 pagesChapter 2. Exhibits y AnexosJulio Arroyo GilNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Quiz 2 - Integrated Review AFARDocument9 pagesQuiz 2 - Integrated Review AFAROjims Christjohn C CadungganNo ratings yet

- Tata Ethical Fund March 2021Document18 pagesTata Ethical Fund March 2021Capitus L. L. PNo ratings yet

- Investment EvaluationDocument44 pagesInvestment Evaluationagung prawiraNo ratings yet

- Sap-C Ts4fi 2021Document38 pagesSap-C Ts4fi 2021xuewupsyNo ratings yet

- IFRS 5 Non Current Assets Held For SaleDocument8 pagesIFRS 5 Non Current Assets Held For Saleharir22No ratings yet

- Book NQN KeyDocument86 pagesBook NQN KeyQuỳnh Trần Thị DiễmNo ratings yet

- QUIZ 5 MidtermsDocument9 pagesQUIZ 5 MidtermsMa. Clovel MosasoNo ratings yet

- Account Movements DetailDocument2 pagesAccount Movements Detailandy sandoval guardiaNo ratings yet

- PRTC AUD 1stPB - 10.21Document15 pagesPRTC AUD 1stPB - 10.21Luna VNo ratings yet

- Activity 1Document7 pagesActivity 1Joanah TayamenNo ratings yet

- CASH - DN3260 - Ataur Rahman - 08 - 02 - 2023Document1 pageCASH - DN3260 - Ataur Rahman - 08 - 02 - 2023Ataur RahmanNo ratings yet

- Fundamental Analysis WorkbookDocument4 pagesFundamental Analysis WorkbookMuaz saleemNo ratings yet

- Value Determinants in Seed Stage SaaS ValuationsDocument100 pagesValue Determinants in Seed Stage SaaS Valuationsabsensi bplNo ratings yet

- Merchant Banking Cha-1 by Saidul AlamDocument3 pagesMerchant Banking Cha-1 by Saidul AlamSaidul AlamNo ratings yet

- Fundamentals of AccountingDocument2 pagesFundamentals of AccountingDiane SorianoNo ratings yet

- Fm-I Chap-V EditedDocument30 pagesFm-I Chap-V Editedtibebu5420No ratings yet

- Analisis Kinerja Keuangan PT - Bank Mandiri Syariah, TBK Periode 2016-2020 Menggunakan Metode Du Pont SystemDocument7 pagesAnalisis Kinerja Keuangan PT - Bank Mandiri Syariah, TBK Periode 2016-2020 Menggunakan Metode Du Pont SystemJasika Jurnal Sistem Informasi AkuntansiNo ratings yet

- BCA MAcc Question BankDocument14 pagesBCA MAcc Question BankpratimapatikaNo ratings yet

- 9 Business CombinationsDocument5 pages9 Business CombinationsChiro VillenaNo ratings yet

- Part 3 - Sale and LeasebackDocument11 pagesPart 3 - Sale and LeasebackPoru SenpiiNo ratings yet

- Pas 12Document5 pagesPas 12elle friasNo ratings yet

- 2023 Analyzing Firm PerformanceDocument29 pages2023 Analyzing Firm PerformanceNguyễn Xuân HoaNo ratings yet

- Share Based Payments ExercisesDocument5 pagesShare Based Payments ExercisesayhanacruzNo ratings yet

- Accounting For PartnershipDocument14 pagesAccounting For PartnershipSangeeta SadeoNo ratings yet

- Nykaa - Fundamental Technical AnalysisDocument6 pagesNykaa - Fundamental Technical Analysiskhyati kaulNo ratings yet

- DAYAG 2015 Installment SalesDocument9 pagesDAYAG 2015 Installment SalesChriz VillasNo ratings yet

- 10 02 Accretion Dilution PracticeDocument2 pages10 02 Accretion Dilution PracticePENG YinglunNo ratings yet

- Ifrs10 SNDocument5 pagesIfrs10 SNjohny SahaNo ratings yet

- Tutorial 1 - Financial Statement (Basic)Document6 pagesTutorial 1 - Financial Statement (Basic)danial kalNo ratings yet

- Agm Minutes enDocument10 pagesAgm Minutes enThomasNo ratings yet

Download as xls, pdf, or txt

You might also like

- Final Solution - New Heritage Doll CompanyDocument6 pagesFinal Solution - New Heritage Doll CompanyRehan Tyagi100% (2)

- Anandam Case Study - AFSDocument20 pagesAnandam Case Study - AFSSiddhesh Mahadik67% (3)

- Group6 - Heritage Doll CaseDocument6 pagesGroup6 - Heritage Doll Casesanket vermaNo ratings yet

- Simple LBODocument16 pagesSimple LBOsingh0001No ratings yet

- Corporate Finance Mini CaseDocument6 pagesCorporate Finance Mini CaseMashaal FNo ratings yet

- New Heritage Doll CompanDocument9 pagesNew Heritage Doll CompanArima ChatterjeeNo ratings yet

- Houzit Pty LTD: 1st Quarter Ended Sept - 2012 Actual Results Budget Q1 Actual Q1 $ VarianceDocument4 pagesHouzit Pty LTD: 1st Quarter Ended Sept - 2012 Actual Results Budget Q1 Actual Q1 $ VarianceHamza Anees100% (1)

- CFI 3 Statement Model Complete in ClassDocument10 pagesCFI 3 Statement Model Complete in ClassThiện NhânNo ratings yet

- Financials at GlanceDocument1 pageFinancials at GlanceSrikanth Marriboyanna MNo ratings yet

- gLLjeluWEem7ixL - 6m9HFg - PolyPanel TO DO Before WEEK 1Document2 pagesgLLjeluWEem7ixL - 6m9HFg - PolyPanel TO DO Before WEEK 1Mohammed Soliman MasliNo ratings yet

- Assignment - 1Document2 pagesAssignment - 1asfandyarkhaliq0% (1)

- Chapter 3. Exhibits y AnexosDocument24 pagesChapter 3. Exhibits y AnexosJulio Arroyo GilNo ratings yet

- CFM Lbo ModelDocument3 pagesCFM Lbo ModelReusNo ratings yet

- Demo File On ValuationDocument3 pagesDemo File On Valuationamaan khanNo ratings yet

- Financials at GlanceDocument1 pageFinancials at Glancekanwal23No ratings yet

- Balance Sheet: Total Equity and LiabilitiesDocument11 pagesBalance Sheet: Total Equity and LiabilitiesSamarth LahotiNo ratings yet

- A - Case Study: Dreaming Corp.: The Financial Statements of Dreaming Corp. Are The Following (In K )Document7 pagesA - Case Study: Dreaming Corp.: The Financial Statements of Dreaming Corp. Are The Following (In K )Mohamed Lamine SanohNo ratings yet

- Five Years' Financial Summary: REPORT 2015Document2 pagesFive Years' Financial Summary: REPORT 2015Rizwan ZisanNo ratings yet

- Key Figures (Euros, Thousands) - Source: Annual Reports 2005-2013Document10 pagesKey Figures (Euros, Thousands) - Source: Annual Reports 2005-2013Wassi Ademola MoudachirouNo ratings yet

- $ Million 2013 2012: Balance SheetDocument3 pages$ Million 2013 2012: Balance Sheetyash sarohaNo ratings yet

- Balance Sheet: Fast Sparrow IncDocument7 pagesBalance Sheet: Fast Sparrow Incmudassir rehmanNo ratings yet

- FM Assignment 02Document1 pageFM Assignment 02Sufyan SarwarNo ratings yet

- Mock Exam FRPM SolutionDocument45 pagesMock Exam FRPM SolutionangelitayosecasetiawanNo ratings yet

- S BqFC2 - T5KgahQtv8 SXQ - Module 3 7 iMBA Example LBO TypeDocument8 pagesS BqFC2 - T5KgahQtv8 SXQ - Module 3 7 iMBA Example LBO TypeharshNo ratings yet

- Lang - Culculate Case StudyDocument6 pagesLang - Culculate Case StudyTrang ĐàiNo ratings yet

- Module-10 Additional Material FSA Template - Session-11 vrTcbcH4leDocument6 pagesModule-10 Additional Material FSA Template - Session-11 vrTcbcH4leBhavya PatelNo ratings yet

- TajvirDocument53 pagesTajvirTajbir Singh GillNo ratings yet

- Case StudyDocument6 pagesCase Studyrajan mishraNo ratings yet

- Ford FS PaiDocument13 pagesFord FS PaiAna Felna R. MirallesNo ratings yet

- Lecture - 5 - CFI-3-statement-model-completeDocument37 pagesLecture - 5 - CFI-3-statement-model-completeshreyasNo ratings yet

- Copia de Caso Healthy Bear 2022Document4 pagesCopia de Caso Healthy Bear 2022rataNo ratings yet

- AnandamDocument12 pagesAnandamNarinderNo ratings yet

- Ilovepdf MergedDocument4 pagesIlovepdf Mergedpahala edwardNo ratings yet

- Project 1 - Match My Doll Clothing Line: WC Assumption: 2010 2011 2012 2013 2014 2015Document4 pagesProject 1 - Match My Doll Clothing Line: WC Assumption: 2010 2011 2012 2013 2014 2015rohitNo ratings yet

- Airthread Acquisition: Income StatementDocument31 pagesAirthread Acquisition: Income StatementnidhidNo ratings yet

- Facts Given in The CaseDocument14 pagesFacts Given in The CaseYashasvi -No ratings yet

- Valuation PracticeDocument19 pagesValuation PracticeAkash PatilNo ratings yet

- AVIS CarsDocument10 pagesAVIS CarsSheikhFaizanUl-HaqueNo ratings yet

- Cost AssignmentDocument16 pagesCost Assignmentmuhammad salmanNo ratings yet

- Stock Analysis Excel Sheet MBPDocument69 pagesStock Analysis Excel Sheet MBPlakeshbeheraaaNo ratings yet

- Particulars 2021: Net SalesDocument17 pagesParticulars 2021: Net SalesSaloni Jain 1820343No ratings yet

- Atlas Honda: Financial ModellingDocument19 pagesAtlas Honda: Financial ModellingSaqib NasirNo ratings yet

- Long Term Loan Details TermDocument67 pagesLong Term Loan Details TermPranjal GuptaNo ratings yet

- Session 11Document5 pagesSession 11samay gargNo ratings yet

- Bcel 2019Q1Document1 pageBcel 2019Q1Dương NguyễnNo ratings yet

- Apple RatiosDocument19 pagesApple RatiosJims Leñar CezarNo ratings yet

- New Heritage Doll Company Capital BudgetDocument10 pagesNew Heritage Doll Company Capital BudgetIris Belen Medina OrozcoNo ratings yet

- Results Results: in Millions of CHF (Except For Data Per Share and Employees)Document1 pageResults Results: in Millions of CHF (Except For Data Per Share and Employees)SibghaNo ratings yet

- IS, SOFP, SCE My WorkDocument6 pagesIS, SOFP, SCE My WorkoluwapelumiotunNo ratings yet

- Accounts AssignsmentDocument8 pagesAccounts Assignsmentadityatiwari8303No ratings yet

- Brief About The Co Brands Competitive Positioning of The Co / Advantages Tracking Points Financials Incl Shareholding Pattern Valuation Rational SwotDocument42 pagesBrief About The Co Brands Competitive Positioning of The Co / Advantages Tracking Points Financials Incl Shareholding Pattern Valuation Rational SwotMitesh PatilNo ratings yet

- Lecture 6 (05-10-2020) 1-10 To 2-30Document2 pagesLecture 6 (05-10-2020) 1-10 To 2-30Mahmood AhmadNo ratings yet

- K10 SFMDocument6 pagesK10 SFMSrijan AgarwalNo ratings yet

- Go Rural FM AssignmentDocument31 pagesGo Rural FM AssignmentHumphrey OsaigbeNo ratings yet

- 7 Ezeebuy SolutionDocument10 pages7 Ezeebuy SolutionRohan JindalNo ratings yet

- Project 1Document5 pagesProject 1Avengers HeroesNo ratings yet

- Taj Power TechDocument12 pagesTaj Power TechNujhat SharminNo ratings yet

- Chapter 2. Exhibits y AnexosDocument20 pagesChapter 2. Exhibits y AnexosJulio Arroyo GilNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Quiz 2 - Integrated Review AFARDocument9 pagesQuiz 2 - Integrated Review AFAROjims Christjohn C CadungganNo ratings yet

- Tata Ethical Fund March 2021Document18 pagesTata Ethical Fund March 2021Capitus L. L. PNo ratings yet

- Investment EvaluationDocument44 pagesInvestment Evaluationagung prawiraNo ratings yet

- Sap-C Ts4fi 2021Document38 pagesSap-C Ts4fi 2021xuewupsyNo ratings yet

- IFRS 5 Non Current Assets Held For SaleDocument8 pagesIFRS 5 Non Current Assets Held For Saleharir22No ratings yet

- Book NQN KeyDocument86 pagesBook NQN KeyQuỳnh Trần Thị DiễmNo ratings yet

- QUIZ 5 MidtermsDocument9 pagesQUIZ 5 MidtermsMa. Clovel MosasoNo ratings yet

- Account Movements DetailDocument2 pagesAccount Movements Detailandy sandoval guardiaNo ratings yet

- PRTC AUD 1stPB - 10.21Document15 pagesPRTC AUD 1stPB - 10.21Luna VNo ratings yet

- Activity 1Document7 pagesActivity 1Joanah TayamenNo ratings yet

- CASH - DN3260 - Ataur Rahman - 08 - 02 - 2023Document1 pageCASH - DN3260 - Ataur Rahman - 08 - 02 - 2023Ataur RahmanNo ratings yet

- Fundamental Analysis WorkbookDocument4 pagesFundamental Analysis WorkbookMuaz saleemNo ratings yet

- Value Determinants in Seed Stage SaaS ValuationsDocument100 pagesValue Determinants in Seed Stage SaaS Valuationsabsensi bplNo ratings yet

- Merchant Banking Cha-1 by Saidul AlamDocument3 pagesMerchant Banking Cha-1 by Saidul AlamSaidul AlamNo ratings yet

- Fundamentals of AccountingDocument2 pagesFundamentals of AccountingDiane SorianoNo ratings yet

- Fm-I Chap-V EditedDocument30 pagesFm-I Chap-V Editedtibebu5420No ratings yet

- Analisis Kinerja Keuangan PT - Bank Mandiri Syariah, TBK Periode 2016-2020 Menggunakan Metode Du Pont SystemDocument7 pagesAnalisis Kinerja Keuangan PT - Bank Mandiri Syariah, TBK Periode 2016-2020 Menggunakan Metode Du Pont SystemJasika Jurnal Sistem Informasi AkuntansiNo ratings yet

- BCA MAcc Question BankDocument14 pagesBCA MAcc Question BankpratimapatikaNo ratings yet

- 9 Business CombinationsDocument5 pages9 Business CombinationsChiro VillenaNo ratings yet

- Part 3 - Sale and LeasebackDocument11 pagesPart 3 - Sale and LeasebackPoru SenpiiNo ratings yet

- Pas 12Document5 pagesPas 12elle friasNo ratings yet

- 2023 Analyzing Firm PerformanceDocument29 pages2023 Analyzing Firm PerformanceNguyễn Xuân HoaNo ratings yet

- Share Based Payments ExercisesDocument5 pagesShare Based Payments ExercisesayhanacruzNo ratings yet

- Accounting For PartnershipDocument14 pagesAccounting For PartnershipSangeeta SadeoNo ratings yet

- Nykaa - Fundamental Technical AnalysisDocument6 pagesNykaa - Fundamental Technical Analysiskhyati kaulNo ratings yet

- DAYAG 2015 Installment SalesDocument9 pagesDAYAG 2015 Installment SalesChriz VillasNo ratings yet

- 10 02 Accretion Dilution PracticeDocument2 pages10 02 Accretion Dilution PracticePENG YinglunNo ratings yet

- Ifrs10 SNDocument5 pagesIfrs10 SNjohny SahaNo ratings yet

- Tutorial 1 - Financial Statement (Basic)Document6 pagesTutorial 1 - Financial Statement (Basic)danial kalNo ratings yet

- Agm Minutes enDocument10 pagesAgm Minutes enThomasNo ratings yet