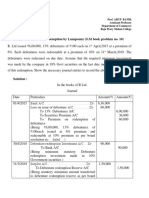

Accounting For Share Capital: Issue, Forfeiture and Re-Issue of Shares

Accounting For Share Capital: Issue, Forfeiture and Re-Issue of Shares

You might also like

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Corporate AccountingDocument79 pagesCorporate Accountingakshrajput2005No ratings yet

- FA Special 2010Document10 pagesFA Special 2010prakash9735No ratings yet

- 12 Accountancy Lyp 2017 Delhi Set1 PDFDocument39 pages12 Accountancy Lyp 2017 Delhi Set1 PDFAshish GangwalNo ratings yet

- Wa0001.Document7 pagesWa0001.akash dasNo ratings yet

- Issue of SharesDocument11 pagesIssue of SharesRamesh KumarNo ratings yet

- Company AccountDocument21 pagesCompany AccountAbhishek BaliarsinghNo ratings yet

- Worksheet On Issue of Debenture - Board QuestionsDocument12 pagesWorksheet On Issue of Debenture - Board QuestionsCfa Deepti BindalNo ratings yet

- Calls in AdvanceDocument14 pagesCalls in AdvanceShruti GoswamiNo ratings yet

- HA2032Document12 pagesHA2032Aayam SubediNo ratings yet

- Problem - 2 (Redemption by Lumpsum) (S.M Book Problem No. 10)Document5 pagesProblem - 2 (Redemption by Lumpsum) (S.M Book Problem No. 10)Gopal DasNo ratings yet

- TrailDocument6 pagesTrailNaman agrawalNo ratings yet

- Share Cap AccountDocument14 pagesShare Cap Accountsauravmedhi7890No ratings yet

- K VJa Pfa CYOae 91 JFTLNCDocument17 pagesK VJa Pfa CYOae 91 JFTLNCAshwin MurthyNo ratings yet

- Issue of Equity Shares Syllabus:: Call in Advance/ Calls in Arrears, Forfeiture and Re Issue of Forfeited SharesDocument8 pagesIssue of Equity Shares Syllabus:: Call in Advance/ Calls in Arrears, Forfeiture and Re Issue of Forfeited SharesMubin Shaikh NooruNo ratings yet

- Company Acc Test SolDocument11 pagesCompany Acc Test Solajay005panditNo ratings yet

- Company Accounts - Issue of DebenturesDocument5 pagesCompany Accounts - Issue of DebenturesPavithra AnupNo ratings yet

- Issue of SharesDocument24 pagesIssue of SharesManasNo ratings yet

- Sample Paper 5 (Final Exam XI Accountancy)Document9 pagesSample Paper 5 (Final Exam XI Accountancy)pritanshutripathi84No ratings yet

- Company Accounts - Issue of DebenturesDocument11 pagesCompany Accounts - Issue of DebenturesHarsh MishraNo ratings yet

- Accounting For Shares NewDocument24 pagesAccounting For Shares NewSteve NtefulNo ratings yet

- Paper 12-Company Accounts & Audit: Suggested Answers - Syl 2016 - December 2019 - Paper 12Document19 pagesPaper 12-Company Accounts & Audit: Suggested Answers - Syl 2016 - December 2019 - Paper 12Sannu VijayeendraNo ratings yet

- Xii Accountancy Question Bank 1Document46 pagesXii Accountancy Question Bank 1KavoNo ratings yet

- Issue of DebenturesDocument12 pagesIssue of Debenturessiva883100% (1)

- Work Sheet On Accounting For Share Capital Board Exam Questions Fro 2016-2020Document22 pagesWork Sheet On Accounting For Share Capital Board Exam Questions Fro 2016-2020Cfa Deepti BindalNo ratings yet

- Isc 2017 BQPDocument25 pagesIsc 2017 BQPPANKAJ's ACCOUNTANCY PATHSHALANo ratings yet

- Aidcom Financial Accounting AnalysisDocument17 pagesAidcom Financial Accounting AnalysisAjmal K HussainNo ratings yet

- Accounting of SharesDocument2 pagesAccounting of SharesDipali PatilNo ratings yet

- Issue of Shares With PremiumDocument4 pagesIssue of Shares With PremiumPankaj KandpalNo ratings yet

- In The Books of A & B Co. LTD.: Journal Entries Date Sr. No. Particulars L.FDocument2 pagesIn The Books of A & B Co. LTD.: Journal Entries Date Sr. No. Particulars L.FIsha KatiyarNo ratings yet

- Financial Accounting AssignentDocument8 pagesFinancial Accounting AssignentHitesh LodayaNo ratings yet

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- Shares & Debentures TestDocument10 pagesShares & Debentures TestAthul Krishna KNo ratings yet

- Issue of SharesDocument11 pagesIssue of SharesSNEHA GUINNo ratings yet

- Question Paper 2016 All India Set 1 Cbse Class 12 AccountancyDocument38 pagesQuestion Paper 2016 All India Set 1 Cbse Class 12 AccountancyAshish GangwalNo ratings yet

- Shares Issued at Premium & DiscountDocument13 pagesShares Issued at Premium & DiscountAwab HamidNo ratings yet

- Caa Assignment SolutionsDocument39 pagesCaa Assignment Solutionschikanesakshi2001No ratings yet

- 12 Accountancy Lyp 2017 Outside Delhi Set3Document42 pages12 Accountancy Lyp 2017 Outside Delhi Set3Ramprasad Sarkar100% (1)

- Redemption of DebenturesDocument16 pagesRedemption of Debenturespratik.kotechaNo ratings yet

- Recapulitation: Collaborating TechniqueDocument6 pagesRecapulitation: Collaborating TechniqueayeshaNo ratings yet

- Pre-Board 22-23 PDFDocument13 pagesPre-Board 22-23 PDFAdrian D'souzaNo ratings yet

- Corporate Accounting Chapter - 8 - Redemption of Debentures: (Notes Compiled by Dr. RUCHIKA KAURA)Document6 pagesCorporate Accounting Chapter - 8 - Redemption of Debentures: (Notes Compiled by Dr. RUCHIKA KAURA)RioNo ratings yet

- Corporate Accounting NotesDocument78 pagesCorporate Accounting NotesdivyanshuNo ratings yet

- Shaares Q With Sol.Document2 pagesShaares Q With Sol.Pankaj KandpalNo ratings yet

- Sample Paper 14 CBSE Accountancy Class 12: Install NODIA App To See The Solutions. Click Here To InstallDocument45 pagesSample Paper 14 CBSE Accountancy Class 12: Install NODIA App To See The Solutions. Click Here To Installumangsingh054No ratings yet

- Conversion or Sale of Partnership Firm Into Limited CompanyDocument24 pagesConversion or Sale of Partnership Firm Into Limited CompanyMadhav TailorNo ratings yet

- CA-II May 2022 SchemeDocument15 pagesCA-II May 2022 SchemeZeroNo ratings yet

- Class Activity - JournalDocument4 pagesClass Activity - JournalKhem Raj GyawaliNo ratings yet

- Sample Paperpre Board II Acct 2324-2Document10 pagesSample Paperpre Board II Acct 2324-2kanakchauhan206No ratings yet

- Issue of ShareDocument3 pagesIssue of ShareSayeed AnwarNo ratings yet

- 12 Accountancy sp10Document26 pages12 Accountancy sp10Akshat AgarwalNo ratings yet

- +1 Accountancy ONLINE Final Examination 2021Document5 pages+1 Accountancy ONLINE Final Examination 2021Rajwinder BansalNo ratings yet

- 67 1 1 Accountancy MsDocument12 pages67 1 1 Accountancy MsEric PottsNo ratings yet

- Issue and Forfeiture and Reissued of SharesDocument59 pagesIssue and Forfeiture and Reissued of Sharesvidhya_yog100% (3)

- 17269pe2 Sugg June09 1 PDFDocument22 pages17269pe2 Sugg June09 1 PDFSahil GoyalNo ratings yet

- Chapter 8-Accounting For Share CapitalDocument5 pagesChapter 8-Accounting For Share Capitalshiv RaghuwanshiNo ratings yet

- Chapter - 7: Case/Source Based Questions:: Kvs Ziet Bhubaneswar 12/10/2021Document18 pagesChapter - 7: Case/Source Based Questions:: Kvs Ziet Bhubaneswar 12/10/2021abiNo ratings yet

- Effective Project Financing Essential Principles And Tactics: An Introduction To Finance, Cash Flows, And Project EvaluationFrom EverandEffective Project Financing Essential Principles And Tactics: An Introduction To Finance, Cash Flows, And Project EvaluationNo ratings yet

- Course Outline HRM 302Document2 pagesCourse Outline HRM 302nogarap767No ratings yet

- Statements 20230714Document6 pagesStatements 20230714Sima KadirNo ratings yet

- An Overview of Banks and Financial Sector Service.Document22 pagesAn Overview of Banks and Financial Sector Service.Mahmudur RahmanNo ratings yet

- Agent Bank Presentation PilotDocument111 pagesAgent Bank Presentation Pilotchimdesa TolesaNo ratings yet

- Card Overview FinalDocument70 pagesCard Overview Finalnhatchau76496No ratings yet

- Fabm1 WK 3 Session 1 Rules of Debit and CreditDocument26 pagesFabm1 WK 3 Session 1 Rules of Debit and CreditDomingo Princess JoyNo ratings yet

- CA Final Advanced Auditing Professional Ethics Important QuestionsDocument7 pagesCA Final Advanced Auditing Professional Ethics Important QuestionsSrinivasan KrishnanNo ratings yet

- A Presentation On Alcar Approach of Value Based NewDocument10 pagesA Presentation On Alcar Approach of Value Based NewMoinuddin FahadNo ratings yet

- X SF STD InvDocument1 pageX SF STD InvABDUL GHAFARNo ratings yet

- CHAPTER 2 StudentDocument10 pagesCHAPTER 2 Studentfelicia tanNo ratings yet

- Income Statement (T-Format)Document15 pagesIncome Statement (T-Format)Apryl TaiNo ratings yet

- International Economics IIDocument237 pagesInternational Economics IImeghasunil24No ratings yet

- Module11 - Personal-Finance - Primeiros 2 CapsDocument35 pagesModule11 - Personal-Finance - Primeiros 2 CapsRafael AndréNo ratings yet

- The Foreclosure Secrets GuideDocument146 pagesThe Foreclosure Secrets GuideAkil BeyNo ratings yet

- ElementsBookKeepingAccountancy SQPDocument6 pagesElementsBookKeepingAccountancy SQPMohd JamaluddinNo ratings yet

- Service Request FormDocument2 pagesService Request FormKowshik ChakrabortyNo ratings yet

- Cash Book TestDocument9 pagesCash Book TesttanishaNo ratings yet

- Book 2Document2 pagesBook 2Khang TrầnNo ratings yet

- Oke Management of Petty Cash FundDocument14 pagesOke Management of Petty Cash FundulaNo ratings yet

- Meaning of NBFCDocument30 pagesMeaning of NBFCRaj SakpalNo ratings yet

- 11 Accountancy Notes ch04 Preparation of Ledger Trial Balance and Bank Reconciliation Statement 02 PDFDocument30 pages11 Accountancy Notes ch04 Preparation of Ledger Trial Balance and Bank Reconciliation Statement 02 PDFVigneshNo ratings yet

- Tutorial 9 FMTDocument5 pagesTutorial 9 FMTNguyễn Vĩnh TháiNo ratings yet

- Auditing ProblemsDocument25 pagesAuditing ProblemsJane DizonNo ratings yet

- CH 05Document99 pagesCH 05Reinch Closs100% (1)

- What Are The Pros and Cons of Investing in The Money Market?Document3 pagesWhat Are The Pros and Cons of Investing in The Money Market?Franciska AdeliaNo ratings yet

- EAB 30703 FAR 4 - Question - Mid Term (OCT 2023)Document4 pagesEAB 30703 FAR 4 - Question - Mid Term (OCT 2023)Umairah HusnaNo ratings yet

- IIFM Sukuk Report 2023Document202 pagesIIFM Sukuk Report 2023আলোর ফেরিওয়ালাNo ratings yet

- CL Exercises SolutionDocument32 pagesCL Exercises SolutionJas AlbosNo ratings yet

- 1577786160969BcF9eaIss9xkmGva PDFDocument10 pages1577786160969BcF9eaIss9xkmGva PDFGovarthanan GopalanNo ratings yet

- Fcohhnte XXX Bic Swift Code - Banco Financiera Comercial Hondurena S.A. (Banco Ficohsa) Honduras - WiseDocument1 pageFcohhnte XXX Bic Swift Code - Banco Financiera Comercial Hondurena S.A. (Banco Ficohsa) Honduras - Wisejudithdelgado492No ratings yet

Download as pdf or txt

You might also like

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Corporate AccountingDocument79 pagesCorporate Accountingakshrajput2005No ratings yet

- FA Special 2010Document10 pagesFA Special 2010prakash9735No ratings yet

- 12 Accountancy Lyp 2017 Delhi Set1 PDFDocument39 pages12 Accountancy Lyp 2017 Delhi Set1 PDFAshish GangwalNo ratings yet

- Wa0001.Document7 pagesWa0001.akash dasNo ratings yet

- Issue of SharesDocument11 pagesIssue of SharesRamesh KumarNo ratings yet

- Company AccountDocument21 pagesCompany AccountAbhishek BaliarsinghNo ratings yet

- Worksheet On Issue of Debenture - Board QuestionsDocument12 pagesWorksheet On Issue of Debenture - Board QuestionsCfa Deepti BindalNo ratings yet

- Calls in AdvanceDocument14 pagesCalls in AdvanceShruti GoswamiNo ratings yet

- HA2032Document12 pagesHA2032Aayam SubediNo ratings yet

- Problem - 2 (Redemption by Lumpsum) (S.M Book Problem No. 10)Document5 pagesProblem - 2 (Redemption by Lumpsum) (S.M Book Problem No. 10)Gopal DasNo ratings yet

- TrailDocument6 pagesTrailNaman agrawalNo ratings yet

- Share Cap AccountDocument14 pagesShare Cap Accountsauravmedhi7890No ratings yet

- K VJa Pfa CYOae 91 JFTLNCDocument17 pagesK VJa Pfa CYOae 91 JFTLNCAshwin MurthyNo ratings yet

- Issue of Equity Shares Syllabus:: Call in Advance/ Calls in Arrears, Forfeiture and Re Issue of Forfeited SharesDocument8 pagesIssue of Equity Shares Syllabus:: Call in Advance/ Calls in Arrears, Forfeiture and Re Issue of Forfeited SharesMubin Shaikh NooruNo ratings yet

- Company Acc Test SolDocument11 pagesCompany Acc Test Solajay005panditNo ratings yet

- Company Accounts - Issue of DebenturesDocument5 pagesCompany Accounts - Issue of DebenturesPavithra AnupNo ratings yet

- Issue of SharesDocument24 pagesIssue of SharesManasNo ratings yet

- Sample Paper 5 (Final Exam XI Accountancy)Document9 pagesSample Paper 5 (Final Exam XI Accountancy)pritanshutripathi84No ratings yet

- Company Accounts - Issue of DebenturesDocument11 pagesCompany Accounts - Issue of DebenturesHarsh MishraNo ratings yet

- Accounting For Shares NewDocument24 pagesAccounting For Shares NewSteve NtefulNo ratings yet

- Paper 12-Company Accounts & Audit: Suggested Answers - Syl 2016 - December 2019 - Paper 12Document19 pagesPaper 12-Company Accounts & Audit: Suggested Answers - Syl 2016 - December 2019 - Paper 12Sannu VijayeendraNo ratings yet

- Xii Accountancy Question Bank 1Document46 pagesXii Accountancy Question Bank 1KavoNo ratings yet

- Issue of DebenturesDocument12 pagesIssue of Debenturessiva883100% (1)

- Work Sheet On Accounting For Share Capital Board Exam Questions Fro 2016-2020Document22 pagesWork Sheet On Accounting For Share Capital Board Exam Questions Fro 2016-2020Cfa Deepti BindalNo ratings yet

- Isc 2017 BQPDocument25 pagesIsc 2017 BQPPANKAJ's ACCOUNTANCY PATHSHALANo ratings yet

- Aidcom Financial Accounting AnalysisDocument17 pagesAidcom Financial Accounting AnalysisAjmal K HussainNo ratings yet

- Accounting of SharesDocument2 pagesAccounting of SharesDipali PatilNo ratings yet

- Issue of Shares With PremiumDocument4 pagesIssue of Shares With PremiumPankaj KandpalNo ratings yet

- In The Books of A & B Co. LTD.: Journal Entries Date Sr. No. Particulars L.FDocument2 pagesIn The Books of A & B Co. LTD.: Journal Entries Date Sr. No. Particulars L.FIsha KatiyarNo ratings yet

- Financial Accounting AssignentDocument8 pagesFinancial Accounting AssignentHitesh LodayaNo ratings yet

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- Shares & Debentures TestDocument10 pagesShares & Debentures TestAthul Krishna KNo ratings yet

- Issue of SharesDocument11 pagesIssue of SharesSNEHA GUINNo ratings yet

- Question Paper 2016 All India Set 1 Cbse Class 12 AccountancyDocument38 pagesQuestion Paper 2016 All India Set 1 Cbse Class 12 AccountancyAshish GangwalNo ratings yet

- Shares Issued at Premium & DiscountDocument13 pagesShares Issued at Premium & DiscountAwab HamidNo ratings yet

- Caa Assignment SolutionsDocument39 pagesCaa Assignment Solutionschikanesakshi2001No ratings yet

- 12 Accountancy Lyp 2017 Outside Delhi Set3Document42 pages12 Accountancy Lyp 2017 Outside Delhi Set3Ramprasad Sarkar100% (1)

- Redemption of DebenturesDocument16 pagesRedemption of Debenturespratik.kotechaNo ratings yet

- Recapulitation: Collaborating TechniqueDocument6 pagesRecapulitation: Collaborating TechniqueayeshaNo ratings yet

- Pre-Board 22-23 PDFDocument13 pagesPre-Board 22-23 PDFAdrian D'souzaNo ratings yet

- Corporate Accounting Chapter - 8 - Redemption of Debentures: (Notes Compiled by Dr. RUCHIKA KAURA)Document6 pagesCorporate Accounting Chapter - 8 - Redemption of Debentures: (Notes Compiled by Dr. RUCHIKA KAURA)RioNo ratings yet

- Corporate Accounting NotesDocument78 pagesCorporate Accounting NotesdivyanshuNo ratings yet

- Shaares Q With Sol.Document2 pagesShaares Q With Sol.Pankaj KandpalNo ratings yet

- Sample Paper 14 CBSE Accountancy Class 12: Install NODIA App To See The Solutions. Click Here To InstallDocument45 pagesSample Paper 14 CBSE Accountancy Class 12: Install NODIA App To See The Solutions. Click Here To Installumangsingh054No ratings yet

- Conversion or Sale of Partnership Firm Into Limited CompanyDocument24 pagesConversion or Sale of Partnership Firm Into Limited CompanyMadhav TailorNo ratings yet

- CA-II May 2022 SchemeDocument15 pagesCA-II May 2022 SchemeZeroNo ratings yet

- Class Activity - JournalDocument4 pagesClass Activity - JournalKhem Raj GyawaliNo ratings yet

- Sample Paperpre Board II Acct 2324-2Document10 pagesSample Paperpre Board II Acct 2324-2kanakchauhan206No ratings yet

- Issue of ShareDocument3 pagesIssue of ShareSayeed AnwarNo ratings yet

- 12 Accountancy sp10Document26 pages12 Accountancy sp10Akshat AgarwalNo ratings yet

- +1 Accountancy ONLINE Final Examination 2021Document5 pages+1 Accountancy ONLINE Final Examination 2021Rajwinder BansalNo ratings yet

- 67 1 1 Accountancy MsDocument12 pages67 1 1 Accountancy MsEric PottsNo ratings yet

- Issue and Forfeiture and Reissued of SharesDocument59 pagesIssue and Forfeiture and Reissued of Sharesvidhya_yog100% (3)

- 17269pe2 Sugg June09 1 PDFDocument22 pages17269pe2 Sugg June09 1 PDFSahil GoyalNo ratings yet

- Chapter 8-Accounting For Share CapitalDocument5 pagesChapter 8-Accounting For Share Capitalshiv RaghuwanshiNo ratings yet

- Chapter - 7: Case/Source Based Questions:: Kvs Ziet Bhubaneswar 12/10/2021Document18 pagesChapter - 7: Case/Source Based Questions:: Kvs Ziet Bhubaneswar 12/10/2021abiNo ratings yet

- Effective Project Financing Essential Principles And Tactics: An Introduction To Finance, Cash Flows, And Project EvaluationFrom EverandEffective Project Financing Essential Principles And Tactics: An Introduction To Finance, Cash Flows, And Project EvaluationNo ratings yet

- Course Outline HRM 302Document2 pagesCourse Outline HRM 302nogarap767No ratings yet

- Statements 20230714Document6 pagesStatements 20230714Sima KadirNo ratings yet

- An Overview of Banks and Financial Sector Service.Document22 pagesAn Overview of Banks and Financial Sector Service.Mahmudur RahmanNo ratings yet

- Agent Bank Presentation PilotDocument111 pagesAgent Bank Presentation Pilotchimdesa TolesaNo ratings yet

- Card Overview FinalDocument70 pagesCard Overview Finalnhatchau76496No ratings yet

- Fabm1 WK 3 Session 1 Rules of Debit and CreditDocument26 pagesFabm1 WK 3 Session 1 Rules of Debit and CreditDomingo Princess JoyNo ratings yet

- CA Final Advanced Auditing Professional Ethics Important QuestionsDocument7 pagesCA Final Advanced Auditing Professional Ethics Important QuestionsSrinivasan KrishnanNo ratings yet

- A Presentation On Alcar Approach of Value Based NewDocument10 pagesA Presentation On Alcar Approach of Value Based NewMoinuddin FahadNo ratings yet

- X SF STD InvDocument1 pageX SF STD InvABDUL GHAFARNo ratings yet

- CHAPTER 2 StudentDocument10 pagesCHAPTER 2 Studentfelicia tanNo ratings yet

- Income Statement (T-Format)Document15 pagesIncome Statement (T-Format)Apryl TaiNo ratings yet

- International Economics IIDocument237 pagesInternational Economics IImeghasunil24No ratings yet

- Module11 - Personal-Finance - Primeiros 2 CapsDocument35 pagesModule11 - Personal-Finance - Primeiros 2 CapsRafael AndréNo ratings yet

- The Foreclosure Secrets GuideDocument146 pagesThe Foreclosure Secrets GuideAkil BeyNo ratings yet

- ElementsBookKeepingAccountancy SQPDocument6 pagesElementsBookKeepingAccountancy SQPMohd JamaluddinNo ratings yet

- Service Request FormDocument2 pagesService Request FormKowshik ChakrabortyNo ratings yet

- Cash Book TestDocument9 pagesCash Book TesttanishaNo ratings yet

- Book 2Document2 pagesBook 2Khang TrầnNo ratings yet

- Oke Management of Petty Cash FundDocument14 pagesOke Management of Petty Cash FundulaNo ratings yet

- Meaning of NBFCDocument30 pagesMeaning of NBFCRaj SakpalNo ratings yet

- 11 Accountancy Notes ch04 Preparation of Ledger Trial Balance and Bank Reconciliation Statement 02 PDFDocument30 pages11 Accountancy Notes ch04 Preparation of Ledger Trial Balance and Bank Reconciliation Statement 02 PDFVigneshNo ratings yet

- Tutorial 9 FMTDocument5 pagesTutorial 9 FMTNguyễn Vĩnh TháiNo ratings yet

- Auditing ProblemsDocument25 pagesAuditing ProblemsJane DizonNo ratings yet

- CH 05Document99 pagesCH 05Reinch Closs100% (1)

- What Are The Pros and Cons of Investing in The Money Market?Document3 pagesWhat Are The Pros and Cons of Investing in The Money Market?Franciska AdeliaNo ratings yet

- EAB 30703 FAR 4 - Question - Mid Term (OCT 2023)Document4 pagesEAB 30703 FAR 4 - Question - Mid Term (OCT 2023)Umairah HusnaNo ratings yet

- IIFM Sukuk Report 2023Document202 pagesIIFM Sukuk Report 2023আলোর ফেরিওয়ালাNo ratings yet

- CL Exercises SolutionDocument32 pagesCL Exercises SolutionJas AlbosNo ratings yet

- 1577786160969BcF9eaIss9xkmGva PDFDocument10 pages1577786160969BcF9eaIss9xkmGva PDFGovarthanan GopalanNo ratings yet

- Fcohhnte XXX Bic Swift Code - Banco Financiera Comercial Hondurena S.A. (Banco Ficohsa) Honduras - WiseDocument1 pageFcohhnte XXX Bic Swift Code - Banco Financiera Comercial Hondurena S.A. (Banco Ficohsa) Honduras - Wisejudithdelgado492No ratings yet