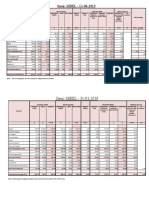

IFBL Oats Cost Model Comparison Statement Draft V1 24.4.24

IFBL Oats Cost Model Comparison Statement Draft V1 24.4.24

You might also like

- Pestle Analysis of Hero Motocorp Case Study HelpDocument24 pagesPestle Analysis of Hero Motocorp Case Study HelpRENUKA THOTENo ratings yet

- PSPCL Bill 3001167479 Due On 2023-JAN-02Document2 pagesPSPCL Bill 3001167479 Due On 2023-JAN-02EKAMPREET KAURNo ratings yet

- UGG ValuationDocument7 pagesUGG ValuationPritam KarmakarNo ratings yet

- Intuit ValuationDocument4 pagesIntuit ValuationcorvettejrwNo ratings yet

- Dabur - ERPDocument20 pagesDabur - ERPavradeepmallik0% (1)

- Management Professional Competence Suggested Answers PAC Mock-Winter 2019Document17 pagesManagement Professional Competence Suggested Answers PAC Mock-Winter 2019Ismail yousufNo ratings yet

- 2MBA Business PlanDocument23 pages2MBA Business PlanJonathan BravoNo ratings yet

- Castrol Bike PointDocument4 pagesCastrol Bike PointVishnu Kant100% (1)

- Customs Duty: 1) Trisha Company Imported A Machine From Europe. From The FollowingDocument32 pagesCustoms Duty: 1) Trisha Company Imported A Machine From Europe. From The FollowingAneesh D'souzaNo ratings yet

- Import Cost CalculationDocument3 pagesImport Cost CalculationNayem UddinNo ratings yet

- Calculations For VE Cost Advantage Note: VE by Change of Norms / SpecificationsDocument4 pagesCalculations For VE Cost Advantage Note: VE by Change of Norms / Specificationsjigyesh sharmaNo ratings yet

- Project: PI Value USD $Document11 pagesProject: PI Value USD $Zahangir KabirNo ratings yet

- Valuation Mergers ProjectDocument3 pagesValuation Mergers Projectsuraj nairNo ratings yet

- Sarni-MBEL - 13-08-2019: Contract Value Bill Processed Payment Made Balance and LD Bills PendingDocument2 pagesSarni-MBEL - 13-08-2019: Contract Value Bill Processed Payment Made Balance and LD Bills PendingRuby masandNo ratings yet

- Rate Analysis BarracksDocument217 pagesRate Analysis BarracksIftikhar AhmadNo ratings yet

- Bill of Supply For Electricity: Due Date: 09-10-2021Document1 pageBill of Supply For Electricity: Due Date: 09-10-2021Khushwant SinghNo ratings yet

- Presentation Preliminary Results For Q1 2022Document8 pagesPresentation Preliminary Results For Q1 2022Manikanta rajaNo ratings yet

- Microsoft Vs Intuit ValuationDocument4 pagesMicrosoft Vs Intuit ValuationcorvettejrwNo ratings yet

- Packet - Ii: Signature Not Verified Signature Not Verified Signature Not VerifiedDocument3 pagesPacket - Ii: Signature Not Verified Signature Not Verified Signature Not VerifiedJaimin PopatNo ratings yet

- Bill of Supply For Electricity: Due Date: 04-10-2021Document1 pageBill of Supply For Electricity: Due Date: 04-10-2021Divya Prakash0% (1)

- Microsoft ValuationDocument4 pagesMicrosoft ValuationcorvettejrwNo ratings yet

- PSPCL Bill 3015013843 Due On 2020-JUN-08Document2 pagesPSPCL Bill 3015013843 Due On 2020-JUN-08RitishNo ratings yet

- Bill of Supply For Electricity (Amended) Due Date: - : BSES Yamuna Power LTDDocument1 pageBill of Supply For Electricity (Amended) Due Date: - : BSES Yamuna Power LTDArman Khan100% (1)

- D Hps UE Rp/hour) : Factor X Delivered Price X Annual Rates Annual Use in Hours RP / Hours)Document3 pagesD Hps UE Rp/hour) : Factor X Delivered Price X Annual Rates Annual Use in Hours RP / Hours)suhadi wahanaNo ratings yet

- PSPCL Bill 3002105108 Due On 2021-JUL-01Document1 pagePSPCL Bill 3002105108 Due On 2021-JUL-01Parvinder SinghNo ratings yet

- 70 06 Reserves To Statements AfterDocument4 pages70 06 Reserves To Statements Aftermerag76668No ratings yet

- AssignmentDocument5 pagesAssignmentSanchay BhararaNo ratings yet

- BOK ValuationDocument7 pagesBOK ValuationsuryagcNo ratings yet

- PSPCL Bill 3008440296 due on 2024-FEB-09Document2 pagesPSPCL Bill 3008440296 due on 2024-FEB-09TusharNo ratings yet

- Bill of Supply For Electricity: Due Date: 02-07-2022Document2 pagesBill of Supply For Electricity: Due Date: 02-07-2022QSEKCERT FSSAI0% (1)

- Revision Excel SheetsDocument9 pagesRevision Excel SheetsPhan Phúc NguyênNo ratings yet

- Description: Crushed Aggregate Sub-Base Course Ref No - 12.03 S.N. Description Unit Quantity Rate Amount in Nrs Remarks Nrs. Nrs. Unit: MDocument2 pagesDescription: Crushed Aggregate Sub-Base Course Ref No - 12.03 S.N. Description Unit Quantity Rate Amount in Nrs Remarks Nrs. Nrs. Unit: MLamichhane SauravNo ratings yet

- Design & Engineering: 3 RAB:25 1 3 RAB:25 1 3 RAB:25 1 True True True RAB:25 True True RAB:25 True True RAB:25 True TrueDocument1 pageDesign & Engineering: 3 RAB:25 1 3 RAB:25 1 3 RAB:25 1 True True True RAB:25 True True RAB:25 True True RAB:25 True TrueRinjumon RinjuNo ratings yet

- Final Assessment BillDocument1 pageFinal Assessment Billbcaabaaba0321No ratings yet

- Annual Fixed Cost, P/Yr FC D+I+Hti: Net Income Generated, Ph/Yr Ni (Co - Ra-Dca) Ca OpDocument14 pagesAnnual Fixed Cost, P/Yr FC D+I+Hti: Net Income Generated, Ph/Yr Ni (Co - Ra-Dca) Ca OpJan James GrazaNo ratings yet

- Willmeng GMP Fire Station #9 Extracted Cost PagesDocument6 pagesWillmeng GMP Fire Station #9 Extracted Cost PagesJimmyNo ratings yet

- GAOC Option 2Document2 pagesGAOC Option 2Amit PhadatareNo ratings yet

- Bill of Supply For Electricity Due Date: 12-09-2022: BSES Rajdhani Power LTDDocument1 pageBill of Supply For Electricity Due Date: 12-09-2022: BSES Rajdhani Power LTDNand Kishor100% (1)

- Sourses of Funds: Balance Sheet 2010 2009Document4 pagesSourses of Funds: Balance Sheet 2010 2009Deven PipaliaNo ratings yet

- Sample Sheet - Make Input On ThisDocument5 pagesSample Sheet - Make Input On ThisHelp YourselfNo ratings yet

- CERC Latest RegulationDocument26 pagesCERC Latest RegulationShubham ChaurasiaNo ratings yet

- F. EstimateDocument45 pagesF. Estimateanthropolozist entertainNo ratings yet

- Duty Calculation: Description Tariff Rate Amt. RefDocument16 pagesDuty Calculation: Description Tariff Rate Amt. RefgargshashankNo ratings yet

- D RKQ VGKDW Ca O1669099523586Document1 pageD RKQ VGKDW Ca O1669099523586Vedans Finances100% (1)

- Bill of Supply For Electricity: Due Date: 11-08-2022Document2 pagesBill of Supply For Electricity: Due Date: 11-08-2022Naitik GoelNo ratings yet

- PSPCL SoniyaDocument2 pagesPSPCL SoniyaJashanpreet SinghNo ratings yet

- PSPCL Bill 3002769928 Due On 2022-NOV-16Document2 pagesPSPCL Bill 3002769928 Due On 2022-NOV-16Rocky SonipatNo ratings yet

- PSPCL Bill 3002769928 Due On 2022-NOV-16Document2 pagesPSPCL Bill 3002769928 Due On 2022-NOV-16Rocky SonipatNo ratings yet

- PSPCL Bill 3002769928 Due On 2022-NOV-16Document2 pagesPSPCL Bill 3002769928 Due On 2022-NOV-16Rocky SonipatNo ratings yet

- PSPCL Bill 3002769928 Due On 2022-NOV-16Document2 pagesPSPCL Bill 3002769928 Due On 2022-NOV-16Rocky SonipatNo ratings yet

- PSPCL Bill 3002769928 Due On 2022-NOV-16Document2 pagesPSPCL Bill 3002769928 Due On 2022-NOV-16Rocky SonipatNo ratings yet

- Bill of Supply For Electricity: Due Date: 13-08-2022Document1 pageBill of Supply For Electricity: Due Date: 13-08-2022Aadit SK100% (1)

- S6 E Working FinalDocument9 pagesS6 E Working FinalROHIT PANDEYNo ratings yet

- Bill of Supply For Electricity: Due Date: 15-02-2022Document2 pagesBill of Supply For Electricity: Due Date: 15-02-2022Shamshad KhanNo ratings yet

- Transmission Corporation of Telangana Limited: 1 132Kv Lingampet-Minpur Line Loc No 69/11Document5 pagesTransmission Corporation of Telangana Limited: 1 132Kv Lingampet-Minpur Line Loc No 69/11Boddu ThirupathiNo ratings yet

- Amended BoQ ContractDocument53 pagesAmended BoQ ContractFikadu KassaNo ratings yet

- Project Calculation Maps Mineralogy - Pertamina RTI 24aug2023Document8 pagesProject Calculation Maps Mineralogy - Pertamina RTI 24aug2023arda.yogatamaNo ratings yet

- VAT Training Day 3Document31 pagesVAT Training Day 3iftekharul alamNo ratings yet

- PROJECT: Bangabandhu Sheikh Mujib Railway Bridge Construction Project Unit Rate AnalysisDocument1 pagePROJECT: Bangabandhu Sheikh Mujib Railway Bridge Construction Project Unit Rate AnalysisUdayan ChakrabortyNo ratings yet

- U44sf161083k - 12 Sep 2022Document2 pagesU44sf161083k - 12 Sep 2022calltoaction365No ratings yet

- Utility Bill-BSES PDFDocument2 pagesUtility Bill-BSES PDFKing Tri-ZiNo ratings yet

- Poly Carbonate - Injection Mould Component Cost EstimationDocument7 pagesPoly Carbonate - Injection Mould Component Cost EstimationVenkateswaran venkateswaranNo ratings yet

- Cost Abstract - Banga-Naina Devi FFRDocument1 pageCost Abstract - Banga-Naina Devi FFRtanmoyofbesu12No ratings yet

- Gas ValueDocument3 pagesGas Valuemahi_kotaNo ratings yet

- Buget Proposal ( )Document2 pagesBuget Proposal ( )Md. Habibullah ACCANo ratings yet

- Chapter 11Document72 pagesChapter 11Md. Habibullah ACCANo ratings yet

- Chapter 1Document20 pagesChapter 1Md. Habibullah ACCANo ratings yet

- Chapter 4Document49 pagesChapter 4Md. Habibullah ACCANo ratings yet

- Books Mar 1Document2 pagesBooks Mar 1mitushiNo ratings yet

- Business Studies Form 5 - MarketingDocument28 pagesBusiness Studies Form 5 - MarketingMuhammed DamphaNo ratings yet

- Channel Partner Presentation (1) - SIGNYDocument12 pagesChannel Partner Presentation (1) - SIGNYrakesh_danduNo ratings yet

- Project On Hospitality Industry: Customer Relationship ManagementDocument36 pagesProject On Hospitality Industry: Customer Relationship ManagementShraddha TiwariNo ratings yet

- Lesson 2 - The Statement of Comprehensive Income - ActivityDocument3 pagesLesson 2 - The Statement of Comprehensive Income - ActivityEmeldinand Padilla Motas0% (2)

- CASE 1-1 Aurore Cosmetics Question: Suggest A Strategy For Mayank As He Is About To Call On Jabby To Try To Recover ItsDocument1 pageCASE 1-1 Aurore Cosmetics Question: Suggest A Strategy For Mayank As He Is About To Call On Jabby To Try To Recover ItsEhsan AbirNo ratings yet

- Chapter 1Document14 pagesChapter 1sopner jalanaNo ratings yet

- Effect of Personal Selling On The Customer Patronage of Nigerian BanksDocument80 pagesEffect of Personal Selling On The Customer Patronage of Nigerian BanksUzochukwu OkpaniNo ratings yet

- Brand ManagementDocument5 pagesBrand ManagementSaba DawoodNo ratings yet

- CIE Section 3 MarketingDocument15 pagesCIE Section 3 MarketingSagar KumarNo ratings yet

- Acctg-5 Problem 15-12Document7 pagesAcctg-5 Problem 15-12Maria Fe Joanna AbonitaNo ratings yet

- Original For RecipientDocument1 pageOriginal For RecipientHarshal BhattNo ratings yet

- Wright Line Case SubmissionDocument6 pagesWright Line Case SubmissionKanika SharmaNo ratings yet

- E-Invoice Data DictionaryDocument124 pagesE-Invoice Data DictionarySaquib.MahmoodNo ratings yet

- Income Statement: Profit/Loss Account Dr. Satish Jangra (2009A229M)Document14 pagesIncome Statement: Profit/Loss Account Dr. Satish Jangra (2009A229M)Dr. Satish Jangra100% (1)

- How Viable Is Mydin Expansion and Growth StrategyDocument5 pagesHow Viable Is Mydin Expansion and Growth StrategySandro McTavishNo ratings yet

- Pricing in International MarketingDocument30 pagesPricing in International MarketingAnonymous d3CGBMzNo ratings yet

- Business Plan of TilesDocument22 pagesBusiness Plan of Tileslucas washingtonNo ratings yet

- Home Base QuizDocument7 pagesHome Base QuizSaad AsifNo ratings yet

- ReviewerDocument6 pagesReviewerSamuel FerolinoNo ratings yet

- TSF 5108235026014504 R PosDocument3 pagesTSF 5108235026014504 R PosJoy MondalNo ratings yet

- Acctg CycleDocument13 pagesAcctg Cyclefer maNo ratings yet

- MKTG 422 - Phillips Food Inc. Case Analysis by Jeremie DalinDocument11 pagesMKTG 422 - Phillips Food Inc. Case Analysis by Jeremie DalinShadman KibriaNo ratings yet

- MPA 602: Cost and Managerial Accounting: Cost-Volume-Profit (CVP) AnalysisDocument63 pagesMPA 602: Cost and Managerial Accounting: Cost-Volume-Profit (CVP) AnalysisMd. ZakariaNo ratings yet

- Pricing Exam - FatimaDocument3 pagesPricing Exam - FatimaElshan GrayNo ratings yet

Download as pdf or txt

You might also like

- Pestle Analysis of Hero Motocorp Case Study HelpDocument24 pagesPestle Analysis of Hero Motocorp Case Study HelpRENUKA THOTENo ratings yet

- PSPCL Bill 3001167479 Due On 2023-JAN-02Document2 pagesPSPCL Bill 3001167479 Due On 2023-JAN-02EKAMPREET KAURNo ratings yet

- UGG ValuationDocument7 pagesUGG ValuationPritam KarmakarNo ratings yet

- Intuit ValuationDocument4 pagesIntuit ValuationcorvettejrwNo ratings yet

- Dabur - ERPDocument20 pagesDabur - ERPavradeepmallik0% (1)

- Management Professional Competence Suggested Answers PAC Mock-Winter 2019Document17 pagesManagement Professional Competence Suggested Answers PAC Mock-Winter 2019Ismail yousufNo ratings yet

- 2MBA Business PlanDocument23 pages2MBA Business PlanJonathan BravoNo ratings yet

- Castrol Bike PointDocument4 pagesCastrol Bike PointVishnu Kant100% (1)

- Customs Duty: 1) Trisha Company Imported A Machine From Europe. From The FollowingDocument32 pagesCustoms Duty: 1) Trisha Company Imported A Machine From Europe. From The FollowingAneesh D'souzaNo ratings yet

- Import Cost CalculationDocument3 pagesImport Cost CalculationNayem UddinNo ratings yet

- Calculations For VE Cost Advantage Note: VE by Change of Norms / SpecificationsDocument4 pagesCalculations For VE Cost Advantage Note: VE by Change of Norms / Specificationsjigyesh sharmaNo ratings yet

- Project: PI Value USD $Document11 pagesProject: PI Value USD $Zahangir KabirNo ratings yet

- Valuation Mergers ProjectDocument3 pagesValuation Mergers Projectsuraj nairNo ratings yet

- Sarni-MBEL - 13-08-2019: Contract Value Bill Processed Payment Made Balance and LD Bills PendingDocument2 pagesSarni-MBEL - 13-08-2019: Contract Value Bill Processed Payment Made Balance and LD Bills PendingRuby masandNo ratings yet

- Rate Analysis BarracksDocument217 pagesRate Analysis BarracksIftikhar AhmadNo ratings yet

- Bill of Supply For Electricity: Due Date: 09-10-2021Document1 pageBill of Supply For Electricity: Due Date: 09-10-2021Khushwant SinghNo ratings yet

- Presentation Preliminary Results For Q1 2022Document8 pagesPresentation Preliminary Results For Q1 2022Manikanta rajaNo ratings yet

- Microsoft Vs Intuit ValuationDocument4 pagesMicrosoft Vs Intuit ValuationcorvettejrwNo ratings yet

- Packet - Ii: Signature Not Verified Signature Not Verified Signature Not VerifiedDocument3 pagesPacket - Ii: Signature Not Verified Signature Not Verified Signature Not VerifiedJaimin PopatNo ratings yet

- Bill of Supply For Electricity: Due Date: 04-10-2021Document1 pageBill of Supply For Electricity: Due Date: 04-10-2021Divya Prakash0% (1)

- Microsoft ValuationDocument4 pagesMicrosoft ValuationcorvettejrwNo ratings yet

- PSPCL Bill 3015013843 Due On 2020-JUN-08Document2 pagesPSPCL Bill 3015013843 Due On 2020-JUN-08RitishNo ratings yet

- Bill of Supply For Electricity (Amended) Due Date: - : BSES Yamuna Power LTDDocument1 pageBill of Supply For Electricity (Amended) Due Date: - : BSES Yamuna Power LTDArman Khan100% (1)

- D Hps UE Rp/hour) : Factor X Delivered Price X Annual Rates Annual Use in Hours RP / Hours)Document3 pagesD Hps UE Rp/hour) : Factor X Delivered Price X Annual Rates Annual Use in Hours RP / Hours)suhadi wahanaNo ratings yet

- PSPCL Bill 3002105108 Due On 2021-JUL-01Document1 pagePSPCL Bill 3002105108 Due On 2021-JUL-01Parvinder SinghNo ratings yet

- 70 06 Reserves To Statements AfterDocument4 pages70 06 Reserves To Statements Aftermerag76668No ratings yet

- AssignmentDocument5 pagesAssignmentSanchay BhararaNo ratings yet

- BOK ValuationDocument7 pagesBOK ValuationsuryagcNo ratings yet

- PSPCL Bill 3008440296 due on 2024-FEB-09Document2 pagesPSPCL Bill 3008440296 due on 2024-FEB-09TusharNo ratings yet

- Bill of Supply For Electricity: Due Date: 02-07-2022Document2 pagesBill of Supply For Electricity: Due Date: 02-07-2022QSEKCERT FSSAI0% (1)

- Revision Excel SheetsDocument9 pagesRevision Excel SheetsPhan Phúc NguyênNo ratings yet

- Description: Crushed Aggregate Sub-Base Course Ref No - 12.03 S.N. Description Unit Quantity Rate Amount in Nrs Remarks Nrs. Nrs. Unit: MDocument2 pagesDescription: Crushed Aggregate Sub-Base Course Ref No - 12.03 S.N. Description Unit Quantity Rate Amount in Nrs Remarks Nrs. Nrs. Unit: MLamichhane SauravNo ratings yet

- Design & Engineering: 3 RAB:25 1 3 RAB:25 1 3 RAB:25 1 True True True RAB:25 True True RAB:25 True True RAB:25 True TrueDocument1 pageDesign & Engineering: 3 RAB:25 1 3 RAB:25 1 3 RAB:25 1 True True True RAB:25 True True RAB:25 True True RAB:25 True TrueRinjumon RinjuNo ratings yet

- Final Assessment BillDocument1 pageFinal Assessment Billbcaabaaba0321No ratings yet

- Annual Fixed Cost, P/Yr FC D+I+Hti: Net Income Generated, Ph/Yr Ni (Co - Ra-Dca) Ca OpDocument14 pagesAnnual Fixed Cost, P/Yr FC D+I+Hti: Net Income Generated, Ph/Yr Ni (Co - Ra-Dca) Ca OpJan James GrazaNo ratings yet

- Willmeng GMP Fire Station #9 Extracted Cost PagesDocument6 pagesWillmeng GMP Fire Station #9 Extracted Cost PagesJimmyNo ratings yet

- GAOC Option 2Document2 pagesGAOC Option 2Amit PhadatareNo ratings yet

- Bill of Supply For Electricity Due Date: 12-09-2022: BSES Rajdhani Power LTDDocument1 pageBill of Supply For Electricity Due Date: 12-09-2022: BSES Rajdhani Power LTDNand Kishor100% (1)

- Sourses of Funds: Balance Sheet 2010 2009Document4 pagesSourses of Funds: Balance Sheet 2010 2009Deven PipaliaNo ratings yet

- Sample Sheet - Make Input On ThisDocument5 pagesSample Sheet - Make Input On ThisHelp YourselfNo ratings yet

- CERC Latest RegulationDocument26 pagesCERC Latest RegulationShubham ChaurasiaNo ratings yet

- F. EstimateDocument45 pagesF. Estimateanthropolozist entertainNo ratings yet

- Duty Calculation: Description Tariff Rate Amt. RefDocument16 pagesDuty Calculation: Description Tariff Rate Amt. RefgargshashankNo ratings yet

- D RKQ VGKDW Ca O1669099523586Document1 pageD RKQ VGKDW Ca O1669099523586Vedans Finances100% (1)

- Bill of Supply For Electricity: Due Date: 11-08-2022Document2 pagesBill of Supply For Electricity: Due Date: 11-08-2022Naitik GoelNo ratings yet

- PSPCL SoniyaDocument2 pagesPSPCL SoniyaJashanpreet SinghNo ratings yet

- PSPCL Bill 3002769928 Due On 2022-NOV-16Document2 pagesPSPCL Bill 3002769928 Due On 2022-NOV-16Rocky SonipatNo ratings yet

- PSPCL Bill 3002769928 Due On 2022-NOV-16Document2 pagesPSPCL Bill 3002769928 Due On 2022-NOV-16Rocky SonipatNo ratings yet

- PSPCL Bill 3002769928 Due On 2022-NOV-16Document2 pagesPSPCL Bill 3002769928 Due On 2022-NOV-16Rocky SonipatNo ratings yet

- PSPCL Bill 3002769928 Due On 2022-NOV-16Document2 pagesPSPCL Bill 3002769928 Due On 2022-NOV-16Rocky SonipatNo ratings yet

- PSPCL Bill 3002769928 Due On 2022-NOV-16Document2 pagesPSPCL Bill 3002769928 Due On 2022-NOV-16Rocky SonipatNo ratings yet

- Bill of Supply For Electricity: Due Date: 13-08-2022Document1 pageBill of Supply For Electricity: Due Date: 13-08-2022Aadit SK100% (1)

- S6 E Working FinalDocument9 pagesS6 E Working FinalROHIT PANDEYNo ratings yet

- Bill of Supply For Electricity: Due Date: 15-02-2022Document2 pagesBill of Supply For Electricity: Due Date: 15-02-2022Shamshad KhanNo ratings yet

- Transmission Corporation of Telangana Limited: 1 132Kv Lingampet-Minpur Line Loc No 69/11Document5 pagesTransmission Corporation of Telangana Limited: 1 132Kv Lingampet-Minpur Line Loc No 69/11Boddu ThirupathiNo ratings yet

- Amended BoQ ContractDocument53 pagesAmended BoQ ContractFikadu KassaNo ratings yet

- Project Calculation Maps Mineralogy - Pertamina RTI 24aug2023Document8 pagesProject Calculation Maps Mineralogy - Pertamina RTI 24aug2023arda.yogatamaNo ratings yet

- VAT Training Day 3Document31 pagesVAT Training Day 3iftekharul alamNo ratings yet

- PROJECT: Bangabandhu Sheikh Mujib Railway Bridge Construction Project Unit Rate AnalysisDocument1 pagePROJECT: Bangabandhu Sheikh Mujib Railway Bridge Construction Project Unit Rate AnalysisUdayan ChakrabortyNo ratings yet

- U44sf161083k - 12 Sep 2022Document2 pagesU44sf161083k - 12 Sep 2022calltoaction365No ratings yet

- Utility Bill-BSES PDFDocument2 pagesUtility Bill-BSES PDFKing Tri-ZiNo ratings yet

- Poly Carbonate - Injection Mould Component Cost EstimationDocument7 pagesPoly Carbonate - Injection Mould Component Cost EstimationVenkateswaran venkateswaranNo ratings yet

- Cost Abstract - Banga-Naina Devi FFRDocument1 pageCost Abstract - Banga-Naina Devi FFRtanmoyofbesu12No ratings yet

- Gas ValueDocument3 pagesGas Valuemahi_kotaNo ratings yet

- Buget Proposal ( )Document2 pagesBuget Proposal ( )Md. Habibullah ACCANo ratings yet

- Chapter 11Document72 pagesChapter 11Md. Habibullah ACCANo ratings yet

- Chapter 1Document20 pagesChapter 1Md. Habibullah ACCANo ratings yet

- Chapter 4Document49 pagesChapter 4Md. Habibullah ACCANo ratings yet

- Books Mar 1Document2 pagesBooks Mar 1mitushiNo ratings yet

- Business Studies Form 5 - MarketingDocument28 pagesBusiness Studies Form 5 - MarketingMuhammed DamphaNo ratings yet

- Channel Partner Presentation (1) - SIGNYDocument12 pagesChannel Partner Presentation (1) - SIGNYrakesh_danduNo ratings yet

- Project On Hospitality Industry: Customer Relationship ManagementDocument36 pagesProject On Hospitality Industry: Customer Relationship ManagementShraddha TiwariNo ratings yet

- Lesson 2 - The Statement of Comprehensive Income - ActivityDocument3 pagesLesson 2 - The Statement of Comprehensive Income - ActivityEmeldinand Padilla Motas0% (2)

- CASE 1-1 Aurore Cosmetics Question: Suggest A Strategy For Mayank As He Is About To Call On Jabby To Try To Recover ItsDocument1 pageCASE 1-1 Aurore Cosmetics Question: Suggest A Strategy For Mayank As He Is About To Call On Jabby To Try To Recover ItsEhsan AbirNo ratings yet

- Chapter 1Document14 pagesChapter 1sopner jalanaNo ratings yet

- Effect of Personal Selling On The Customer Patronage of Nigerian BanksDocument80 pagesEffect of Personal Selling On The Customer Patronage of Nigerian BanksUzochukwu OkpaniNo ratings yet

- Brand ManagementDocument5 pagesBrand ManagementSaba DawoodNo ratings yet

- CIE Section 3 MarketingDocument15 pagesCIE Section 3 MarketingSagar KumarNo ratings yet

- Acctg-5 Problem 15-12Document7 pagesAcctg-5 Problem 15-12Maria Fe Joanna AbonitaNo ratings yet

- Original For RecipientDocument1 pageOriginal For RecipientHarshal BhattNo ratings yet

- Wright Line Case SubmissionDocument6 pagesWright Line Case SubmissionKanika SharmaNo ratings yet

- E-Invoice Data DictionaryDocument124 pagesE-Invoice Data DictionarySaquib.MahmoodNo ratings yet

- Income Statement: Profit/Loss Account Dr. Satish Jangra (2009A229M)Document14 pagesIncome Statement: Profit/Loss Account Dr. Satish Jangra (2009A229M)Dr. Satish Jangra100% (1)

- How Viable Is Mydin Expansion and Growth StrategyDocument5 pagesHow Viable Is Mydin Expansion and Growth StrategySandro McTavishNo ratings yet

- Pricing in International MarketingDocument30 pagesPricing in International MarketingAnonymous d3CGBMzNo ratings yet

- Business Plan of TilesDocument22 pagesBusiness Plan of Tileslucas washingtonNo ratings yet

- Home Base QuizDocument7 pagesHome Base QuizSaad AsifNo ratings yet

- ReviewerDocument6 pagesReviewerSamuel FerolinoNo ratings yet

- TSF 5108235026014504 R PosDocument3 pagesTSF 5108235026014504 R PosJoy MondalNo ratings yet

- Acctg CycleDocument13 pagesAcctg Cyclefer maNo ratings yet

- MKTG 422 - Phillips Food Inc. Case Analysis by Jeremie DalinDocument11 pagesMKTG 422 - Phillips Food Inc. Case Analysis by Jeremie DalinShadman KibriaNo ratings yet

- MPA 602: Cost and Managerial Accounting: Cost-Volume-Profit (CVP) AnalysisDocument63 pagesMPA 602: Cost and Managerial Accounting: Cost-Volume-Profit (CVP) AnalysisMd. ZakariaNo ratings yet

- Pricing Exam - FatimaDocument3 pagesPricing Exam - FatimaElshan GrayNo ratings yet