FRA Futures Options Past Papers

FRA Futures Options Past Papers

You might also like

- BV - Assignement 2Document7 pagesBV - Assignement 2AkshatAgarwal50% (2)

- Business Finance Assignment 2Document8 pagesBusiness Finance Assignment 2Akshat100% (1)

- Case Study - Corp Finance - Padgett Paper ProductsDocument26 pagesCase Study - Corp Finance - Padgett Paper ProductsJed Estanislao100% (1)

- Aniket Kulkarni Finance Black Book PDFDocument75 pagesAniket Kulkarni Finance Black Book PDFAniket KulkarniNo ratings yet

- MATH 108X - Skill Practice: Mike's Savings AccountDocument18 pagesMATH 108X - Skill Practice: Mike's Savings Accountkhardiatu siryon0% (1)

- Momentum Investing: Mi25 An Alternate Investing StrategyDocument18 pagesMomentum Investing: Mi25 An Alternate Investing Strategysantosh MaliNo ratings yet

- All AFM Technical Articles 2021Document139 pagesAll AFM Technical Articles 2021Ashfaq Ul Haq OniNo ratings yet

- How to Trade Cfds Profitably: A Trader's Guide to Successful Cfd TradingFrom EverandHow to Trade Cfds Profitably: A Trader's Guide to Successful Cfd TradingNo ratings yet

- SSS Disbursement Account Enrollment Module RemindersDocument2 pagesSSS Disbursement Account Enrollment Module Remindersgemvillarin100% (3)

- Ibm Accounting Analysis ProjectDocument15 pagesIbm Accounting Analysis Projectapi-295032978No ratings yet

- Transaction To Be HedgedDocument155 pagesTransaction To Be HedgedPREX WEXNo ratings yet

- Special Class Managing Interest Rate RisksDocument7 pagesSpecial Class Managing Interest Rate Risksmiradvance studyNo ratings yet

- FRM 5Document4 pagesFRM 5irfanhaidersewagNo ratings yet

- Managing Interest Rate RisksDocument15 pagesManaging Interest Rate RisksShakil IslamNo ratings yet

- Problem 1.35Document8 pagesProblem 1.35zmm45x7sjtNo ratings yet

- Yield Curves RiskWorXDocument7 pagesYield Curves RiskWorXraghu_prabhuNo ratings yet

- Evaluating The Firm'S Dividend PolicyDocument11 pagesEvaluating The Firm'S Dividend PolicyYash Aggarwal BD20073No ratings yet

- May 12 SuggestedDocument19 pagesMay 12 SuggestedRaul KarkyNo ratings yet

- Revision Exercise 2 - Int Rates + Capl Budgeting - SolutionsDocument25 pagesRevision Exercise 2 - Int Rates + Capl Budgeting - SolutionsBaher WilliamNo ratings yet

- Afm Technical Articles As On 18042019 PDFDocument147 pagesAfm Technical Articles As On 18042019 PDFحسین جلیل پورNo ratings yet

- Chapter 2 Overview Financial Risk MGMT Questions and Answers-RevisedDocument3 pagesChapter 2 Overview Financial Risk MGMT Questions and Answers-RevisedSahaana VijayNo ratings yet

- Interest Rate Futures Most Important Question SolutionDocument3 pagesInterest Rate Futures Most Important Question SolutionAshish GoelNo ratings yet

- RisksDocument23 pagesRisksfnf7qfskfbNo ratings yet

- Mutual Fund Data Sheet - Summary NewDocument5 pagesMutual Fund Data Sheet - Summary NewBharathi 3280No ratings yet

- Answers To Problem Sets: Est. Time: 01-05Document16 pagesAnswers To Problem Sets: Est. Time: 01-05Ankit SaxenaNo ratings yet

- WK 4 FDM Morgan SolutionDocument8 pagesWK 4 FDM Morgan Solutionnguyenthanhtra56271No ratings yet

- Calculate The Cost of Long-Term FinanceDocument26 pagesCalculate The Cost of Long-Term Financedevikatadi777No ratings yet

- Interest Rate Hedging-Examples: Arshad HassanDocument32 pagesInterest Rate Hedging-Examples: Arshad HassanirfanhaidersewagNo ratings yet

- Case Study 2-Actuarial Valuation - ReportDocument8 pagesCase Study 2-Actuarial Valuation - Reportflávio guilhermeNo ratings yet

- Dividend Decesion: A Strategic PerspectiveDocument34 pagesDividend Decesion: A Strategic PerspectivePrashant MittalNo ratings yet

- Bond Portfolio MGTDocument22 pagesBond Portfolio MGTChandrabhan NathawatNo ratings yet

- Wealth Creation: - Fire Bolt InvestmentsDocument22 pagesWealth Creation: - Fire Bolt Investmentskrish3291No ratings yet

- Bifs Session 18 Ay 2022-23 First Round - Swap PricingDocument21 pagesBifs Session 18 Ay 2022-23 First Round - Swap Pricingrajan tiwariNo ratings yet

- Section e - AnswersDocument7 pagesSection e - AnswersAhmed Raza MirNo ratings yet

- Section B Dividend Policy and Sources of FinanceDocument21 pagesSection B Dividend Policy and Sources of Financebijesh babuNo ratings yet

- Chap 004Document32 pagesChap 004Hyunjoo NohNo ratings yet

- Chapter 5: Interest Rate Risks: Lecturer: Amadeus GABRIEL La Rochelle Business SchoolDocument25 pagesChapter 5: Interest Rate Risks: Lecturer: Amadeus GABRIEL La Rochelle Business SchoolJuana BoresNo ratings yet

- III. Estimating Growth: DCF ValuationDocument48 pagesIII. Estimating Growth: DCF ValuationYến NhiNo ratings yet

- Fixed Income Attribution AnalysisDocument21 pagesFixed Income Attribution AnalysisJaz MNo ratings yet

- CH 4 - in ClassDocument3 pagesCH 4 - in ClassJOSEPH MICHAEL MCGUINNESSNo ratings yet

- PRUretirement GrowthDocument32 pagesPRUretirement GrowthlongcyNo ratings yet

- Active Investment StrategiesDocument58 pagesActive Investment StrategiesaliNo ratings yet

- I. The Stable Growth DDM: Gordon Growth Model: Estimate For The USDocument30 pagesI. The Stable Growth DDM: Gordon Growth Model: Estimate For The USgagan585No ratings yet

- RAMACHANDRANDocument40 pagesRAMACHANDRANYoges YogeswaranNo ratings yet

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document10 pages3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali0% (1)

- Bod AnswerDocument5 pagesBod AnswerJosh alexNo ratings yet

- CA FINAL AFM ADVANCED FINANCIAL MANAGEMENT Pawan Sir Volume 03Document357 pagesCA FINAL AFM ADVANCED FINANCIAL MANAGEMENT Pawan Sir Volume 03neerajsakotwalNo ratings yet

- Solutions Topic4Document4 pagesSolutions Topic4Thirusha balamuraliNo ratings yet

- IM6. Fixed IncomeDocument42 pagesIM6. Fixed IncomeZoon KiatNo ratings yet

- Aditya Birla Group-Birla Sun Life Insurance Co LTD.: About The CompanyDocument9 pagesAditya Birla Group-Birla Sun Life Insurance Co LTD.: About The CompanySasha AgarwalNo ratings yet

- Ch13 SolutionsManual FINAL 050417Document30 pagesCh13 SolutionsManual FINAL 050417Natalie ChoiNo ratings yet

- Chapter 13 - SolutionsManual - FINAL - 050417 PDFDocument30 pagesChapter 13 - SolutionsManual - FINAL - 050417 PDFNatalie ChoiNo ratings yet

- MNGT 604 Day2 Problem Set Solutions-2Document7 pagesMNGT 604 Day2 Problem Set Solutions-2harini muthuNo ratings yet

- 67733bos54256 Fold P2aDocument11 pages67733bos54256 Fold P2aVipul JainNo ratings yet

- Sample Final Term Exam-Solutions PGDocument3 pagesSample Final Term Exam-Solutions PGYilin YANGNo ratings yet

- Wilderness WordDocument3 pagesWilderness Wordarsenali damuNo ratings yet

- Derivatives and Risk ManagementDocument136 pagesDerivatives and Risk Managementabbas ali100% (3)

- Dividend Discount Model: AssumptionsDocument27 pagesDividend Discount Model: AssumptionsSairam GovarthananNo ratings yet

- Global Edition: Bond Price VolatilityDocument54 pagesGlobal Edition: Bond Price VolatilityTesar Handy AfrianNo ratings yet

- Investment Philosophy - Lecture 2Document13 pagesInvestment Philosophy - Lecture 2Khurram AliNo ratings yet

- Assignment 2Document3 pagesAssignment 2lcergoNo ratings yet

- 考官文章Document44 pages考官文章Hannah GohNo ratings yet

- Pricing with Confidence: Ten Rules for Increasing Profits and Staying Ahead of InflationFrom EverandPricing with Confidence: Ten Rules for Increasing Profits and Staying Ahead of InflationNo ratings yet

- Fa1 Examreport d15Document3 pagesFa1 Examreport d15S RaihanNo ratings yet

- Exam On Double EntryDocument3 pagesExam On Double EntryS RaihanNo ratings yet

- Control AccountsDocument4 pagesControl AccountsS RaihanNo ratings yet

- Finance Act 2022Document124 pagesFinance Act 2022S RaihanNo ratings yet

- Section 1 Lesson 1 Unit 1Document20 pagesSection 1 Lesson 1 Unit 1S RaihanNo ratings yet

- Assets and LiabilitiesDocument2 pagesAssets and LiabilitiesS RaihanNo ratings yet

- C O M P A N Y P R O F I L E: Achal Gupta Managing Director & Chief Executive OfficerDocument61 pagesC O M P A N Y P R O F I L E: Achal Gupta Managing Director & Chief Executive OfficervipinkathpalNo ratings yet

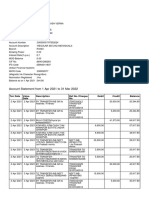

- Account Statement 280619 180719Document3 pagesAccount Statement 280619 180719Naresh SeerviNo ratings yet

- Money Market HedgeDocument8 pagesMoney Market HedgeTanim Misbahul MNo ratings yet

- Banking Regulation Act Made EasyDocument11 pagesBanking Regulation Act Made EasywahilNo ratings yet

- Module 8. International Financial Market and Innovations ObjectivesDocument9 pagesModule 8. International Financial Market and Innovations ObjectivesSalma AbdullahNo ratings yet

- Topic 3 Circular Flow Grade 10Document15 pagesTopic 3 Circular Flow Grade 10DJAY TIDO-KNo ratings yet

- Portfolio SelectionDocument6 pagesPortfolio SelectionAssfaw KebedeNo ratings yet

- K1 TNHFHN TRQLZ 1 OBDocument15 pagesK1 TNHFHN TRQLZ 1 OBjai vermaNo ratings yet

- Report of Commerical Banknof EthiopiaDocument22 pagesReport of Commerical Banknof EthiopiaTariku RichNo ratings yet

- Greece: Preliminary Draft Debt Sustainability AnalysisDocument24 pagesGreece: Preliminary Draft Debt Sustainability AnalysisCostas EfimerosNo ratings yet

- Audit ReportDocument22 pagesAudit ReportTasya Febriani AdrianaNo ratings yet

- Sample MCQs Income Tax - DEADocument15 pagesSample MCQs Income Tax - DEACrick CompactNo ratings yet

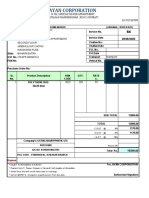

- Ayan Corp Exel PDFDocument1 pageAyan Corp Exel PDFmaharaj ( prashant dave)No ratings yet

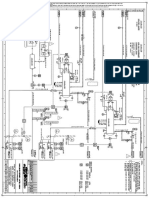

- P&ID For SRU-2Document1 pageP&ID For SRU-2Sukdeb MaityNo ratings yet

- International Working Capital ManagementDocument28 pagesInternational Working Capital ManagementAvayant Kumar Singh100% (2)

- Ratio Table - ACCT 3BDocument10 pagesRatio Table - ACCT 3BHoàng Minh ChuNo ratings yet

- Capital BudgetingDocument22 pagesCapital BudgetingKamal GanugulaNo ratings yet

- PSPCL Receipt For Ac Txnid INT1802229566634Document1 pagePSPCL Receipt For Ac Txnid INT1802229566634Tom McGovernNo ratings yet

- Accounting & Excel Assignment - ExperiencedDocument21 pagesAccounting & Excel Assignment - Experienceddivyaparashar10No ratings yet

- Public Finance Study GUIDE 2019/2020: Morning/Evening/WeekendDocument67 pagesPublic Finance Study GUIDE 2019/2020: Morning/Evening/Weekendhayenje rebeccaNo ratings yet

- UTTARA BANK Formula SheetDocument15 pagesUTTARA BANK Formula SheetAlamesuNo ratings yet

- LU2 Lecturer NotesDocument23 pagesLU2 Lecturer NotesShweta SinghNo ratings yet

- Can Gopal Kavalireddi Tell Us What He Looks For Before Picking A Stock For A Short Period of TimeDocument9 pagesCan Gopal Kavalireddi Tell Us What He Looks For Before Picking A Stock For A Short Period of TimeAnonymous w6TIxI0G8lNo ratings yet

- Advanced Corporate Finance ACC3140Document7 pagesAdvanced Corporate Finance ACC3140arthurnitsopoulos_14No ratings yet

- Odisa Farm AgriDocument220 pagesOdisa Farm AgriUmakant PNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- BV - Assignement 2Document7 pagesBV - Assignement 2AkshatAgarwal50% (2)

- Business Finance Assignment 2Document8 pagesBusiness Finance Assignment 2Akshat100% (1)

- Case Study - Corp Finance - Padgett Paper ProductsDocument26 pagesCase Study - Corp Finance - Padgett Paper ProductsJed Estanislao100% (1)

- Aniket Kulkarni Finance Black Book PDFDocument75 pagesAniket Kulkarni Finance Black Book PDFAniket KulkarniNo ratings yet

- MATH 108X - Skill Practice: Mike's Savings AccountDocument18 pagesMATH 108X - Skill Practice: Mike's Savings Accountkhardiatu siryon0% (1)

- Momentum Investing: Mi25 An Alternate Investing StrategyDocument18 pagesMomentum Investing: Mi25 An Alternate Investing Strategysantosh MaliNo ratings yet

- All AFM Technical Articles 2021Document139 pagesAll AFM Technical Articles 2021Ashfaq Ul Haq OniNo ratings yet

- How to Trade Cfds Profitably: A Trader's Guide to Successful Cfd TradingFrom EverandHow to Trade Cfds Profitably: A Trader's Guide to Successful Cfd TradingNo ratings yet

- SSS Disbursement Account Enrollment Module RemindersDocument2 pagesSSS Disbursement Account Enrollment Module Remindersgemvillarin100% (3)

- Ibm Accounting Analysis ProjectDocument15 pagesIbm Accounting Analysis Projectapi-295032978No ratings yet

- Transaction To Be HedgedDocument155 pagesTransaction To Be HedgedPREX WEXNo ratings yet

- Special Class Managing Interest Rate RisksDocument7 pagesSpecial Class Managing Interest Rate Risksmiradvance studyNo ratings yet

- FRM 5Document4 pagesFRM 5irfanhaidersewagNo ratings yet

- Managing Interest Rate RisksDocument15 pagesManaging Interest Rate RisksShakil IslamNo ratings yet

- Problem 1.35Document8 pagesProblem 1.35zmm45x7sjtNo ratings yet

- Yield Curves RiskWorXDocument7 pagesYield Curves RiskWorXraghu_prabhuNo ratings yet

- Evaluating The Firm'S Dividend PolicyDocument11 pagesEvaluating The Firm'S Dividend PolicyYash Aggarwal BD20073No ratings yet

- May 12 SuggestedDocument19 pagesMay 12 SuggestedRaul KarkyNo ratings yet

- Revision Exercise 2 - Int Rates + Capl Budgeting - SolutionsDocument25 pagesRevision Exercise 2 - Int Rates + Capl Budgeting - SolutionsBaher WilliamNo ratings yet

- Afm Technical Articles As On 18042019 PDFDocument147 pagesAfm Technical Articles As On 18042019 PDFحسین جلیل پورNo ratings yet

- Chapter 2 Overview Financial Risk MGMT Questions and Answers-RevisedDocument3 pagesChapter 2 Overview Financial Risk MGMT Questions and Answers-RevisedSahaana VijayNo ratings yet

- Interest Rate Futures Most Important Question SolutionDocument3 pagesInterest Rate Futures Most Important Question SolutionAshish GoelNo ratings yet

- RisksDocument23 pagesRisksfnf7qfskfbNo ratings yet

- Mutual Fund Data Sheet - Summary NewDocument5 pagesMutual Fund Data Sheet - Summary NewBharathi 3280No ratings yet

- Answers To Problem Sets: Est. Time: 01-05Document16 pagesAnswers To Problem Sets: Est. Time: 01-05Ankit SaxenaNo ratings yet

- WK 4 FDM Morgan SolutionDocument8 pagesWK 4 FDM Morgan Solutionnguyenthanhtra56271No ratings yet

- Calculate The Cost of Long-Term FinanceDocument26 pagesCalculate The Cost of Long-Term Financedevikatadi777No ratings yet

- Interest Rate Hedging-Examples: Arshad HassanDocument32 pagesInterest Rate Hedging-Examples: Arshad HassanirfanhaidersewagNo ratings yet

- Case Study 2-Actuarial Valuation - ReportDocument8 pagesCase Study 2-Actuarial Valuation - Reportflávio guilhermeNo ratings yet

- Dividend Decesion: A Strategic PerspectiveDocument34 pagesDividend Decesion: A Strategic PerspectivePrashant MittalNo ratings yet

- Bond Portfolio MGTDocument22 pagesBond Portfolio MGTChandrabhan NathawatNo ratings yet

- Wealth Creation: - Fire Bolt InvestmentsDocument22 pagesWealth Creation: - Fire Bolt Investmentskrish3291No ratings yet

- Bifs Session 18 Ay 2022-23 First Round - Swap PricingDocument21 pagesBifs Session 18 Ay 2022-23 First Round - Swap Pricingrajan tiwariNo ratings yet

- Section e - AnswersDocument7 pagesSection e - AnswersAhmed Raza MirNo ratings yet

- Section B Dividend Policy and Sources of FinanceDocument21 pagesSection B Dividend Policy and Sources of Financebijesh babuNo ratings yet

- Chap 004Document32 pagesChap 004Hyunjoo NohNo ratings yet

- Chapter 5: Interest Rate Risks: Lecturer: Amadeus GABRIEL La Rochelle Business SchoolDocument25 pagesChapter 5: Interest Rate Risks: Lecturer: Amadeus GABRIEL La Rochelle Business SchoolJuana BoresNo ratings yet

- III. Estimating Growth: DCF ValuationDocument48 pagesIII. Estimating Growth: DCF ValuationYến NhiNo ratings yet

- Fixed Income Attribution AnalysisDocument21 pagesFixed Income Attribution AnalysisJaz MNo ratings yet

- CH 4 - in ClassDocument3 pagesCH 4 - in ClassJOSEPH MICHAEL MCGUINNESSNo ratings yet

- PRUretirement GrowthDocument32 pagesPRUretirement GrowthlongcyNo ratings yet

- Active Investment StrategiesDocument58 pagesActive Investment StrategiesaliNo ratings yet

- I. The Stable Growth DDM: Gordon Growth Model: Estimate For The USDocument30 pagesI. The Stable Growth DDM: Gordon Growth Model: Estimate For The USgagan585No ratings yet

- RAMACHANDRANDocument40 pagesRAMACHANDRANYoges YogeswaranNo ratings yet

- 3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Document10 pages3.7 Strategic Financial Management (Old Syllabus) of ACCA Past Papers With Answers From2002-2006Sajid Ali0% (1)

- Bod AnswerDocument5 pagesBod AnswerJosh alexNo ratings yet

- CA FINAL AFM ADVANCED FINANCIAL MANAGEMENT Pawan Sir Volume 03Document357 pagesCA FINAL AFM ADVANCED FINANCIAL MANAGEMENT Pawan Sir Volume 03neerajsakotwalNo ratings yet

- Solutions Topic4Document4 pagesSolutions Topic4Thirusha balamuraliNo ratings yet

- IM6. Fixed IncomeDocument42 pagesIM6. Fixed IncomeZoon KiatNo ratings yet

- Aditya Birla Group-Birla Sun Life Insurance Co LTD.: About The CompanyDocument9 pagesAditya Birla Group-Birla Sun Life Insurance Co LTD.: About The CompanySasha AgarwalNo ratings yet

- Ch13 SolutionsManual FINAL 050417Document30 pagesCh13 SolutionsManual FINAL 050417Natalie ChoiNo ratings yet

- Chapter 13 - SolutionsManual - FINAL - 050417 PDFDocument30 pagesChapter 13 - SolutionsManual - FINAL - 050417 PDFNatalie ChoiNo ratings yet

- MNGT 604 Day2 Problem Set Solutions-2Document7 pagesMNGT 604 Day2 Problem Set Solutions-2harini muthuNo ratings yet

- 67733bos54256 Fold P2aDocument11 pages67733bos54256 Fold P2aVipul JainNo ratings yet

- Sample Final Term Exam-Solutions PGDocument3 pagesSample Final Term Exam-Solutions PGYilin YANGNo ratings yet

- Wilderness WordDocument3 pagesWilderness Wordarsenali damuNo ratings yet

- Derivatives and Risk ManagementDocument136 pagesDerivatives and Risk Managementabbas ali100% (3)

- Dividend Discount Model: AssumptionsDocument27 pagesDividend Discount Model: AssumptionsSairam GovarthananNo ratings yet

- Global Edition: Bond Price VolatilityDocument54 pagesGlobal Edition: Bond Price VolatilityTesar Handy AfrianNo ratings yet

- Investment Philosophy - Lecture 2Document13 pagesInvestment Philosophy - Lecture 2Khurram AliNo ratings yet

- Assignment 2Document3 pagesAssignment 2lcergoNo ratings yet

- 考官文章Document44 pages考官文章Hannah GohNo ratings yet

- Pricing with Confidence: Ten Rules for Increasing Profits and Staying Ahead of InflationFrom EverandPricing with Confidence: Ten Rules for Increasing Profits and Staying Ahead of InflationNo ratings yet

- Fa1 Examreport d15Document3 pagesFa1 Examreport d15S RaihanNo ratings yet

- Exam On Double EntryDocument3 pagesExam On Double EntryS RaihanNo ratings yet

- Control AccountsDocument4 pagesControl AccountsS RaihanNo ratings yet

- Finance Act 2022Document124 pagesFinance Act 2022S RaihanNo ratings yet

- Section 1 Lesson 1 Unit 1Document20 pagesSection 1 Lesson 1 Unit 1S RaihanNo ratings yet

- Assets and LiabilitiesDocument2 pagesAssets and LiabilitiesS RaihanNo ratings yet

- C O M P A N Y P R O F I L E: Achal Gupta Managing Director & Chief Executive OfficerDocument61 pagesC O M P A N Y P R O F I L E: Achal Gupta Managing Director & Chief Executive OfficervipinkathpalNo ratings yet

- Account Statement 280619 180719Document3 pagesAccount Statement 280619 180719Naresh SeerviNo ratings yet

- Money Market HedgeDocument8 pagesMoney Market HedgeTanim Misbahul MNo ratings yet

- Banking Regulation Act Made EasyDocument11 pagesBanking Regulation Act Made EasywahilNo ratings yet

- Module 8. International Financial Market and Innovations ObjectivesDocument9 pagesModule 8. International Financial Market and Innovations ObjectivesSalma AbdullahNo ratings yet

- Topic 3 Circular Flow Grade 10Document15 pagesTopic 3 Circular Flow Grade 10DJAY TIDO-KNo ratings yet

- Portfolio SelectionDocument6 pagesPortfolio SelectionAssfaw KebedeNo ratings yet

- K1 TNHFHN TRQLZ 1 OBDocument15 pagesK1 TNHFHN TRQLZ 1 OBjai vermaNo ratings yet

- Report of Commerical Banknof EthiopiaDocument22 pagesReport of Commerical Banknof EthiopiaTariku RichNo ratings yet

- Greece: Preliminary Draft Debt Sustainability AnalysisDocument24 pagesGreece: Preliminary Draft Debt Sustainability AnalysisCostas EfimerosNo ratings yet

- Audit ReportDocument22 pagesAudit ReportTasya Febriani AdrianaNo ratings yet

- Sample MCQs Income Tax - DEADocument15 pagesSample MCQs Income Tax - DEACrick CompactNo ratings yet

- Ayan Corp Exel PDFDocument1 pageAyan Corp Exel PDFmaharaj ( prashant dave)No ratings yet

- P&ID For SRU-2Document1 pageP&ID For SRU-2Sukdeb MaityNo ratings yet

- International Working Capital ManagementDocument28 pagesInternational Working Capital ManagementAvayant Kumar Singh100% (2)

- Ratio Table - ACCT 3BDocument10 pagesRatio Table - ACCT 3BHoàng Minh ChuNo ratings yet

- Capital BudgetingDocument22 pagesCapital BudgetingKamal GanugulaNo ratings yet

- PSPCL Receipt For Ac Txnid INT1802229566634Document1 pagePSPCL Receipt For Ac Txnid INT1802229566634Tom McGovernNo ratings yet

- Accounting & Excel Assignment - ExperiencedDocument21 pagesAccounting & Excel Assignment - Experienceddivyaparashar10No ratings yet

- Public Finance Study GUIDE 2019/2020: Morning/Evening/WeekendDocument67 pagesPublic Finance Study GUIDE 2019/2020: Morning/Evening/Weekendhayenje rebeccaNo ratings yet

- UTTARA BANK Formula SheetDocument15 pagesUTTARA BANK Formula SheetAlamesuNo ratings yet

- LU2 Lecturer NotesDocument23 pagesLU2 Lecturer NotesShweta SinghNo ratings yet

- Can Gopal Kavalireddi Tell Us What He Looks For Before Picking A Stock For A Short Period of TimeDocument9 pagesCan Gopal Kavalireddi Tell Us What He Looks For Before Picking A Stock For A Short Period of TimeAnonymous w6TIxI0G8lNo ratings yet

- Advanced Corporate Finance ACC3140Document7 pagesAdvanced Corporate Finance ACC3140arthurnitsopoulos_14No ratings yet

- Odisa Farm AgriDocument220 pagesOdisa Farm AgriUmakant PNo ratings yet