Cambodian Taxation Reviewers 5

Cambodian Taxation Reviewers 5

You might also like

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- Salary Slip Format For HCLDocument1 pageSalary Slip Format For HCLAmar Rajput58% (12)

- CBLM - Bookkeeping NC III (Aporbo, J)Document28 pagesCBLM - Bookkeeping NC III (Aporbo, J)denmark macalisangNo ratings yet

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionFrom EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNo ratings yet

- Economics Formula SheetDocument10 pagesEconomics Formula SheetCratos_Poseidon100% (1)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Fin623 Solved MCQs For EamsDocument24 pagesFin623 Solved MCQs For EamsSohail Merchant79% (14)

- Cambodian Taxation Reviewers 4Document24 pagesCambodian Taxation Reviewers 4Ken JomelNo ratings yet

- Cambodian Taxation Reviewers 3Document23 pagesCambodian Taxation Reviewers 3Ken JomelNo ratings yet

- Cambodian Taxation Reviewers 2Document25 pagesCambodian Taxation Reviewers 2Ken JomelNo ratings yet

- Cambodian Taxation Reviewers 1Document25 pagesCambodian Taxation Reviewers 1Ken JomelNo ratings yet

- For Sir Red - 20 MCQs - TAXATIONDocument5 pagesFor Sir Red - 20 MCQs - TAXATIONRed Christian PalustreNo ratings yet

- Quiz 4 Vat Business Tax 1322 - CompressDocument3 pagesQuiz 4 Vat Business Tax 1322 - CompressChris MartinezNo ratings yet

- ICAB Knowledge Level Taxation-I Suggested Answer May June 2010 - Nov Dec 2017Document150 pagesICAB Knowledge Level Taxation-I Suggested Answer May June 2010 - Nov Dec 2017Optimal Management Solution91% (11)

- 3rdyr 1stF BusinessTax 2324Document43 pages3rdyr 1stF BusinessTax 2324zaounxosakubNo ratings yet

- Tax Final ExamDocument7 pagesTax Final ExamJulienne UntalascoNo ratings yet

- Input Tax CreditDocument8 pagesInput Tax CreditPranjal AgrawalNo ratings yet

- Tax UpdatesDocument79 pagesTax UpdatesFreijiah SonNo ratings yet

- JPIA Review S3 Installment 2 (Business Tax)Document30 pagesJPIA Review S3 Installment 2 (Business Tax)rylNo ratings yet

- Additions To TaxDocument6 pagesAdditions To TaxJustin Robert RoqueNo ratings yet

- 10-Practical Questions of Individuals (78-113)Document38 pages10-Practical Questions of Individuals (78-113)Sajid Saith0% (1)

- 3rd Quizzer 1st Sem SY 2020-2021 - AKDocument6 pages3rd Quizzer 1st Sem SY 2020-2021 - AKMitzi WamarNo ratings yet

- Vivad Se Vishwas Tax 2025Document17 pagesVivad Se Vishwas Tax 2025Juzer JiruNo ratings yet

- NIRC V. TRAInDocument11 pagesNIRC V. TRAInJin De GuzmanNo ratings yet

- TAX Final PreboardDocument23 pagesTAX Final PreboardEDUARDO JR. VILLANUEVANo ratings yet

- Final Examination - TaxationDocument9 pagesFinal Examination - TaxationCatherine LavadiaNo ratings yet

- Ewt Exam - FormareDocument3 pagesEwt Exam - FormareMikaela SalvadorNo ratings yet

- Allowed Deductions From Gross IncomeDocument8 pagesAllowed Deductions From Gross Incomealliahbilities currentNo ratings yet

- First Preboard TAX ReviewDocument17 pagesFirst Preboard TAX Reviewlois martinNo ratings yet

- Statutory Updates For Nov-21 ExamsDocument50 pagesStatutory Updates For Nov-21 ExamsShodasakshari VidyaNo ratings yet

- MCQ Dimaampao W Answer KeyDocument16 pagesMCQ Dimaampao W Answer KeyvalkyriorNo ratings yet

- 2020NMBE Taxation With AnswersDocument21 pages2020NMBE Taxation With AnswersWilsonNo ratings yet

- Income Tax 2017 Edazdb1013Document50 pagesIncome Tax 2017 Edazdb1013Pradeep PatilNo ratings yet

- Bam 031 CfeDocument43 pagesBam 031 CfeMs VampireNo ratings yet

- VAT - MCQ Test Questions by Mahbub SirDocument16 pagesVAT - MCQ Test Questions by Mahbub SirAysha Alam100% (1)

- Tax Alert No. 91 (Senate Bill (SB) No. 1357 or The Corporate Recovery and Tax Incentives For Enterprises Act (CREATE) )Document9 pagesTax Alert No. 91 (Senate Bill (SB) No. 1357 or The Corporate Recovery and Tax Incentives For Enterprises Act (CREATE) )Karina PulidoNo ratings yet

- National Federation of Junior Philipinne Institute of Accountants - National Capital Region Taxation (Tax)Document10 pagesNational Federation of Junior Philipinne Institute of Accountants - National Capital Region Taxation (Tax)joyceNo ratings yet

- Input Tax Credit (Itc) SystemDocument17 pagesInput Tax Credit (Itc) SystemJasmin BidNo ratings yet

- TAX 2021 - Theories and Independent ProblemsDocument28 pagesTAX 2021 - Theories and Independent ProblemsMingcheng JeeNo ratings yet

- What Is Input Tax Credit - GST IndiaDocument4 pagesWhat Is Input Tax Credit - GST Indiaaslam_bechemNo ratings yet

- BAM031 P3 Q1 Answer FBT DeductionsDocument12 pagesBAM031 P3 Q1 Answer FBT DeductionsMary Lyn DatuinNo ratings yet

- Supllimentary Duty, Submission of Vat ReturnDocument51 pagesSupllimentary Duty, Submission of Vat ReturnKhadeeza ShammeeNo ratings yet

- Taxation: Multiple ChoiceDocument16 pagesTaxation: Multiple ChoiceJomar VillenaNo ratings yet

- Taxation Material 1Document11 pagesTaxation Material 1Shaira Bugayong100% (1)

- 5 - Principles of Taxation07092021Document10 pages5 - Principles of Taxation07092021Jahirul IslamNo ratings yet

- MCQ - Taxation Law ReviewDocument24 pagesMCQ - Taxation Law ReviewphiongskiNo ratings yet

- MOCK BAR EXAMINATION MCQs IN TAXATIONDocument10 pagesMOCK BAR EXAMINATION MCQs IN TAXATIONALFONSO CRUZ, JRNo ratings yet

- FAR05 - Accounting For Income and Deferred TaxesDocument4 pagesFAR05 - Accounting For Income and Deferred TaxesDisguised owlNo ratings yet

- Final Examintation - TaxationDocument5 pagesFinal Examintation - TaxationMPCINo ratings yet

- Value Added TaxDocument4 pagesValue Added TaxAllen KateNo ratings yet

- HOMEWORK 2 Tax AdministrationDocument4 pagesHOMEWORK 2 Tax Administrationfitz garlitos100% (1)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- CAso - Tire City ResueltoDocument11 pagesCAso - Tire City ResueltoJhoseph MoraNo ratings yet

- Sales 24344504 q3Document3 pagesSales 24344504 q3Vedantam GuptaNo ratings yet

- Income Statement Hide Corp. Seek Corp. Dr. CR.: Book Value of Stocholders' Equity of Seek CorpDocument11 pagesIncome Statement Hide Corp. Seek Corp. Dr. CR.: Book Value of Stocholders' Equity of Seek CorpmoreNo ratings yet

- 05 Multinational OperationsDocument59 pages05 Multinational OperationsIan ChanNo ratings yet

- A892642655 24805 4 2019 FinancialstatementanalysisDocument7 pagesA892642655 24805 4 2019 FinancialstatementanalysisAshish kumar ThapaNo ratings yet

- Accounts (NEW DRAFT) 24 SeptDocument45 pagesAccounts (NEW DRAFT) 24 Septsaria.ossama.95No ratings yet

- 16 Consolidation Subsequent To The Date of AcquisitionDocument3 pages16 Consolidation Subsequent To The Date of AcquisitionMila Casandra CastañedaNo ratings yet

- Flow Chart (L-2)Document1 pageFlow Chart (L-2)JazaNo ratings yet

- Slide of Chapter 4Document16 pagesSlide of Chapter 4Uyen ThuNo ratings yet

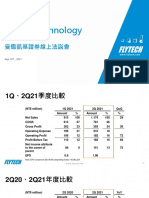

- Flytech TechnologyDocument7 pagesFlytech TechnologyLouis ChenNo ratings yet

- Intermediate Accounting: Reporting Financial PerformanceDocument45 pagesIntermediate Accounting: Reporting Financial PerformancenasduioahwaNo ratings yet

- Income Taxation - Ampongan (SolMan)Document56 pagesIncome Taxation - Ampongan (SolMan)John Dale Mondejar75% (12)

- Economics Today 19th Edition Miller Solutions ManualDocument19 pagesEconomics Today 19th Edition Miller Solutions Manualtusseh.itemm0lh100% (25)

- Conceptual Framework Elements of Financial StatementsDocument18 pagesConceptual Framework Elements of Financial StatementsmaricrisNo ratings yet

- Tax Planning AssignmentDocument10 pagesTax Planning AssignmentJayashree Mohandass100% (1)

- Clouie Jid Malino TLA 6.2Document9 pagesClouie Jid Malino TLA 6.2Raynon AbasNo ratings yet

- Salary SchemeDocument2 pagesSalary SchemeMichelle Acebuche SibayanNo ratings yet

- FinancialsDocument26 pagesFinancials崔梦炎No ratings yet

- Fabm2 q1 Module7 Week7Document6 pagesFabm2 q1 Module7 Week7Ria LomitengNo ratings yet

- Pathuma Distributors - MataraDocument3 pagesPathuma Distributors - MataraChamara Chinthaka RanasingheNo ratings yet

- AFAR Last Minute by HerculesDocument8 pagesAFAR Last Minute by Herculesjanjan3256No ratings yet

- SCOSMAN 3. AbsorptionVariable Costing ModuleDocument7 pagesSCOSMAN 3. AbsorptionVariable Costing ModuleJoneric RamosNo ratings yet

- Project Report: Honours of SEMESTER VI, 2021 in Accounting & Finance Under The University of Calcutta ONDocument20 pagesProject Report: Honours of SEMESTER VI, 2021 in Accounting & Finance Under The University of Calcutta ONBishal AdakNo ratings yet

- Ch-2 Bangladesh Income TaxDocument6 pagesCh-2 Bangladesh Income TaxMd. Rayhanul IslamNo ratings yet

- ExpleoDocument13 pagesExpleog_sivakumarNo ratings yet

- Volume7 Issue8 (2) 2018Document357 pagesVolume7 Issue8 (2) 2018diah savitriNo ratings yet

- Financial Accounting - TheoriesDocument5 pagesFinancial Accounting - TheoriesKim Cristian MaañoNo ratings yet

Download as pdf or txt

You might also like

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- Salary Slip Format For HCLDocument1 pageSalary Slip Format For HCLAmar Rajput58% (12)

- CBLM - Bookkeeping NC III (Aporbo, J)Document28 pagesCBLM - Bookkeeping NC III (Aporbo, J)denmark macalisangNo ratings yet

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionFrom EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNo ratings yet

- Economics Formula SheetDocument10 pagesEconomics Formula SheetCratos_Poseidon100% (1)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Fin623 Solved MCQs For EamsDocument24 pagesFin623 Solved MCQs For EamsSohail Merchant79% (14)

- Cambodian Taxation Reviewers 4Document24 pagesCambodian Taxation Reviewers 4Ken JomelNo ratings yet

- Cambodian Taxation Reviewers 3Document23 pagesCambodian Taxation Reviewers 3Ken JomelNo ratings yet

- Cambodian Taxation Reviewers 2Document25 pagesCambodian Taxation Reviewers 2Ken JomelNo ratings yet

- Cambodian Taxation Reviewers 1Document25 pagesCambodian Taxation Reviewers 1Ken JomelNo ratings yet

- For Sir Red - 20 MCQs - TAXATIONDocument5 pagesFor Sir Red - 20 MCQs - TAXATIONRed Christian PalustreNo ratings yet

- Quiz 4 Vat Business Tax 1322 - CompressDocument3 pagesQuiz 4 Vat Business Tax 1322 - CompressChris MartinezNo ratings yet

- ICAB Knowledge Level Taxation-I Suggested Answer May June 2010 - Nov Dec 2017Document150 pagesICAB Knowledge Level Taxation-I Suggested Answer May June 2010 - Nov Dec 2017Optimal Management Solution91% (11)

- 3rdyr 1stF BusinessTax 2324Document43 pages3rdyr 1stF BusinessTax 2324zaounxosakubNo ratings yet

- Tax Final ExamDocument7 pagesTax Final ExamJulienne UntalascoNo ratings yet

- Input Tax CreditDocument8 pagesInput Tax CreditPranjal AgrawalNo ratings yet

- Tax UpdatesDocument79 pagesTax UpdatesFreijiah SonNo ratings yet

- JPIA Review S3 Installment 2 (Business Tax)Document30 pagesJPIA Review S3 Installment 2 (Business Tax)rylNo ratings yet

- Additions To TaxDocument6 pagesAdditions To TaxJustin Robert RoqueNo ratings yet

- 10-Practical Questions of Individuals (78-113)Document38 pages10-Practical Questions of Individuals (78-113)Sajid Saith0% (1)

- 3rd Quizzer 1st Sem SY 2020-2021 - AKDocument6 pages3rd Quizzer 1st Sem SY 2020-2021 - AKMitzi WamarNo ratings yet

- Vivad Se Vishwas Tax 2025Document17 pagesVivad Se Vishwas Tax 2025Juzer JiruNo ratings yet

- NIRC V. TRAInDocument11 pagesNIRC V. TRAInJin De GuzmanNo ratings yet

- TAX Final PreboardDocument23 pagesTAX Final PreboardEDUARDO JR. VILLANUEVANo ratings yet

- Final Examination - TaxationDocument9 pagesFinal Examination - TaxationCatherine LavadiaNo ratings yet

- Ewt Exam - FormareDocument3 pagesEwt Exam - FormareMikaela SalvadorNo ratings yet

- Allowed Deductions From Gross IncomeDocument8 pagesAllowed Deductions From Gross Incomealliahbilities currentNo ratings yet

- First Preboard TAX ReviewDocument17 pagesFirst Preboard TAX Reviewlois martinNo ratings yet

- Statutory Updates For Nov-21 ExamsDocument50 pagesStatutory Updates For Nov-21 ExamsShodasakshari VidyaNo ratings yet

- MCQ Dimaampao W Answer KeyDocument16 pagesMCQ Dimaampao W Answer KeyvalkyriorNo ratings yet

- 2020NMBE Taxation With AnswersDocument21 pages2020NMBE Taxation With AnswersWilsonNo ratings yet

- Income Tax 2017 Edazdb1013Document50 pagesIncome Tax 2017 Edazdb1013Pradeep PatilNo ratings yet

- Bam 031 CfeDocument43 pagesBam 031 CfeMs VampireNo ratings yet

- VAT - MCQ Test Questions by Mahbub SirDocument16 pagesVAT - MCQ Test Questions by Mahbub SirAysha Alam100% (1)

- Tax Alert No. 91 (Senate Bill (SB) No. 1357 or The Corporate Recovery and Tax Incentives For Enterprises Act (CREATE) )Document9 pagesTax Alert No. 91 (Senate Bill (SB) No. 1357 or The Corporate Recovery and Tax Incentives For Enterprises Act (CREATE) )Karina PulidoNo ratings yet

- National Federation of Junior Philipinne Institute of Accountants - National Capital Region Taxation (Tax)Document10 pagesNational Federation of Junior Philipinne Institute of Accountants - National Capital Region Taxation (Tax)joyceNo ratings yet

- Input Tax Credit (Itc) SystemDocument17 pagesInput Tax Credit (Itc) SystemJasmin BidNo ratings yet

- TAX 2021 - Theories and Independent ProblemsDocument28 pagesTAX 2021 - Theories and Independent ProblemsMingcheng JeeNo ratings yet

- What Is Input Tax Credit - GST IndiaDocument4 pagesWhat Is Input Tax Credit - GST Indiaaslam_bechemNo ratings yet

- BAM031 P3 Q1 Answer FBT DeductionsDocument12 pagesBAM031 P3 Q1 Answer FBT DeductionsMary Lyn DatuinNo ratings yet

- Supllimentary Duty, Submission of Vat ReturnDocument51 pagesSupllimentary Duty, Submission of Vat ReturnKhadeeza ShammeeNo ratings yet

- Taxation: Multiple ChoiceDocument16 pagesTaxation: Multiple ChoiceJomar VillenaNo ratings yet

- Taxation Material 1Document11 pagesTaxation Material 1Shaira Bugayong100% (1)

- 5 - Principles of Taxation07092021Document10 pages5 - Principles of Taxation07092021Jahirul IslamNo ratings yet

- MCQ - Taxation Law ReviewDocument24 pagesMCQ - Taxation Law ReviewphiongskiNo ratings yet

- MOCK BAR EXAMINATION MCQs IN TAXATIONDocument10 pagesMOCK BAR EXAMINATION MCQs IN TAXATIONALFONSO CRUZ, JRNo ratings yet

- FAR05 - Accounting For Income and Deferred TaxesDocument4 pagesFAR05 - Accounting For Income and Deferred TaxesDisguised owlNo ratings yet

- Final Examintation - TaxationDocument5 pagesFinal Examintation - TaxationMPCINo ratings yet

- Value Added TaxDocument4 pagesValue Added TaxAllen KateNo ratings yet

- HOMEWORK 2 Tax AdministrationDocument4 pagesHOMEWORK 2 Tax Administrationfitz garlitos100% (1)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- CAso - Tire City ResueltoDocument11 pagesCAso - Tire City ResueltoJhoseph MoraNo ratings yet

- Sales 24344504 q3Document3 pagesSales 24344504 q3Vedantam GuptaNo ratings yet

- Income Statement Hide Corp. Seek Corp. Dr. CR.: Book Value of Stocholders' Equity of Seek CorpDocument11 pagesIncome Statement Hide Corp. Seek Corp. Dr. CR.: Book Value of Stocholders' Equity of Seek CorpmoreNo ratings yet

- 05 Multinational OperationsDocument59 pages05 Multinational OperationsIan ChanNo ratings yet

- A892642655 24805 4 2019 FinancialstatementanalysisDocument7 pagesA892642655 24805 4 2019 FinancialstatementanalysisAshish kumar ThapaNo ratings yet

- Accounts (NEW DRAFT) 24 SeptDocument45 pagesAccounts (NEW DRAFT) 24 Septsaria.ossama.95No ratings yet

- 16 Consolidation Subsequent To The Date of AcquisitionDocument3 pages16 Consolidation Subsequent To The Date of AcquisitionMila Casandra CastañedaNo ratings yet

- Flow Chart (L-2)Document1 pageFlow Chart (L-2)JazaNo ratings yet

- Slide of Chapter 4Document16 pagesSlide of Chapter 4Uyen ThuNo ratings yet

- Flytech TechnologyDocument7 pagesFlytech TechnologyLouis ChenNo ratings yet

- Intermediate Accounting: Reporting Financial PerformanceDocument45 pagesIntermediate Accounting: Reporting Financial PerformancenasduioahwaNo ratings yet

- Income Taxation - Ampongan (SolMan)Document56 pagesIncome Taxation - Ampongan (SolMan)John Dale Mondejar75% (12)

- Economics Today 19th Edition Miller Solutions ManualDocument19 pagesEconomics Today 19th Edition Miller Solutions Manualtusseh.itemm0lh100% (25)

- Conceptual Framework Elements of Financial StatementsDocument18 pagesConceptual Framework Elements of Financial StatementsmaricrisNo ratings yet

- Tax Planning AssignmentDocument10 pagesTax Planning AssignmentJayashree Mohandass100% (1)

- Clouie Jid Malino TLA 6.2Document9 pagesClouie Jid Malino TLA 6.2Raynon AbasNo ratings yet

- Salary SchemeDocument2 pagesSalary SchemeMichelle Acebuche SibayanNo ratings yet

- FinancialsDocument26 pagesFinancials崔梦炎No ratings yet

- Fabm2 q1 Module7 Week7Document6 pagesFabm2 q1 Module7 Week7Ria LomitengNo ratings yet

- Pathuma Distributors - MataraDocument3 pagesPathuma Distributors - MataraChamara Chinthaka RanasingheNo ratings yet

- AFAR Last Minute by HerculesDocument8 pagesAFAR Last Minute by Herculesjanjan3256No ratings yet

- SCOSMAN 3. AbsorptionVariable Costing ModuleDocument7 pagesSCOSMAN 3. AbsorptionVariable Costing ModuleJoneric RamosNo ratings yet

- Project Report: Honours of SEMESTER VI, 2021 in Accounting & Finance Under The University of Calcutta ONDocument20 pagesProject Report: Honours of SEMESTER VI, 2021 in Accounting & Finance Under The University of Calcutta ONBishal AdakNo ratings yet

- Ch-2 Bangladesh Income TaxDocument6 pagesCh-2 Bangladesh Income TaxMd. Rayhanul IslamNo ratings yet

- ExpleoDocument13 pagesExpleog_sivakumarNo ratings yet

- Volume7 Issue8 (2) 2018Document357 pagesVolume7 Issue8 (2) 2018diah savitriNo ratings yet

- Financial Accounting - TheoriesDocument5 pagesFinancial Accounting - TheoriesKim Cristian MaañoNo ratings yet