Responding To Service of Legal Process Subpoenas Garnishments and Levies

Responding To Service of Legal Process Subpoenas Garnishments and Levies

You might also like

- Pipe & Excavation Contracting RevisedDocument407 pagesPipe & Excavation Contracting RevisedKarl Terzaghi86% (7)

- WiproDocument11 pagesWipromyclicksNo ratings yet

- Levy LawsuitDocument13 pagesLevy LawsuitAsbury Park PressNo ratings yet

- Articles of Organization Limited-Liability Company: (Pursuant To Nrs Chapter 86)Document9 pagesArticles of Organization Limited-Liability Company: (Pursuant To Nrs Chapter 86)RocketLawyer100% (1)

- Notice of Tort ClaimDocument2 pagesNotice of Tort ClaimMarie Marilyn100% (1)

- Assurance of Discontinuance With Praying Pelicans MissionsDocument25 pagesAssurance of Discontinuance With Praying Pelicans MissionsDuluth News Tribune100% (2)

- DLR DismissalDocument11 pagesDLR DismissalMike Carraggi100% (1)

- Types of ContractsDocument96 pagesTypes of ContractsrachelNo ratings yet

- Gec CaseDocument4 pagesGec CaseMayank RajNo ratings yet

- Casa Baixo CustoDocument45 pagesCasa Baixo CustoMicael CruzNo ratings yet

- United Nations Convention On The Law of The SeaDocument12 pagesUnited Nations Convention On The Law of The SeaoduronyarkolawreneNo ratings yet

- Foreclosure Prevention Process AgreementDocument3 pagesForeclosure Prevention Process AgreementAnthonyHansenNo ratings yet

- Judge Helen Blackwood Ethics Violation #2Document2 pagesJudge Helen Blackwood Ethics Violation #2Samuel L. RiversNo ratings yet

- ssm2006 03 PDFDocument257 pagesssm2006 03 PDFPatrick PerezNo ratings yet

- 150813bock AmicusbriefDocument46 pages150813bock AmicusbriefSamuelNo ratings yet

- Steinberg Hart - A Guide To Converting Hotels To Housing PDFDocument21 pagesSteinberg Hart - A Guide To Converting Hotels To Housing PDFFahmi AdhitamaNo ratings yet

- PV 2023 Session 2Document47 pagesPV 2023 Session 2BezawitNo ratings yet

- An Aid SuiteDocument4 pagesAn Aid SuiteNaamir Wahiyd BeyNo ratings yet

- Protecting Tenants at Foreclosure: BackgroundDocument4 pagesProtecting Tenants at Foreclosure: BackgroundPatrick LongNo ratings yet

- STC 2012 10k Without ContractsDocument80 pagesSTC 2012 10k Without Contractspeterlee100100% (1)

- Assignment 5 - Wrongful DismissalDocument3 pagesAssignment 5 - Wrongful DismissalAraceli Gloria-Francisco100% (1)

- Buczek 20100914 Judicial Notice of Harassing EmailsDocument18 pagesBuczek 20100914 Judicial Notice of Harassing EmailsBob Hurt100% (1)

- Divine LawDocument51 pagesDivine LawLeo GuillermoNo ratings yet

- Quitclaim DeedDocument4 pagesQuitclaim Deedjusmathoughts2No ratings yet

- Fraud Asuransi KesehatanDocument9 pagesFraud Asuransi KesehatanOlivia JosianaNo ratings yet

- Internal Remedies Must Be Exhausted Before Resorting To CourtDocument8 pagesInternal Remedies Must Be Exhausted Before Resorting To CourtEwurama BoatengNo ratings yet

- Polk County Circuit Court Clerk ReportDocument11 pagesPolk County Circuit Court Clerk ReportDan LehrNo ratings yet

- Bill of RightsDocument4 pagesBill of RightsArahbellsNo ratings yet

- Buczek 20101025 Skretny Order Denying Motion To Revoke Bail 121Document3 pagesBuczek 20101025 Skretny Order Denying Motion To Revoke Bail 121Bob HurtNo ratings yet

- Durable Power of Attorney DocumentDocument2 pagesDurable Power of Attorney DocumentQuincy Von Wildbeast100% (1)

- Affidavit and Documents in SupportDocument17 pagesAffidavit and Documents in SupportLegal Public NoticesNo ratings yet

- Weintraub v. QUICKEN LOANS, INC, 594 F.3d 270, 4th Cir. (2010)Document12 pagesWeintraub v. QUICKEN LOANS, INC, 594 F.3d 270, 4th Cir. (2010)Scribd Government DocsNo ratings yet

- Solar Energy: Y.MOHAN SAI (BA15ARC060) Vamshi Krishna (Ba15Arc059) Shibadatta Shibani Prasad (Ba15Arc049)Document29 pagesSolar Energy: Y.MOHAN SAI (BA15ARC060) Vamshi Krishna (Ba15Arc059) Shibadatta Shibani Prasad (Ba15Arc049)Kaushiki KambojNo ratings yet

- The Complete Guide To AffirmationsDocument7 pagesThe Complete Guide To AffirmationsMastersam888No ratings yet

- Real Estate Power of Attorney TemplateDocument5 pagesReal Estate Power of Attorney TemplateRandolph AlvarezNo ratings yet

- Notice of Acceptance of Oath of OfficeDocument10 pagesNotice of Acceptance of Oath of OfficeJustin BurgessNo ratings yet

- No More YearsDocument12 pagesNo More Yearstfaber2933100% (1)

- Uniform Statutory Power of AttorneyDocument3 pagesUniform Statutory Power of Attorneyabrarh100% (1)

- c75s3 PDFDocument1,724 pagesc75s3 PDFRichard LucianoNo ratings yet

- Illinois Freedom of Information Act (FOIA) : Frequently Asked Questions by The PublicDocument12 pagesIllinois Freedom of Information Act (FOIA) : Frequently Asked Questions by The PublicletscurecancerNo ratings yet

- Sample: MERS Mortgage Language Has Been Inserted As Blue TextDocument3 pagesSample: MERS Mortgage Language Has Been Inserted As Blue TextRichie CollinsNo ratings yet

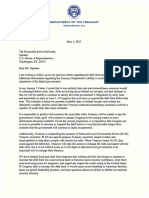

- Sec. Yellen Letter To Speaker McCarthyDocument2 pagesSec. Yellen Letter To Speaker McCarthyDaily Caller News FoundationNo ratings yet

- The Numbers Refer To Section A-B Sheet, Section A DetailDocument41 pagesThe Numbers Refer To Section A-B Sheet, Section A DetailenyonyoziNo ratings yet

- Notice of Proposed RulemakingDocument8 pagesNotice of Proposed RulemakingCircuit MediaNo ratings yet

- Big Banks Puppet Attorney General Organized Crime PersonifiedDocument5 pagesBig Banks Puppet Attorney General Organized Crime PersonifiedFrank GallagherNo ratings yet

- Susan B Anthony V United States US CitizenshipDocument14 pagesSusan B Anthony V United States US CitizenshipSolankhNo ratings yet

- MaxPlanck Yearbook of United Nations LawDocument24 pagesMaxPlanck Yearbook of United Nations LawIvar Jesus Calixto PeñafielNo ratings yet

- Today 10.lenderDocument9 pagesToday 10.lenderGamaya EmmanuelNo ratings yet

- Declaration of Trust With Power of AttorneyDocument1 pageDeclaration of Trust With Power of AttorneyCora EleazarNo ratings yet

- Legality of MinorDocument50 pagesLegality of Minorkareem hassanNo ratings yet

- Property Wood 2016-2-1 2Document34 pagesProperty Wood 2016-2-1 2JjjjmmmmNo ratings yet

- Universal Premium Acceptance Corporation v. The York Bank & Trust Company, 69 F.3d 695, 3rd Cir. (1995)Document13 pagesUniversal Premium Acceptance Corporation v. The York Bank & Trust Company, 69 F.3d 695, 3rd Cir. (1995)Scribd Government DocsNo ratings yet

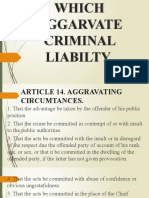

- Circumtances Which Aggarvate Criminal LiabiltyDocument45 pagesCircumtances Which Aggarvate Criminal LiabiltyAstro SteezyNo ratings yet

- Fdcpa HandoutsDocument7 pagesFdcpa HandoutsStephen MonaghanNo ratings yet

- Loan Modification: Contract & FormsDocument16 pagesLoan Modification: Contract & Formsldobbins2No ratings yet

- Wells Fargo v. Crown, Ariz. Ct. App. (2014)Document16 pagesWells Fargo v. Crown, Ariz. Ct. App. (2014)Scribd Government Docs100% (1)

- Organizational Chart of LawDocument5 pagesOrganizational Chart of LawThom Arvin Recardo100% (1)

- ReviewerDocument19 pagesReviewerailynvdsNo ratings yet

- ICCForm Reparation 2 enDocument14 pagesICCForm Reparation 2 enEmpressInINo ratings yet

- Cease and Desist Advance AutoDocument2 pagesCease and Desist Advance AutoGersh KuntzmanNo ratings yet

- Safe Guarding Your Future: Financial Literacy How a Trusts Can Shield Your Assets & Reduce TaxesFrom EverandSafe Guarding Your Future: Financial Literacy How a Trusts Can Shield Your Assets & Reduce TaxesNo ratings yet

- Order Denying Motion For Preliminary Injunction Seascape PropertiesDocument32 pagesOrder Denying Motion For Preliminary Injunction Seascape PropertiesKevin AccettullaNo ratings yet

- EU Micro Policies - CAP TradeDocument15 pagesEU Micro Policies - CAP Tradezeynepbastug02No ratings yet

- Jun 2006 - Qns Mod BDocument13 pagesJun 2006 - Qns Mod BHubbak KhanNo ratings yet

- 21 30Document46 pages21 30Michael Renz PalabayNo ratings yet

- TN NINAN The Arbitary StateDocument1 pageTN NINAN The Arbitary Stateankit_ag@hotmail.comNo ratings yet

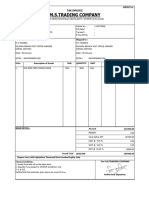

- Max Super Speciality Hospital, Saket (East) 2, Press Enclave Road, Saket New Delhi - 110017 Bill of SupplyDocument2 pagesMax Super Speciality Hospital, Saket (East) 2, Press Enclave Road, Saket New Delhi - 110017 Bill of SupplymnzNo ratings yet

- Tax Return Filling ProcedureDocument16 pagesTax Return Filling Procedurefrankline nyabutoNo ratings yet

- Literature Review On Equity AnalysisDocument8 pagesLiterature Review On Equity Analysisafdtnybjp100% (1)

- 8 RR No. 16-2021 (Allowing Submission of Scanned Copies of 2307)Document3 pages8 RR No. 16-2021 (Allowing Submission of Scanned Copies of 2307)Mark DomingoNo ratings yet

- Salary SlipDocument1 pageSalary SlipGaurav DevraNo ratings yet

- 2019-01 Nieuwsbrief Uzk ENUDocument2 pages2019-01 Nieuwsbrief Uzk ENUAdrian OanceaNo ratings yet

- Proposed Production Distribution of Coconut Wine Contained in Tetra Packs PDFDocument373 pagesProposed Production Distribution of Coconut Wine Contained in Tetra Packs PDFREADS RESEARCHNo ratings yet

- CBDTChallanForm25 06 2022Document1 pageCBDTChallanForm25 06 2022Shivaani ManoharanNo ratings yet

- Barandai Kalai-1Document1 pageBarandai Kalai-1mysterious.eyes121No ratings yet

- Salary Slip (31563893 September 2019)Document1 pageSalary Slip (31563893 September 2019)Asif AliNo ratings yet

- Tax InvoiceDocument1 pageTax InvoiceRatna BharathNo ratings yet

- C. Corpo DigestDocument9 pagesC. Corpo DigestRaymarc Elizer AsuncionNo ratings yet

- Assignment (Pre-Answers) PDFDocument63 pagesAssignment (Pre-Answers) PDFRussell KeyesNo ratings yet

- National Power Corporation vs. The Provincial Treasurer of Benguet, Et Al.Document13 pagesNational Power Corporation vs. The Provincial Treasurer of Benguet, Et Al.red gynNo ratings yet

- Payroll Accounting 2018 28Th Edition Bieg Test Bank Full Chapter PDFDocument36 pagesPayroll Accounting 2018 28Th Edition Bieg Test Bank Full Chapter PDFentrickaretologyswr100% (9)

- MODULE 2 Business FinanceDocument16 pagesMODULE 2 Business FinanceWinshei CaguladaNo ratings yet

- Technizer-Java8-Online - Invoice - 8Document4 pagesTechnizer-Java8-Online - Invoice - 8Srinivasa HelavarNo ratings yet

- Arogya Sanjeevani Policy, Icici Lombard Prospectus: What Is Covered?Document11 pagesArogya Sanjeevani Policy, Icici Lombard Prospectus: What Is Covered?pradiphdasNo ratings yet

- Old Form 0605 PDFDocument2 pagesOld Form 0605 PDFeugene badere50% (2)

- Up23t 4849Document3 pagesUp23t 4849arshadnsdl8No ratings yet

- Taxation Auditing Problems: (Monday) (Wednesday)Document2 pagesTaxation Auditing Problems: (Monday) (Wednesday)Carmen TabundaNo ratings yet

- CH 18 ControlDocument20 pagesCH 18 ControlSameh YassienNo ratings yet

Download as pdf or txt

You might also like

- Pipe & Excavation Contracting RevisedDocument407 pagesPipe & Excavation Contracting RevisedKarl Terzaghi86% (7)

- WiproDocument11 pagesWipromyclicksNo ratings yet

- Levy LawsuitDocument13 pagesLevy LawsuitAsbury Park PressNo ratings yet

- Articles of Organization Limited-Liability Company: (Pursuant To Nrs Chapter 86)Document9 pagesArticles of Organization Limited-Liability Company: (Pursuant To Nrs Chapter 86)RocketLawyer100% (1)

- Notice of Tort ClaimDocument2 pagesNotice of Tort ClaimMarie Marilyn100% (1)

- Assurance of Discontinuance With Praying Pelicans MissionsDocument25 pagesAssurance of Discontinuance With Praying Pelicans MissionsDuluth News Tribune100% (2)

- DLR DismissalDocument11 pagesDLR DismissalMike Carraggi100% (1)

- Types of ContractsDocument96 pagesTypes of ContractsrachelNo ratings yet

- Gec CaseDocument4 pagesGec CaseMayank RajNo ratings yet

- Casa Baixo CustoDocument45 pagesCasa Baixo CustoMicael CruzNo ratings yet

- United Nations Convention On The Law of The SeaDocument12 pagesUnited Nations Convention On The Law of The SeaoduronyarkolawreneNo ratings yet

- Foreclosure Prevention Process AgreementDocument3 pagesForeclosure Prevention Process AgreementAnthonyHansenNo ratings yet

- Judge Helen Blackwood Ethics Violation #2Document2 pagesJudge Helen Blackwood Ethics Violation #2Samuel L. RiversNo ratings yet

- ssm2006 03 PDFDocument257 pagesssm2006 03 PDFPatrick PerezNo ratings yet

- 150813bock AmicusbriefDocument46 pages150813bock AmicusbriefSamuelNo ratings yet

- Steinberg Hart - A Guide To Converting Hotels To Housing PDFDocument21 pagesSteinberg Hart - A Guide To Converting Hotels To Housing PDFFahmi AdhitamaNo ratings yet

- PV 2023 Session 2Document47 pagesPV 2023 Session 2BezawitNo ratings yet

- An Aid SuiteDocument4 pagesAn Aid SuiteNaamir Wahiyd BeyNo ratings yet

- Protecting Tenants at Foreclosure: BackgroundDocument4 pagesProtecting Tenants at Foreclosure: BackgroundPatrick LongNo ratings yet

- STC 2012 10k Without ContractsDocument80 pagesSTC 2012 10k Without Contractspeterlee100100% (1)

- Assignment 5 - Wrongful DismissalDocument3 pagesAssignment 5 - Wrongful DismissalAraceli Gloria-Francisco100% (1)

- Buczek 20100914 Judicial Notice of Harassing EmailsDocument18 pagesBuczek 20100914 Judicial Notice of Harassing EmailsBob Hurt100% (1)

- Divine LawDocument51 pagesDivine LawLeo GuillermoNo ratings yet

- Quitclaim DeedDocument4 pagesQuitclaim Deedjusmathoughts2No ratings yet

- Fraud Asuransi KesehatanDocument9 pagesFraud Asuransi KesehatanOlivia JosianaNo ratings yet

- Internal Remedies Must Be Exhausted Before Resorting To CourtDocument8 pagesInternal Remedies Must Be Exhausted Before Resorting To CourtEwurama BoatengNo ratings yet

- Polk County Circuit Court Clerk ReportDocument11 pagesPolk County Circuit Court Clerk ReportDan LehrNo ratings yet

- Bill of RightsDocument4 pagesBill of RightsArahbellsNo ratings yet

- Buczek 20101025 Skretny Order Denying Motion To Revoke Bail 121Document3 pagesBuczek 20101025 Skretny Order Denying Motion To Revoke Bail 121Bob HurtNo ratings yet

- Durable Power of Attorney DocumentDocument2 pagesDurable Power of Attorney DocumentQuincy Von Wildbeast100% (1)

- Affidavit and Documents in SupportDocument17 pagesAffidavit and Documents in SupportLegal Public NoticesNo ratings yet

- Weintraub v. QUICKEN LOANS, INC, 594 F.3d 270, 4th Cir. (2010)Document12 pagesWeintraub v. QUICKEN LOANS, INC, 594 F.3d 270, 4th Cir. (2010)Scribd Government DocsNo ratings yet

- Solar Energy: Y.MOHAN SAI (BA15ARC060) Vamshi Krishna (Ba15Arc059) Shibadatta Shibani Prasad (Ba15Arc049)Document29 pagesSolar Energy: Y.MOHAN SAI (BA15ARC060) Vamshi Krishna (Ba15Arc059) Shibadatta Shibani Prasad (Ba15Arc049)Kaushiki KambojNo ratings yet

- The Complete Guide To AffirmationsDocument7 pagesThe Complete Guide To AffirmationsMastersam888No ratings yet

- Real Estate Power of Attorney TemplateDocument5 pagesReal Estate Power of Attorney TemplateRandolph AlvarezNo ratings yet

- Notice of Acceptance of Oath of OfficeDocument10 pagesNotice of Acceptance of Oath of OfficeJustin BurgessNo ratings yet

- No More YearsDocument12 pagesNo More Yearstfaber2933100% (1)

- Uniform Statutory Power of AttorneyDocument3 pagesUniform Statutory Power of Attorneyabrarh100% (1)

- c75s3 PDFDocument1,724 pagesc75s3 PDFRichard LucianoNo ratings yet

- Illinois Freedom of Information Act (FOIA) : Frequently Asked Questions by The PublicDocument12 pagesIllinois Freedom of Information Act (FOIA) : Frequently Asked Questions by The PublicletscurecancerNo ratings yet

- Sample: MERS Mortgage Language Has Been Inserted As Blue TextDocument3 pagesSample: MERS Mortgage Language Has Been Inserted As Blue TextRichie CollinsNo ratings yet

- Sec. Yellen Letter To Speaker McCarthyDocument2 pagesSec. Yellen Letter To Speaker McCarthyDaily Caller News FoundationNo ratings yet

- The Numbers Refer To Section A-B Sheet, Section A DetailDocument41 pagesThe Numbers Refer To Section A-B Sheet, Section A DetailenyonyoziNo ratings yet

- Notice of Proposed RulemakingDocument8 pagesNotice of Proposed RulemakingCircuit MediaNo ratings yet

- Big Banks Puppet Attorney General Organized Crime PersonifiedDocument5 pagesBig Banks Puppet Attorney General Organized Crime PersonifiedFrank GallagherNo ratings yet

- Susan B Anthony V United States US CitizenshipDocument14 pagesSusan B Anthony V United States US CitizenshipSolankhNo ratings yet

- MaxPlanck Yearbook of United Nations LawDocument24 pagesMaxPlanck Yearbook of United Nations LawIvar Jesus Calixto PeñafielNo ratings yet

- Today 10.lenderDocument9 pagesToday 10.lenderGamaya EmmanuelNo ratings yet

- Declaration of Trust With Power of AttorneyDocument1 pageDeclaration of Trust With Power of AttorneyCora EleazarNo ratings yet

- Legality of MinorDocument50 pagesLegality of Minorkareem hassanNo ratings yet

- Property Wood 2016-2-1 2Document34 pagesProperty Wood 2016-2-1 2JjjjmmmmNo ratings yet

- Universal Premium Acceptance Corporation v. The York Bank & Trust Company, 69 F.3d 695, 3rd Cir. (1995)Document13 pagesUniversal Premium Acceptance Corporation v. The York Bank & Trust Company, 69 F.3d 695, 3rd Cir. (1995)Scribd Government DocsNo ratings yet

- Circumtances Which Aggarvate Criminal LiabiltyDocument45 pagesCircumtances Which Aggarvate Criminal LiabiltyAstro SteezyNo ratings yet

- Fdcpa HandoutsDocument7 pagesFdcpa HandoutsStephen MonaghanNo ratings yet

- Loan Modification: Contract & FormsDocument16 pagesLoan Modification: Contract & Formsldobbins2No ratings yet

- Wells Fargo v. Crown, Ariz. Ct. App. (2014)Document16 pagesWells Fargo v. Crown, Ariz. Ct. App. (2014)Scribd Government Docs100% (1)

- Organizational Chart of LawDocument5 pagesOrganizational Chart of LawThom Arvin Recardo100% (1)

- ReviewerDocument19 pagesReviewerailynvdsNo ratings yet

- ICCForm Reparation 2 enDocument14 pagesICCForm Reparation 2 enEmpressInINo ratings yet

- Cease and Desist Advance AutoDocument2 pagesCease and Desist Advance AutoGersh KuntzmanNo ratings yet

- Safe Guarding Your Future: Financial Literacy How a Trusts Can Shield Your Assets & Reduce TaxesFrom EverandSafe Guarding Your Future: Financial Literacy How a Trusts Can Shield Your Assets & Reduce TaxesNo ratings yet

- Order Denying Motion For Preliminary Injunction Seascape PropertiesDocument32 pagesOrder Denying Motion For Preliminary Injunction Seascape PropertiesKevin AccettullaNo ratings yet

- EU Micro Policies - CAP TradeDocument15 pagesEU Micro Policies - CAP Tradezeynepbastug02No ratings yet

- Jun 2006 - Qns Mod BDocument13 pagesJun 2006 - Qns Mod BHubbak KhanNo ratings yet

- 21 30Document46 pages21 30Michael Renz PalabayNo ratings yet

- TN NINAN The Arbitary StateDocument1 pageTN NINAN The Arbitary Stateankit_ag@hotmail.comNo ratings yet

- Max Super Speciality Hospital, Saket (East) 2, Press Enclave Road, Saket New Delhi - 110017 Bill of SupplyDocument2 pagesMax Super Speciality Hospital, Saket (East) 2, Press Enclave Road, Saket New Delhi - 110017 Bill of SupplymnzNo ratings yet

- Tax Return Filling ProcedureDocument16 pagesTax Return Filling Procedurefrankline nyabutoNo ratings yet

- Literature Review On Equity AnalysisDocument8 pagesLiterature Review On Equity Analysisafdtnybjp100% (1)

- 8 RR No. 16-2021 (Allowing Submission of Scanned Copies of 2307)Document3 pages8 RR No. 16-2021 (Allowing Submission of Scanned Copies of 2307)Mark DomingoNo ratings yet

- Salary SlipDocument1 pageSalary SlipGaurav DevraNo ratings yet

- 2019-01 Nieuwsbrief Uzk ENUDocument2 pages2019-01 Nieuwsbrief Uzk ENUAdrian OanceaNo ratings yet

- Proposed Production Distribution of Coconut Wine Contained in Tetra Packs PDFDocument373 pagesProposed Production Distribution of Coconut Wine Contained in Tetra Packs PDFREADS RESEARCHNo ratings yet

- CBDTChallanForm25 06 2022Document1 pageCBDTChallanForm25 06 2022Shivaani ManoharanNo ratings yet

- Barandai Kalai-1Document1 pageBarandai Kalai-1mysterious.eyes121No ratings yet

- Salary Slip (31563893 September 2019)Document1 pageSalary Slip (31563893 September 2019)Asif AliNo ratings yet

- Tax InvoiceDocument1 pageTax InvoiceRatna BharathNo ratings yet

- C. Corpo DigestDocument9 pagesC. Corpo DigestRaymarc Elizer AsuncionNo ratings yet

- Assignment (Pre-Answers) PDFDocument63 pagesAssignment (Pre-Answers) PDFRussell KeyesNo ratings yet

- National Power Corporation vs. The Provincial Treasurer of Benguet, Et Al.Document13 pagesNational Power Corporation vs. The Provincial Treasurer of Benguet, Et Al.red gynNo ratings yet

- Payroll Accounting 2018 28Th Edition Bieg Test Bank Full Chapter PDFDocument36 pagesPayroll Accounting 2018 28Th Edition Bieg Test Bank Full Chapter PDFentrickaretologyswr100% (9)

- MODULE 2 Business FinanceDocument16 pagesMODULE 2 Business FinanceWinshei CaguladaNo ratings yet

- Technizer-Java8-Online - Invoice - 8Document4 pagesTechnizer-Java8-Online - Invoice - 8Srinivasa HelavarNo ratings yet

- Arogya Sanjeevani Policy, Icici Lombard Prospectus: What Is Covered?Document11 pagesArogya Sanjeevani Policy, Icici Lombard Prospectus: What Is Covered?pradiphdasNo ratings yet

- Old Form 0605 PDFDocument2 pagesOld Form 0605 PDFeugene badere50% (2)

- Up23t 4849Document3 pagesUp23t 4849arshadnsdl8No ratings yet

- Taxation Auditing Problems: (Monday) (Wednesday)Document2 pagesTaxation Auditing Problems: (Monday) (Wednesday)Carmen TabundaNo ratings yet

- CH 18 ControlDocument20 pagesCH 18 ControlSameh YassienNo ratings yet