Download as pdf or txt

You might also like

- Lesson Guide 2.2 Beware of Banking FeesDocument4 pagesLesson Guide 2.2 Beware of Banking FeesKent TiclavilcaNo ratings yet

- Cochan Singapore Pte. Ltd. - Annual Report 2011Document30 pagesCochan Singapore Pte. Ltd. - Annual Report 2011aliciawittmeyerNo ratings yet

- Stock Market For BeginnersDocument166 pagesStock Market For BeginnersJatin Rana100% (5)

- Financial Shenanigans 3rd EditionDocument6 pagesFinancial Shenanigans 3rd Editionpwsicher100% (1)

- Stellar Account Presentation123Document8 pagesStellar Account Presentation123Supriya SantNo ratings yet

- Hsa Vs MetcDocument14 pagesHsa Vs MetcgwzglNo ratings yet

- Lesson 1 DebtDocument21 pagesLesson 1 DebtAlf ChingNo ratings yet

- Credit and CollectionDocument17 pagesCredit and CollectionDia Cessianne VillarolaNo ratings yet

- 2017 Employee Benefit Highlights - Support StaffDocument8 pages2017 Employee Benefit Highlights - Support StaffJohn AcardoNo ratings yet

- Personalized Cost EstimateDocument15 pagesPersonalized Cost EstimateOswaldo ParraNo ratings yet

- 2020 Ankura Benefits GuideDocument20 pages2020 Ankura Benefits GuidegpperkNo ratings yet

- Important Information About Your Insurance: GPO Box 1901 Melbourne VIC 3001 Australia T 1300 300 273 F 1300 366 273Document8 pagesImportant Information About Your Insurance: GPO Box 1901 Melbourne VIC 3001 Australia T 1300 300 273 F 1300 366 273Antoine Nabil ZakiNo ratings yet

- Ten Principles of Personal Financial LiteracyDocument20 pagesTen Principles of Personal Financial LiteracyARCHEL ORASANo ratings yet

- Summary of 2022 Benefit Changes: MedicalDocument5 pagesSummary of 2022 Benefit Changes: MedicalChinnu SalimathNo ratings yet

- 2022 Steven Charles BAG - CODocument4 pages2022 Steven Charles BAG - COAlejuanchis Kamacho GarciaNo ratings yet

- Description: Micro Grameen What Ismicro Grameen?Document8 pagesDescription: Micro Grameen What Ismicro Grameen?Saligan DolfNo ratings yet

- Get Help Paying Your Medicare CostsDocument2 pagesGet Help Paying Your Medicare CostsdfdgfdfgfdfgNo ratings yet

- AR CC Finance Committee February 2018.2 - 01 17 2018Document10 pagesAR CC Finance Committee February 2018.2 - 01 17 2018The Daily LineNo ratings yet

- Buget - Again.Document9 pagesBuget - Again.Rolan Mart SasongkoNo ratings yet

- DxwebDocument7 pagesDxwebjamespaulgilbertNo ratings yet

- FY 2022-2023 Instruction Partners Benefits OverviewDocument16 pagesFY 2022-2023 Instruction Partners Benefits OverviewSendhil RevuluriNo ratings yet

- Submitted Successfully Required Follow UpsDocument4 pagesSubmitted Successfully Required Follow UpsEmme WeaverNo ratings yet

- Investment Planning Workbook: Getting StartedDocument8 pagesInvestment Planning Workbook: Getting StartedshanpiePLNo ratings yet

- Tema 3 Rev3Document49 pagesTema 3 Rev3CarlosA.HurtadoNo ratings yet

- The Broker Network Powerpoint 2019Document18 pagesThe Broker Network Powerpoint 2019api-325349652No ratings yet

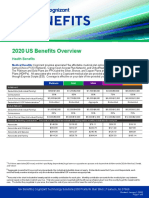

- 2020 US Benefits OverviewDocument5 pages2020 US Benefits OverviewrdmNo ratings yet

- Dunlapslk PresentationDocument18 pagesDunlapslk Presentationapi-325349652No ratings yet

- AA1B Index Statement of AccountsDocument5 pagesAA1B Index Statement of AccountsbscurNo ratings yet

- 123 Student Current Account KFD Do-Ec-188Document10 pages123 Student Current Account KFD Do-Ec-188bugNo ratings yet

- 1500SBC2021Document8 pages1500SBC2021Carlos Andres Correa Gomez (Carlos Gomez)No ratings yet

- 5-Benefits at A GlanceDocument2 pages5-Benefits at A GlanceBlackBunny103No ratings yet

- WWW Healthcare Gov/sbc-GlossaryDocument6 pagesWWW Healthcare Gov/sbc-Glossarytroubledcutie1987No ratings yet

- Checking Accounts: Personal BankingDocument2 pagesChecking Accounts: Personal BankingAjimisinmi ToluwalaseNo ratings yet

- Summary of Benefits: Quartz Medicare Advantage (HMO), in Partnership With UW HealthDocument20 pagesSummary of Benefits: Quartz Medicare Advantage (HMO), in Partnership With UW HealthChris CoulmanNo ratings yet

- Sione and Andrea (Rework)Document10 pagesSione and Andrea (Rework)Ammer Yaser MehetanNo ratings yet

- Life InsuranceDocument2 pagesLife InsuranceaclassensNo ratings yet

- S608CHC Blue Choice Silver PPO 024: This Is Only A SummaryDocument8 pagesS608CHC Blue Choice Silver PPO 024: This Is Only A SummaryAnonymous nx3VC6zHn2No ratings yet

- Benefits SummaryDocument2 pagesBenefits SummaryGustavo StorNo ratings yet

- Account Summary - PlumDocument1 pageAccount Summary - Plumpeck.visperasNo ratings yet

- OE Powerpoint PresentationDocument35 pagesOE Powerpoint PresentationAnonymous ibpKT07GNo ratings yet

- DBS Multiplier Programme - FAQDocument19 pagesDBS Multiplier Programme - FAQverve1977No ratings yet

- Coverage Statement: Employee 888888888Document2 pagesCoverage Statement: Employee 888888888007shivangNo ratings yet

- W-1QMBR Medicare Savings Redetermination Form PDFDocument3 pagesW-1QMBR Medicare Savings Redetermination Form PDFehaegertNo ratings yet

- Personal Finances Lecture NotesDocument10 pagesPersonal Finances Lecture NotesJasmine Clemons-Mills [STUDENT]No ratings yet

- HSBC Premier TcsDocument3 pagesHSBC Premier TcsDreamworxx DevelopmentsNo ratings yet

- Elite Financial Form B - 12feb2014 PDFDocument2 pagesElite Financial Form B - 12feb2014 PDFSharmaine JucoNo ratings yet

- We're Here To Help.: Creating A Spending PlanDocument4 pagesWe're Here To Help.: Creating A Spending Planf.sistersonNo ratings yet

- The Rajastan Co-Operative BankDocument12 pagesThe Rajastan Co-Operative Bankjini03No ratings yet

- Premier Savings TcsDocument2 pagesPremier Savings TcsCorey BrooksNo ratings yet

- G622CHC Blue Choice Gold PPO 022: This Is Only A SummaryDocument8 pagesG622CHC Blue Choice Gold PPO 022: This Is Only A SummaryAnonymous nx3VC6zHn2No ratings yet

- Ucla Mca Casebook 2009Document42 pagesUcla Mca Casebook 2009benjamin_435293819No ratings yet

- Sumario Every Day BrozeDocument9 pagesSumario Every Day BrozeMiriangely GonzalezNo ratings yet

- A Budget Sheet For FinanceDocument12 pagesA Budget Sheet For Financegraham100% (1)

- Chapter 4 P3Document24 pagesChapter 4 P3Huyền PhạmNo ratings yet

- E-Medical Pass Takaful PDSDocument3 pagesE-Medical Pass Takaful PDSGolden ChainNo ratings yet

- SBC - Cdo - 2019 2Document6 pagesSBC - Cdo - 2019 2Dinko KajtezovićNo ratings yet

- Final Draft Gig Harbor Enrollment Guide 2024Document24 pagesFinal Draft Gig Harbor Enrollment Guide 2024api-307235383No ratings yet

- Co-Pay vs. Deductible What's The DifferenceDocument3 pagesCo-Pay vs. Deductible What's The DifferenceKrîzèllê B. MëndòzâNo ratings yet

- Financial-Accounting-Analysis-Dec 2022Document12 pagesFinancial-Accounting-Analysis-Dec 2022Rameshwar BhatiNo ratings yet

- Important Questions Answers Why This MattersDocument10 pagesImportant Questions Answers Why This MattersJunior GatbuntonNo ratings yet

- Napkin Finance: Build Your Wealth in 30 Seconds or LessFrom EverandNapkin Finance: Build Your Wealth in 30 Seconds or LessRating: 3 out of 5 stars3/5 (3)

- Money for Nothing: How to land the best deals on your insurances, loans, cards, er, tax and moreFrom EverandMoney for Nothing: How to land the best deals on your insurances, loans, cards, er, tax and moreNo ratings yet

- FIN202 - Quiz Test 1Document4 pagesFIN202 - Quiz Test 1Nguyen Phuong Linh (k17 HCM)No ratings yet

- Module 1Document5 pagesModule 1Its Nico & SandyNo ratings yet

- 1234449Document19 pages1234449Jade MarkNo ratings yet

- Far-Pw 5.23Document9 pagesFar-Pw 5.23Miguel ManagoNo ratings yet

- Basic Financial and Accounting Systems ToolkitDocument78 pagesBasic Financial and Accounting Systems ToolkitAhsin KhanNo ratings yet

- November 2016 Reading Between The Lines by Dhiraj Dave Version 1Document22 pagesNovember 2016 Reading Between The Lines by Dhiraj Dave Version 1Abhinav SrivastavaNo ratings yet

- Good Practice Report On Innovative Business Incubators in CroatiaDocument43 pagesGood Practice Report On Innovative Business Incubators in CroatiaNikhil AIC-SRS-NDRINo ratings yet

- Chapter 10: Responsibility Accounting Centralized OrganizationDocument5 pagesChapter 10: Responsibility Accounting Centralized OrganizationLee SuarezNo ratings yet

- Operating Decisions and The Accounting System: Answers To QuestionsDocument64 pagesOperating Decisions and The Accounting System: Answers To Questionsforumuse3bNo ratings yet

- Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionDocument8 pagesIdentify The Letter of The Choice That Best Completes The Statement or Answers The QuestionJhazz DoNo ratings yet

- Assessment TestDocument3 pagesAssessment TestDaniel HunksNo ratings yet

- FABM ActivityDocument3 pagesFABM ActivityRey VillaNo ratings yet

- A Benefit-Sharing Model For Hydropower Projects Based On Stakeholder Input-Output Analysis: A Case Study of The Xiluodu Project in ChinaDocument13 pagesA Benefit-Sharing Model For Hydropower Projects Based On Stakeholder Input-Output Analysis: A Case Study of The Xiluodu Project in ChinaSuraj PantNo ratings yet

- CRD Foods PVT LTDDocument15 pagesCRD Foods PVT LTDsanju kumarNo ratings yet

- Accounting Activity 6Document2 pagesAccounting Activity 6Kae Abegail GarciaNo ratings yet

- 3 March - Group 1Document2 pages3 March - Group 1Lydia limNo ratings yet

- Problem 1:: JournalsDocument11 pagesProblem 1:: JournalsPriyasNo ratings yet

- Receivables 3,936,400 3,320,000: Balance Sheet Items 2018 2017Document4 pagesReceivables 3,936,400 3,320,000: Balance Sheet Items 2018 2017CulitaBogdanNo ratings yet

- Kyla Business PlanDocument27 pagesKyla Business Planbelinda dagohoyNo ratings yet

- Question 2 CashFlowDocument6 pagesQuestion 2 CashFlowsuraj lamaNo ratings yet

- 03 - Handout - Partnership DissolutionDocument4 pages03 - Handout - Partnership DissolutionJanysse CalderonNo ratings yet

- Comparative Income Statement of Star Company For 2016-2018 Star Company Comparative Income Statement December 31, 2016,2017 and 2018Document5 pagesComparative Income Statement of Star Company For 2016-2018 Star Company Comparative Income Statement December 31, 2016,2017 and 2018JonellNo ratings yet

- Business Development and ValueDocument20 pagesBusiness Development and Valueer_hvpatelNo ratings yet

- Chap 014Document27 pagesChap 014kainattariq67% (3)

- Case Study - BCVE and Preacquistion EntriesDocument3 pagesCase Study - BCVE and Preacquistion EntriesHuỳnh Minh Gia HàoNo ratings yet

- Marking SchemeDocument16 pagesMarking SchemeWaqas PirzadaNo ratings yet

- NU - Correction of Errors Single Entry Cash To AccrualDocument8 pagesNU - Correction of Errors Single Entry Cash To AccrualJem ValmonteNo ratings yet

- Armenian National Constitution - EnglishDocument23 pagesArmenian National Constitution - EnglishCem YamanNo ratings yet