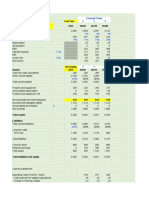

Consolidation Q57

Consolidation Q57

You might also like

- Starbucks Supply ChainDocument22 pagesStarbucks Supply Chainxozab90% (20)

- List of Audit Firms in Dubai, Audit Firms in Dubai, Dubai Auditors, Auditors in UAEDocument6 pagesList of Audit Firms in Dubai, Audit Firms in Dubai, Dubai Auditors, Auditors in UAEImtiaz Javed100% (4)

- December 2006 P4 QuestionDocument11 pagesDecember 2006 P4 QuestionKrishantha WeerasiriNo ratings yet

- Company LAW: Classification of CompaniesDocument1 pageCompany LAW: Classification of Companiessiti nadhirah100% (1)

- AC201 Cash Flow - LLOYDDocument17 pagesAC201 Cash Flow - LLOYDJustice DhliwayoNo ratings yet

- BUSI 2093 Exam Cover Sheet (Set C) : Professor Use OnlyDocument6 pagesBUSI 2093 Exam Cover Sheet (Set C) : Professor Use OnlySimranjeet KaurNo ratings yet

- C.F. Zambeze Q - ADocument5 pagesC.F. Zambeze Q - AthesaqibonlineNo ratings yet

- 11 - Excelfiles - Student Text - Assignments - 2010Document6 pages11 - Excelfiles - Student Text - Assignments - 2010leuleuNo ratings yet

- 11 Excelfiles Student Text Assignments 2010Document6 pages11 Excelfiles Student Text Assignments 2010leuleuNo ratings yet

- Question 2 (30 Marks) : Sales 8000 Cost of Sales (6000)Document4 pagesQuestion 2 (30 Marks) : Sales 8000 Cost of Sales (6000)Chitradevi RamooNo ratings yet

- Cash Flow Explanatory SheetDocument4 pagesCash Flow Explanatory SheetTony DarwishNo ratings yet

- UntitledDocument69 pagesUntitledJonathan OngNo ratings yet

- Consolidation Q55Document8 pagesConsolidation Q55Krishna 11No ratings yet

- Assignment 7 SolutionsDocument10 pagesAssignment 7 SolutionsjoanNo ratings yet

- Consolidated Fi Nancial Statements and Notes To The Consolidated Fi Nancial StatementsDocument5 pagesConsolidated Fi Nancial Statements and Notes To The Consolidated Fi Nancial Statementsria septiani putriNo ratings yet

- TyuhDocument16 pagesTyuhNikhilNo ratings yet

- Emirates Integrated Telecommunications Company PJSC and Its Subsidiaries Consolidated Financial Statements For The Year Ended 31 December 2022Document74 pagesEmirates Integrated Telecommunications Company PJSC and Its Subsidiaries Consolidated Financial Statements For The Year Ended 31 December 2022Vanshita SharmaNo ratings yet

- Kuwait Privatization Projects Holding Co.: Financial Statement - 2006Document21 pagesKuwait Privatization Projects Holding Co.: Financial Statement - 2006phckuwaitNo ratings yet

- NYSE_CIT_1997Document8 pagesNYSE_CIT_1997pcelica77No ratings yet

- Accounts 23rd JanuaryDocument3 pagesAccounts 23rd Januarychali.k.mushibweNo ratings yet

- Statement of Cash Flow - Thorstved CoDocument5 pagesStatement of Cash Flow - Thorstved Cotun ibrahimNo ratings yet

- Consolidated Financial Statements 2023Document69 pagesConsolidated Financial Statements 2023Jordan BorkNo ratings yet

- Laforge Systems, Inc. Balance Sheet (In Millions) Years Ended December 31 2007 2008Document6 pagesLaforge Systems, Inc. Balance Sheet (In Millions) Years Ended December 31 2007 2008Dina WongNo ratings yet

- Consolidated Financial Statements 2022Document64 pagesConsolidated Financial Statements 2022mohaksmartNo ratings yet

- CR Inter QuestionsDocument22 pagesCR Inter QuestionsRichie BoomaNo ratings yet

- Hong Fok Corporation Limited: Revenue (Note 1)Document10 pagesHong Fok Corporation Limited: Revenue (Note 1)Theng RogerNo ratings yet

- 2001 Interim Results Release EngDocument14 pages2001 Interim Results Release EngVikas SinghalNo ratings yet

- 9539 MUH QR 2023-06-30 MUHQ420230630Result 71098896Document15 pages9539 MUH QR 2023-06-30 MUHQ420230630Result 71098896Eugene OngNo ratings yet

- JHM 1Qtr21 Financial Report (Amendment)Document13 pagesJHM 1Qtr21 Financial Report (Amendment)Ooi Gim SengNo ratings yet

- Infineon Annual Report 2021-153-156Document4 pagesInfineon Annual Report 2021-153-156Ddaeng StudiosNo ratings yet

- 7001 Assignment #3Document9 pages7001 Assignment #3南玖No ratings yet

- Careplus Group Berhad: Unaudited Condensed Consolidated Statements of Comprehensive IncomeDocument16 pagesCareplus Group Berhad: Unaudited Condensed Consolidated Statements of Comprehensive IncomethamNo ratings yet

- HKICPA QP Exam (Module A) Sep2008 Question PaperDocument9 pagesHKICPA QP Exam (Module A) Sep2008 Question Papercynthia tsui67% (3)

- Adamjee Consolidated Financial S 2009Document63 pagesAdamjee Consolidated Financial S 2009takingtheflowerNo ratings yet

- Acct 401 Tutorial Set FiveDocument13 pagesAcct 401 Tutorial Set FiveStudy GirlNo ratings yet

- Practice Problems, CH 12Document6 pagesPractice Problems, CH 12scridNo ratings yet

- Company AccountsDocument4 pagesCompany AccountsShlokNo ratings yet

- Ch02 Mini CaseDocument11 pagesCh02 Mini CaseCarl GarrettNo ratings yet

- Хариу HW2 ACC732Document6 pagesХариу HW2 ACC732ZayaNo ratings yet

- 1.cash Flow AnalysisDocument8 pages1.cash Flow AnalysisHoai ThuongNo ratings yet

- Colgate Cash FlowsDocument2 pagesColgate Cash FlowsChetan DhuriNo ratings yet

- Karora FS Q1 2021Document16 pagesKarora FS Q1 2021Predrag MarkovicNo ratings yet

- HomeDepot F22 SolutionDocument4 pagesHomeDepot F22 SolutionFalguni ShomeNo ratings yet

- Plaquette Annuelle 31 Decembre 2021 ENDocument85 pagesPlaquette Annuelle 31 Decembre 2021 ENHari ShankarNo ratings yet

- 2000 Financial Statements enDocument72 pages2000 Financial Statements enEarn8348No ratings yet

- HHB - Announcement - 1Q FY2022 Result - 20210803Document14 pagesHHB - Announcement - 1Q FY2022 Result - 20210803Dennis HaNo ratings yet

- 664998Document2 pages664998Muhammad Saad UmarNo ratings yet

- Chapter 23 An Introduction To The Accounts of Limited Companies Q1 Bracket and Racket Ltd. (A)Document3 pagesChapter 23 An Introduction To The Accounts of Limited Companies Q1 Bracket and Racket Ltd. (A)melody shayanwakoNo ratings yet

- Standard Chartered Bank Ghana PLC: Unaudited Financial Statements For The Period Ended 30 September 2021Document1 pageStandard Chartered Bank Ghana PLC: Unaudited Financial Statements For The Period Ended 30 September 2021Fuaad DodooNo ratings yet

- Accounting IAS (Malaysia) Model Answers Series 2 2005 Old SyllabusDocument20 pagesAccounting IAS (Malaysia) Model Answers Series 2 2005 Old SyllabusAung Zaw HtweNo ratings yet

- Financial Report For The Year 2020-21Document280 pagesFinancial Report For The Year 2020-21Amanuel TewoldeNo ratings yet

- Dic FS Ann e 20 03 2023Document77 pagesDic FS Ann e 20 03 2023MarizeteNo ratings yet

- Five Below 2018 Financial StatementsDocument4 pagesFive Below 2018 Financial StatementsElie GergesNo ratings yet

- 2023AcF100EXAM1JUNEFINAL AccountingandFSADocument11 pages2023AcF100EXAM1JUNEFINAL AccountingandFSAnikoleta demosthenousNo ratings yet

- Kin Pang Holdings Limited 建 鵬 控 股 有 限 公 司: Audited Annual Results Announcement For The Year Ended 31 December 2021Document37 pagesKin Pang Holdings Limited 建 鵬 控 股 有 限 公 司: Audited Annual Results Announcement For The Year Ended 31 December 2021ALNo ratings yet

- Pathfinder MAY 2016 ProfessionalDocument184 pagesPathfinder MAY 2016 ProfessionalALIU HADINo ratings yet

- Practice Exam - SolutionsDocument12 pagesPractice Exam - SolutionsSu Suan TanNo ratings yet

- Midterm Excel Worksheet Olivieri Version 2Document21 pagesMidterm Excel Worksheet Olivieri Version 2Emanuele OlivieriNo ratings yet

- FS BarlettDocument4 pagesFS BarlettmixxNo ratings yet

- Karora Resources FS Q3 2021Document19 pagesKarora Resources FS Q3 2021prenges prengesNo ratings yet

- MR D.I.Y. Group (M) Berhad: Interim Financial Report For The Third Quarter Ended 30 September 2020Document15 pagesMR D.I.Y. Group (M) Berhad: Interim Financial Report For The Third Quarter Ended 30 September 2020Mzm Zahir MzmNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- XdfdhfheDocument2 pagesXdfdhfheKrishna 11No ratings yet

- ZOHO TrainingDocument4 pagesZOHO TrainingKrishna 11No ratings yet

- If Mr. Paul Resided in The UK For ADocument1 pageIf Mr. Paul Resided in The UK For AKrishna 11No ratings yet

- General LedgerDocument3 pagesGeneral LedgerKrishna 11No ratings yet

- Abc FR129Document3 pagesAbc FR129Krishna 11No ratings yet

- Abc FR264Document1 pageAbc FR264Krishna 11No ratings yet

- Analysing Institutional and Government Support ForDocument3 pagesAnalysing Institutional and Government Support ForKrishna 11No ratings yet

- HKICA Train Carbon Audit Dec22 CKDocument6 pagesHKICA Train Carbon Audit Dec22 CKlpdung-duoc13b-vb2No ratings yet

- Ability Course 1 Assignment 2Document15 pagesAbility Course 1 Assignment 2Saurabh TiwariNo ratings yet

- MTR Food: (Mavalli Tiffin Rooms)Document8 pagesMTR Food: (Mavalli Tiffin Rooms)KARTIK BABREKARNo ratings yet

- AGENCY MoUDocument17 pagesAGENCY MoUAbhIshEk BishtNo ratings yet

- Managerial Economics & Business Strategy: Market Forces: Demand and SupplyDocument38 pagesManagerial Economics & Business Strategy: Market Forces: Demand and SupplyRizki WibowoNo ratings yet

- RDPL 2022 - ItDocument15 pagesRDPL 2022 - ItZezen ZeNo ratings yet

- Business Economics Assignment#1Document3 pagesBusiness Economics Assignment#1Ayesha RehmanNo ratings yet

- Industry Economics Market ModelsDocument10 pagesIndustry Economics Market ModelsrosheelNo ratings yet

- Valuation NotesDocument5 pagesValuation NotesVienne MaceNo ratings yet

- OMKAR OPTICALS (ZEISS) - 1346-12 Dec 23Document1 pageOMKAR OPTICALS (ZEISS) - 1346-12 Dec 23akansha16.kumariNo ratings yet

- Meilani Ferdinan PDFDocument11 pagesMeilani Ferdinan PDFhilmyNo ratings yet

- Business Differences in Developing CountriesDocument2 pagesBusiness Differences in Developing CountriesSevinc SalmanovaNo ratings yet

- g3. Facilities Management 2Document16 pagesg3. Facilities Management 2cdaquiz81No ratings yet

- Program GovernanceDocument213 pagesProgram GovernanceUsman A. KalamNo ratings yet

- ACS3063Document11 pagesACS3063Muhamad Asri Bin Yaakub A20A2162No ratings yet

- Food Truck ProjectDocument8 pagesFood Truck Projectapi-634941134No ratings yet

- Mission, Vission & Swot Anaylysis of Standard Chartred BankDocument3 pagesMission, Vission & Swot Anaylysis of Standard Chartred BankFahad Khan TareenNo ratings yet

- DrillsDocument4 pagesDrillsKRISTINA DENISSE SAN JOSENo ratings yet

- DCF PracticeDocument3 pagesDCF PracticeAli ShehrwaniNo ratings yet

- Question 7,8,9,10Document2 pagesQuestion 7,8,9,10Khawar ayubNo ratings yet

- Principles of Marketing Promotions DecisionsDocument15 pagesPrinciples of Marketing Promotions DecisionsMehak guptaNo ratings yet

- Corrigendum 01Document3 pagesCorrigendum 01sagi prathimaNo ratings yet

- Treasury Contact USADocument8 pagesTreasury Contact USAkittukishore35No ratings yet

- CasestudyDocument3 pagesCasestudyKarthik ThippirisettiNo ratings yet

- Question - Certification Exam-NewDocument94 pagesQuestion - Certification Exam-NewvijayNo ratings yet

- Risk-Coverage Risks: Chapter - 9 Insurance ClaimsDocument24 pagesRisk-Coverage Risks: Chapter - 9 Insurance Claimss2sNo ratings yet

- Bernabe Accounting-FirmDocument33 pagesBernabe Accounting-FirmElla Ramos100% (1)

Download as pdf or txt

You might also like

- Starbucks Supply ChainDocument22 pagesStarbucks Supply Chainxozab90% (20)

- List of Audit Firms in Dubai, Audit Firms in Dubai, Dubai Auditors, Auditors in UAEDocument6 pagesList of Audit Firms in Dubai, Audit Firms in Dubai, Dubai Auditors, Auditors in UAEImtiaz Javed100% (4)

- December 2006 P4 QuestionDocument11 pagesDecember 2006 P4 QuestionKrishantha WeerasiriNo ratings yet

- Company LAW: Classification of CompaniesDocument1 pageCompany LAW: Classification of Companiessiti nadhirah100% (1)

- AC201 Cash Flow - LLOYDDocument17 pagesAC201 Cash Flow - LLOYDJustice DhliwayoNo ratings yet

- BUSI 2093 Exam Cover Sheet (Set C) : Professor Use OnlyDocument6 pagesBUSI 2093 Exam Cover Sheet (Set C) : Professor Use OnlySimranjeet KaurNo ratings yet

- C.F. Zambeze Q - ADocument5 pagesC.F. Zambeze Q - AthesaqibonlineNo ratings yet

- 11 - Excelfiles - Student Text - Assignments - 2010Document6 pages11 - Excelfiles - Student Text - Assignments - 2010leuleuNo ratings yet

- 11 Excelfiles Student Text Assignments 2010Document6 pages11 Excelfiles Student Text Assignments 2010leuleuNo ratings yet

- Question 2 (30 Marks) : Sales 8000 Cost of Sales (6000)Document4 pagesQuestion 2 (30 Marks) : Sales 8000 Cost of Sales (6000)Chitradevi RamooNo ratings yet

- Cash Flow Explanatory SheetDocument4 pagesCash Flow Explanatory SheetTony DarwishNo ratings yet

- UntitledDocument69 pagesUntitledJonathan OngNo ratings yet

- Consolidation Q55Document8 pagesConsolidation Q55Krishna 11No ratings yet

- Assignment 7 SolutionsDocument10 pagesAssignment 7 SolutionsjoanNo ratings yet

- Consolidated Fi Nancial Statements and Notes To The Consolidated Fi Nancial StatementsDocument5 pagesConsolidated Fi Nancial Statements and Notes To The Consolidated Fi Nancial Statementsria septiani putriNo ratings yet

- TyuhDocument16 pagesTyuhNikhilNo ratings yet

- Emirates Integrated Telecommunications Company PJSC and Its Subsidiaries Consolidated Financial Statements For The Year Ended 31 December 2022Document74 pagesEmirates Integrated Telecommunications Company PJSC and Its Subsidiaries Consolidated Financial Statements For The Year Ended 31 December 2022Vanshita SharmaNo ratings yet

- Kuwait Privatization Projects Holding Co.: Financial Statement - 2006Document21 pagesKuwait Privatization Projects Holding Co.: Financial Statement - 2006phckuwaitNo ratings yet

- NYSE_CIT_1997Document8 pagesNYSE_CIT_1997pcelica77No ratings yet

- Accounts 23rd JanuaryDocument3 pagesAccounts 23rd Januarychali.k.mushibweNo ratings yet

- Statement of Cash Flow - Thorstved CoDocument5 pagesStatement of Cash Flow - Thorstved Cotun ibrahimNo ratings yet

- Consolidated Financial Statements 2023Document69 pagesConsolidated Financial Statements 2023Jordan BorkNo ratings yet

- Laforge Systems, Inc. Balance Sheet (In Millions) Years Ended December 31 2007 2008Document6 pagesLaforge Systems, Inc. Balance Sheet (In Millions) Years Ended December 31 2007 2008Dina WongNo ratings yet

- Consolidated Financial Statements 2022Document64 pagesConsolidated Financial Statements 2022mohaksmartNo ratings yet

- CR Inter QuestionsDocument22 pagesCR Inter QuestionsRichie BoomaNo ratings yet

- Hong Fok Corporation Limited: Revenue (Note 1)Document10 pagesHong Fok Corporation Limited: Revenue (Note 1)Theng RogerNo ratings yet

- 2001 Interim Results Release EngDocument14 pages2001 Interim Results Release EngVikas SinghalNo ratings yet

- 9539 MUH QR 2023-06-30 MUHQ420230630Result 71098896Document15 pages9539 MUH QR 2023-06-30 MUHQ420230630Result 71098896Eugene OngNo ratings yet

- JHM 1Qtr21 Financial Report (Amendment)Document13 pagesJHM 1Qtr21 Financial Report (Amendment)Ooi Gim SengNo ratings yet

- Infineon Annual Report 2021-153-156Document4 pagesInfineon Annual Report 2021-153-156Ddaeng StudiosNo ratings yet

- 7001 Assignment #3Document9 pages7001 Assignment #3南玖No ratings yet

- Careplus Group Berhad: Unaudited Condensed Consolidated Statements of Comprehensive IncomeDocument16 pagesCareplus Group Berhad: Unaudited Condensed Consolidated Statements of Comprehensive IncomethamNo ratings yet

- HKICPA QP Exam (Module A) Sep2008 Question PaperDocument9 pagesHKICPA QP Exam (Module A) Sep2008 Question Papercynthia tsui67% (3)

- Adamjee Consolidated Financial S 2009Document63 pagesAdamjee Consolidated Financial S 2009takingtheflowerNo ratings yet

- Acct 401 Tutorial Set FiveDocument13 pagesAcct 401 Tutorial Set FiveStudy GirlNo ratings yet

- Practice Problems, CH 12Document6 pagesPractice Problems, CH 12scridNo ratings yet

- Company AccountsDocument4 pagesCompany AccountsShlokNo ratings yet

- Ch02 Mini CaseDocument11 pagesCh02 Mini CaseCarl GarrettNo ratings yet

- Хариу HW2 ACC732Document6 pagesХариу HW2 ACC732ZayaNo ratings yet

- 1.cash Flow AnalysisDocument8 pages1.cash Flow AnalysisHoai ThuongNo ratings yet

- Colgate Cash FlowsDocument2 pagesColgate Cash FlowsChetan DhuriNo ratings yet

- Karora FS Q1 2021Document16 pagesKarora FS Q1 2021Predrag MarkovicNo ratings yet

- HomeDepot F22 SolutionDocument4 pagesHomeDepot F22 SolutionFalguni ShomeNo ratings yet

- Plaquette Annuelle 31 Decembre 2021 ENDocument85 pagesPlaquette Annuelle 31 Decembre 2021 ENHari ShankarNo ratings yet

- 2000 Financial Statements enDocument72 pages2000 Financial Statements enEarn8348No ratings yet

- HHB - Announcement - 1Q FY2022 Result - 20210803Document14 pagesHHB - Announcement - 1Q FY2022 Result - 20210803Dennis HaNo ratings yet

- 664998Document2 pages664998Muhammad Saad UmarNo ratings yet

- Chapter 23 An Introduction To The Accounts of Limited Companies Q1 Bracket and Racket Ltd. (A)Document3 pagesChapter 23 An Introduction To The Accounts of Limited Companies Q1 Bracket and Racket Ltd. (A)melody shayanwakoNo ratings yet

- Standard Chartered Bank Ghana PLC: Unaudited Financial Statements For The Period Ended 30 September 2021Document1 pageStandard Chartered Bank Ghana PLC: Unaudited Financial Statements For The Period Ended 30 September 2021Fuaad DodooNo ratings yet

- Accounting IAS (Malaysia) Model Answers Series 2 2005 Old SyllabusDocument20 pagesAccounting IAS (Malaysia) Model Answers Series 2 2005 Old SyllabusAung Zaw HtweNo ratings yet

- Financial Report For The Year 2020-21Document280 pagesFinancial Report For The Year 2020-21Amanuel TewoldeNo ratings yet

- Dic FS Ann e 20 03 2023Document77 pagesDic FS Ann e 20 03 2023MarizeteNo ratings yet

- Five Below 2018 Financial StatementsDocument4 pagesFive Below 2018 Financial StatementsElie GergesNo ratings yet

- 2023AcF100EXAM1JUNEFINAL AccountingandFSADocument11 pages2023AcF100EXAM1JUNEFINAL AccountingandFSAnikoleta demosthenousNo ratings yet

- Kin Pang Holdings Limited 建 鵬 控 股 有 限 公 司: Audited Annual Results Announcement For The Year Ended 31 December 2021Document37 pagesKin Pang Holdings Limited 建 鵬 控 股 有 限 公 司: Audited Annual Results Announcement For The Year Ended 31 December 2021ALNo ratings yet

- Pathfinder MAY 2016 ProfessionalDocument184 pagesPathfinder MAY 2016 ProfessionalALIU HADINo ratings yet

- Practice Exam - SolutionsDocument12 pagesPractice Exam - SolutionsSu Suan TanNo ratings yet

- Midterm Excel Worksheet Olivieri Version 2Document21 pagesMidterm Excel Worksheet Olivieri Version 2Emanuele OlivieriNo ratings yet

- FS BarlettDocument4 pagesFS BarlettmixxNo ratings yet

- Karora Resources FS Q3 2021Document19 pagesKarora Resources FS Q3 2021prenges prengesNo ratings yet

- MR D.I.Y. Group (M) Berhad: Interim Financial Report For The Third Quarter Ended 30 September 2020Document15 pagesMR D.I.Y. Group (M) Berhad: Interim Financial Report For The Third Quarter Ended 30 September 2020Mzm Zahir MzmNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- XdfdhfheDocument2 pagesXdfdhfheKrishna 11No ratings yet

- ZOHO TrainingDocument4 pagesZOHO TrainingKrishna 11No ratings yet

- If Mr. Paul Resided in The UK For ADocument1 pageIf Mr. Paul Resided in The UK For AKrishna 11No ratings yet

- General LedgerDocument3 pagesGeneral LedgerKrishna 11No ratings yet

- Abc FR129Document3 pagesAbc FR129Krishna 11No ratings yet

- Abc FR264Document1 pageAbc FR264Krishna 11No ratings yet

- Analysing Institutional and Government Support ForDocument3 pagesAnalysing Institutional and Government Support ForKrishna 11No ratings yet

- HKICA Train Carbon Audit Dec22 CKDocument6 pagesHKICA Train Carbon Audit Dec22 CKlpdung-duoc13b-vb2No ratings yet

- Ability Course 1 Assignment 2Document15 pagesAbility Course 1 Assignment 2Saurabh TiwariNo ratings yet

- MTR Food: (Mavalli Tiffin Rooms)Document8 pagesMTR Food: (Mavalli Tiffin Rooms)KARTIK BABREKARNo ratings yet

- AGENCY MoUDocument17 pagesAGENCY MoUAbhIshEk BishtNo ratings yet

- Managerial Economics & Business Strategy: Market Forces: Demand and SupplyDocument38 pagesManagerial Economics & Business Strategy: Market Forces: Demand and SupplyRizki WibowoNo ratings yet

- RDPL 2022 - ItDocument15 pagesRDPL 2022 - ItZezen ZeNo ratings yet

- Business Economics Assignment#1Document3 pagesBusiness Economics Assignment#1Ayesha RehmanNo ratings yet

- Industry Economics Market ModelsDocument10 pagesIndustry Economics Market ModelsrosheelNo ratings yet

- Valuation NotesDocument5 pagesValuation NotesVienne MaceNo ratings yet

- OMKAR OPTICALS (ZEISS) - 1346-12 Dec 23Document1 pageOMKAR OPTICALS (ZEISS) - 1346-12 Dec 23akansha16.kumariNo ratings yet

- Meilani Ferdinan PDFDocument11 pagesMeilani Ferdinan PDFhilmyNo ratings yet

- Business Differences in Developing CountriesDocument2 pagesBusiness Differences in Developing CountriesSevinc SalmanovaNo ratings yet

- g3. Facilities Management 2Document16 pagesg3. Facilities Management 2cdaquiz81No ratings yet

- Program GovernanceDocument213 pagesProgram GovernanceUsman A. KalamNo ratings yet

- ACS3063Document11 pagesACS3063Muhamad Asri Bin Yaakub A20A2162No ratings yet

- Food Truck ProjectDocument8 pagesFood Truck Projectapi-634941134No ratings yet

- Mission, Vission & Swot Anaylysis of Standard Chartred BankDocument3 pagesMission, Vission & Swot Anaylysis of Standard Chartred BankFahad Khan TareenNo ratings yet

- DrillsDocument4 pagesDrillsKRISTINA DENISSE SAN JOSENo ratings yet

- DCF PracticeDocument3 pagesDCF PracticeAli ShehrwaniNo ratings yet

- Question 7,8,9,10Document2 pagesQuestion 7,8,9,10Khawar ayubNo ratings yet

- Principles of Marketing Promotions DecisionsDocument15 pagesPrinciples of Marketing Promotions DecisionsMehak guptaNo ratings yet

- Corrigendum 01Document3 pagesCorrigendum 01sagi prathimaNo ratings yet

- Treasury Contact USADocument8 pagesTreasury Contact USAkittukishore35No ratings yet

- CasestudyDocument3 pagesCasestudyKarthik ThippirisettiNo ratings yet

- Question - Certification Exam-NewDocument94 pagesQuestion - Certification Exam-NewvijayNo ratings yet

- Risk-Coverage Risks: Chapter - 9 Insurance ClaimsDocument24 pagesRisk-Coverage Risks: Chapter - 9 Insurance Claimss2sNo ratings yet

- Bernabe Accounting-FirmDocument33 pagesBernabe Accounting-FirmElla Ramos100% (1)