Chapter 3

Chapter 3

You might also like

- CPLTDDocument11 pagesCPLTDCA Kiran KoshtiNo ratings yet

- Emnace FinMa Activity 2Document2 pagesEmnace FinMa Activity 2CASTOR, Vincent PaulNo ratings yet

- New GL and Classic GLDocument3 pagesNew GL and Classic GLRizky Wahyu100% (1)

- FINANCIAL MARKETS AND INSTITUTIONS - NotesDocument32 pagesFINANCIAL MARKETS AND INSTITUTIONS - NotessreginatoNo ratings yet

- BLACKBOOKDocument72 pagesBLACKBOOKSawant MithilNo ratings yet

- PDF To Document 687Document29 pagesPDF To Document 687karthikmerwade4No ratings yet

- Overview of Indian Financial SystemDocument17 pagesOverview of Indian Financial SystemKIng KumarNo ratings yet

- 1,2. Financial System and Interest Rate 2022-23Document115 pages1,2. Financial System and Interest Rate 2022-23RAUSHAN KUMARNo ratings yet

- P3 RSW 01 - Running A PracticeDocument4 pagesP3 RSW 01 - Running A PracticeZane BevsNo ratings yet

- Features of The Financial System of DevelpoedDocument35 pagesFeatures of The Financial System of DevelpoedChahat PartapNo ratings yet

- Introduction To FinanceDocument6 pagesIntroduction To FinancemiranahumasaNo ratings yet

- Indian Financial System: Prepared by Jinesh A. ShahDocument42 pagesIndian Financial System: Prepared by Jinesh A. ShahSai charan Reddy CHINTHALAPALLINo ratings yet

- Solved Paper FSD-2010Document11 pagesSolved Paper FSD-2010Kiran SoniNo ratings yet

- IFSS Notes 2Document42 pagesIFSS Notes 2sibaram374No ratings yet

- Issue ManagementDocument194 pagesIssue ManagementBubune KofiNo ratings yet

- Legal 2Document19 pagesLegal 2shortsmotivationhubNo ratings yet

- Presentation by Group 2Document23 pagesPresentation by Group 2Hum h banaras keNo ratings yet

- Financial Service Promotional (Strategy Icici Bank)Document51 pagesFinancial Service Promotional (Strategy Icici Bank)goodwynj100% (2)

- MFS IntroDocument18 pagesMFS IntroChirag GoyalNo ratings yet

- SAMPLEDocument2 pagesSAMPLEgibsonamerica16No ratings yet

- About The SubjectDocument9 pagesAbout The SubjectSåif RøçKêrNo ratings yet

- Conceptual FrameworkDocument5 pagesConceptual FrameworkMaica PontillasNo ratings yet

- True HDFCDocument21 pagesTrue HDFC15vsa010169No ratings yet

- BBA FMI Unit 1 - NoDocument31 pagesBBA FMI Unit 1 - NoRuhani AroraNo ratings yet

- Objectives of Credit Rating: Financial Statements CreditworthinessDocument6 pagesObjectives of Credit Rating: Financial Statements CreditworthinessvishNo ratings yet

- Components of IfsDocument4 pagesComponents of IfsEzhilarasan PerumalNo ratings yet

- MFS NotesDocument139 pagesMFS NotesSHANAT BENNYNo ratings yet

- SAM-5 Marketing of Financial ServicesDocument13 pagesSAM-5 Marketing of Financial Serviceskartik singhNo ratings yet

- WegagenDocument63 pagesWegagenYonas100% (1)

- Hide 1 Financial Controls and Monitoring 2 Financial Services 3 See Also 4 References EditDocument21 pagesHide 1 Financial Controls and Monitoring 2 Financial Services 3 See Also 4 References EditPankaj GautamNo ratings yet

- Acc 906Document40 pagesAcc 906jonathanephraim1No ratings yet

- 10 - Chapter 1 PDFDocument34 pages10 - Chapter 1 PDFRitesh RamanNo ratings yet

- Definition of Financial ServicesDocument25 pagesDefinition of Financial ServicesShailesh SoniNo ratings yet

- Draft 444Document1 pageDraft 444tiegomotswediNo ratings yet

- Financial Services and Merchant BankingDocument54 pagesFinancial Services and Merchant Bankingananya_nagrajNo ratings yet

- Fims Unit - 1Document17 pagesFims Unit - 1arjunmba119624No ratings yet

- Financial Intitutions and MarketsDocument92 pagesFinancial Intitutions and MarketsBalaji KannanNo ratings yet

- Disha Agarwal (1) Financial Services BNFDocument20 pagesDisha Agarwal (1) Financial Services BNFdisha agarwalNo ratings yet

- Role of Managerial Finance and Financial Market and InstitutionsDocument4 pagesRole of Managerial Finance and Financial Market and InstitutionsNimra AhmedNo ratings yet

- IndirectDocument4 pagesIndirectPayal KaraiyaNo ratings yet

- Management of Financial InstitutionsDocument34 pagesManagement of Financial InstitutionsLilian MuthoniNo ratings yet

- UP34Document2 pagesUP34Khushal GargNo ratings yet

- Financial CompanyDocument5 pagesFinancial Company050610220838No ratings yet

- Module IDocument36 pagesModule IKrishna GuptaNo ratings yet

- Indian Financial SystemDocument24 pagesIndian Financial SystemParth GuptaNo ratings yet

- FinanceDocument11 pagesFinanceshivanipandey2224No ratings yet

- Black Book ShubhamDocument82 pagesBlack Book ShubhamShubham GaikarNo ratings yet

- Corporate Financial ReportingPPT 2003Document14 pagesCorporate Financial ReportingPPT 2003ashish3009No ratings yet

- CH 1 FIIMDocument28 pagesCH 1 FIIMMulata KahsayNo ratings yet

- The Fascinating World of FinanceDocument2 pagesThe Fascinating World of FinanceHendrik_216No ratings yet

- Components of IFS NotesDocument6 pagesComponents of IFS NotesPrasad IngoleNo ratings yet

- A Project Report ON "Asset Liability Management in Banks": Submitted ToDocument19 pagesA Project Report ON "Asset Liability Management in Banks": Submitted ToMahesh KhebadeNo ratings yet

- UP3Document1 pageUP3Khushal GargNo ratings yet

- Corporate BankerDocument3 pagesCorporate Bankerishitgadia04No ratings yet

- Indian Financial SystemDocument4 pagesIndian Financial SystemLbsim-akash100% (2)

- From-Nikunjkumar Sanghavi ROLL NO.140 Sybba C'Document18 pagesFrom-Nikunjkumar Sanghavi ROLL NO.140 Sybba C'Nik SanghviNo ratings yet

- Financial ServicesDocument392 pagesFinancial ServicesCLAUDINE MUGABEKAZINo ratings yet

- 205 Finance Market & Banking OperationsDocument10 pages205 Finance Market & Banking Operationsxonline022No ratings yet

- Chapter One and Three Introduction To Financial System and FinancialDocument132 pagesChapter One and Three Introduction To Financial System and FinancialAbdiNo ratings yet

- Business Finance: I. Regulators of Financial MarketsDocument6 pagesBusiness Finance: I. Regulators of Financial Marketscristine aguilarNo ratings yet

- Kami Export - MFS (Unit 1-4) Combine NotesDocument81 pagesKami Export - MFS (Unit 1-4) Combine Notesamangt9988No ratings yet

- Financial Literacy for Entrepreneurs: Understanding the Numbers Behind Your BusinessFrom EverandFinancial Literacy for Entrepreneurs: Understanding the Numbers Behind Your BusinessNo ratings yet

- Stifel ComplaintDocument47 pagesStifel ComplaintZerohedgeNo ratings yet

- Consumer ArithmeticDocument40 pagesConsumer ArithmeticShannon SmithNo ratings yet

- AbhinavDocument3 pagesAbhinavpraveen kumarNo ratings yet

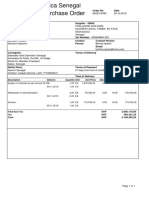

- Description Delivery Quantity Unit Unit Price Disc% Tax% AmountDocument2 pagesDescription Delivery Quantity Unit Unit Price Disc% Tax% AmountAbdou DIENGNo ratings yet

- DMAIC Approach To Improving PRDocument69 pagesDMAIC Approach To Improving PRVen LagunayNo ratings yet

- Powerpoint PresentationDocument9 pagesPowerpoint PresentationempirechocoNo ratings yet

- Unit I: Introduction: 6 Business Level Strategic Planning: Porter FourDocument2 pagesUnit I: Introduction: 6 Business Level Strategic Planning: Porter FourPriyank GangwalNo ratings yet

- Topic: Adjusting Entries / Adjustments Compiled By: Sir Ghalib HussainDocument8 pagesTopic: Adjusting Entries / Adjustments Compiled By: Sir Ghalib HussainGhalib HussainNo ratings yet

- Atma-Automotive Tyre MfrsDocument3 pagesAtma-Automotive Tyre MfrsjayveeNo ratings yet

- Labor Law Unfair Labor PracticeDocument10 pagesLabor Law Unfair Labor PracticeHaven GarciaNo ratings yet

- Comm Planning ProcessDocument6 pagesComm Planning ProcessTracy Sherwin ZothnerNo ratings yet

- E-Commerce Solved MCQs (Set-5)Document6 pagesE-Commerce Solved MCQs (Set-5)Shailendra SinghNo ratings yet

- Quiz AuditingDocument11 pagesQuiz Auditingmaria avia kimNo ratings yet

- Statement XXXXXX0676 2023 08 15Document6 pagesStatement XXXXXX0676 2023 08 15garrettloehrNo ratings yet

- Quiz 1 3 CfasDocument15 pagesQuiz 1 3 CfasDan Edriel RonabioNo ratings yet

- Secretarial Audit and Auditors' ReportDocument11 pagesSecretarial Audit and Auditors' ReportGulbaz KhanNo ratings yet

- AISA Afghanistan - A Comperhensive Study of The Organization Structure and FunctioningDocument50 pagesAISA Afghanistan - A Comperhensive Study of The Organization Structure and FunctioningDelawar BarekzaiNo ratings yet

- Performance ToolsDocument4 pagesPerformance ToolsT YungNo ratings yet

- Import of Rough, Cut and Polished DiamondsDocument2 pagesImport of Rough, Cut and Polished Diamondsanon_575460230No ratings yet

- Manoj Verma 0620Document2 pagesManoj Verma 0620Jaiswal ManojNo ratings yet

- Bit Continent: Project Presentation MaterialsDocument31 pagesBit Continent: Project Presentation MaterialsAnonymous DpzpvMLubNo ratings yet

- Anx 3429Document3 pagesAnx 3429subair achathNo ratings yet

- Major Project BBA 6th SemesterDocument51 pagesMajor Project BBA 6th SemesterGungun KumariNo ratings yet

- Ed Cia 3Document9 pagesEd Cia 3Sanchit MaitraNo ratings yet

- Bhel SipDocument60 pagesBhel SipKhalid HussainNo ratings yet

- Tri 4 Time TableDocument1 pageTri 4 Time TableRaja Babu SharmaNo ratings yet

- IQA Checklist - SmpleDocument16 pagesIQA Checklist - SmpleHarits As Siddiq100% (1)

Download as pdf or txt

You might also like

- CPLTDDocument11 pagesCPLTDCA Kiran KoshtiNo ratings yet

- Emnace FinMa Activity 2Document2 pagesEmnace FinMa Activity 2CASTOR, Vincent PaulNo ratings yet

- New GL and Classic GLDocument3 pagesNew GL and Classic GLRizky Wahyu100% (1)

- FINANCIAL MARKETS AND INSTITUTIONS - NotesDocument32 pagesFINANCIAL MARKETS AND INSTITUTIONS - NotessreginatoNo ratings yet

- BLACKBOOKDocument72 pagesBLACKBOOKSawant MithilNo ratings yet

- PDF To Document 687Document29 pagesPDF To Document 687karthikmerwade4No ratings yet

- Overview of Indian Financial SystemDocument17 pagesOverview of Indian Financial SystemKIng KumarNo ratings yet

- 1,2. Financial System and Interest Rate 2022-23Document115 pages1,2. Financial System and Interest Rate 2022-23RAUSHAN KUMARNo ratings yet

- P3 RSW 01 - Running A PracticeDocument4 pagesP3 RSW 01 - Running A PracticeZane BevsNo ratings yet

- Features of The Financial System of DevelpoedDocument35 pagesFeatures of The Financial System of DevelpoedChahat PartapNo ratings yet

- Introduction To FinanceDocument6 pagesIntroduction To FinancemiranahumasaNo ratings yet

- Indian Financial System: Prepared by Jinesh A. ShahDocument42 pagesIndian Financial System: Prepared by Jinesh A. ShahSai charan Reddy CHINTHALAPALLINo ratings yet

- Solved Paper FSD-2010Document11 pagesSolved Paper FSD-2010Kiran SoniNo ratings yet

- IFSS Notes 2Document42 pagesIFSS Notes 2sibaram374No ratings yet

- Issue ManagementDocument194 pagesIssue ManagementBubune KofiNo ratings yet

- Legal 2Document19 pagesLegal 2shortsmotivationhubNo ratings yet

- Presentation by Group 2Document23 pagesPresentation by Group 2Hum h banaras keNo ratings yet

- Financial Service Promotional (Strategy Icici Bank)Document51 pagesFinancial Service Promotional (Strategy Icici Bank)goodwynj100% (2)

- MFS IntroDocument18 pagesMFS IntroChirag GoyalNo ratings yet

- SAMPLEDocument2 pagesSAMPLEgibsonamerica16No ratings yet

- About The SubjectDocument9 pagesAbout The SubjectSåif RøçKêrNo ratings yet

- Conceptual FrameworkDocument5 pagesConceptual FrameworkMaica PontillasNo ratings yet

- True HDFCDocument21 pagesTrue HDFC15vsa010169No ratings yet

- BBA FMI Unit 1 - NoDocument31 pagesBBA FMI Unit 1 - NoRuhani AroraNo ratings yet

- Objectives of Credit Rating: Financial Statements CreditworthinessDocument6 pagesObjectives of Credit Rating: Financial Statements CreditworthinessvishNo ratings yet

- Components of IfsDocument4 pagesComponents of IfsEzhilarasan PerumalNo ratings yet

- MFS NotesDocument139 pagesMFS NotesSHANAT BENNYNo ratings yet

- SAM-5 Marketing of Financial ServicesDocument13 pagesSAM-5 Marketing of Financial Serviceskartik singhNo ratings yet

- WegagenDocument63 pagesWegagenYonas100% (1)

- Hide 1 Financial Controls and Monitoring 2 Financial Services 3 See Also 4 References EditDocument21 pagesHide 1 Financial Controls and Monitoring 2 Financial Services 3 See Also 4 References EditPankaj GautamNo ratings yet

- Acc 906Document40 pagesAcc 906jonathanephraim1No ratings yet

- 10 - Chapter 1 PDFDocument34 pages10 - Chapter 1 PDFRitesh RamanNo ratings yet

- Definition of Financial ServicesDocument25 pagesDefinition of Financial ServicesShailesh SoniNo ratings yet

- Draft 444Document1 pageDraft 444tiegomotswediNo ratings yet

- Financial Services and Merchant BankingDocument54 pagesFinancial Services and Merchant Bankingananya_nagrajNo ratings yet

- Fims Unit - 1Document17 pagesFims Unit - 1arjunmba119624No ratings yet

- Financial Intitutions and MarketsDocument92 pagesFinancial Intitutions and MarketsBalaji KannanNo ratings yet

- Disha Agarwal (1) Financial Services BNFDocument20 pagesDisha Agarwal (1) Financial Services BNFdisha agarwalNo ratings yet

- Role of Managerial Finance and Financial Market and InstitutionsDocument4 pagesRole of Managerial Finance and Financial Market and InstitutionsNimra AhmedNo ratings yet

- IndirectDocument4 pagesIndirectPayal KaraiyaNo ratings yet

- Management of Financial InstitutionsDocument34 pagesManagement of Financial InstitutionsLilian MuthoniNo ratings yet

- UP34Document2 pagesUP34Khushal GargNo ratings yet

- Financial CompanyDocument5 pagesFinancial Company050610220838No ratings yet

- Module IDocument36 pagesModule IKrishna GuptaNo ratings yet

- Indian Financial SystemDocument24 pagesIndian Financial SystemParth GuptaNo ratings yet

- FinanceDocument11 pagesFinanceshivanipandey2224No ratings yet

- Black Book ShubhamDocument82 pagesBlack Book ShubhamShubham GaikarNo ratings yet

- Corporate Financial ReportingPPT 2003Document14 pagesCorporate Financial ReportingPPT 2003ashish3009No ratings yet

- CH 1 FIIMDocument28 pagesCH 1 FIIMMulata KahsayNo ratings yet

- The Fascinating World of FinanceDocument2 pagesThe Fascinating World of FinanceHendrik_216No ratings yet

- Components of IFS NotesDocument6 pagesComponents of IFS NotesPrasad IngoleNo ratings yet

- A Project Report ON "Asset Liability Management in Banks": Submitted ToDocument19 pagesA Project Report ON "Asset Liability Management in Banks": Submitted ToMahesh KhebadeNo ratings yet

- UP3Document1 pageUP3Khushal GargNo ratings yet

- Corporate BankerDocument3 pagesCorporate Bankerishitgadia04No ratings yet

- Indian Financial SystemDocument4 pagesIndian Financial SystemLbsim-akash100% (2)

- From-Nikunjkumar Sanghavi ROLL NO.140 Sybba C'Document18 pagesFrom-Nikunjkumar Sanghavi ROLL NO.140 Sybba C'Nik SanghviNo ratings yet

- Financial ServicesDocument392 pagesFinancial ServicesCLAUDINE MUGABEKAZINo ratings yet

- 205 Finance Market & Banking OperationsDocument10 pages205 Finance Market & Banking Operationsxonline022No ratings yet

- Chapter One and Three Introduction To Financial System and FinancialDocument132 pagesChapter One and Three Introduction To Financial System and FinancialAbdiNo ratings yet

- Business Finance: I. Regulators of Financial MarketsDocument6 pagesBusiness Finance: I. Regulators of Financial Marketscristine aguilarNo ratings yet

- Kami Export - MFS (Unit 1-4) Combine NotesDocument81 pagesKami Export - MFS (Unit 1-4) Combine Notesamangt9988No ratings yet

- Financial Literacy for Entrepreneurs: Understanding the Numbers Behind Your BusinessFrom EverandFinancial Literacy for Entrepreneurs: Understanding the Numbers Behind Your BusinessNo ratings yet

- Stifel ComplaintDocument47 pagesStifel ComplaintZerohedgeNo ratings yet

- Consumer ArithmeticDocument40 pagesConsumer ArithmeticShannon SmithNo ratings yet

- AbhinavDocument3 pagesAbhinavpraveen kumarNo ratings yet

- Description Delivery Quantity Unit Unit Price Disc% Tax% AmountDocument2 pagesDescription Delivery Quantity Unit Unit Price Disc% Tax% AmountAbdou DIENGNo ratings yet

- DMAIC Approach To Improving PRDocument69 pagesDMAIC Approach To Improving PRVen LagunayNo ratings yet

- Powerpoint PresentationDocument9 pagesPowerpoint PresentationempirechocoNo ratings yet

- Unit I: Introduction: 6 Business Level Strategic Planning: Porter FourDocument2 pagesUnit I: Introduction: 6 Business Level Strategic Planning: Porter FourPriyank GangwalNo ratings yet

- Topic: Adjusting Entries / Adjustments Compiled By: Sir Ghalib HussainDocument8 pagesTopic: Adjusting Entries / Adjustments Compiled By: Sir Ghalib HussainGhalib HussainNo ratings yet

- Atma-Automotive Tyre MfrsDocument3 pagesAtma-Automotive Tyre MfrsjayveeNo ratings yet

- Labor Law Unfair Labor PracticeDocument10 pagesLabor Law Unfair Labor PracticeHaven GarciaNo ratings yet

- Comm Planning ProcessDocument6 pagesComm Planning ProcessTracy Sherwin ZothnerNo ratings yet

- E-Commerce Solved MCQs (Set-5)Document6 pagesE-Commerce Solved MCQs (Set-5)Shailendra SinghNo ratings yet

- Quiz AuditingDocument11 pagesQuiz Auditingmaria avia kimNo ratings yet

- Statement XXXXXX0676 2023 08 15Document6 pagesStatement XXXXXX0676 2023 08 15garrettloehrNo ratings yet

- Quiz 1 3 CfasDocument15 pagesQuiz 1 3 CfasDan Edriel RonabioNo ratings yet

- Secretarial Audit and Auditors' ReportDocument11 pagesSecretarial Audit and Auditors' ReportGulbaz KhanNo ratings yet

- AISA Afghanistan - A Comperhensive Study of The Organization Structure and FunctioningDocument50 pagesAISA Afghanistan - A Comperhensive Study of The Organization Structure and FunctioningDelawar BarekzaiNo ratings yet

- Performance ToolsDocument4 pagesPerformance ToolsT YungNo ratings yet

- Import of Rough, Cut and Polished DiamondsDocument2 pagesImport of Rough, Cut and Polished Diamondsanon_575460230No ratings yet

- Manoj Verma 0620Document2 pagesManoj Verma 0620Jaiswal ManojNo ratings yet

- Bit Continent: Project Presentation MaterialsDocument31 pagesBit Continent: Project Presentation MaterialsAnonymous DpzpvMLubNo ratings yet

- Anx 3429Document3 pagesAnx 3429subair achathNo ratings yet

- Major Project BBA 6th SemesterDocument51 pagesMajor Project BBA 6th SemesterGungun KumariNo ratings yet

- Ed Cia 3Document9 pagesEd Cia 3Sanchit MaitraNo ratings yet

- Bhel SipDocument60 pagesBhel SipKhalid HussainNo ratings yet

- Tri 4 Time TableDocument1 pageTri 4 Time TableRaja Babu SharmaNo ratings yet

- IQA Checklist - SmpleDocument16 pagesIQA Checklist - SmpleHarits As Siddiq100% (1)