Download as pdf or txt

You might also like

- Principles of Insurance Law with Case StudiesFrom EverandPrinciples of Insurance Law with Case StudiesRating: 5 out of 5 stars5/5 (1)

- Theranos 421 Motion To Compel PDFDocument85 pagesTheranos 421 Motion To Compel PDFkalookallayNo ratings yet

- Sample Nuisance ComplaintDocument45 pagesSample Nuisance ComplaintSan Deep100% (3)

- Remedies OutlineDocument11 pagesRemedies OutlineRonnie Barcena Jr.100% (3)

- Rescission of Insurance ContractsDocument4 pagesRescission of Insurance ContractsKharol EdeaNo ratings yet

- 02 Midterm - CodalDocument3 pages02 Midterm - Codalezmailer75No ratings yet

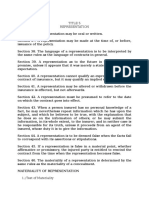

- Title 5 RepresentationDocument4 pagesTitle 5 RepresentationMakoy MolinaNo ratings yet

- WarrantiesDocument2 pagesWarrantiesBiboy GSNo ratings yet

- Business, Within The Meaning of This Code, Shall IncludeDocument20 pagesBusiness, Within The Meaning of This Code, Shall Includeraechelle bulosNo ratings yet

- Insurance ProvisionsDocument16 pagesInsurance ProvisionsCris GondaNo ratings yet

- WarrantiesDocument19 pagesWarrantiesowenNo ratings yet

- Part Three - InsuranceDocument4 pagesPart Three - InsuranceIreneLeahC.RomeroNo ratings yet

- Ingredients or Principles of Insurance LawDocument4 pagesIngredients or Principles of Insurance Lawshakti ranjan mohantyNo ratings yet

- Insurance Final Exam NotesDocument5 pagesInsurance Final Exam NotesJaymee Andomang Os-agNo ratings yet

- Insurance Finals ReviewerDocument15 pagesInsurance Finals ReviewerAmanda LoveNo ratings yet

- What Is Representation?Document5 pagesWhat Is Representation?frankieNo ratings yet

- Reviewer in Insurance Law (VIII-IX)Document12 pagesReviewer in Insurance Law (VIII-IX)Guiller C. MagsumbolNo ratings yet

- Commercial Law Notes April 2Document29 pagesCommercial Law Notes April 2Barnz ShpNo ratings yet

- Insurance CodeDocument15 pagesInsurance CodeOw WawieNo ratings yet

- Concealment NotesDocument5 pagesConcealment NotesSZNo ratings yet

- Double InsuranceDocument9 pagesDouble InsuranceElmer SarabiaNo ratings yet

- Insurance 1Document42 pagesInsurance 1markbulloNo ratings yet

- Insurance Code: 7. Personal - Each Party Having in ViewDocument26 pagesInsurance Code: 7. Personal - Each Party Having in ViewAlberto NicholsNo ratings yet

- Sections 26-66Document5 pagesSections 26-66LandAsia Butuan RealtyNo ratings yet

- Insurance Cod AlDocument3 pagesInsurance Cod AlShine BillonesNo ratings yet

- Commercial Law 2021Document385 pagesCommercial Law 2021Roberto Galano Jr.0% (1)

- Codal Provisions For Insurance (Philippines)Document23 pagesCodal Provisions For Insurance (Philippines)Camille AngelicaNo ratings yet

- INSURANCE - NotesDocument18 pagesINSURANCE - NotesJulienne Aristoza100% (1)

- InsuranceDocument115 pagesInsuranceChris InocencioNo ratings yet

- Finals - Insurance NotesDocument22 pagesFinals - Insurance NotesBlaise VENo ratings yet

- Pointers in Insurance Law PDFDocument5 pagesPointers in Insurance Law PDFMaria Diory RabajanteNo ratings yet

- Law 3 Act No. 2427 Insurance CodeDocument33 pagesLaw 3 Act No. 2427 Insurance CodeNylinad Etnerfacir ObmilNo ratings yet

- 16 50 InsuranceDocument25 pages16 50 InsuranceMartha IlaganNo ratings yet

- Insurance Code RevDocument13 pagesInsurance Code RevPaterno S. Brotamonte Jr.No ratings yet

- Insurance Finals (Atty. Soleng)Document6 pagesInsurance Finals (Atty. Soleng)Bar GRazNo ratings yet

- Insurance CodeDocument18 pagesInsurance CodeKenneth Holasca100% (1)

- Petitioner vs. vs. Respondents: First DivisionDocument10 pagesPetitioner vs. vs. Respondents: First DivisionAggy AlbotraNo ratings yet

- Insurance Code of The PhilippinesDocument37 pagesInsurance Code of The PhilippinesAMIDA ISMAEL. SALISANo ratings yet

- Geagonia vs. CA (February 6, 1995)Document12 pagesGeagonia vs. CA (February 6, 1995)Reina Anne JaymeNo ratings yet

- An Act Revising The Insurance Laws and Regulating Insurance Business in The Philippine IslandsDocument44 pagesAn Act Revising The Insurance Laws and Regulating Insurance Business in The Philippine IslandsjoebzNo ratings yet

- Ra 10607Document15 pagesRa 10607mblopez1100% (1)

- Insurance Reviewer Midterm ExamsDocument9 pagesInsurance Reviewer Midterm ExamsSantoy CartallaNo ratings yet

- Insurance ReviewerDocument16 pagesInsurance Reviewermanol_salaNo ratings yet

- Summary of Insurance MidtermsDocument91 pagesSummary of Insurance MidtermsMarichu Castillo HernandezNo ratings yet

- Insurance NotesDocument30 pagesInsurance NotesAliyah SandersNo ratings yet

- Insurance Rev SyllabusxDocument50 pagesInsurance Rev SyllabusxPanzer OverlordNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument9 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledAnonymous lvUVwZMNo ratings yet

- PlayDocument6 pagesPlaylance zoletaNo ratings yet

- THE Insurance Code of The Philippines (Pres. Decree No. 1460, As Amended.) General ProvisionsDocument13 pagesTHE Insurance Code of The Philippines (Pres. Decree No. 1460, As Amended.) General ProvisionsDonna TreceñeNo ratings yet

- Codal - INSURANCE-MX ReviewerDocument7 pagesCodal - INSURANCE-MX ReviewerElmer SarabiaNo ratings yet

- Upload 1.4Document5 pagesUpload 1.4DAVID JEROMENo ratings yet

- Insurance Reviewer Atty GapuzDocument6 pagesInsurance Reviewer Atty GapuzJohn Soap Reznov MacTavishNo ratings yet

- Presidential Decree No. 612: Business", Within The Meaning of This Code, Shall IncludeDocument21 pagesPresidential Decree No. 612: Business", Within The Meaning of This Code, Shall IncludeRowan O'mearaNo ratings yet

- Armando Geagonia vs. Court of Appeals & Country Bankers Insurance Corp.Document8 pagesArmando Geagonia vs. Court of Appeals & Country Bankers Insurance Corp.talla aldoverNo ratings yet

- Insurance NotesDocument31 pagesInsurance NotesKevin SalazarNo ratings yet

- 0 CHARACTERISTICS OF AN INSURANCE CONTRACT (The Insurance Code of The Philippines AnnotatedDocument48 pages0 CHARACTERISTICS OF AN INSURANCE CONTRACT (The Insurance Code of The Philippines AnnotatedAlarm GuardiansNo ratings yet

- Insurance Sections 25 44Document30 pagesInsurance Sections 25 44raymund lumantaoNo ratings yet

- Petitioner vs. vs. Respondents: First DivisionDocument11 pagesPetitioner vs. vs. Respondents: First DivisionmichelledugsNo ratings yet

- Insurance Memoaid 1Document42 pagesInsurance Memoaid 1washburnx20No ratings yet

- Life, Accident and Health Insurance in the United StatesFrom EverandLife, Accident and Health Insurance in the United StatesRating: 5 out of 5 stars5/5 (1)

- Understanding Named, Automatic and Additional Insureds in the CGL PolicyFrom EverandUnderstanding Named, Automatic and Additional Insureds in the CGL PolicyNo ratings yet

- The Basic Structure of Financial MarketsDocument10 pagesThe Basic Structure of Financial Markets202220012No ratings yet

- No. FMDocument1 pageNo. FM202220012No ratings yet

- Letter For Class SuspensionDocument1 pageLetter For Class Suspension202220012No ratings yet

- SBA 7 EssentialsDocument2 pagesSBA 7 Essentials202220012No ratings yet

- CalPERS LTC LawsuitDocument28 pagesCalPERS LTC Lawsuitjon_ortizNo ratings yet

- Prospectus and Allotment of SecuritiesDocument39 pagesProspectus and Allotment of SecuritiesLogesh JanagarajNo ratings yet

- Zarah NotesDocument31 pagesZarah NotesYieMaghirangNo ratings yet

- 131 General Lnsurance V NG Hua Double InsuranceDocument2 pages131 General Lnsurance V NG Hua Double InsuranceJovelan V. Escaño0% (1)

- Example of A Valid Auto-Contract: If The Agent Has Been Empowered To Borrow Money, He May Himself Be The Lender atDocument9 pagesExample of A Valid Auto-Contract: If The Agent Has Been Empowered To Borrow Money, He May Himself Be The Lender atDwight BlezaNo ratings yet

- Falcon v. Saint-Veltri, 10th Cir. (2001)Document7 pagesFalcon v. Saint-Veltri, 10th Cir. (2001)Scribd Government DocsNo ratings yet

- 5 Cases Digested For FinalsDocument6 pages5 Cases Digested For FinalsDis CatNo ratings yet

- Chi Kit Co LTD V Lucky Health International Enterprise LTD (2000) 3 HKCFAR 268Document20 pagesChi Kit Co LTD V Lucky Health International Enterprise LTD (2000) 3 HKCFAR 268Adrian Chan ACNo ratings yet

- Si Paper 18 Aug Shift 2 Paper 2Document15 pagesSi Paper 18 Aug Shift 2 Paper 2jattNo ratings yet

- Mytest For Smyth: The Law and Business Administrations, Thirteenth Edition Chapter 4: Professional Liability: The Legal ChallengesDocument22 pagesMytest For Smyth: The Law and Business Administrations, Thirteenth Edition Chapter 4: Professional Liability: The Legal ChallengesCalvinNo ratings yet

- Sun Life of Canada Phils. Inc. vs. Sibya GR No. 211212 June 8 2016Document4 pagesSun Life of Canada Phils. Inc. vs. Sibya GR No. 211212 June 8 2016wenny capplemanNo ratings yet

- RAMON P. JACINTO and JAIME J. COLAYCO, Petitioners, vs. FIRST WOMENS CREDIT CORPORATION, Represented in This Derivative Suit by SHIG KATAYAMA, RespondentsDocument6 pagesRAMON P. JACINTO and JAIME J. COLAYCO, Petitioners, vs. FIRST WOMENS CREDIT CORPORATION, Represented in This Derivative Suit by SHIG KATAYAMA, RespondentsVic Cajurao0% (1)

- Marketing Communications Ethics in Marketing CommunicationsDocument5 pagesMarketing Communications Ethics in Marketing CommunicationsTonderai ChamahuruNo ratings yet

- Accountancy Review Center (ARC) of The Philippines IncDocument8 pagesAccountancy Review Center (ARC) of The Philippines IncLouiseNo ratings yet

- Voidable Contracts NurliDocument38 pagesVoidable Contracts NurlihaziqqNo ratings yet

- Application Form For Certificate of ExclusionDocument2 pagesApplication Form For Certificate of ExclusionJohann Benedict BorromeoNo ratings yet

- Utmost Good Faith in Insurance ContractsDocument5 pagesUtmost Good Faith in Insurance Contractscarolsaviapeters100% (1)

- SovCit Pseudo-Legal Document From Heather Ann Tucci-Jarraf's TrialDocument6 pagesSovCit Pseudo-Legal Document From Heather Ann Tucci-Jarraf's TrialJohn P CapitalistNo ratings yet

- DOLE - ESPRD-AEP-FORM-Revised-Application-FormDocument2 pagesDOLE - ESPRD-AEP-FORM-Revised-Application-FormSecretary JoyNo ratings yet

- Ca Foundation Indian Contract Act PDFDocument33 pagesCa Foundation Indian Contract Act PDFAshutosh PaithankarNo ratings yet

- Tang Vs CADocument2 pagesTang Vs CAAnonymous 5MiN6I78I0No ratings yet

- 2022 ALF LMT Commercial LawDocument38 pages2022 ALF LMT Commercial LawDianalyn QuitebesNo ratings yet

- Business Law RajDocument10 pagesBusiness Law RajHesanRajaraniNo ratings yet

- Insurance Code". Commissioner". Chanrobles Virtual LawDocument9 pagesInsurance Code". Commissioner". Chanrobles Virtual LawDairen CanlasNo ratings yet

- Restatement (Second) of ContractsDocument20 pagesRestatement (Second) of ContractsJorgeNo ratings yet

- Unit 2 Study MaterialDocument23 pagesUnit 2 Study MaterialPoorna PrakashNo ratings yet

- FHFA V Banks Attachment 1Document308 pagesFHFA V Banks Attachment 1ny1davidNo ratings yet