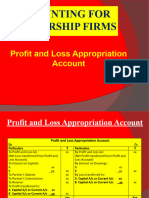

CH-01 Fundamenats

CH-01 Fundamenats

You might also like

- FinAccUnit 3 - Partnership Accounts Lecture Notes PDFDocument8 pagesFinAccUnit 3 - Partnership Accounts Lecture Notes PDFSherona Reid100% (5)

- Affidavit of Loss Policy FORMATDocument1 pageAffidavit of Loss Policy FORMATJC Ardiente100% (2)

- SA Constitution Advantages and DisadvantagesDocument2 pagesSA Constitution Advantages and DisadvantagesPravind KumarNo ratings yet

- 1 - Accounting For Partnership Firms - FundamentalsDocument12 pages1 - Accounting For Partnership Firms - FundamentalsAnkit Roy100% (1)

- Chapter 1 - Formation of PartnershipDocument31 pagesChapter 1 - Formation of PartnershipAisyah Basir33% (3)

- Harry & Meghan V Doe Stipulated InjunctionDocument5 pagesHarry & Meghan V Doe Stipulated InjunctionTHROnline100% (1)

- CH - 2 Accounting For Partnership Firms: Fundamentals: According To Section 4 of The Partnership Act 1932Document12 pagesCH - 2 Accounting For Partnership Firms: Fundamentals: According To Section 4 of The Partnership Act 1932Laksh KhannaNo ratings yet

- Buku Nota PertnershipDocument33 pagesBuku Nota PertnershipmaiNo ratings yet

- Final Account 2020Document30 pagesFinal Account 2020Viransh Coaching ClassesNo ratings yet

- C-1 (Fundamentals of Partnership)Document6 pagesC-1 (Fundamentals of Partnership)adwitanegi068No ratings yet

- Chapter 7: PARTNERSHIPDocument45 pagesChapter 7: PARTNERSHIPSuresh LamsalNo ratings yet

- Chapter 2 - Normal PartnershipDocument18 pagesChapter 2 - Normal PartnershipmaiNo ratings yet

- Accounting For PartnershipDocument15 pagesAccounting For Partnershipnagesh dashNo ratings yet

- Study Material CH.-1 Fundamentals of Partnership 2023-24Document28 pagesStudy Material CH.-1 Fundamentals of Partnership 2023-24vsy9926No ratings yet

- Accounting For Partnership Firms - Fundamentals 2021Document183 pagesAccounting For Partnership Firms - Fundamentals 2021JPS J100% (1)

- MBD SS Q. Bank ACC - G12 - Ch01Document26 pagesMBD SS Q. Bank ACC - G12 - Ch01Muskan KheraNo ratings yet

- Accounts Theory Chapterwise - 27069624 - 2023 - 12 - 27 - 19 - 231227 - 193022Document80 pagesAccounts Theory Chapterwise - 27069624 - 2023 - 12 - 27 - 19 - 231227 - 193022Vibhu VashishthNo ratings yet

- Partnership NotesDocument35 pagesPartnership Notesa86476007No ratings yet

- Partnership: Basics: DefinitionsDocument13 pagesPartnership: Basics: DefinitionsShiv PatelNo ratings yet

- All Theory Accounts SPCC - 18126678 - 2023 - 05 - 11 - 03 - 26Document28 pagesAll Theory Accounts SPCC - 18126678 - 2023 - 05 - 11 - 03 - 26guptavrinda911No ratings yet

- Work Sheet On Accounting For Partnership FundamentalsDocument19 pagesWork Sheet On Accounting For Partnership Fundamentals8qk77kkhwbNo ratings yet

- 3525 25108 Textbooksolution PDFDocument44 pages3525 25108 Textbooksolution PDFSatinder SinghNo ratings yet

- Partnership AccountingDocument7 pagesPartnership AccountingZaid ZubairiNo ratings yet

- Xii Accounts NOTESDocument13 pagesXii Accounts NOTESNavin PatidarNo ratings yet

- Chapter 2-Accounting For Partnership Firms - Fundamentals: ExerciseDocument44 pagesChapter 2-Accounting For Partnership Firms - Fundamentals: Exercise11 Mahin KhanNo ratings yet

- Fundamentals 2024 PDF SPCCDocument82 pagesFundamentals 2024 PDF SPCCJeetalal GadaNo ratings yet

- Accounting For Partnership Firms - FundamentalsDocument5 pagesAccounting For Partnership Firms - FundamentalsPainNo ratings yet

- Partnership AccountDocument9 pagesPartnership Accountndanujoy180No ratings yet

- Session 4 - Partnership AccountsDocument23 pagesSession 4 - Partnership AccountsFrederickNo ratings yet

- Part 1 Partnership BasicDocument11 pagesPart 1 Partnership BasicSagar YadavNo ratings yet

- IPCC Paper I: Accounting Chapter No. 14 CA Shakuntala ChhanganiDocument130 pagesIPCC Paper I: Accounting Chapter No. 14 CA Shakuntala ChhanganiM SheikhaNo ratings yet

- FAR 2 REVIEWER Other SourceDocument120 pagesFAR 2 REVIEWER Other SourceAirish GeronimoNo ratings yet

- New AccountsDocument26 pagesNew AccountsStudyNo ratings yet

- A001 - PartnershipDocument22 pagesA001 - PartnershipDesiree Dawn GabalesNo ratings yet

- 12 Accountancy Revision Notes Part A CH 1 PDFDocument16 pages12 Accountancy Revision Notes Part A CH 1 PDFniks525No ratings yet

- 12 Accountancy Revision Notes Part A CH 1Document16 pages12 Accountancy Revision Notes Part A CH 1SukhsanjamNo ratings yet

- Assignments For +2Document3 pagesAssignments For +2Prakhar SinghNo ratings yet

- Flow Chart (L-2)Document1 pageFlow Chart (L-2)JazaNo ratings yet

- ACC406 - Chapter 7Document24 pagesACC406 - Chapter 7Carol LeslyNo ratings yet

- Partnership AccountsDocument26 pagesPartnership Accountsoneunique.1unqNo ratings yet

- Partnership Firms Part 2 Appropriation of ProfitDocument14 pagesPartnership Firms Part 2 Appropriation of ProfitDeepti BistNo ratings yet

- Theories Chapter 1 - 5Document11 pagesTheories Chapter 1 - 5u got no jamsNo ratings yet

- Partnership ActivitiesDocument32 pagesPartnership Activitiesandrea.huerto0730No ratings yet

- 457712th MCQ Test 29-1-2019Document6 pages457712th MCQ Test 29-1-2019MohitTagotraNo ratings yet

- Account: 5. in Case of Fixed Capitals, Partners Will HaveDocument3 pagesAccount: 5. in Case of Fixed Capitals, Partners Will HaveNavin PatidarNo ratings yet

- Chapter 6: Appropriation of Profits: Rohit AgarwalDocument4 pagesChapter 6: Appropriation of Profits: Rohit AgarwalbcomNo ratings yet

- Fundamental of Partnership Revision NotesDocument16 pagesFundamental of Partnership Revision NotesTarun SinghalNo ratings yet

- Accounts Full ConceptsDocument91 pagesAccounts Full ConceptsAnmol BehalNo ratings yet

- The Following Instances Do Not Necessarily Establish A PartnershipDocument4 pagesThe Following Instances Do Not Necessarily Establish A PartnershipGIRLNo ratings yet

- Basic AccountingDocument35 pagesBasic AccountingKaraCassandra LayuganNo ratings yet

- Complete TheoryDocument28 pagesComplete TheoryGODSPEED. AltNo ratings yet

- Fundamentals PDFDocument103 pagesFundamentals PDFDhairya JainNo ratings yet

- DocxDocument11 pagesDocxClyden Jaile RamirezNo ratings yet

- Partnership AccountDocument67 pagesPartnership Accounttetteh godwinNo ratings yet

- PartnershipDocument6 pagesPartnershipabhishekanandsingh123goNo ratings yet

- Saint Vincent College of Cabuyao Brgy. Mamatid, City of Cabuyao, Laguna Law On Partnerships Midterm ExamDocument17 pagesSaint Vincent College of Cabuyao Brgy. Mamatid, City of Cabuyao, Laguna Law On Partnerships Midterm ExamDan RyanNo ratings yet

- Of 5% Charging Partnership Monthly (A) 7,5000 (B) 16,500 (C) 8,250Document3 pagesOf 5% Charging Partnership Monthly (A) 7,5000 (B) 16,500 (C) 8,250abhishekNo ratings yet

- Chapter 1 - Formation of PartnershipDocument31 pagesChapter 1 - Formation of PartnershipAisyah BasirNo ratings yet

- Financial Statements of A PartnershipDocument12 pagesFinancial Statements of A PartnershipCharlesNo ratings yet

- Partnership AccountingDocument8 pagesPartnership Accountingferdinand kan pennNo ratings yet

- MCQ Chap1 Scholars PDFDocument11 pagesMCQ Chap1 Scholars PDFPrince TyagiNo ratings yet

- 12 - Acc - Ch2 - Learning FeedbackDocument2 pages12 - Acc - Ch2 - Learning FeedbackSHAH SHREYANo ratings yet

- Basic Legal Ethics - Module 2 - Admission To The Practice of LawDocument39 pagesBasic Legal Ethics - Module 2 - Admission To The Practice of LawDash BencioNo ratings yet

- Binding Sales and Purchase Contract....Document6 pagesBinding Sales and Purchase Contract....Autosale PLCNo ratings yet

- 2022-01-11 Webb ComplaintDocument13 pages2022-01-11 Webb ComplaintErin FuchsNo ratings yet

- Foundation Plan Roof Beam Plan: C D E B A 14.00m C D E B ADocument1 pageFoundation Plan Roof Beam Plan: C D E B A 14.00m C D E B AJohn Carl SalasNo ratings yet

- Week 3 - Professional Practice5Document6 pagesWeek 3 - Professional Practice5jomarie apolinarioNo ratings yet

- Ramcharan V Deonarine - ProbateDocument23 pagesRamcharan V Deonarine - ProbateDarian SammyNo ratings yet

- Property Law-I NotesDocument7 pagesProperty Law-I NotesKritin BahugunaNo ratings yet

- Attachment 1a - SSF Project Memorandum of AgreementDocument6 pagesAttachment 1a - SSF Project Memorandum of AgreementCatherine BenbanNo ratings yet

- Nreing2021091402 5900086294Document2 pagesNreing2021091402 5900086294Thanh Hà LêNo ratings yet

- Industrial Relations: Chapter FourDocument3 pagesIndustrial Relations: Chapter FourAmir HamzahNo ratings yet

- Law Association of Zambia ActDocument41 pagesLaw Association of Zambia Actrobertkarabo.jNo ratings yet

- Appln Form - BTO For BCP (Aug 2018)Document7 pagesAppln Form - BTO For BCP (Aug 2018)Joharn ANo ratings yet

- Innodata v. IntingDocument2 pagesInnodata v. IntingJamiah Hulipas100% (1)

- Letter of Credit Proof of Purchase Funds Affidavit + Tampa Marriott WestshoreDocument2 pagesLetter of Credit Proof of Purchase Funds Affidavit + Tampa Marriott Westshoreshasha ann bey100% (4)

- Pope Francis Motu ProprioDocument18 pagesPope Francis Motu Proprionujahm1639No ratings yet

- VAT in General - CIR Vs CA &CMS, GR No. 125355Document2 pagesVAT in General - CIR Vs CA &CMS, GR No. 125355Christine Gel MadrilejoNo ratings yet

- 6 - Araneta v. Gatmaitan, G.R. Nos. L-8895 and L-9191, April 30, 1957Document2 pages6 - Araneta v. Gatmaitan, G.R. Nos. L-8895 and L-9191, April 30, 1957dasai watashiNo ratings yet

- Ceylon Builders SDN BHD V Ultimate Pursuit SDN BHD and Another Appeal (2018) MLJU 1918Document11 pagesCeylon Builders SDN BHD V Ultimate Pursuit SDN BHD and Another Appeal (2018) MLJU 1918Lawrence LauNo ratings yet

- Graduation 14092023 1Document51 pagesGraduation 14092023 1Venkatesh BhatNo ratings yet

- Name: Sahil Verma ROLL NO.: 2148 Semester: 5 YEAR: 2019-2024 Course: B.A., LL.B (Hons.)Document13 pagesName: Sahil Verma ROLL NO.: 2148 Semester: 5 YEAR: 2019-2024 Course: B.A., LL.B (Hons.)Sachin KumarNo ratings yet

- Testimony Poder Especial Zenaida - Ver EnglishDocument2 pagesTestimony Poder Especial Zenaida - Ver EnglishErnesto VelasquezNo ratings yet

- Halsbury's MistakeDocument73 pagesHalsbury's MistakeMinisterNo ratings yet

- Contract Law in Hong KongDocument52 pagesContract Law in Hong Kongtechang1No ratings yet

- FCC FOIA: StingRay, KingFish User Manual (2010)Document58 pagesFCC FOIA: StingRay, KingFish User Manual (2010)Matthew Keys86% (7)

- Annual Holidays Act 1944Document23 pagesAnnual Holidays Act 1944Ian FlynnNo ratings yet

- (1847) Beloved Physician (Edgar Allan Poe)Document1 page(1847) Beloved Physician (Edgar Allan Poe)StelioPassarisNo ratings yet

- The High Court of Orissa, Cuttack: List of Business For Friday The 18Th October 2019Document46 pagesThe High Court of Orissa, Cuttack: List of Business For Friday The 18Th October 2019sunita beharaNo ratings yet

Download as docx, pdf, or txt

You might also like

- FinAccUnit 3 - Partnership Accounts Lecture Notes PDFDocument8 pagesFinAccUnit 3 - Partnership Accounts Lecture Notes PDFSherona Reid100% (5)

- Affidavit of Loss Policy FORMATDocument1 pageAffidavit of Loss Policy FORMATJC Ardiente100% (2)

- SA Constitution Advantages and DisadvantagesDocument2 pagesSA Constitution Advantages and DisadvantagesPravind KumarNo ratings yet

- 1 - Accounting For Partnership Firms - FundamentalsDocument12 pages1 - Accounting For Partnership Firms - FundamentalsAnkit Roy100% (1)

- Chapter 1 - Formation of PartnershipDocument31 pagesChapter 1 - Formation of PartnershipAisyah Basir33% (3)

- Harry & Meghan V Doe Stipulated InjunctionDocument5 pagesHarry & Meghan V Doe Stipulated InjunctionTHROnline100% (1)

- CH - 2 Accounting For Partnership Firms: Fundamentals: According To Section 4 of The Partnership Act 1932Document12 pagesCH - 2 Accounting For Partnership Firms: Fundamentals: According To Section 4 of The Partnership Act 1932Laksh KhannaNo ratings yet

- Buku Nota PertnershipDocument33 pagesBuku Nota PertnershipmaiNo ratings yet

- Final Account 2020Document30 pagesFinal Account 2020Viransh Coaching ClassesNo ratings yet

- C-1 (Fundamentals of Partnership)Document6 pagesC-1 (Fundamentals of Partnership)adwitanegi068No ratings yet

- Chapter 7: PARTNERSHIPDocument45 pagesChapter 7: PARTNERSHIPSuresh LamsalNo ratings yet

- Chapter 2 - Normal PartnershipDocument18 pagesChapter 2 - Normal PartnershipmaiNo ratings yet

- Accounting For PartnershipDocument15 pagesAccounting For Partnershipnagesh dashNo ratings yet

- Study Material CH.-1 Fundamentals of Partnership 2023-24Document28 pagesStudy Material CH.-1 Fundamentals of Partnership 2023-24vsy9926No ratings yet

- Accounting For Partnership Firms - Fundamentals 2021Document183 pagesAccounting For Partnership Firms - Fundamentals 2021JPS J100% (1)

- MBD SS Q. Bank ACC - G12 - Ch01Document26 pagesMBD SS Q. Bank ACC - G12 - Ch01Muskan KheraNo ratings yet

- Accounts Theory Chapterwise - 27069624 - 2023 - 12 - 27 - 19 - 231227 - 193022Document80 pagesAccounts Theory Chapterwise - 27069624 - 2023 - 12 - 27 - 19 - 231227 - 193022Vibhu VashishthNo ratings yet

- Partnership NotesDocument35 pagesPartnership Notesa86476007No ratings yet

- Partnership: Basics: DefinitionsDocument13 pagesPartnership: Basics: DefinitionsShiv PatelNo ratings yet

- All Theory Accounts SPCC - 18126678 - 2023 - 05 - 11 - 03 - 26Document28 pagesAll Theory Accounts SPCC - 18126678 - 2023 - 05 - 11 - 03 - 26guptavrinda911No ratings yet

- Work Sheet On Accounting For Partnership FundamentalsDocument19 pagesWork Sheet On Accounting For Partnership Fundamentals8qk77kkhwbNo ratings yet

- 3525 25108 Textbooksolution PDFDocument44 pages3525 25108 Textbooksolution PDFSatinder SinghNo ratings yet

- Partnership AccountingDocument7 pagesPartnership AccountingZaid ZubairiNo ratings yet

- Xii Accounts NOTESDocument13 pagesXii Accounts NOTESNavin PatidarNo ratings yet

- Chapter 2-Accounting For Partnership Firms - Fundamentals: ExerciseDocument44 pagesChapter 2-Accounting For Partnership Firms - Fundamentals: Exercise11 Mahin KhanNo ratings yet

- Fundamentals 2024 PDF SPCCDocument82 pagesFundamentals 2024 PDF SPCCJeetalal GadaNo ratings yet

- Accounting For Partnership Firms - FundamentalsDocument5 pagesAccounting For Partnership Firms - FundamentalsPainNo ratings yet

- Partnership AccountDocument9 pagesPartnership Accountndanujoy180No ratings yet

- Session 4 - Partnership AccountsDocument23 pagesSession 4 - Partnership AccountsFrederickNo ratings yet

- Part 1 Partnership BasicDocument11 pagesPart 1 Partnership BasicSagar YadavNo ratings yet

- IPCC Paper I: Accounting Chapter No. 14 CA Shakuntala ChhanganiDocument130 pagesIPCC Paper I: Accounting Chapter No. 14 CA Shakuntala ChhanganiM SheikhaNo ratings yet

- FAR 2 REVIEWER Other SourceDocument120 pagesFAR 2 REVIEWER Other SourceAirish GeronimoNo ratings yet

- New AccountsDocument26 pagesNew AccountsStudyNo ratings yet

- A001 - PartnershipDocument22 pagesA001 - PartnershipDesiree Dawn GabalesNo ratings yet

- 12 Accountancy Revision Notes Part A CH 1 PDFDocument16 pages12 Accountancy Revision Notes Part A CH 1 PDFniks525No ratings yet

- 12 Accountancy Revision Notes Part A CH 1Document16 pages12 Accountancy Revision Notes Part A CH 1SukhsanjamNo ratings yet

- Assignments For +2Document3 pagesAssignments For +2Prakhar SinghNo ratings yet

- Flow Chart (L-2)Document1 pageFlow Chart (L-2)JazaNo ratings yet

- ACC406 - Chapter 7Document24 pagesACC406 - Chapter 7Carol LeslyNo ratings yet

- Partnership AccountsDocument26 pagesPartnership Accountsoneunique.1unqNo ratings yet

- Partnership Firms Part 2 Appropriation of ProfitDocument14 pagesPartnership Firms Part 2 Appropriation of ProfitDeepti BistNo ratings yet

- Theories Chapter 1 - 5Document11 pagesTheories Chapter 1 - 5u got no jamsNo ratings yet

- Partnership ActivitiesDocument32 pagesPartnership Activitiesandrea.huerto0730No ratings yet

- 457712th MCQ Test 29-1-2019Document6 pages457712th MCQ Test 29-1-2019MohitTagotraNo ratings yet

- Account: 5. in Case of Fixed Capitals, Partners Will HaveDocument3 pagesAccount: 5. in Case of Fixed Capitals, Partners Will HaveNavin PatidarNo ratings yet

- Chapter 6: Appropriation of Profits: Rohit AgarwalDocument4 pagesChapter 6: Appropriation of Profits: Rohit AgarwalbcomNo ratings yet

- Fundamental of Partnership Revision NotesDocument16 pagesFundamental of Partnership Revision NotesTarun SinghalNo ratings yet

- Accounts Full ConceptsDocument91 pagesAccounts Full ConceptsAnmol BehalNo ratings yet

- The Following Instances Do Not Necessarily Establish A PartnershipDocument4 pagesThe Following Instances Do Not Necessarily Establish A PartnershipGIRLNo ratings yet

- Basic AccountingDocument35 pagesBasic AccountingKaraCassandra LayuganNo ratings yet

- Complete TheoryDocument28 pagesComplete TheoryGODSPEED. AltNo ratings yet

- Fundamentals PDFDocument103 pagesFundamentals PDFDhairya JainNo ratings yet

- DocxDocument11 pagesDocxClyden Jaile RamirezNo ratings yet

- Partnership AccountDocument67 pagesPartnership Accounttetteh godwinNo ratings yet

- PartnershipDocument6 pagesPartnershipabhishekanandsingh123goNo ratings yet

- Saint Vincent College of Cabuyao Brgy. Mamatid, City of Cabuyao, Laguna Law On Partnerships Midterm ExamDocument17 pagesSaint Vincent College of Cabuyao Brgy. Mamatid, City of Cabuyao, Laguna Law On Partnerships Midterm ExamDan RyanNo ratings yet

- Of 5% Charging Partnership Monthly (A) 7,5000 (B) 16,500 (C) 8,250Document3 pagesOf 5% Charging Partnership Monthly (A) 7,5000 (B) 16,500 (C) 8,250abhishekNo ratings yet

- Chapter 1 - Formation of PartnershipDocument31 pagesChapter 1 - Formation of PartnershipAisyah BasirNo ratings yet

- Financial Statements of A PartnershipDocument12 pagesFinancial Statements of A PartnershipCharlesNo ratings yet

- Partnership AccountingDocument8 pagesPartnership Accountingferdinand kan pennNo ratings yet

- MCQ Chap1 Scholars PDFDocument11 pagesMCQ Chap1 Scholars PDFPrince TyagiNo ratings yet

- 12 - Acc - Ch2 - Learning FeedbackDocument2 pages12 - Acc - Ch2 - Learning FeedbackSHAH SHREYANo ratings yet

- Basic Legal Ethics - Module 2 - Admission To The Practice of LawDocument39 pagesBasic Legal Ethics - Module 2 - Admission To The Practice of LawDash BencioNo ratings yet

- Binding Sales and Purchase Contract....Document6 pagesBinding Sales and Purchase Contract....Autosale PLCNo ratings yet

- 2022-01-11 Webb ComplaintDocument13 pages2022-01-11 Webb ComplaintErin FuchsNo ratings yet

- Foundation Plan Roof Beam Plan: C D E B A 14.00m C D E B ADocument1 pageFoundation Plan Roof Beam Plan: C D E B A 14.00m C D E B AJohn Carl SalasNo ratings yet

- Week 3 - Professional Practice5Document6 pagesWeek 3 - Professional Practice5jomarie apolinarioNo ratings yet

- Ramcharan V Deonarine - ProbateDocument23 pagesRamcharan V Deonarine - ProbateDarian SammyNo ratings yet

- Property Law-I NotesDocument7 pagesProperty Law-I NotesKritin BahugunaNo ratings yet

- Attachment 1a - SSF Project Memorandum of AgreementDocument6 pagesAttachment 1a - SSF Project Memorandum of AgreementCatherine BenbanNo ratings yet

- Nreing2021091402 5900086294Document2 pagesNreing2021091402 5900086294Thanh Hà LêNo ratings yet

- Industrial Relations: Chapter FourDocument3 pagesIndustrial Relations: Chapter FourAmir HamzahNo ratings yet

- Law Association of Zambia ActDocument41 pagesLaw Association of Zambia Actrobertkarabo.jNo ratings yet

- Appln Form - BTO For BCP (Aug 2018)Document7 pagesAppln Form - BTO For BCP (Aug 2018)Joharn ANo ratings yet

- Innodata v. IntingDocument2 pagesInnodata v. IntingJamiah Hulipas100% (1)

- Letter of Credit Proof of Purchase Funds Affidavit + Tampa Marriott WestshoreDocument2 pagesLetter of Credit Proof of Purchase Funds Affidavit + Tampa Marriott Westshoreshasha ann bey100% (4)

- Pope Francis Motu ProprioDocument18 pagesPope Francis Motu Proprionujahm1639No ratings yet

- VAT in General - CIR Vs CA &CMS, GR No. 125355Document2 pagesVAT in General - CIR Vs CA &CMS, GR No. 125355Christine Gel MadrilejoNo ratings yet

- 6 - Araneta v. Gatmaitan, G.R. Nos. L-8895 and L-9191, April 30, 1957Document2 pages6 - Araneta v. Gatmaitan, G.R. Nos. L-8895 and L-9191, April 30, 1957dasai watashiNo ratings yet

- Ceylon Builders SDN BHD V Ultimate Pursuit SDN BHD and Another Appeal (2018) MLJU 1918Document11 pagesCeylon Builders SDN BHD V Ultimate Pursuit SDN BHD and Another Appeal (2018) MLJU 1918Lawrence LauNo ratings yet

- Graduation 14092023 1Document51 pagesGraduation 14092023 1Venkatesh BhatNo ratings yet

- Name: Sahil Verma ROLL NO.: 2148 Semester: 5 YEAR: 2019-2024 Course: B.A., LL.B (Hons.)Document13 pagesName: Sahil Verma ROLL NO.: 2148 Semester: 5 YEAR: 2019-2024 Course: B.A., LL.B (Hons.)Sachin KumarNo ratings yet

- Testimony Poder Especial Zenaida - Ver EnglishDocument2 pagesTestimony Poder Especial Zenaida - Ver EnglishErnesto VelasquezNo ratings yet

- Halsbury's MistakeDocument73 pagesHalsbury's MistakeMinisterNo ratings yet

- Contract Law in Hong KongDocument52 pagesContract Law in Hong Kongtechang1No ratings yet

- FCC FOIA: StingRay, KingFish User Manual (2010)Document58 pagesFCC FOIA: StingRay, KingFish User Manual (2010)Matthew Keys86% (7)

- Annual Holidays Act 1944Document23 pagesAnnual Holidays Act 1944Ian FlynnNo ratings yet

- (1847) Beloved Physician (Edgar Allan Poe)Document1 page(1847) Beloved Physician (Edgar Allan Poe)StelioPassarisNo ratings yet

- The High Court of Orissa, Cuttack: List of Business For Friday The 18Th October 2019Document46 pagesThe High Court of Orissa, Cuttack: List of Business For Friday The 18Th October 2019sunita beharaNo ratings yet