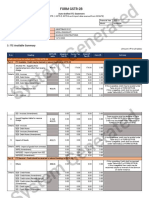

GSTR2B 09aakfe8442j1zz 032024 27042024

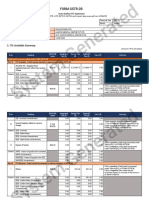

GSTR2B 09aakfe8442j1zz 032024 27042024

You might also like

- GSTR2B 19bfgpa3781l1z6 052024 21062024Document7 pagesGSTR2B 19bfgpa3781l1z6 052024 21062024jasodaglobalNo ratings yet

- GSTR2B 20CHSPM6149M1ZS 032023 10062023Document7 pagesGSTR2B 20CHSPM6149M1ZS 032023 10062023laxmi handloommdpNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryMoolaram NaiNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryRohit GoyalNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryRohit GoyalNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryRohit GoyalNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryRohit GoyalNo ratings yet

- GSTR2B 06alzps2257h2zf 072022 24092022Document7 pagesGSTR2B 06alzps2257h2zf 072022 24092022Robin JoseNo ratings yet

- GSTR2BQ 23Z6 032024 24042024Document7 pagesGSTR2BQ 23Z6 032024 24042024Neha JainNo ratings yet

- GSTR2B 06alzps2257h2zf 112020 24092022Document7 pagesGSTR2B 06alzps2257h2zf 112020 24092022Robin JoseNo ratings yet

- GSTR2B 06alzps2257h2zf 032022 24092022Document7 pagesGSTR2B 06alzps2257h2zf 032022 24092022Robin JoseNo ratings yet

- GSTR9 08aaafu3205h1zh 032022Document8 pagesGSTR9 08aaafu3205h1zh 032022Deepanshu AgarwalNo ratings yet

- GSTR9 09aaact9363l1zq 032023Document8 pagesGSTR9 09aaact9363l1zq 032023sachinkumar.rkcjNo ratings yet

- GSTR9Document8 pagesGSTR9legendry007No ratings yet

- GSTR9 09bwbpk7755a1zk 032021Document8 pagesGSTR9 09bwbpk7755a1zk 032021Ankit JainNo ratings yet

- Gstr3b 20bejps1674a1zv 052023 SystemgeneratedDocument8 pagesGstr3b 20bejps1674a1zv 052023 SystemgeneratedMukund MayankNo ratings yet

- CMP08 33aiwpv0583f1zs 142019 PDFDocument1 pageCMP08 33aiwpv0583f1zs 142019 PDFSoundar RajanNo ratings yet

- GSTR9 22aabcn2864p1z7 032018Document8 pagesGSTR9 22aabcn2864p1z7 032018Sumit K JhaNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BDocument6 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BMUJAHIDUL ISLAM SHAIKHNo ratings yet

- DRC01C PartA 09FZMPP1720E2Z8 092023Document2 pagesDRC01C PartA 09FZMPP1720E2Z8 092023ANISH SHAIKHNo ratings yet

- Gstr3b 19bbspr1755d1z8 062023 SystemgeneratedDocument8 pagesGstr3b 19bbspr1755d1z8 062023 Systemgeneratedb2bservices007No ratings yet

- Gstr3b 27avhpk4246l1z8 052022 SystemgeneratedDocument7 pagesGstr3b 27avhpk4246l1z8 052022 SystemgeneratedRohit GoleNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BDocument6 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BMUJAHIDUL ISLAM SHAIKHNo ratings yet

- GSTR3B 27CHHPP4347K1ZU 032021 SystemGeneratedDocument7 pagesGSTR3B 27CHHPP4347K1ZU 032021 SystemGeneratedShreenath AgarwalNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument8 pagesForm Gstr-2B: 3. ITC Available SummaryNaga DineshNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BDocument7 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BSankar GaneshNo ratings yet

- GSTR3B 03K1Z6 032024 SystemGeneratedDocument10 pagesGSTR3B 03K1Z6 032024 SystemGeneratedNeha JainNo ratings yet

- GSTR9 19GCBPS5582Q1ZH 032023Document8 pagesGSTR9 19GCBPS5582Q1ZH 032023nirmalku2061No ratings yet

- Gstr3b 09ehmpm8928j1zf 062021 SystemgeneratedDocument6 pagesGstr3b 09ehmpm8928j1zf 062021 SystemgeneratedAnkur mittalNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BDocument6 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3Bhiteshmohakar15No ratings yet

- GSTR3B 24GLPPD7998C1ZL 042024 SystemGeneratedDocument9 pagesGSTR3B 24GLPPD7998C1ZL 042024 SystemGeneratedmihirdonga0000No ratings yet

- Gstr3b 10ckvpk6948n1zc 042023 SystemgeneratedDocument8 pagesGstr3b 10ckvpk6948n1zc 042023 Systemgeneratedharshitkr1805No ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BDocument6 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BRahulNo ratings yet

- GSTR3B 24AHSPS6763P1Z6 012023 SystemGeneratedDocument8 pagesGSTR3B 24AHSPS6763P1Z6 012023 SystemGeneratedsammy shergilNo ratings yet

- GSTR3B 18acvpa7546a1zk 032023Document4 pagesGSTR3B 18acvpa7546a1zk 032023SUBHASH MOURNo ratings yet

- Draf T: Form GST CMP - 08Document1 pageDraf T: Form GST CMP - 08akshaya beheraNo ratings yet

- GSTR3B 33AAKCB0823F1Z5 022023 SystemGenerated PDFDocument8 pagesGSTR3B 33AAKCB0823F1Z5 022023 SystemGenerated PDFBairava MotorsNo ratings yet

- GSTR3B 06AACFP9032F1ZF 012024 SystemGeneratedDocument11 pagesGSTR3B 06AACFP9032F1ZF 012024 SystemGeneratedsangeeta.pgcNo ratings yet

- GSTR3B 29AVRPA8118R1ZP 032024 SystemGeneratedDocument10 pagesGSTR3B 29AVRPA8118R1ZP 032024 SystemGeneratedzeeshanNo ratings yet

- GSTR3B 08BYJPV8296H1ZF 122023 SystemGeneratedDocument9 pagesGSTR3B 08BYJPV8296H1ZF 122023 SystemGenerateddeepak9921.vscNo ratings yet

- GSTR 9Document83 pagesGSTR 9arnavsingh9681No ratings yet

- GSTR9 27aasfp7032r1za 032020Document9 pagesGSTR9 27aasfp7032r1za 032020sharad agarwalNo ratings yet

- Gstr3b 09cthpc2168r1z3 012024 SystemgeneratedDocument11 pagesGstr3b 09cthpc2168r1z3 012024 SystemgeneratedColt HogeNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BDocument7 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3Bgotbaya rNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BDocument7 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BMaddy GamerNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BDocument7 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BArun SasidharanNo ratings yet

- GSTR3B 27AEKPA5006N1ZI 122022 SystemGeneratedDocument7 pagesGSTR3B 27AEKPA5006N1ZI 122022 SystemGeneratedGSTMS ANSARINo ratings yet

- GSTR3B 07AALCP1900G1ZN 112022 SystemGeneratedDocument7 pagesGSTR3B 07AALCP1900G1ZN 112022 SystemGeneratedChandan KumarNo ratings yet

- Form No. 16A: From ToDocument2 pagesForm No. 16A: From ToAYUSH PRADHANNo ratings yet

- GSTR9 07balps3408q1z0 032023Document4 pagesGSTR9 07balps3408q1z0 032023RINKOO SHARMANo ratings yet

- GSTR3B 27CHHPP4347K1ZU 042021 SystemGeneratedDocument7 pagesGSTR3B 27CHHPP4347K1ZU 042021 SystemGeneratedShreenath AgarwalNo ratings yet

- FIN AL: Form GSTR-9Document8 pagesFIN AL: Form GSTR-9mani samiNo ratings yet

- GSTR9 09abepk8302l1zh 032018Document8 pagesGSTR9 09abepk8302l1zh 032018Capraful PrabhakaranNo ratings yet

- 1478316c PDFDocument9 pages1478316c PDFmurapakasrinivasNo ratings yet

- GSTR3B 21ACGPD6446D2Z5 062023 SystemGeneratedDocument7 pagesGSTR3B 21ACGPD6446D2Z5 062023 SystemGeneratedsamir ranjan dhalNo ratings yet

- GSTR3B 07AAQCM3579H1ZW 122023 SystemGeneratedDocument9 pagesGSTR3B 07AAQCM3579H1ZW 122023 SystemGeneratedAshish SinhaNo ratings yet

- GSTR9 18acvpa7546a1zk 032022Document8 pagesGSTR9 18acvpa7546a1zk 032022SUBHASH MOURNo ratings yet

- New Form 16 AY 11 12Document5 pagesNew Form 16 AY 11 12RMD Financial ServicesNo ratings yet

- GSTR9 29aahcv2115k1z5 032020Document8 pagesGSTR9 29aahcv2115k1z5 032020MICO EMPLOYEES CO OPERATIVE SOCIETY LTDNo ratings yet

- Starter Motors & Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandStarter Motors & Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- Ahaan HR Services Agreement 2024Document5 pagesAhaan HR Services Agreement 2024pm.shailendratiwariNo ratings yet

- T No 32WODocument7 pagesT No 32WOpm.shailendratiwariNo ratings yet

- Po PlacedDocument1 pagePo Placedpm.shailendratiwariNo ratings yet

- SUMMARYDocument1 pageSUMMARYpm.shailendratiwariNo ratings yet

- Signature Not Verified: Digitally Signed by ANUPAM KHARE Date: 2024.01.20 16:28:28 IST Location: Uttar Pradesh-UPDocument1 pageSignature Not Verified: Digitally Signed by ANUPAM KHARE Date: 2024.01.20 16:28:28 IST Location: Uttar Pradesh-UPpm.shailendratiwariNo ratings yet

- Emsons Company Profile NEwDocument7 pagesEmsons Company Profile NEwpm.shailendratiwariNo ratings yet

- JCIL Work OrderDocument1 pageJCIL Work Orderpm.shailendratiwariNo ratings yet

- Ecommerce BookDocument80 pagesEcommerce BookUsman ArifNo ratings yet

- Project File On E-CommerceDocument33 pagesProject File On E-CommerceHimanshu HNo ratings yet

- Chapter - Ii Review of LiteratureDocument22 pagesChapter - Ii Review of LiteraturePurnima SidhwaniNo ratings yet

- Define Your Brand Positioning To Help Your B2B Brand Win 1578080062Document22 pagesDefine Your Brand Positioning To Help Your B2B Brand Win 1578080062Franc NearyNo ratings yet

- Entrepreneurship and StartupDocument20 pagesEntrepreneurship and Startupsumiths32No ratings yet

- Street Food IndustryDocument29 pagesStreet Food IndustryÚhõk ĐëvąśïNo ratings yet

- Unicorn Startups Case StudiesDocument39 pagesUnicorn Startups Case StudiesPranay Singh RaghuvanshiNo ratings yet

- Tausif Hossain Khan 192480Document46 pagesTausif Hossain Khan 192480khan.stu2018No ratings yet

- Expressions!: Marketing WordsDocument3 pagesExpressions!: Marketing WordsJOEL ISRAEL MENECES LUTINONo ratings yet

- CBM0016Document8 pagesCBM0016Dyna RoseteNo ratings yet

- Customer Relationship Management NDocument192 pagesCustomer Relationship Management NInfotech Edge100% (1)

- Sales Manager in Atlanta GA Resume David CrookDocument2 pagesSales Manager in Atlanta GA Resume David Crookdavidcrook1No ratings yet

- Data Collection Survey On Formulation and Promotion of Wellness Clusters in JordanDocument326 pagesData Collection Survey On Formulation and Promotion of Wellness Clusters in Jordanlancesara747zaidatrNo ratings yet

- Finma7 Module2Document12 pagesFinma7 Module2melody longakitNo ratings yet

- Session 12 - Marketing - Helping Buyers BuyDocument36 pagesSession 12 - Marketing - Helping Buyers BuyAprilia FransiskaNo ratings yet

- HubSpots 2024 Sales Trends ReportDocument45 pagesHubSpots 2024 Sales Trends Reportindrax64100% (1)

- The Chief Marketing Officer First Quarter 2023 - Shared by WorldLine TechnologyDocument41 pagesThe Chief Marketing Officer First Quarter 2023 - Shared by WorldLine TechnologySang TrầnNo ratings yet

- B2BM Case Maersk LineDocument23 pagesB2BM Case Maersk LineRoshan GurjarNo ratings yet

- Literature Review On Purchase IntentionDocument5 pagesLiterature Review On Purchase Intentionaflsjnfvj100% (1)

- Test Bank With Answers of Accounting Information System by Turner Chapter 14Document33 pagesTest Bank With Answers of Accounting Information System by Turner Chapter 14Ebook free0% (1)

- Information Technology Project ReportDocument124 pagesInformation Technology Project ReportPriyal Gajjar100% (1)

- Design and Implementation of Online Cash Receipt Generating System For A SupermarketDocument51 pagesDesign and Implementation of Online Cash Receipt Generating System For A Supermarketofficial adeNo ratings yet

- Unit 5Document61 pagesUnit 5Gaurav -VGPNo ratings yet

- Short Answer Questions / 2 Mark Question With Answers: Marketing ManagementDocument5 pagesShort Answer Questions / 2 Mark Question With Answers: Marketing Managementmba deptNo ratings yet

- Customer Satisfaction Level of Customer's of Amazon Company (1) 1Document88 pagesCustomer Satisfaction Level of Customer's of Amazon Company (1) 1deepak GuptaNo ratings yet

- E-Commerce Business Models and Concepts: Slide 2-1Document52 pagesE-Commerce Business Models and Concepts: Slide 2-1zoe regina castroNo ratings yet

- Agua Pitch Deck 16030842549614924Document14 pagesAgua Pitch Deck 16030842549614924kavenindiaNo ratings yet

- Introduction To Business-to-Business (B2B) MarketingDocument15 pagesIntroduction To Business-to-Business (B2B) Marketingkhawer masoodNo ratings yet

- E-Commerce: Dr. Babasaheb Ambedkar Open University AhmedabadDocument61 pagesE-Commerce: Dr. Babasaheb Ambedkar Open University Ahmedabadmaulik shahNo ratings yet

- Chapter 15 Test Bank - Version1Document26 pagesChapter 15 Test Bank - Version1mjjongh103No ratings yet

Download as pdf or txt

You might also like

- GSTR2B 19bfgpa3781l1z6 052024 21062024Document7 pagesGSTR2B 19bfgpa3781l1z6 052024 21062024jasodaglobalNo ratings yet

- GSTR2B 20CHSPM6149M1ZS 032023 10062023Document7 pagesGSTR2B 20CHSPM6149M1ZS 032023 10062023laxmi handloommdpNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryMoolaram NaiNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryRohit GoyalNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryRohit GoyalNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryRohit GoyalNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument7 pagesForm Gstr-2B: 3. ITC Available SummaryRohit GoyalNo ratings yet

- GSTR2B 06alzps2257h2zf 072022 24092022Document7 pagesGSTR2B 06alzps2257h2zf 072022 24092022Robin JoseNo ratings yet

- GSTR2BQ 23Z6 032024 24042024Document7 pagesGSTR2BQ 23Z6 032024 24042024Neha JainNo ratings yet

- GSTR2B 06alzps2257h2zf 112020 24092022Document7 pagesGSTR2B 06alzps2257h2zf 112020 24092022Robin JoseNo ratings yet

- GSTR2B 06alzps2257h2zf 032022 24092022Document7 pagesGSTR2B 06alzps2257h2zf 032022 24092022Robin JoseNo ratings yet

- GSTR9 08aaafu3205h1zh 032022Document8 pagesGSTR9 08aaafu3205h1zh 032022Deepanshu AgarwalNo ratings yet

- GSTR9 09aaact9363l1zq 032023Document8 pagesGSTR9 09aaact9363l1zq 032023sachinkumar.rkcjNo ratings yet

- GSTR9Document8 pagesGSTR9legendry007No ratings yet

- GSTR9 09bwbpk7755a1zk 032021Document8 pagesGSTR9 09bwbpk7755a1zk 032021Ankit JainNo ratings yet

- Gstr3b 20bejps1674a1zv 052023 SystemgeneratedDocument8 pagesGstr3b 20bejps1674a1zv 052023 SystemgeneratedMukund MayankNo ratings yet

- CMP08 33aiwpv0583f1zs 142019 PDFDocument1 pageCMP08 33aiwpv0583f1zs 142019 PDFSoundar RajanNo ratings yet

- GSTR9 22aabcn2864p1z7 032018Document8 pagesGSTR9 22aabcn2864p1z7 032018Sumit K JhaNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BDocument6 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BMUJAHIDUL ISLAM SHAIKHNo ratings yet

- DRC01C PartA 09FZMPP1720E2Z8 092023Document2 pagesDRC01C PartA 09FZMPP1720E2Z8 092023ANISH SHAIKHNo ratings yet

- Gstr3b 19bbspr1755d1z8 062023 SystemgeneratedDocument8 pagesGstr3b 19bbspr1755d1z8 062023 Systemgeneratedb2bservices007No ratings yet

- Gstr3b 27avhpk4246l1z8 052022 SystemgeneratedDocument7 pagesGstr3b 27avhpk4246l1z8 052022 SystemgeneratedRohit GoleNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BDocument6 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BMUJAHIDUL ISLAM SHAIKHNo ratings yet

- GSTR3B 27CHHPP4347K1ZU 032021 SystemGeneratedDocument7 pagesGSTR3B 27CHHPP4347K1ZU 032021 SystemGeneratedShreenath AgarwalNo ratings yet

- Form Gstr-2B: 3. ITC Available SummaryDocument8 pagesForm Gstr-2B: 3. ITC Available SummaryNaga DineshNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BDocument7 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BSankar GaneshNo ratings yet

- GSTR3B 03K1Z6 032024 SystemGeneratedDocument10 pagesGSTR3B 03K1Z6 032024 SystemGeneratedNeha JainNo ratings yet

- GSTR9 19GCBPS5582Q1ZH 032023Document8 pagesGSTR9 19GCBPS5582Q1ZH 032023nirmalku2061No ratings yet

- Gstr3b 09ehmpm8928j1zf 062021 SystemgeneratedDocument6 pagesGstr3b 09ehmpm8928j1zf 062021 SystemgeneratedAnkur mittalNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BDocument6 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3Bhiteshmohakar15No ratings yet

- GSTR3B 24GLPPD7998C1ZL 042024 SystemGeneratedDocument9 pagesGSTR3B 24GLPPD7998C1ZL 042024 SystemGeneratedmihirdonga0000No ratings yet

- Gstr3b 10ckvpk6948n1zc 042023 SystemgeneratedDocument8 pagesGstr3b 10ckvpk6948n1zc 042023 Systemgeneratedharshitkr1805No ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BDocument6 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1,3.2 and 4 of FORM GSTR-3BRahulNo ratings yet

- GSTR3B 24AHSPS6763P1Z6 012023 SystemGeneratedDocument8 pagesGSTR3B 24AHSPS6763P1Z6 012023 SystemGeneratedsammy shergilNo ratings yet

- GSTR3B 18acvpa7546a1zk 032023Document4 pagesGSTR3B 18acvpa7546a1zk 032023SUBHASH MOURNo ratings yet

- Draf T: Form GST CMP - 08Document1 pageDraf T: Form GST CMP - 08akshaya beheraNo ratings yet

- GSTR3B 33AAKCB0823F1Z5 022023 SystemGenerated PDFDocument8 pagesGSTR3B 33AAKCB0823F1Z5 022023 SystemGenerated PDFBairava MotorsNo ratings yet

- GSTR3B 06AACFP9032F1ZF 012024 SystemGeneratedDocument11 pagesGSTR3B 06AACFP9032F1ZF 012024 SystemGeneratedsangeeta.pgcNo ratings yet

- GSTR3B 29AVRPA8118R1ZP 032024 SystemGeneratedDocument10 pagesGSTR3B 29AVRPA8118R1ZP 032024 SystemGeneratedzeeshanNo ratings yet

- GSTR3B 08BYJPV8296H1ZF 122023 SystemGeneratedDocument9 pagesGSTR3B 08BYJPV8296H1ZF 122023 SystemGenerateddeepak9921.vscNo ratings yet

- GSTR 9Document83 pagesGSTR 9arnavsingh9681No ratings yet

- GSTR9 27aasfp7032r1za 032020Document9 pagesGSTR9 27aasfp7032r1za 032020sharad agarwalNo ratings yet

- Gstr3b 09cthpc2168r1z3 012024 SystemgeneratedDocument11 pagesGstr3b 09cthpc2168r1z3 012024 SystemgeneratedColt HogeNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BDocument7 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3Bgotbaya rNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BDocument7 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BMaddy GamerNo ratings yet

- Form GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BDocument7 pagesForm GSTR-3B System Generated Summary: Section I: Auto-Populated Details of Table 3.1, 3.2, 4 and 5.1 of FORM GSTR-3BArun SasidharanNo ratings yet

- GSTR3B 27AEKPA5006N1ZI 122022 SystemGeneratedDocument7 pagesGSTR3B 27AEKPA5006N1ZI 122022 SystemGeneratedGSTMS ANSARINo ratings yet

- GSTR3B 07AALCP1900G1ZN 112022 SystemGeneratedDocument7 pagesGSTR3B 07AALCP1900G1ZN 112022 SystemGeneratedChandan KumarNo ratings yet

- Form No. 16A: From ToDocument2 pagesForm No. 16A: From ToAYUSH PRADHANNo ratings yet

- GSTR9 07balps3408q1z0 032023Document4 pagesGSTR9 07balps3408q1z0 032023RINKOO SHARMANo ratings yet

- GSTR3B 27CHHPP4347K1ZU 042021 SystemGeneratedDocument7 pagesGSTR3B 27CHHPP4347K1ZU 042021 SystemGeneratedShreenath AgarwalNo ratings yet

- FIN AL: Form GSTR-9Document8 pagesFIN AL: Form GSTR-9mani samiNo ratings yet

- GSTR9 09abepk8302l1zh 032018Document8 pagesGSTR9 09abepk8302l1zh 032018Capraful PrabhakaranNo ratings yet

- 1478316c PDFDocument9 pages1478316c PDFmurapakasrinivasNo ratings yet

- GSTR3B 21ACGPD6446D2Z5 062023 SystemGeneratedDocument7 pagesGSTR3B 21ACGPD6446D2Z5 062023 SystemGeneratedsamir ranjan dhalNo ratings yet

- GSTR3B 07AAQCM3579H1ZW 122023 SystemGeneratedDocument9 pagesGSTR3B 07AAQCM3579H1ZW 122023 SystemGeneratedAshish SinhaNo ratings yet

- GSTR9 18acvpa7546a1zk 032022Document8 pagesGSTR9 18acvpa7546a1zk 032022SUBHASH MOURNo ratings yet

- New Form 16 AY 11 12Document5 pagesNew Form 16 AY 11 12RMD Financial ServicesNo ratings yet

- GSTR9 29aahcv2115k1z5 032020Document8 pagesGSTR9 29aahcv2115k1z5 032020MICO EMPLOYEES CO OPERATIVE SOCIETY LTDNo ratings yet

- Starter Motors & Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandStarter Motors & Parts (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- Ahaan HR Services Agreement 2024Document5 pagesAhaan HR Services Agreement 2024pm.shailendratiwariNo ratings yet

- T No 32WODocument7 pagesT No 32WOpm.shailendratiwariNo ratings yet

- Po PlacedDocument1 pagePo Placedpm.shailendratiwariNo ratings yet

- SUMMARYDocument1 pageSUMMARYpm.shailendratiwariNo ratings yet

- Signature Not Verified: Digitally Signed by ANUPAM KHARE Date: 2024.01.20 16:28:28 IST Location: Uttar Pradesh-UPDocument1 pageSignature Not Verified: Digitally Signed by ANUPAM KHARE Date: 2024.01.20 16:28:28 IST Location: Uttar Pradesh-UPpm.shailendratiwariNo ratings yet

- Emsons Company Profile NEwDocument7 pagesEmsons Company Profile NEwpm.shailendratiwariNo ratings yet

- JCIL Work OrderDocument1 pageJCIL Work Orderpm.shailendratiwariNo ratings yet

- Ecommerce BookDocument80 pagesEcommerce BookUsman ArifNo ratings yet

- Project File On E-CommerceDocument33 pagesProject File On E-CommerceHimanshu HNo ratings yet

- Chapter - Ii Review of LiteratureDocument22 pagesChapter - Ii Review of LiteraturePurnima SidhwaniNo ratings yet

- Define Your Brand Positioning To Help Your B2B Brand Win 1578080062Document22 pagesDefine Your Brand Positioning To Help Your B2B Brand Win 1578080062Franc NearyNo ratings yet

- Entrepreneurship and StartupDocument20 pagesEntrepreneurship and Startupsumiths32No ratings yet

- Street Food IndustryDocument29 pagesStreet Food IndustryÚhõk ĐëvąśïNo ratings yet

- Unicorn Startups Case StudiesDocument39 pagesUnicorn Startups Case StudiesPranay Singh RaghuvanshiNo ratings yet

- Tausif Hossain Khan 192480Document46 pagesTausif Hossain Khan 192480khan.stu2018No ratings yet

- Expressions!: Marketing WordsDocument3 pagesExpressions!: Marketing WordsJOEL ISRAEL MENECES LUTINONo ratings yet

- CBM0016Document8 pagesCBM0016Dyna RoseteNo ratings yet

- Customer Relationship Management NDocument192 pagesCustomer Relationship Management NInfotech Edge100% (1)

- Sales Manager in Atlanta GA Resume David CrookDocument2 pagesSales Manager in Atlanta GA Resume David Crookdavidcrook1No ratings yet

- Data Collection Survey On Formulation and Promotion of Wellness Clusters in JordanDocument326 pagesData Collection Survey On Formulation and Promotion of Wellness Clusters in Jordanlancesara747zaidatrNo ratings yet

- Finma7 Module2Document12 pagesFinma7 Module2melody longakitNo ratings yet

- Session 12 - Marketing - Helping Buyers BuyDocument36 pagesSession 12 - Marketing - Helping Buyers BuyAprilia FransiskaNo ratings yet

- HubSpots 2024 Sales Trends ReportDocument45 pagesHubSpots 2024 Sales Trends Reportindrax64100% (1)

- The Chief Marketing Officer First Quarter 2023 - Shared by WorldLine TechnologyDocument41 pagesThe Chief Marketing Officer First Quarter 2023 - Shared by WorldLine TechnologySang TrầnNo ratings yet

- B2BM Case Maersk LineDocument23 pagesB2BM Case Maersk LineRoshan GurjarNo ratings yet

- Literature Review On Purchase IntentionDocument5 pagesLiterature Review On Purchase Intentionaflsjnfvj100% (1)

- Test Bank With Answers of Accounting Information System by Turner Chapter 14Document33 pagesTest Bank With Answers of Accounting Information System by Turner Chapter 14Ebook free0% (1)

- Information Technology Project ReportDocument124 pagesInformation Technology Project ReportPriyal Gajjar100% (1)

- Design and Implementation of Online Cash Receipt Generating System For A SupermarketDocument51 pagesDesign and Implementation of Online Cash Receipt Generating System For A Supermarketofficial adeNo ratings yet

- Unit 5Document61 pagesUnit 5Gaurav -VGPNo ratings yet

- Short Answer Questions / 2 Mark Question With Answers: Marketing ManagementDocument5 pagesShort Answer Questions / 2 Mark Question With Answers: Marketing Managementmba deptNo ratings yet

- Customer Satisfaction Level of Customer's of Amazon Company (1) 1Document88 pagesCustomer Satisfaction Level of Customer's of Amazon Company (1) 1deepak GuptaNo ratings yet

- E-Commerce Business Models and Concepts: Slide 2-1Document52 pagesE-Commerce Business Models and Concepts: Slide 2-1zoe regina castroNo ratings yet

- Agua Pitch Deck 16030842549614924Document14 pagesAgua Pitch Deck 16030842549614924kavenindiaNo ratings yet

- Introduction To Business-to-Business (B2B) MarketingDocument15 pagesIntroduction To Business-to-Business (B2B) Marketingkhawer masoodNo ratings yet

- E-Commerce: Dr. Babasaheb Ambedkar Open University AhmedabadDocument61 pagesE-Commerce: Dr. Babasaheb Ambedkar Open University Ahmedabadmaulik shahNo ratings yet

- Chapter 15 Test Bank - Version1Document26 pagesChapter 15 Test Bank - Version1mjjongh103No ratings yet