EC2B3 Topic 10 Lecture Slides

EC2B3 Topic 10 Lecture Slides

You might also like

- Questions With Answers On is-LM ModelDocument12 pagesQuestions With Answers On is-LM ModelAkshay Singh67% (3)

- Business Cycles and Aggregate DemandDocument40 pagesBusiness Cycles and Aggregate DemandSnehal Joshi100% (1)

- Fiscal and Monetary Policy of GermanyDocument125 pagesFiscal and Monetary Policy of Germanyarpit vora100% (2)

- Introductory Macroeconomics ECON10003: Lecture 6: The Keynesian Model of The Economy IDocument24 pagesIntroductory Macroeconomics ECON10003: Lecture 6: The Keynesian Model of The Economy IImaweeb 77No ratings yet

- EC2B3 Topic 9 Lecture SlidesDocument40 pagesEC2B3 Topic 9 Lecture Slidescherryyu.nyNo ratings yet

- End Term Cheat SheetDocument2 pagesEnd Term Cheat SheetnupurNo ratings yet

- Lecture 13Document20 pagesLecture 13MaríaNo ratings yet

- EC2B3 Topic 8 Lecture SlidesDocument37 pagesEC2B3 Topic 8 Lecture Slidescherryyu.nyNo ratings yet

- ECO 302 Intermediate Macroeconomic Theory I: The IS Curve (Jones Chapter 11)Document45 pagesECO 302 Intermediate Macroeconomic Theory I: The IS Curve (Jones Chapter 11)Md SafiNo ratings yet

- Ch. 2Document22 pagesCh. 2suinyun16No ratings yet

- Example Example: (5.5) : Continuation of (5.4)Document22 pagesExample Example: (5.5) : Continuation of (5.4)KoyakuNo ratings yet

- 1.6 Savings and BorrowingDocument35 pages1.6 Savings and BorrowingAnh Quan NguyenNo ratings yet

- Unit 5: Long-Run Consequences of Stabilization PoliciesDocument81 pagesUnit 5: Long-Run Consequences of Stabilization PoliciesPriscilla SamaniegoNo ratings yet

- Week10 Monday SlidesDocument26 pagesWeek10 Monday Slidesnellyu761No ratings yet

- Inflation - Curbing InflationDocument11 pagesInflation - Curbing InflationMỹ HàNo ratings yet

- Homework 6 - AKDocument4 pagesHomework 6 - AKMaríaNo ratings yet

- Session 17 - Fiscal PolicyDocument54 pagesSession 17 - Fiscal PolicyLakshmi Harshitha mNo ratings yet

- Chapter 4 Fiscal PolicyDocument29 pagesChapter 4 Fiscal PolicyMinh HuỳnhNo ratings yet

- Week 2 - Economic and Industry Analysis 2023Document43 pagesWeek 2 - Economic and Industry Analysis 2023Katty MothaNo ratings yet

- Econ 112 Lecture 6Document23 pagesEcon 112 Lecture 6CHUA WEI JINNo ratings yet

- Macro5 Lecppt ch11Document88 pagesMacro5 Lecppt ch11이가빈[학생](국제대학 국제학과)No ratings yet

- Chapter 40 Macroeconomic Demand Side PoliciesDocument12 pagesChapter 40 Macroeconomic Demand Side Policiesmoots altNo ratings yet

- EC 102 Revisions Lectures - Macro - 2015Document54 pagesEC 102 Revisions Lectures - Macro - 2015TylerTangTengYangNo ratings yet

- Monetary & Fiscal PolicyDocument5 pagesMonetary & Fiscal PolicyAlya MaisarahNo ratings yet

- MECO121 UM S2024 Session18Document25 pagesMECO121 UM S2024 Session18rizwanf026No ratings yet

- Slides For Topic 4 - InflationDocument23 pagesSlides For Topic 4 - InflationNesma HusseinNo ratings yet

- Aggregate Demand - MacroDocument21 pagesAggregate Demand - MacroHaardik GandhiNo ratings yet

- CH 11 Lo - Fiscal - PolicyDocument28 pagesCH 11 Lo - Fiscal - Policytariku1234No ratings yet

- MECO121 UM S2024 Session17Document30 pagesMECO121 UM S2024 Session17rizwanf026No ratings yet

- Ch. 31-34Document66 pagesCh. 31-34Alaa DawoudNo ratings yet

- Lecture 5 - Cyclical InstabilityDocument66 pagesLecture 5 - Cyclical InstabilityTechno NowNo ratings yet

- Krugman Unit Four Modules 16 To 21Document76 pagesKrugman Unit Four Modules 16 To 21derengungorNo ratings yet

- The Consumption FunctionDocument21 pagesThe Consumption Functionsadhu124No ratings yet

- Economy SR 1Document34 pagesEconomy SR 1PriyanshNo ratings yet

- Final Fresentation GOVERNMENT DEBTDocument18 pagesFinal Fresentation GOVERNMENT DEBTIzba ShahzadNo ratings yet

- Shifts of The Curve: Price Level Money Supply ExogenousDocument28 pagesShifts of The Curve: Price Level Money Supply ExogenousKoyakuNo ratings yet

- Chapter 26-02.09.09Document54 pagesChapter 26-02.09.09af.rashedi79No ratings yet

- My Aggregate Demand & Aggregate Supply (Edited For Class)Document113 pagesMy Aggregate Demand & Aggregate Supply (Edited For Class)ShivamNo ratings yet

- CH3 Aggregate Demand and Aggregate SupplyDocument40 pagesCH3 Aggregate Demand and Aggregate SupplyTiviyaNo ratings yet

- Group 5 1 Slides Wide - MDDocument70 pagesGroup 5 1 Slides Wide - MDSumukh VasishtNo ratings yet

- Definition of Fiscal Policy: ADocument21 pagesDefinition of Fiscal Policy: Amanish9890No ratings yet

- Video Lecture 4.3 IS-LM-PC ModelDocument5 pagesVideo Lecture 4.3 IS-LM-PC ModelAndrás TímárNo ratings yet

- Lecture 4Document25 pagesLecture 4CHUA WEI JINNo ratings yet

- Macroeconomics - Keynesian ModelsDocument22 pagesMacroeconomics - Keynesian ModelsAlfa RydesterNo ratings yet

- Chapter 7 MMDocument44 pagesChapter 7 MMbusi.kg.tshNo ratings yet

- CH6 Fiscal Policy, Taxes and BudgetsDocument28 pagesCH6 Fiscal Policy, Taxes and BudgetsTiviyaNo ratings yet

- The Income Statement and Adjusting Entries: Financial Accounting - Lecture 2Document21 pagesThe Income Statement and Adjusting Entries: Financial Accounting - Lecture 2Peter Shang100% (1)

- CH 10 Lo - Economic - InstabilityDocument26 pagesCH 10 Lo - Economic - Instabilitytariku1234No ratings yet

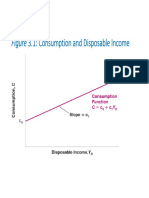

- Figure 3.1: Consumption and Disposable IncomeDocument33 pagesFigure 3.1: Consumption and Disposable IncomeKoyakuNo ratings yet

- Global Economics: PGP: Shekhar TomarDocument38 pagesGlobal Economics: PGP: Shekhar TomarDivyang SaxenaNo ratings yet

- Chaopte r34 NotesDocument5 pagesChaopte r34 Noteschinsu6893No ratings yet

- 1 Economic Influences-Macroeconomic PoliciesDocument16 pages1 Economic Influences-Macroeconomic PoliciesNinjaTylerFortniteBlevins 2.0No ratings yet

- Monetary Policies During Excess Demand and Deficient DemandDocument38 pagesMonetary Policies During Excess Demand and Deficient DemandABIN THOMASNo ratings yet

- Business Cycles Week 6 29102023 035246pmDocument18 pagesBusiness Cycles Week 6 29102023 035246pmMuhammad SarmadNo ratings yet

- Money and InflationDocument29 pagesMoney and InflationBogdan BoldeaNo ratings yet

- FM03 Debt 0831Document68 pagesFM03 Debt 0831Kenneth KwokNo ratings yet

- Inflation and The Quantity Theory of MoneyDocument22 pagesInflation and The Quantity Theory of MoneyBình Nguyễn ĐăngNo ratings yet

- Week 11-14 - Chapters 22-23 - Fiscal and Monetary PoliciesDocument33 pagesWeek 11-14 - Chapters 22-23 - Fiscal and Monetary PoliciesOona NiallNo ratings yet

- Lecture 2 - National Income Accounting - PT 1 PDFDocument45 pagesLecture 2 - National Income Accounting - PT 1 PDFDavidNo ratings yet

- The Food Service Professional Guide to Controlling Liquor, Wine & Beverage CostsFrom EverandThe Food Service Professional Guide to Controlling Liquor, Wine & Beverage CostsNo ratings yet

- Bloomberg Ticker Codes EPRA-NAREITDocument4 pagesBloomberg Ticker Codes EPRA-NAREITps4scribdNo ratings yet

- Chapter 3Document49 pagesChapter 3Trang ĐoànNo ratings yet

- Practice MCQDocument6 pagesPractice MCQsaiNo ratings yet

- Kimberly Amadeo: Money SupplyDocument3 pagesKimberly Amadeo: Money SupplytawandaNo ratings yet

- CH 29Document36 pagesCH 29Robelen CallantaNo ratings yet

- Fiscal PolicyDocument21 pagesFiscal PolicycamilleNo ratings yet

- Mishkin Econ13e PPT 15Document31 pagesMishkin Econ13e PPT 15quynhle.31221021604No ratings yet

- Martinez Monetary Policy Vs Fiscal PolicyDocument18 pagesMartinez Monetary Policy Vs Fiscal Policyapi-273088531No ratings yet

- Course: Understanding Economic Policymaking by IE Business School Week-2: Fiscal Policy Tool QuizDocument6 pagesCourse: Understanding Economic Policymaking by IE Business School Week-2: Fiscal Policy Tool QuizSofia Yurina100% (1)

- EssayDocument5 pagesEssayJim_Tsao_4234No ratings yet

- Phillips CurveDocument5 pagesPhillips CurveAnkush PalNo ratings yet

- Chapter 31 - Parkin - PowerPointDocument15 pagesChapter 31 - Parkin - PowerPointUzair IsmailNo ratings yet

- Macroeconomic Policy in An Open Economy: EconomicsDocument26 pagesMacroeconomic Policy in An Open Economy: EconomicsAman PratikNo ratings yet

- CH - 9 - Income and Spending - Keynesian Multipliers PDFDocument18 pagesCH - 9 - Income and Spending - Keynesian Multipliers PDFHarmandeep Singh50% (2)

- Instruments of Moneytary PolicyDocument3 pagesInstruments of Moneytary PolicyJaydeep Paul100% (1)

- Mundell Fleming ModelDocument22 pagesMundell Fleming ModelDhruv BhandariNo ratings yet

- Principles of Macroeconomics IDocument3 pagesPrinciples of Macroeconomics IanushkaanandaniiiNo ratings yet

- The Gold Standard &Document20 pagesThe Gold Standard &Paavni SharmaNo ratings yet

- Keynesian and MonetaristDocument9 pagesKeynesian and MonetaristCeaserNo ratings yet

- Fed Rate Cut N ImplicationsDocument8 pagesFed Rate Cut N Implicationssplusk100% (1)

- Chapter 11 Dornbusch Fisher SolutionsDocument13 pagesChapter 11 Dornbusch Fisher Solutions22ech040No ratings yet

- MoneyDocument6 pagesMoneyritoja770No ratings yet

- Multiple Choice Questions: d) d) R d) θ (1−c) M θ) increaseDocument3 pagesMultiple Choice Questions: d) d) R d) θ (1−c) M θ) increaseHelen ToNo ratings yet

- Unit 14 - Monetary & Fiscal Policy & EconomyDocument41 pagesUnit 14 - Monetary & Fiscal Policy & EconomySyeda WasqaNo ratings yet

- 7 EMU-Wang AoDocument22 pages7 EMU-Wang AoWang AoNo ratings yet

- Comparative Economic Planning: Ma. Kissiah L. BialenDocument7 pagesComparative Economic Planning: Ma. Kissiah L. BialenLexus CruzNo ratings yet

- Difference Between Monetary & Fiscal PolicyDocument15 pagesDifference Between Monetary & Fiscal Policybivek kumarNo ratings yet

- CH 17Document26 pagesCH 17Ngọc LinhNo ratings yet

Download as pdf or txt

You might also like

- Questions With Answers On is-LM ModelDocument12 pagesQuestions With Answers On is-LM ModelAkshay Singh67% (3)

- Business Cycles and Aggregate DemandDocument40 pagesBusiness Cycles and Aggregate DemandSnehal Joshi100% (1)

- Fiscal and Monetary Policy of GermanyDocument125 pagesFiscal and Monetary Policy of Germanyarpit vora100% (2)

- Introductory Macroeconomics ECON10003: Lecture 6: The Keynesian Model of The Economy IDocument24 pagesIntroductory Macroeconomics ECON10003: Lecture 6: The Keynesian Model of The Economy IImaweeb 77No ratings yet

- EC2B3 Topic 9 Lecture SlidesDocument40 pagesEC2B3 Topic 9 Lecture Slidescherryyu.nyNo ratings yet

- End Term Cheat SheetDocument2 pagesEnd Term Cheat SheetnupurNo ratings yet

- Lecture 13Document20 pagesLecture 13MaríaNo ratings yet

- EC2B3 Topic 8 Lecture SlidesDocument37 pagesEC2B3 Topic 8 Lecture Slidescherryyu.nyNo ratings yet

- ECO 302 Intermediate Macroeconomic Theory I: The IS Curve (Jones Chapter 11)Document45 pagesECO 302 Intermediate Macroeconomic Theory I: The IS Curve (Jones Chapter 11)Md SafiNo ratings yet

- Ch. 2Document22 pagesCh. 2suinyun16No ratings yet

- Example Example: (5.5) : Continuation of (5.4)Document22 pagesExample Example: (5.5) : Continuation of (5.4)KoyakuNo ratings yet

- 1.6 Savings and BorrowingDocument35 pages1.6 Savings and BorrowingAnh Quan NguyenNo ratings yet

- Unit 5: Long-Run Consequences of Stabilization PoliciesDocument81 pagesUnit 5: Long-Run Consequences of Stabilization PoliciesPriscilla SamaniegoNo ratings yet

- Week10 Monday SlidesDocument26 pagesWeek10 Monday Slidesnellyu761No ratings yet

- Inflation - Curbing InflationDocument11 pagesInflation - Curbing InflationMỹ HàNo ratings yet

- Homework 6 - AKDocument4 pagesHomework 6 - AKMaríaNo ratings yet

- Session 17 - Fiscal PolicyDocument54 pagesSession 17 - Fiscal PolicyLakshmi Harshitha mNo ratings yet

- Chapter 4 Fiscal PolicyDocument29 pagesChapter 4 Fiscal PolicyMinh HuỳnhNo ratings yet

- Week 2 - Economic and Industry Analysis 2023Document43 pagesWeek 2 - Economic and Industry Analysis 2023Katty MothaNo ratings yet

- Econ 112 Lecture 6Document23 pagesEcon 112 Lecture 6CHUA WEI JINNo ratings yet

- Macro5 Lecppt ch11Document88 pagesMacro5 Lecppt ch11이가빈[학생](국제대학 국제학과)No ratings yet

- Chapter 40 Macroeconomic Demand Side PoliciesDocument12 pagesChapter 40 Macroeconomic Demand Side Policiesmoots altNo ratings yet

- EC 102 Revisions Lectures - Macro - 2015Document54 pagesEC 102 Revisions Lectures - Macro - 2015TylerTangTengYangNo ratings yet

- Monetary & Fiscal PolicyDocument5 pagesMonetary & Fiscal PolicyAlya MaisarahNo ratings yet

- MECO121 UM S2024 Session18Document25 pagesMECO121 UM S2024 Session18rizwanf026No ratings yet

- Slides For Topic 4 - InflationDocument23 pagesSlides For Topic 4 - InflationNesma HusseinNo ratings yet

- Aggregate Demand - MacroDocument21 pagesAggregate Demand - MacroHaardik GandhiNo ratings yet

- CH 11 Lo - Fiscal - PolicyDocument28 pagesCH 11 Lo - Fiscal - Policytariku1234No ratings yet

- MECO121 UM S2024 Session17Document30 pagesMECO121 UM S2024 Session17rizwanf026No ratings yet

- Ch. 31-34Document66 pagesCh. 31-34Alaa DawoudNo ratings yet

- Lecture 5 - Cyclical InstabilityDocument66 pagesLecture 5 - Cyclical InstabilityTechno NowNo ratings yet

- Krugman Unit Four Modules 16 To 21Document76 pagesKrugman Unit Four Modules 16 To 21derengungorNo ratings yet

- The Consumption FunctionDocument21 pagesThe Consumption Functionsadhu124No ratings yet

- Economy SR 1Document34 pagesEconomy SR 1PriyanshNo ratings yet

- Final Fresentation GOVERNMENT DEBTDocument18 pagesFinal Fresentation GOVERNMENT DEBTIzba ShahzadNo ratings yet

- Shifts of The Curve: Price Level Money Supply ExogenousDocument28 pagesShifts of The Curve: Price Level Money Supply ExogenousKoyakuNo ratings yet

- Chapter 26-02.09.09Document54 pagesChapter 26-02.09.09af.rashedi79No ratings yet

- My Aggregate Demand & Aggregate Supply (Edited For Class)Document113 pagesMy Aggregate Demand & Aggregate Supply (Edited For Class)ShivamNo ratings yet

- CH3 Aggregate Demand and Aggregate SupplyDocument40 pagesCH3 Aggregate Demand and Aggregate SupplyTiviyaNo ratings yet

- Group 5 1 Slides Wide - MDDocument70 pagesGroup 5 1 Slides Wide - MDSumukh VasishtNo ratings yet

- Definition of Fiscal Policy: ADocument21 pagesDefinition of Fiscal Policy: Amanish9890No ratings yet

- Video Lecture 4.3 IS-LM-PC ModelDocument5 pagesVideo Lecture 4.3 IS-LM-PC ModelAndrás TímárNo ratings yet

- Lecture 4Document25 pagesLecture 4CHUA WEI JINNo ratings yet

- Macroeconomics - Keynesian ModelsDocument22 pagesMacroeconomics - Keynesian ModelsAlfa RydesterNo ratings yet

- Chapter 7 MMDocument44 pagesChapter 7 MMbusi.kg.tshNo ratings yet

- CH6 Fiscal Policy, Taxes and BudgetsDocument28 pagesCH6 Fiscal Policy, Taxes and BudgetsTiviyaNo ratings yet

- The Income Statement and Adjusting Entries: Financial Accounting - Lecture 2Document21 pagesThe Income Statement and Adjusting Entries: Financial Accounting - Lecture 2Peter Shang100% (1)

- CH 10 Lo - Economic - InstabilityDocument26 pagesCH 10 Lo - Economic - Instabilitytariku1234No ratings yet

- Figure 3.1: Consumption and Disposable IncomeDocument33 pagesFigure 3.1: Consumption and Disposable IncomeKoyakuNo ratings yet

- Global Economics: PGP: Shekhar TomarDocument38 pagesGlobal Economics: PGP: Shekhar TomarDivyang SaxenaNo ratings yet

- Chaopte r34 NotesDocument5 pagesChaopte r34 Noteschinsu6893No ratings yet

- 1 Economic Influences-Macroeconomic PoliciesDocument16 pages1 Economic Influences-Macroeconomic PoliciesNinjaTylerFortniteBlevins 2.0No ratings yet

- Monetary Policies During Excess Demand and Deficient DemandDocument38 pagesMonetary Policies During Excess Demand and Deficient DemandABIN THOMASNo ratings yet

- Business Cycles Week 6 29102023 035246pmDocument18 pagesBusiness Cycles Week 6 29102023 035246pmMuhammad SarmadNo ratings yet

- Money and InflationDocument29 pagesMoney and InflationBogdan BoldeaNo ratings yet

- FM03 Debt 0831Document68 pagesFM03 Debt 0831Kenneth KwokNo ratings yet

- Inflation and The Quantity Theory of MoneyDocument22 pagesInflation and The Quantity Theory of MoneyBình Nguyễn ĐăngNo ratings yet

- Week 11-14 - Chapters 22-23 - Fiscal and Monetary PoliciesDocument33 pagesWeek 11-14 - Chapters 22-23 - Fiscal and Monetary PoliciesOona NiallNo ratings yet

- Lecture 2 - National Income Accounting - PT 1 PDFDocument45 pagesLecture 2 - National Income Accounting - PT 1 PDFDavidNo ratings yet

- The Food Service Professional Guide to Controlling Liquor, Wine & Beverage CostsFrom EverandThe Food Service Professional Guide to Controlling Liquor, Wine & Beverage CostsNo ratings yet

- Bloomberg Ticker Codes EPRA-NAREITDocument4 pagesBloomberg Ticker Codes EPRA-NAREITps4scribdNo ratings yet

- Chapter 3Document49 pagesChapter 3Trang ĐoànNo ratings yet

- Practice MCQDocument6 pagesPractice MCQsaiNo ratings yet

- Kimberly Amadeo: Money SupplyDocument3 pagesKimberly Amadeo: Money SupplytawandaNo ratings yet

- CH 29Document36 pagesCH 29Robelen CallantaNo ratings yet

- Fiscal PolicyDocument21 pagesFiscal PolicycamilleNo ratings yet

- Mishkin Econ13e PPT 15Document31 pagesMishkin Econ13e PPT 15quynhle.31221021604No ratings yet

- Martinez Monetary Policy Vs Fiscal PolicyDocument18 pagesMartinez Monetary Policy Vs Fiscal Policyapi-273088531No ratings yet

- Course: Understanding Economic Policymaking by IE Business School Week-2: Fiscal Policy Tool QuizDocument6 pagesCourse: Understanding Economic Policymaking by IE Business School Week-2: Fiscal Policy Tool QuizSofia Yurina100% (1)

- EssayDocument5 pagesEssayJim_Tsao_4234No ratings yet

- Phillips CurveDocument5 pagesPhillips CurveAnkush PalNo ratings yet

- Chapter 31 - Parkin - PowerPointDocument15 pagesChapter 31 - Parkin - PowerPointUzair IsmailNo ratings yet

- Macroeconomic Policy in An Open Economy: EconomicsDocument26 pagesMacroeconomic Policy in An Open Economy: EconomicsAman PratikNo ratings yet

- CH - 9 - Income and Spending - Keynesian Multipliers PDFDocument18 pagesCH - 9 - Income and Spending - Keynesian Multipliers PDFHarmandeep Singh50% (2)

- Instruments of Moneytary PolicyDocument3 pagesInstruments of Moneytary PolicyJaydeep Paul100% (1)

- Mundell Fleming ModelDocument22 pagesMundell Fleming ModelDhruv BhandariNo ratings yet

- Principles of Macroeconomics IDocument3 pagesPrinciples of Macroeconomics IanushkaanandaniiiNo ratings yet

- The Gold Standard &Document20 pagesThe Gold Standard &Paavni SharmaNo ratings yet

- Keynesian and MonetaristDocument9 pagesKeynesian and MonetaristCeaserNo ratings yet

- Fed Rate Cut N ImplicationsDocument8 pagesFed Rate Cut N Implicationssplusk100% (1)

- Chapter 11 Dornbusch Fisher SolutionsDocument13 pagesChapter 11 Dornbusch Fisher Solutions22ech040No ratings yet

- MoneyDocument6 pagesMoneyritoja770No ratings yet

- Multiple Choice Questions: d) d) R d) θ (1−c) M θ) increaseDocument3 pagesMultiple Choice Questions: d) d) R d) θ (1−c) M θ) increaseHelen ToNo ratings yet

- Unit 14 - Monetary & Fiscal Policy & EconomyDocument41 pagesUnit 14 - Monetary & Fiscal Policy & EconomySyeda WasqaNo ratings yet

- 7 EMU-Wang AoDocument22 pages7 EMU-Wang AoWang AoNo ratings yet

- Comparative Economic Planning: Ma. Kissiah L. BialenDocument7 pagesComparative Economic Planning: Ma. Kissiah L. BialenLexus CruzNo ratings yet

- Difference Between Monetary & Fiscal PolicyDocument15 pagesDifference Between Monetary & Fiscal Policybivek kumarNo ratings yet

- CH 17Document26 pagesCH 17Ngọc LinhNo ratings yet