Download as pdf or txt

You might also like

- Case Indian River Citrus Company - Cap.budgetingDocument6 pagesCase Indian River Citrus Company - Cap.budgetingNipunSahrawat100% (1)

- Term Paper - Case Study: Ashok AmbashankerDocument7 pagesTerm Paper - Case Study: Ashok Ambashankercollinpaul0% (1)

- Required Us Supreme Court Case Matrix NameDocument3 pagesRequired Us Supreme Court Case Matrix NameellieNo ratings yet

- Practical Research 1 Quarter 1 - Module 20: Literature Review On SpotlightDocument9 pagesPractical Research 1 Quarter 1 - Module 20: Literature Review On SpotlightMark Allen Labasan100% (1)

- Bavadekar, T. (2020) - Importance of Proper Cost Management in Construction Industry. International Research Journal of Engineering and Technology.Document3 pagesBavadekar, T. (2020) - Importance of Proper Cost Management in Construction Industry. International Research Journal of Engineering and Technology.beast mickeyNo ratings yet

- Contracts' Performance Measurement in Czeck Const CompaniesDocument23 pagesContracts' Performance Measurement in Czeck Const CompaniesMohamed El-turkiNo ratings yet

- H.5 Practical Cost, Estimation in A Competitive EnvironmentDocument9 pagesH.5 Practical Cost, Estimation in A Competitive EnvironmentBTconcordNo ratings yet

- Factors Affecting Subcontracting StrategyDocument12 pagesFactors Affecting Subcontracting StrategyAbdulrahman NogsaneNo ratings yet

- EBQS3103 Measurement in Works Notes 1Document10 pagesEBQS3103 Measurement in Works Notes 1arif husainNo ratings yet

- Optimal Techniques For Cost Reduction and Control in Construction SitesDocument10 pagesOptimal Techniques For Cost Reduction and Control in Construction SitesAngelo VillalobosNo ratings yet

- An International Competitiveness Evaluation Model in The Global Construction IndustryDocument14 pagesAn International Competitiveness Evaluation Model in The Global Construction Industryzimbazimba75No ratings yet

- Ar2002-013-022 Eksteen and RosenbergDocument10 pagesAr2002-013-022 Eksteen and Rosenbergkabamba KundaNo ratings yet

- Control of Time Cost and Quality of Construction PDocument5 pagesControl of Time Cost and Quality of Construction PMuhammad Aulia RezaNo ratings yet

- Benchmarking Uk Government Procurement Performance in Construction ProjectsDocument9 pagesBenchmarking Uk Government Procurement Performance in Construction ProjectsmaazizNo ratings yet

- Dec - For Prob - Project Cost MGT ReviewDocument9 pagesDec - For Prob - Project Cost MGT Reviewwondwossen19chNo ratings yet

- Complexities of Cost Overrun in Construction ProjectsDocument4 pagesComplexities of Cost Overrun in Construction ProjectsInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- The Management of Construction CompanyDocument9 pagesThe Management of Construction CompanyRey Eduard Q. UmelNo ratings yet

- D31CF Toc TZ1-TZ2Document5 pagesD31CF Toc TZ1-TZ204122No ratings yet

- A Review of ® Nancial Ratio Tools For Predicting Contractor InsolvencyDocument11 pagesA Review of ® Nancial Ratio Tools For Predicting Contractor InsolvencyLuthfi'ahNo ratings yet

- Cost Management Strategy of Highway Engineering CoDocument6 pagesCost Management Strategy of Highway Engineering CoJawad AhmadNo ratings yet

- Li 2018 IOP Conf. Ser. Mater. Sci. Eng. 394 032057Document6 pagesLi 2018 IOP Conf. Ser. Mater. Sci. Eng. 394 032057melandro pabalanNo ratings yet

- Process of Pricing Tenders and Determining Profit MarginsDocument8 pagesProcess of Pricing Tenders and Determining Profit MarginsRajendra TharmakulasinghamNo ratings yet

- Cost MarkupDocument26 pagesCost Markupkedir salihNo ratings yet

- Buildings 10 00230 v4Document24 pagesBuildings 10 00230 v4Zakky AZNo ratings yet

- Study of Quality Assurance and Quality Management System in Multistroyed RCC BuildingDocument2 pagesStudy of Quality Assurance and Quality Management System in Multistroyed RCC BuildingEditor IJRITCCNo ratings yet

- 06_IJETMR18_A01_222Document8 pages06_IJETMR18_A01_222Melak tarkoNo ratings yet

- Rashid 2, 2018Document6 pagesRashid 2, 2018Cheng Ling YongNo ratings yet

- Kazaz, 2005 - Determination of Quality Level in Mass Housing Projects in TurkeyDocument8 pagesKazaz, 2005 - Determination of Quality Level in Mass Housing Projects in TurkeyDavid MartinezNo ratings yet

- Contractor Selection in The Housing Sector Using The Simple Multi-Attribute Rating TechniqueDocument6 pagesContractor Selection in The Housing Sector Using The Simple Multi-Attribute Rating TechniquehopetofindmyownwayNo ratings yet

- A Guide To Construction Cost Sources: What Can They Tell Us About Competitiveness?Document10 pagesA Guide To Construction Cost Sources: What Can They Tell Us About Competitiveness?julio_salas_59No ratings yet

- Rohit Agarwal (12000922028)Document7 pagesRohit Agarwal (12000922028)gokenox449No ratings yet

- Dissertation - An Analysis of Cost Control System in The Constructions Industry in DubaiDocument17 pagesDissertation - An Analysis of Cost Control System in The Constructions Industry in DubaiSds HarshanaNo ratings yet

- Cost Estimation Model of Prefabricated Construction For General Contractors Based On System DynamicsDocument18 pagesCost Estimation Model of Prefabricated Construction For General Contractors Based On System DynamicsAmadosi J. EmmanuelNo ratings yet

- Implementation of Fishbone DiagramDocument3 pagesImplementation of Fishbone DiagramabelNo ratings yet

- Benchmarking and Improving Construction ProductivityDocument10 pagesBenchmarking and Improving Construction ProductivityTerrance OngNo ratings yet

- Indus - Overhead Cost - Swati S PatilDocument6 pagesIndus - Overhead Cost - Swati S PatilTJPRC PublicationsNo ratings yet

- TQM ReportDocument3 pagesTQM ReportTom OwtramNo ratings yet

- 9159-Article Text PDF-33276-3-10-20180129Document11 pages9159-Article Text PDF-33276-3-10-20180129Aishwarya SwamyNo ratings yet

- Performance Measurement Systems in Construction: Roshana Takim, Akintola Akintoye and John KellyDocument10 pagesPerformance Measurement Systems in Construction: Roshana Takim, Akintola Akintoye and John KellyAsitha RathnayakeNo ratings yet

- System Dynamics Modeling Approach To QuaDocument13 pagesSystem Dynamics Modeling Approach To QuaBrunoNo ratings yet

- Paper FormatDocument1 pagePaper FormatGuts GriffithNo ratings yet

- BCME405 Learning Trigger 1 - Lachy FentonDocument16 pagesBCME405 Learning Trigger 1 - Lachy FentonLachy FentonNo ratings yet

- 1 s2.0 S2590123022002663 MainDocument14 pages1 s2.0 S2590123022002663 MainLaura StefaniaNo ratings yet

- A1 - Critical Review of The Causes of Cost Overrun in Construction Industries in Developing CountriesDocument10 pagesA1 - Critical Review of The Causes of Cost Overrun in Construction Industries in Developing CountriesTong Yi NieNo ratings yet

- Scorecard For Subcontractor Performance AppraisalDocument9 pagesScorecard For Subcontractor Performance Appraisalluis5107No ratings yet

- MarkupDocument6 pagesMarkupBTconcordNo ratings yet

- Benefit Quantification of Interoperability in Coordinate MetrologyDocument4 pagesBenefit Quantification of Interoperability in Coordinate MetrologyCelso Vito Gewehr JuniorNo ratings yet

- An Empirical Case Study and Approach On TQM in A SDocument12 pagesAn Empirical Case Study and Approach On TQM in A Sgladiator 033No ratings yet

- 3072-Article Text-6644-5-10-20181011Document17 pages3072-Article Text-6644-5-10-20181011Ayesha MuniraNo ratings yet

- Articulo Cientifico 2Document14 pagesArticulo Cientifico 2humberto bordaNo ratings yet

- 17 Ramalingam2020Document14 pages17 Ramalingam2020Dhika AdhityaNo ratings yet

- (Artigo) - An Analysis of Bidding Strategy, Project Performance and Company Performance Relationship in ConstructionDocument8 pages(Artigo) - An Analysis of Bidding Strategy, Project Performance and Company Performance Relationship in ConstructionNuno HenriquesNo ratings yet

- ICRA Rating Methodology: Construction CompaniesDocument11 pagesICRA Rating Methodology: Construction Companieshesham zakiNo ratings yet

- The Integration of Activity Based Costing and Enterprise Modeling For Reengineering PurposesDocument12 pagesThe Integration of Activity Based Costing and Enterprise Modeling For Reengineering PurposesLivia MarsaNo ratings yet

- Study On Application of Value Engineering On Construction DesignDocument4 pagesStudy On Application of Value Engineering On Construction DesignAhmed JeddaweeNo ratings yet

- Chen 2021 J. Phys. Conf. Ser. 1881 022036Document6 pagesChen 2021 J. Phys. Conf. Ser. 1881 022036veronica3yuNo ratings yet

- An Assessment of Factors Affecting The Cost and Time Performance of Subcontractors Vol.026Document17 pagesAn Assessment of Factors Affecting The Cost and Time Performance of Subcontractors Vol.026ADEDAYO JEREMIAH ADEYEKUNNo ratings yet

- The Management of Construction Company Overhead CostsDocument9 pagesThe Management of Construction Company Overhead CostsAlfred De Vera GabuatNo ratings yet

- Factors Affecting The Accuracy of Construction Project Cost Estimation in EgyptDocument17 pagesFactors Affecting The Accuracy of Construction Project Cost Estimation in EgyptPSNo ratings yet

- 6885-Article Text-16105-1-10-20181203Document11 pages6885-Article Text-16105-1-10-20181203Jeedi SrinuNo ratings yet

- Factors Affecting The Cost of Building Work - An OverviewDocument22 pagesFactors Affecting The Cost of Building Work - An OverviewColin100% (1)

- Pts B.ing 21-22Document5 pagesPts B.ing 21-22YantisYtNo ratings yet

- LS2005209-DeEP Assignment 1Document6 pagesLS2005209-DeEP Assignment 1Thanhalul Alam DipNo ratings yet

- 01HDM 4introduction2008 10 22Document51 pages01HDM 4introduction2008 10 22Alberto Enrique Nash BaezNo ratings yet

- How To Use Your EBT CardDocument1 pageHow To Use Your EBT CardnoxinqwertyNo ratings yet

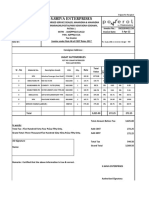

- S.Shiva Enterprises: Jagat AutomobilesDocument2 pagesS.Shiva Enterprises: Jagat AutomobilesS.SHIVA ENTERPRISESNo ratings yet

- WEB Proof of Authorization Industry PracticesDocument4 pagesWEB Proof of Authorization Industry PracticesAnh Tuấn Nguyễn CôngNo ratings yet

- Criticism of Human Geography PDFDocument15 pagesCriticism of Human Geography PDFtwiceokNo ratings yet

- Full Download PDF of (Ebook PDF) Forensic Accounting and Fraud Examination 2nd Edition All ChapterDocument43 pagesFull Download PDF of (Ebook PDF) Forensic Accounting and Fraud Examination 2nd Edition All Chapterguurhawk9100% (7)

- Apl Apollo Annual Report 2017-18Document216 pagesApl Apollo Annual Report 2017-18Nitin PatidarNo ratings yet

- Active and Passive Voice DiscussionDocument11 pagesActive and Passive Voice DiscussionRol ParochaNo ratings yet

- RMFB5 Schedule of Yuletide Break Updated December 17 2022 BDocument17 pagesRMFB5 Schedule of Yuletide Break Updated December 17 2022 Bjohn paul AbraganNo ratings yet

- Edward Broughton v. Russell A. Courtney, Donald A. D'Lugos, 861 F.2d 639, 11th Cir. (1988)Document8 pagesEdward Broughton v. Russell A. Courtney, Donald A. D'Lugos, 861 F.2d 639, 11th Cir. (1988)Scribd Government DocsNo ratings yet

- IAP GuidebookDocument21 pagesIAP Guidebooksuheena.CNo ratings yet

- Case 3-1 Prudent Provisions For PensionsDocument2 pagesCase 3-1 Prudent Provisions For PensionspamelaNo ratings yet

- Bhakti - TheologiansDocument9 pagesBhakti - TheologiansHiviNo ratings yet

- Lumbini Pradesh - WikipediaDocument16 pagesLumbini Pradesh - WikipediaPramish PMNo ratings yet

- HSS UFC Lesson 3Document3 pagesHSS UFC Lesson 3latifa hachemiNo ratings yet

- Newes InfoDocument14 pagesNewes InfoLouina YnciertoNo ratings yet

- FS Q2 Module 2Document10 pagesFS Q2 Module 2Ahrcelie FranciscoNo ratings yet

- A Quick Guide To The Employment Rights Act: OcumentationDocument4 pagesA Quick Guide To The Employment Rights Act: OcumentationGeorgia SimmsNo ratings yet

- UP08 Labor Law 01Document56 pagesUP08 Labor Law 01jojitus100% (2)

- Florida House Bill ScribDocument4 pagesFlorida House Bill ScribJoe HoNo ratings yet

- Hindu Marriage ActDocument13 pagesHindu Marriage ActAshok GautamNo ratings yet

- Mr. Ranjit Kumar Paswan PDFDocument27 pagesMr. Ranjit Kumar Paswan PDFAysha SafrinaNo ratings yet

- Quita v. Court of AppealsDocument6 pagesQuita v. Court of AppealsShairaCamilleGarciaNo ratings yet

- CV Sample FormatDocument6 pagesCV Sample FormatVijay MindfireNo ratings yet

- Women Entrepreneurship in Karnataka - An: Chapter - 5Document33 pagesWomen Entrepreneurship in Karnataka - An: Chapter - 5SreekanthNo ratings yet