Download as pdf or txt

You might also like

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- 13.000 Grupos DivulgaçãoDocument92 pages13.000 Grupos Divulgaçãofranciscojotta4100% (1)

- Chapter 2.1 The Logic of The Budget ProcessDocument20 pagesChapter 2.1 The Logic of The Budget ProcessNeal MicutuanNo ratings yet

- Examiner Comments-Summer 2015Document6 pagesExaminer Comments-Summer 2015Mahendar BhojwaniNo ratings yet

- The Institute of Chartered Accountants of Pakistan Examiners' Comments Subject SessionDocument6 pagesThe Institute of Chartered Accountants of Pakistan Examiners' Comments Subject SessionGhulam Murtaza KoraiNo ratings yet

- Examiner Comments-Summer 2019Document4 pagesExaminer Comments-Summer 2019Mahendar BhojwaniNo ratings yet

- Examiner Comments-Summer 2013Document4 pagesExaminer Comments-Summer 2013Mahendar BhojwaniNo ratings yet

- Examiner's Report: F6 Taxation (UK) December 2010Document3 pagesExaminer's Report: F6 Taxation (UK) December 2010yorcpl200No ratings yet

- Caf 6 Tax Spring 2019 2Document5 pagesCaf 6 Tax Spring 2019 2Abdullah QureshiNo ratings yet

- Examiner Comments-Summer 2011Document3 pagesExaminer Comments-Summer 2011Mahendar BhojwaniNo ratings yet

- Examiner Comments-Summer 2018Document7 pagesExaminer Comments-Summer 2018Mahendar BhojwaniNo ratings yet

- Examiner Comments-Summer 2012Document4 pagesExaminer Comments-Summer 2012Mahendar BhojwaniNo ratings yet

- December 2015 DipIFR - Question - AnswerDocument20 pagesDecember 2015 DipIFR - Question - Answerksaqib89No ratings yet

- Examiner's Report: F6 Taxation (UK) December 2011Document3 pagesExaminer's Report: F6 Taxation (UK) December 2011Zeeshan BhattiNo ratings yet

- The Institute of Chartered Accountants of PakistanDocument3 pagesThe Institute of Chartered Accountants of PakistanShamail AsimNo ratings yet

- Principle of TaxationDocument6 pagesPrinciple of TaxationKhurram ShahzadNo ratings yet

- Caf 2 Tax Spring 2022Document4 pagesCaf 2 Tax Spring 2022khanmobeen2023No ratings yet

- 1210 DipifrDocument3 pages1210 DipifrkazimkorogluNo ratings yet

- Caf 2 Tax Autumn 2022Document4 pagesCaf 2 Tax Autumn 2022M AHMAD MAQBOOLNo ratings yet

- Examiner Report - ASE20104 - January 2019Document13 pagesExaminer Report - ASE20104 - January 2019Aung Zaw Htwe100% (1)

- © The Institute of Chartered Accountants of IndiaDocument8 pages© The Institute of Chartered Accountants of IndiaArnav BarmanNo ratings yet

- 18517pcc Sugg Paper Nov09 Commentsgp2 PDFDocument7 pages18517pcc Sugg Paper Nov09 Commentsgp2 PDFGaurang AgarwalNo ratings yet

- TX VNM J21 Examiner's ReportDocument11 pagesTX VNM J21 Examiner's ReportĐạt LêNo ratings yet

- 0611 DipifrDocument3 pages0611 DipifrkazimkorogluNo ratings yet

- ACCA F6rom-Examreport-J12Document3 pagesACCA F6rom-Examreport-J12georgetacaprarescuNo ratings yet

- ACCA F6rom-Examreport-D12Document4 pagesACCA F6rom-Examreport-D12georgetacaprarescuNo ratings yet

- 1211 DipifrDocument4 pages1211 DipifrkazimkorogluNo ratings yet

- ASE20104 - Examiner Report - November 2018Document14 pagesASE20104 - Examiner Report - November 2018Aung Zaw HtweNo ratings yet

- Qualification Programme Examination Panelists' ReportDocument4 pagesQualification Programme Examination Panelists' ReportVong Yu Kwan EdwinNo ratings yet

- AccountingDocument8 pagesAccountingBilal MustafaNo ratings yet

- Taxation South Africa (TX Zaf) June 2022 Examiner's ReportDocument9 pagesTaxation South Africa (TX Zaf) June 2022 Examiner's ReportwaseNo ratings yet

- Taxation Examiners Report 2014septemberDocument7 pagesTaxation Examiners Report 2014septemberKen ChiaNo ratings yet

- Advanced Taxation 3.3 August 2022Document26 pagesAdvanced Taxation 3.3 August 2022Obed AsamoahNo ratings yet

- ACCA F7 Examiner's Report 15Document5 pagesACCA F7 Examiner's Report 15kevior2No ratings yet

- FR Examreport June20Document10 pagesFR Examreport June20kokoNo ratings yet

- Examiner's Report: F7 Financial Reporting December 2012Document6 pagesExaminer's Report: F7 Financial Reporting December 2012Selva Bavani SelwaduraiNo ratings yet

- Examiner's Report: June 2012Document3 pagesExaminer's Report: June 2012SherryKiuNo ratings yet

- TX RUS D20 Examiner's ReportDocument9 pagesTX RUS D20 Examiner's ReportErik NguyenNo ratings yet

- Advanced Level Accounting 600102 Examiners Report November 2022Document3 pagesAdvanced Level Accounting 600102 Examiners Report November 2022jayapriscilla1No ratings yet

- The Institute of Chartered Accountants of PakistanDocument4 pagesThe Institute of Chartered Accountants of PakistanANo ratings yet

- CAPEJune2012Accounting SRDocument15 pagesCAPEJune2012Accounting SRChrisana LawrenceNo ratings yet

- CFAP 1 AAFR Winter 2020Document2 pagesCFAP 1 AAFR Winter 2020ANo ratings yet

- The Institute of Chartered Accountants of PakistanDocument6 pagesThe Institute of Chartered Accountants of PakistanWajahat GhafoorNo ratings yet

- Examiner Report ASE20104 January 2018Document22 pagesExaminer Report ASE20104 January 2018Aung Zaw HtweNo ratings yet

- Dip IFR Examiner ReportDocument11 pagesDip IFR Examiner Reportluckyjulie567No ratings yet

- FM MJ20 Detailed CommentaryDocument4 pagesFM MJ20 Detailed CommentaryleylaNo ratings yet

- Examiner Report ASE20104 Sept 18Document18 pagesExaminer Report ASE20104 Sept 18Aung Zaw HtweNo ratings yet

- PKN 1209 f6Document4 pagesPKN 1209 f6Farhan HasanNo ratings yet

- The Institute of Chartered Accountants of PakistanDocument2 pagesThe Institute of Chartered Accountants of PakistanAqib SheikhNo ratings yet

- 2000 Economics Candidates' PerformanceDocument4 pages2000 Economics Candidates' PerformanceKathy WongNo ratings yet

- Pearson LCCI Certificate in Accounting (VRQ) Level 3Document20 pagesPearson LCCI Certificate in Accounting (VRQ) Level 3Aung Zaw HtweNo ratings yet

- Institute and Faculty of Actuaries: Subject CT2 - Finance and Financial Reporting Core TechnicalDocument9 pagesInstitute and Faculty of Actuaries: Subject CT2 - Finance and Financial Reporting Core TechnicalPatrick MugoNo ratings yet

- Examiner Report ASE20104 July 2018Document22 pagesExaminer Report ASE20104 July 2018Aung Zaw HtweNo ratings yet

- Examiners' Report: T10 Managing Finances June 2009Document3 pagesExaminers' Report: T10 Managing Finances June 2009leanhvu13No ratings yet

- Caf 4 Blw Spring 2020Document6 pagesCaf 4 Blw Spring 2020Noor AhmedNo ratings yet

- Pearson LCCI Certificate in Accounting (VRQ) Level 3Document22 pagesPearson LCCI Certificate in Accounting (VRQ) Level 3Aung Zaw HtweNo ratings yet

- Qualification Programme Examination Panelists' Report Module A - Financial Reporting (December 2011 Session)Document4 pagesQualification Programme Examination Panelists' Report Module A - Financial Reporting (December 2011 Session)Vong Yu Kwan EdwinNo ratings yet

- Financial Accounting March 2009 Marks PlanDocument14 pagesFinancial Accounting March 2009 Marks Plankarlr9No ratings yet

- ACC 103 P1 ExamDocument7 pagesACC 103 P1 Exammkrisnaharq99No ratings yet

- Principles of Accounts: Paper 7110/01 Multiple ChoiceDocument5 pagesPrinciples of Accounts: Paper 7110/01 Multiple Choicemstudy123456No ratings yet

- Dipifr Examiner's Report June 2022Document11 pagesDipifr Examiner's Report June 2022Kareem KhaledNo ratings yet

- Deped - Zamboanga Del Norte Division Summary of Cash Disbursement Register Reported Month - June, 2019 Salug 1 DistrictDocument2 pagesDeped - Zamboanga Del Norte Division Summary of Cash Disbursement Register Reported Month - June, 2019 Salug 1 DistrictRONIL APAOPEDROTESNo ratings yet

- Tax Invoice: Excitel Broadband Pvt. LTDDocument1 pageTax Invoice: Excitel Broadband Pvt. LTDMittal GalaxyNo ratings yet

- Jess SSG Ass 1Document10 pagesJess SSG Ass 1Jaydine Jenny SonnekusNo ratings yet

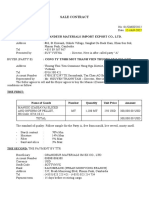

- Sale Contract:: Cong Ty TNHH Mot Thanh Vien Thuong Mai Gia LocDocument2 pagesSale Contract:: Cong Ty TNHH Mot Thanh Vien Thuong Mai Gia LocNiron CompanyNo ratings yet

- New FGE Chapter I and IIDocument18 pagesNew FGE Chapter I and IImubarek kemalNo ratings yet

- Hubli DatabaseDocument20 pagesHubli Databaseshweta_gupta0718444No ratings yet

- Caltex V COA DigestDocument3 pagesCaltex V COA DigestCarlito HilvanoNo ratings yet

- 22 1184 ResolutionDocument3 pages22 1184 ResolutionTMJ4 NewsNo ratings yet

- M25 DesignDocument4 pagesM25 DesignAmit KumarNo ratings yet

- Lecture 3 - National Income Accounting PDFDocument20 pagesLecture 3 - National Income Accounting PDFDavidNo ratings yet

- Topic 1-Overview of Business To Business MarketingDocument11 pagesTopic 1-Overview of Business To Business MarketinggregNo ratings yet

- Dung Sonang RohangkuDocument3 pagesDung Sonang RohangkuRichoNo ratings yet

- 4q22 Investor Presentaion February 2023Document34 pages4q22 Investor Presentaion February 2023mukeshindpatiNo ratings yet

- Portfolio ReconstructionDocument2 pagesPortfolio ReconstructionOsmaan GóÑÍNo ratings yet

- Managerial Economics 8th Edition Samuelson Test BankDocument22 pagesManagerial Economics 8th Edition Samuelson Test Bankstarfishcomposero5cglt100% (31)

- Fiscal Policy and Public Finace in IndiaDocument3 pagesFiscal Policy and Public Finace in IndiaMADHU SUDANNo ratings yet

- Eco261 Banking IndustryDocument25 pagesEco261 Banking IndustryAHMAD FILZA ADIRANo ratings yet

- International BusinessDocument13 pagesInternational BusinessPhạm Ngọc AnhNo ratings yet

- Essay On The Influence of Microfinance On The Business Development of Merchants in The San José International Market in The City of JuliacaDocument4 pagesEssay On The Influence of Microfinance On The Business Development of Merchants in The San José International Market in The City of JuliacaEvelyn CastilloNo ratings yet

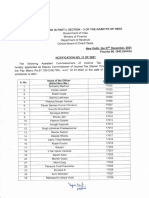

- To Be Published in Part-I, Section - 2 of The Gazette of IndiaDocument6 pagesTo Be Published in Part-I, Section - 2 of The Gazette of Indiajudicial teamworkNo ratings yet

- The Vampire Economy - Doing Business Under FascismDocument288 pagesThe Vampire Economy - Doing Business Under FascismSouthern FuturistNo ratings yet

- Goods and Services: Super Teacher WorksheetsDocument2 pagesGoods and Services: Super Teacher WorksheetsJorge AlvarezNo ratings yet

- Final Module in Ss 13Document13 pagesFinal Module in Ss 13marvsNo ratings yet

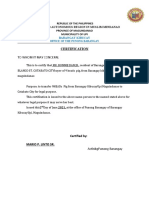

- Certification: To Whom It May ConcernDocument4 pagesCertification: To Whom It May ConcernMichael Carinal MontoyaNo ratings yet

- Foreign Exchange: The Structure and Operation of The FX MarketDocument44 pagesForeign Exchange: The Structure and Operation of The FX MarketThu NguyenNo ratings yet

- IIF SecuritiesDocument296 pagesIIF SecuritiesReTHINK INDIANo ratings yet

- Materi Pengenalan Akuntansi DasarDocument30 pagesMateri Pengenalan Akuntansi DasarsaifulNo ratings yet