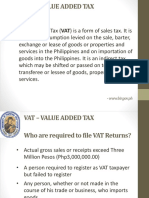

VAT - Is A Tax On The Value Added by Every Seller To The Purchase Price or

VAT - Is A Tax On The Value Added by Every Seller To The Purchase Price or

You might also like

- Business and Transfer Taxation by BanggawanDocument38 pagesBusiness and Transfer Taxation by BanggawanBryan Orbina Fruto67% (24)

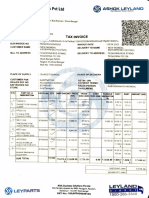

- Suzuki InvoiceDocument1 pageSuzuki InvoiceMUKESH KUMAR0% (3)

- Value Added Tax in The PhilippinesDocument14 pagesValue Added Tax in The Philippinesagathe laurent100% (1)

- Intero Enterprises: Total Value 69,502.00Document1 pageIntero Enterprises: Total Value 69,502.00Ashish AgarwalNo ratings yet

- Mamalateo Part 1 VATDocument12 pagesMamalateo Part 1 VATPeterNo ratings yet

- SlideshowDocument37 pagesSlideshowBhavesh AgrawalNo ratings yet

- Module 3 - Value Added TaxDocument113 pagesModule 3 - Value Added TaxAllan C. MarquezNo ratings yet

- WWW - Bir.gov - PHDocument4 pagesWWW - Bir.gov - PHRoy Amigo Jr.No ratings yet

- Value-Added Tax PDFDocument118 pagesValue-Added Tax PDFRazel MhinNo ratings yet

- Tax Ii - Value Added Tax: APRIL 27, 2018Document82 pagesTax Ii - Value Added Tax: APRIL 27, 2018Ronald VillanuevaNo ratings yet

- TAXATION - Value-Added TaxDocument10 pagesTAXATION - Value-Added TaxJohn Mahatma Agripa100% (2)

- Value Added TaxDocument9 pagesValue Added TaxĴõ ĔĺNo ratings yet

- Case: Cir V PLDTDocument29 pagesCase: Cir V PLDTJaymee Andomang Os-agNo ratings yet

- Lecture VAT With ExercisesDocument82 pagesLecture VAT With ExercisesAko C JamzNo ratings yet

- Vat PDFDocument81 pagesVat PDFAudrey DeguzmanNo ratings yet

- Value Added TaxationDocument76 pagesValue Added Taxationxz wyNo ratings yet

- VAT ReportDocument32 pagesVAT ReportNoel Christopher G. BellezaNo ratings yet

- Unit 6: Value Added Tax (Proclamation 285/2002 Regulation 79/2002 Proclamation 609/2008)Document23 pagesUnit 6: Value Added Tax (Proclamation 285/2002 Regulation 79/2002 Proclamation 609/2008)Bizu AtnafuNo ratings yet

- ALL ABOUT VALUE ADDED TAX - Mamalateo 2014POWERMAXDocument37 pagesALL ABOUT VALUE ADDED TAX - Mamalateo 2014POWERMAXjohn apostolNo ratings yet

- A. VatDocument5 pagesA. VatKaye L. Dela CruzNo ratings yet

- Tax 2 Notes Finals 4Document36 pagesTax 2 Notes Finals 4Boom ManuelNo ratings yet

- Gimenez Jose Mari CDocument14 pagesGimenez Jose Mari CMari Calica GimenezNo ratings yet

- Business TaxDocument33 pagesBusiness TaxKiro ParafrostNo ratings yet

- Vat System and OptDocument15 pagesVat System and Optlyra21No ratings yet

- VatDocument50 pagesVatnikolaevnavalentinaNo ratings yet

- Comprehensive VAT TAXATION (3!31!14)Document166 pagesComprehensive VAT TAXATION (3!31!14)dereckriveraNo ratings yet

- VATPT For PicpaDocument73 pagesVATPT For PicpaJoy Superales SalaoNo ratings yet

- Business TaxesDocument100 pagesBusiness Taxeslynne tahilNo ratings yet

- VALUE ADDED TAX Goods Properties and ServicesDocument65 pagesVALUE ADDED TAX Goods Properties and ServicesPrincess LimNo ratings yet

- Vat On Sales of Goods or PropertiesDocument10 pagesVat On Sales of Goods or Propertiesgoerginamarquez100% (1)

- VAT Casasola NotesDocument7 pagesVAT Casasola NotesCharm AgripaNo ratings yet

- VAT Powerpoint PDFDocument202 pagesVAT Powerpoint PDFRuchie EtolleNo ratings yet

- Accounting For Indirect TaxesDocument40 pagesAccounting For Indirect TaxesSabaa if100% (1)

- Value Added Tax - VatDocument37 pagesValue Added Tax - VatTimoth MbwiloNo ratings yet

- National Taxation System - RamosDocument10 pagesNational Taxation System - RamosAldrich RamosNo ratings yet

- National Taxation System - RamosDocument10 pagesNational Taxation System - RamosAldrich RamosNo ratings yet

- Notes On VATDocument15 pagesNotes On VATErnest Benz Sabella DavilaNo ratings yet

- Value-Added Tax (VAT) Is A Tax On Consumption Levied On The Sale, Barter, Exchange or LeaseDocument27 pagesValue-Added Tax (VAT) Is A Tax On Consumption Levied On The Sale, Barter, Exchange or LeaseDon CabasiNo ratings yet

- VAT Questions For Professional Stage Knowledge LevelDocument14 pagesVAT Questions For Professional Stage Knowledge LevelFahimaAkterNo ratings yet

- Vat IiDocument19 pagesVat IiPCNo ratings yet

- Business TaxDocument34 pagesBusiness Taxprecy.calusaNo ratings yet

- 8VATDocument70 pages8VATNoelNo ratings yet

- Notes On Vat On Importation Feb 09 2023Document2 pagesNotes On Vat On Importation Feb 09 2023barneyaguilar8732No ratings yet

- VatDocument70 pagesVatPETERWILLE CHUANo ratings yet

- Value Added Tax (Cap 476)Document15 pagesValue Added Tax (Cap 476)Triila manillaNo ratings yet

- Taxn03b Vat IntroDocument20 pagesTaxn03b Vat IntroTrishamae legaspiNo ratings yet

- Export Sale of Goods (Sec. 106 (A) (2) (B) ) : Effectively Zero-Rated SalesDocument13 pagesExport Sale of Goods (Sec. 106 (A) (2) (B) ) : Effectively Zero-Rated SalesTricia Rozl PimentelNo ratings yet

- Percentage Tax in The PhilippinesDocument3 pagesPercentage Tax in The PhilippinesfrazieNo ratings yet

- 1 Basics of Value Added TaxDocument58 pages1 Basics of Value Added TaxHazel Andrea Garduque LopezNo ratings yet

- Business TaxesDocument51 pagesBusiness TaxesLuna CakesNo ratings yet

- Notes in Value Added TaxDocument52 pagesNotes in Value Added Taxedelyn roncalesNo ratings yet

- Tax and Basic Common TaxesDocument13 pagesTax and Basic Common TaxesDENGDENG HUANGNo ratings yet

- Business & Transfer Taxation: Rex B. Banggawan, Cpa, MbaDocument38 pagesBusiness & Transfer Taxation: Rex B. Banggawan, Cpa, Mbajustine reine cornicoNo ratings yet

- Taxation Report2Document22 pagesTaxation Report2Ritchelyn ArbonNo ratings yet

- VAT AnnotatedDocument46 pagesVAT AnnotatedDr SafaNo ratings yet

- Tax UpdatesDocument19 pagesTax UpdatesYeoh MaeNo ratings yet

- VAT Concepts Tax 321Document28 pagesVAT Concepts Tax 321justineNo ratings yet

- Comprehensive VAT TaxationDocument172 pagesComprehensive VAT TaxationIan JameroNo ratings yet

- Business Taxation 2 Lesson 1Document5 pagesBusiness Taxation 2 Lesson 1Darlyn Dalida San PedroNo ratings yet

- Tax - Vat GuidenotesDocument13 pagesTax - Vat GuidenotesNardz AndananNo ratings yet

- Very Awkward Tax: A bite-size guide to VAT for small businessFrom EverandVery Awkward Tax: A bite-size guide to VAT for small businessNo ratings yet

- Affidavit of Contractor License and BondingDocument2 pagesAffidavit of Contractor License and BondingfirsttenorNo ratings yet

- RCM On Residential DwellingDocument5 pagesRCM On Residential Dwellingashok babuNo ratings yet

- FORM47Document2 pagesFORM47TMRCHS TMRCHSNo ratings yet

- TheMomsCo Invoice 1658466994-76Document1 pageTheMomsCo Invoice 1658466994-76Aravind KrishNo ratings yet

- Qi0243 - Amnpn5168p - 2022-23 - Fy 2022 - 2023Document9 pagesQi0243 - Amnpn5168p - 2022-23 - Fy 2022 - 2023Dharma kurraNo ratings yet

- Salary Slip MainDocument1 pageSalary Slip MainVineetBaliyan100% (1)

- Destruction FormDocument2 pagesDestruction FormHanabishi RekkaNo ratings yet

- July 2022Document6 pagesJuly 2022Alexis sanchesNo ratings yet

- 3 - 2551442 - Salary - Illustration - 7 - 19 - 2022 9 - 16 - 28 PMDocument1 page3 - 2551442 - Salary - Illustration - 7 - 19 - 2022 9 - 16 - 28 PMShauryaNo ratings yet

- Accra V CA G.R. No. 96322 December 20, 1991Document2 pagesAccra V CA G.R. No. 96322 December 20, 1991Felicia AllenNo ratings yet

- SummaryDocument2 pagesSummaryASWIN.M.MNo ratings yet

- 200 ReceivedDocument1 page200 ReceivedMANI BHARATHINo ratings yet

- 1081 Supporting BillDocument2 pages1081 Supporting BillAshirwad BanerjeeNo ratings yet

- Air Canada v. CIR - Taxation Law - DebtDocument3 pagesAir Canada v. CIR - Taxation Law - DebtMichael Villalon100% (1)

- Mepco Online Billl PDFDocument1 pageMepco Online Billl PDFArslanNo ratings yet

- IDBI Bank LTD.: Application Print E-Receipt Print Tax InvoiceDocument1 pageIDBI Bank LTD.: Application Print E-Receipt Print Tax InvoicePratik DalwadiNo ratings yet

- #60 CIR vs. TMX SalesDocument2 pages#60 CIR vs. TMX SalesJan Rhoneil SantillanaNo ratings yet

- Presentation On Income TaxDocument9 pagesPresentation On Income TaxUnnati GuptaNo ratings yet

- E-Payslip Advice: Eco Green City SDN BHDDocument1 pageE-Payslip Advice: Eco Green City SDN BHDNur Jannah Marwa HamdanNo ratings yet

- UDA Avenue - Employee Self ServiceDocument1 pageUDA Avenue - Employee Self ServiceAliffNo ratings yet

- Od429286320133715100 1Document1 pageOd429286320133715100 1ANDREW CENANo ratings yet

- InvoiceDocument2 pagesInvoiceRK userNo ratings yet

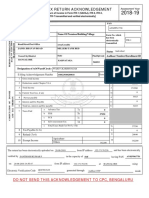

- Indian Income Tax Return Acknowledgement: Name of Premises/Building/VillageDocument1 pageIndian Income Tax Return Acknowledgement: Name of Premises/Building/Villagesanthosh kumarNo ratings yet

- Sample IRSTax Return TranscriptDocument6 pagesSample IRSTax Return TranscriptnowayNo ratings yet

- BS Pack 3 Flat CAP 20 - BSC20: Mushak: 6.3Document1 pageBS Pack 3 Flat CAP 20 - BSC20: Mushak: 6.3Onek KothaNo ratings yet

- Notes Class XDocument2 pagesNotes Class XmailinspectoryadavNo ratings yet

- Flipkart izTDLqDhhUGmP4d9CTVuPGDocument79 pagesFlipkart izTDLqDhhUGmP4d9CTVuPGAI TOOLS FOR BUSINESSNo ratings yet

- Assignment 1Document4 pagesAssignment 111dylan97No ratings yet

Download as docx, pdf, or txt

You might also like

- Business and Transfer Taxation by BanggawanDocument38 pagesBusiness and Transfer Taxation by BanggawanBryan Orbina Fruto67% (24)

- Suzuki InvoiceDocument1 pageSuzuki InvoiceMUKESH KUMAR0% (3)

- Value Added Tax in The PhilippinesDocument14 pagesValue Added Tax in The Philippinesagathe laurent100% (1)

- Intero Enterprises: Total Value 69,502.00Document1 pageIntero Enterprises: Total Value 69,502.00Ashish AgarwalNo ratings yet

- Mamalateo Part 1 VATDocument12 pagesMamalateo Part 1 VATPeterNo ratings yet

- SlideshowDocument37 pagesSlideshowBhavesh AgrawalNo ratings yet

- Module 3 - Value Added TaxDocument113 pagesModule 3 - Value Added TaxAllan C. MarquezNo ratings yet

- WWW - Bir.gov - PHDocument4 pagesWWW - Bir.gov - PHRoy Amigo Jr.No ratings yet

- Value-Added Tax PDFDocument118 pagesValue-Added Tax PDFRazel MhinNo ratings yet

- Tax Ii - Value Added Tax: APRIL 27, 2018Document82 pagesTax Ii - Value Added Tax: APRIL 27, 2018Ronald VillanuevaNo ratings yet

- TAXATION - Value-Added TaxDocument10 pagesTAXATION - Value-Added TaxJohn Mahatma Agripa100% (2)

- Value Added TaxDocument9 pagesValue Added TaxĴõ ĔĺNo ratings yet

- Case: Cir V PLDTDocument29 pagesCase: Cir V PLDTJaymee Andomang Os-agNo ratings yet

- Lecture VAT With ExercisesDocument82 pagesLecture VAT With ExercisesAko C JamzNo ratings yet

- Vat PDFDocument81 pagesVat PDFAudrey DeguzmanNo ratings yet

- Value Added TaxationDocument76 pagesValue Added Taxationxz wyNo ratings yet

- VAT ReportDocument32 pagesVAT ReportNoel Christopher G. BellezaNo ratings yet

- Unit 6: Value Added Tax (Proclamation 285/2002 Regulation 79/2002 Proclamation 609/2008)Document23 pagesUnit 6: Value Added Tax (Proclamation 285/2002 Regulation 79/2002 Proclamation 609/2008)Bizu AtnafuNo ratings yet

- ALL ABOUT VALUE ADDED TAX - Mamalateo 2014POWERMAXDocument37 pagesALL ABOUT VALUE ADDED TAX - Mamalateo 2014POWERMAXjohn apostolNo ratings yet

- A. VatDocument5 pagesA. VatKaye L. Dela CruzNo ratings yet

- Tax 2 Notes Finals 4Document36 pagesTax 2 Notes Finals 4Boom ManuelNo ratings yet

- Gimenez Jose Mari CDocument14 pagesGimenez Jose Mari CMari Calica GimenezNo ratings yet

- Business TaxDocument33 pagesBusiness TaxKiro ParafrostNo ratings yet

- Vat System and OptDocument15 pagesVat System and Optlyra21No ratings yet

- VatDocument50 pagesVatnikolaevnavalentinaNo ratings yet

- Comprehensive VAT TAXATION (3!31!14)Document166 pagesComprehensive VAT TAXATION (3!31!14)dereckriveraNo ratings yet

- VATPT For PicpaDocument73 pagesVATPT For PicpaJoy Superales SalaoNo ratings yet

- Business TaxesDocument100 pagesBusiness Taxeslynne tahilNo ratings yet

- VALUE ADDED TAX Goods Properties and ServicesDocument65 pagesVALUE ADDED TAX Goods Properties and ServicesPrincess LimNo ratings yet

- Vat On Sales of Goods or PropertiesDocument10 pagesVat On Sales of Goods or Propertiesgoerginamarquez100% (1)

- VAT Casasola NotesDocument7 pagesVAT Casasola NotesCharm AgripaNo ratings yet

- VAT Powerpoint PDFDocument202 pagesVAT Powerpoint PDFRuchie EtolleNo ratings yet

- Accounting For Indirect TaxesDocument40 pagesAccounting For Indirect TaxesSabaa if100% (1)

- Value Added Tax - VatDocument37 pagesValue Added Tax - VatTimoth MbwiloNo ratings yet

- National Taxation System - RamosDocument10 pagesNational Taxation System - RamosAldrich RamosNo ratings yet

- National Taxation System - RamosDocument10 pagesNational Taxation System - RamosAldrich RamosNo ratings yet

- Notes On VATDocument15 pagesNotes On VATErnest Benz Sabella DavilaNo ratings yet

- Value-Added Tax (VAT) Is A Tax On Consumption Levied On The Sale, Barter, Exchange or LeaseDocument27 pagesValue-Added Tax (VAT) Is A Tax On Consumption Levied On The Sale, Barter, Exchange or LeaseDon CabasiNo ratings yet

- VAT Questions For Professional Stage Knowledge LevelDocument14 pagesVAT Questions For Professional Stage Knowledge LevelFahimaAkterNo ratings yet

- Vat IiDocument19 pagesVat IiPCNo ratings yet

- Business TaxDocument34 pagesBusiness Taxprecy.calusaNo ratings yet

- 8VATDocument70 pages8VATNoelNo ratings yet

- Notes On Vat On Importation Feb 09 2023Document2 pagesNotes On Vat On Importation Feb 09 2023barneyaguilar8732No ratings yet

- VatDocument70 pagesVatPETERWILLE CHUANo ratings yet

- Value Added Tax (Cap 476)Document15 pagesValue Added Tax (Cap 476)Triila manillaNo ratings yet

- Taxn03b Vat IntroDocument20 pagesTaxn03b Vat IntroTrishamae legaspiNo ratings yet

- Export Sale of Goods (Sec. 106 (A) (2) (B) ) : Effectively Zero-Rated SalesDocument13 pagesExport Sale of Goods (Sec. 106 (A) (2) (B) ) : Effectively Zero-Rated SalesTricia Rozl PimentelNo ratings yet

- Percentage Tax in The PhilippinesDocument3 pagesPercentage Tax in The PhilippinesfrazieNo ratings yet

- 1 Basics of Value Added TaxDocument58 pages1 Basics of Value Added TaxHazel Andrea Garduque LopezNo ratings yet

- Business TaxesDocument51 pagesBusiness TaxesLuna CakesNo ratings yet

- Notes in Value Added TaxDocument52 pagesNotes in Value Added Taxedelyn roncalesNo ratings yet

- Tax and Basic Common TaxesDocument13 pagesTax and Basic Common TaxesDENGDENG HUANGNo ratings yet

- Business & Transfer Taxation: Rex B. Banggawan, Cpa, MbaDocument38 pagesBusiness & Transfer Taxation: Rex B. Banggawan, Cpa, Mbajustine reine cornicoNo ratings yet

- Taxation Report2Document22 pagesTaxation Report2Ritchelyn ArbonNo ratings yet

- VAT AnnotatedDocument46 pagesVAT AnnotatedDr SafaNo ratings yet

- Tax UpdatesDocument19 pagesTax UpdatesYeoh MaeNo ratings yet

- VAT Concepts Tax 321Document28 pagesVAT Concepts Tax 321justineNo ratings yet

- Comprehensive VAT TaxationDocument172 pagesComprehensive VAT TaxationIan JameroNo ratings yet

- Business Taxation 2 Lesson 1Document5 pagesBusiness Taxation 2 Lesson 1Darlyn Dalida San PedroNo ratings yet

- Tax - Vat GuidenotesDocument13 pagesTax - Vat GuidenotesNardz AndananNo ratings yet

- Very Awkward Tax: A bite-size guide to VAT for small businessFrom EverandVery Awkward Tax: A bite-size guide to VAT for small businessNo ratings yet

- Affidavit of Contractor License and BondingDocument2 pagesAffidavit of Contractor License and BondingfirsttenorNo ratings yet

- RCM On Residential DwellingDocument5 pagesRCM On Residential Dwellingashok babuNo ratings yet

- FORM47Document2 pagesFORM47TMRCHS TMRCHSNo ratings yet

- TheMomsCo Invoice 1658466994-76Document1 pageTheMomsCo Invoice 1658466994-76Aravind KrishNo ratings yet

- Qi0243 - Amnpn5168p - 2022-23 - Fy 2022 - 2023Document9 pagesQi0243 - Amnpn5168p - 2022-23 - Fy 2022 - 2023Dharma kurraNo ratings yet

- Salary Slip MainDocument1 pageSalary Slip MainVineetBaliyan100% (1)

- Destruction FormDocument2 pagesDestruction FormHanabishi RekkaNo ratings yet

- July 2022Document6 pagesJuly 2022Alexis sanchesNo ratings yet

- 3 - 2551442 - Salary - Illustration - 7 - 19 - 2022 9 - 16 - 28 PMDocument1 page3 - 2551442 - Salary - Illustration - 7 - 19 - 2022 9 - 16 - 28 PMShauryaNo ratings yet

- Accra V CA G.R. No. 96322 December 20, 1991Document2 pagesAccra V CA G.R. No. 96322 December 20, 1991Felicia AllenNo ratings yet

- SummaryDocument2 pagesSummaryASWIN.M.MNo ratings yet

- 200 ReceivedDocument1 page200 ReceivedMANI BHARATHINo ratings yet

- 1081 Supporting BillDocument2 pages1081 Supporting BillAshirwad BanerjeeNo ratings yet

- Air Canada v. CIR - Taxation Law - DebtDocument3 pagesAir Canada v. CIR - Taxation Law - DebtMichael Villalon100% (1)

- Mepco Online Billl PDFDocument1 pageMepco Online Billl PDFArslanNo ratings yet

- IDBI Bank LTD.: Application Print E-Receipt Print Tax InvoiceDocument1 pageIDBI Bank LTD.: Application Print E-Receipt Print Tax InvoicePratik DalwadiNo ratings yet

- #60 CIR vs. TMX SalesDocument2 pages#60 CIR vs. TMX SalesJan Rhoneil SantillanaNo ratings yet

- Presentation On Income TaxDocument9 pagesPresentation On Income TaxUnnati GuptaNo ratings yet

- E-Payslip Advice: Eco Green City SDN BHDDocument1 pageE-Payslip Advice: Eco Green City SDN BHDNur Jannah Marwa HamdanNo ratings yet

- UDA Avenue - Employee Self ServiceDocument1 pageUDA Avenue - Employee Self ServiceAliffNo ratings yet

- Od429286320133715100 1Document1 pageOd429286320133715100 1ANDREW CENANo ratings yet

- InvoiceDocument2 pagesInvoiceRK userNo ratings yet

- Indian Income Tax Return Acknowledgement: Name of Premises/Building/VillageDocument1 pageIndian Income Tax Return Acknowledgement: Name of Premises/Building/Villagesanthosh kumarNo ratings yet

- Sample IRSTax Return TranscriptDocument6 pagesSample IRSTax Return TranscriptnowayNo ratings yet

- BS Pack 3 Flat CAP 20 - BSC20: Mushak: 6.3Document1 pageBS Pack 3 Flat CAP 20 - BSC20: Mushak: 6.3Onek KothaNo ratings yet

- Notes Class XDocument2 pagesNotes Class XmailinspectoryadavNo ratings yet

- Flipkart izTDLqDhhUGmP4d9CTVuPGDocument79 pagesFlipkart izTDLqDhhUGmP4d9CTVuPGAI TOOLS FOR BUSINESSNo ratings yet

- Assignment 1Document4 pagesAssignment 111dylan97No ratings yet