Download as docx, pdf, or txt

You might also like

- PowerTech IndiaDocument4 pagesPowerTech IndiasarthakNo ratings yet

- Industrial Relations Management Exam NotesDocument56 pagesIndustrial Relations Management Exam NotesAbbas T P75% (12)

- What Is The American Approach To HRMDocument18 pagesWhat Is The American Approach To HRMkiranaishaNo ratings yet

- Essay On Economic Problems of Pakistan: Jan. 27th, 2018Document13 pagesEssay On Economic Problems of Pakistan: Jan. 27th, 2018Abid HussainNo ratings yet

- Marcoz 2 CompleteDocument50 pagesMarcoz 2 Completemaaz bangiNo ratings yet

- 11th August, 2021 Express Turbine OpinionDocument6 pages11th August, 2021 Express Turbine Opinionmajid khanNo ratings yet

- Etd 2011 2 7 29Document1 pageEtd 2011 2 7 29143mahimaNo ratings yet

- Essay On Economic Problems of PakistanDocument13 pagesEssay On Economic Problems of PakistanNatasha Inayyat100% (1)

- ITFM Assignment 1Document7 pagesITFM Assignment 1SharjeelNo ratings yet

- Informal Economic Activities and Criminal Acts: M S SiddiquiDocument4 pagesInformal Economic Activities and Criminal Acts: M S SiddiquiMohammad Shahjahan SiddiquiNo ratings yet

- SMEs 2Document4 pagesSMEs 2Engr Ikram UllahNo ratings yet

- Views From The MarketDocument8 pagesViews From The MarketihtashamNo ratings yet

- Micro, Small, and Medium Enterprises (Msmes) : Presenter: Engr - Eufemia A. SantosDocument36 pagesMicro, Small, and Medium Enterprises (Msmes) : Presenter: Engr - Eufemia A. SantosJhi Ghi RawringNo ratings yet

- CHAPTER TWO (Small Bussiness)Document13 pagesCHAPTER TWO (Small Bussiness)Abdurahman Mankovic100% (1)

- Critical Risks and Crimes in Small Business PresentationDocument37 pagesCritical Risks and Crimes in Small Business PresentationTeddyNo ratings yet

- Budget DeficitDocument5 pagesBudget DeficitSaima Afzal Saima AfzalNo ratings yet

- $ 1,700m FDI Received Last Year - Financial Express - Financial Newspaper of BanDocument2 pages$ 1,700m FDI Received Last Year - Financial Express - Financial Newspaper of Banam_lunaticNo ratings yet

- SFAD Assignment 2 (23652)Document3 pagesSFAD Assignment 2 (23652)Muhammad Raffay MaqboolNo ratings yet

- New Microsoft Office Word DocumentDocument6 pagesNew Microsoft Office Word DocumentSandhya NagarNo ratings yet

- The Great Indian Black EconomyDocument4 pagesThe Great Indian Black EconomyKartik RaiNo ratings yet

- Stability With Growth: October 23, 2013Document2 pagesStability With Growth: October 23, 2013NiDa JaVedNo ratings yet

- Corporate Socialism's 2G OrgyDocument3 pagesCorporate Socialism's 2G OrgyVikas BajpaiNo ratings yet

- The Author Is Associate Professor of Economics, Indian Institute of Management Kozhikode. Views Are Personal. Email: Srn@iimk - Ac.inDocument2 pagesThe Author Is Associate Professor of Economics, Indian Institute of Management Kozhikode. Views Are Personal. Email: Srn@iimk - Ac.inKuldeep BarwalNo ratings yet

- Explained: Why Are Medium, Small, Micro Enterprises Worst Hit by Covid-19 Lockdown?Document10 pagesExplained: Why Are Medium, Small, Micro Enterprises Worst Hit by Covid-19 Lockdown?Keerthi LankaNo ratings yet

- Essay Economic CrisiDocument19 pagesEssay Economic CrisiSyed Mushtaq AhmedNo ratings yet

- SME & Consumer BankingDocument39 pagesSME & Consumer Bankingarman_277276271No ratings yet

- GS Paper 3Document73 pagesGS Paper 3Akhil ShastryNo ratings yet

- FInal Project Report IOB 1Document52 pagesFInal Project Report IOB 1Jain NirmalNo ratings yet

- Why MSME?: Why Does India Need The Micro, Small and Medium Enterprises?Document4 pagesWhy MSME?: Why Does India Need The Micro, Small and Medium Enterprises?Don LazarusNo ratings yet

- Why MSME?: Why Does India Need The Micro, Small and Medium Enterprises?Document4 pagesWhy MSME?: Why Does India Need The Micro, Small and Medium Enterprises?Don LazarusNo ratings yet

- Why Does India Need MSMEDocument4 pagesWhy Does India Need MSMEDon LazarusNo ratings yet

- Philippines Micro Small Medium EnterprisesDocument4 pagesPhilippines Micro Small Medium Enterprisesmilesdeasis25No ratings yet

- Pakistan - Enigma of Taxation (Chapter VIII)Document6 pagesPakistan - Enigma of Taxation (Chapter VIII)Zaid NaveedNo ratings yet

- Importance of Smes: Page - 1Document28 pagesImportance of Smes: Page - 1Ariful RussellNo ratings yet

- Black Money in Bangladesh: What, How and RemediesDocument2 pagesBlack Money in Bangladesh: What, How and RemediesArif TusherNo ratings yet

- Role & Significance of Corporate Sector in Pakistan Economy: Development of Pakistan. Yes, The Operating and RegulatoryDocument6 pagesRole & Significance of Corporate Sector in Pakistan Economy: Development of Pakistan. Yes, The Operating and RegulatoryAli AgralNo ratings yet

- Assignment 1 EC3752Document10 pagesAssignment 1 EC3752Qhomeke HlabatheNo ratings yet

- Impact of Tax Policies On Small and Medium-Sized Enterprises (Smes) in Nigeria (A Case Study of Smes in Gwagwalada, Fct-Abuja)Document15 pagesImpact of Tax Policies On Small and Medium-Sized Enterprises (Smes) in Nigeria (A Case Study of Smes in Gwagwalada, Fct-Abuja)Osilama Vincent OmosimuaNo ratings yet

- Why India and Nepal Rank Low in Economic Freedom IndexDocument3 pagesWhy India and Nepal Rank Low in Economic Freedom IndexVinay PandeyNo ratings yet

- Data: Living Off The LandDocument18 pagesData: Living Off The LandRitu WaliaNo ratings yet

- Chapter OneDocument14 pagesChapter OneOsilama Vincent OmosimuaNo ratings yet

- Sociology HM 321: Chaudhry Saad Ullah (2018095)Document3 pagesSociology HM 321: Chaudhry Saad Ullah (2018095)Chaudhrysaad UllahNo ratings yet

- EconomyDocument4 pagesEconomySajid Ali MaharNo ratings yet

- A Community Connect Report On Small Medium Enterprise (Sme) : YEAR-2019 Isha Lohani 2018016014 MBA (B&F)Document41 pagesA Community Connect Report On Small Medium Enterprise (Sme) : YEAR-2019 Isha Lohani 2018016014 MBA (B&F)Isha lohaniNo ratings yet

- Report On Quality Management Practices and Tools Being Used by SME's in Industries in PunjabDocument32 pagesReport On Quality Management Practices and Tools Being Used by SME's in Industries in Punjabmandeep_tcNo ratings yet

- HE Conomic Imes: It Isn't Big, But It's Full of BangDocument1 pageHE Conomic Imes: It Isn't Big, But It's Full of Bangsmdali05No ratings yet

- The Role Played by ZIM-ASSET in Entrepreneurship DevelopmentDocument5 pagesThe Role Played by ZIM-ASSET in Entrepreneurship DevelopmentRewardMaturureNo ratings yet

- Small and Medium Enterprises: Foreign LiteratureDocument16 pagesSmall and Medium Enterprises: Foreign LiteratureMiscaCruzNo ratings yet

- Analyzing An AMPAO EconomyDocument4 pagesAnalyzing An AMPAO Economyjb68No ratings yet

- Ways To Develop A Competitive Environment in The Field of EntrepreneurshipDocument5 pagesWays To Develop A Competitive Environment in The Field of EntrepreneurshipIJRASETPublicationsNo ratings yet

- PEST AnalysisDocument5 pagesPEST AnalysisSultan HaiderNo ratings yet

- Pestle MalaysiaDocument3 pagesPestle MalaysiajunayetNo ratings yet

- GST AssignmentDocument14 pagesGST AssignmentamsupergamingNo ratings yet

- Economics Project: Micro and Small Scale IndustriesDocument13 pagesEconomics Project: Micro and Small Scale IndustriesAnonymous ldN95iANo ratings yet

- KARKUVELRAJDocument9 pagesKARKUVELRAJஸ்ரீ கற்குவேல் அய்யனார் துணைNo ratings yet

- Article PDFDocument7 pagesArticle PDFRabia RajputNo ratings yet

- August 2019Document2 pagesAugust 2019Kiran MNo ratings yet

- Entrepreneurship SystemsDocument4 pagesEntrepreneurship SystemsJosephine SikuteNo ratings yet

- Who Will Pay For Pakistan's State?: Plugging Leaks, Poking HolesDocument3 pagesWho Will Pay For Pakistan's State?: Plugging Leaks, Poking HolesUmer ManzoorNo ratings yet

- Interpreunerial Skills Assignment 1Document10 pagesInterpreunerial Skills Assignment 1Fungai MajuriraNo ratings yet

- International Marketing ComparisonDocument8 pagesInternational Marketing ComparisonNapa ChuenjaiNo ratings yet

- Data VisulizationDocument2 pagesData VisulizationjamilkhannNo ratings yet

- Debt Is CostierDocument3 pagesDebt Is CostierjamilkhannNo ratings yet

- Money and Banking (Money Multiplier Assignment)Document2 pagesMoney and Banking (Money Multiplier Assignment)jamilkhannNo ratings yet

- 95-Harunnurrasyid Et Al. (pp.2060-2078)Document19 pages95-Harunnurrasyid Et Al. (pp.2060-2078)jamilkhannNo ratings yet

- A COMMON Refrain of Donors Is That Pakistan Needs To Raise Its TaxDocument6 pagesA COMMON Refrain of Donors Is That Pakistan Needs To Raise Its TaxjamilkhannNo ratings yet

- Exchange Rate DR MrtazaDocument5 pagesExchange Rate DR MrtazajamilkhannNo ratings yet

- Zzzhao 2000Document33 pagesZzzhao 2000jamilkhannNo ratings yet

- Money and Banking Notes-1Document16 pagesMoney and Banking Notes-1jamilkhannNo ratings yet

- 04 Irfan Ul Haque FinalDocument30 pages04 Irfan Ul Haque FinaljamilkhannNo ratings yet

- TheoilsectorDocument24 pagesTheoilsectorjamilkhannNo ratings yet

- E3sconf Uesf2021 05010Document10 pagesE3sconf Uesf2021 05010jamilkhannNo ratings yet

- Interest Rate NotesDocument11 pagesInterest Rate NotesjamilkhannNo ratings yet

- FF OverheadsDocument8 pagesFF OverheadsjamilkhannNo ratings yet

- A412-Final BanglaDocument7 pagesA412-Final BanglajamilkhannNo ratings yet

- Zheng 2010Document7 pagesZheng 2010jamilkhannNo ratings yet

- J Jtrangeo 2020 102653Document10 pagesJ Jtrangeo 2020 102653jamilkhannNo ratings yet

- 1678-Article Text-6479-1-10-20220218 IndiaDocument18 pages1678-Article Text-6479-1-10-20220218 IndiajamilkhannNo ratings yet

- IJSE 10 2016 0281banglaDocument30 pagesIJSE 10 2016 0281banglajamilkhannNo ratings yet

- Global Concentration FinalDocument28 pagesGlobal Concentration FinaljamilkhannNo ratings yet

- w19898 2014Document13 pagesw19898 2014jamilkhannNo ratings yet

- EDIG-Research-Paper-No.-1 BanglaDocument70 pagesEDIG-Research-Paper-No.-1 BanglajamilkhannNo ratings yet

- Hong 2011Document16 pagesHong 2011jamilkhannNo ratings yet

- Li XiangDocument10 pagesLi XiangjamilkhannNo ratings yet

- 6058 BanglaDocument30 pages6058 BanglajamilkhannNo ratings yet

- CPSD BangladeshDocument172 pagesCPSD BangladeshjamilkhannNo ratings yet

- 9-Concentration-and-Competition-in-the-Non BanglaDocument9 pages9-Concentration-and-Competition-in-the-Non BanglajamilkhannNo ratings yet

- 0003603x21997019 IndiaDocument19 pages0003603x21997019 IndiajamilkhannNo ratings yet

- Gearing Up For The Future of Manufacturing in BangladeshDocument90 pagesGearing Up For The Future of Manufacturing in BangladeshjamilkhannNo ratings yet

- 7up2 BangladeshDocument24 pages7up2 BangladeshjamilkhannNo ratings yet

- 0703 HirtDocument19 pages0703 HirtjamilkhannNo ratings yet

- Three Faces of HRMDocument52 pagesThree Faces of HRMaddiyat100% (2)

- Labor 1 - Digests - 092215Document9 pagesLabor 1 - Digests - 092215Karla BeeNo ratings yet

- Employees' Provident Fund Organization: (Ministry of Labour, Govt. of India)Document1 pageEmployees' Provident Fund Organization: (Ministry of Labour, Govt. of India)Sanjeev KumarNo ratings yet

- Report in Legal & Practice Barriers For Migrant Workers in The Access To Social ProtectionDocument30 pagesReport in Legal & Practice Barriers For Migrant Workers in The Access To Social ProtectionOxfam in Vietnam100% (4)

- Dela Cruz V NLRCDocument9 pagesDela Cruz V NLRCMp CasNo ratings yet

- Bar Examination Questionnaire For Labor LawDocument193 pagesBar Examination Questionnaire For Labor LawCris Estrada RoyalèNo ratings yet

- Ir328 2021Document1 pageIr328 2021api-527215716No ratings yet

- Incentive PlansDocument4 pagesIncentive PlansmaraiaNo ratings yet

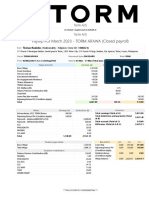

- Payslip For March 2023 - TORM ARAWA (Closed Payroll) : Torm A/S Torm A/SDocument1 pagePayslip For March 2023 - TORM ARAWA (Closed Payroll) : Torm A/S Torm A/SRodelio TomasNo ratings yet

- Labor Cases Security of Tenure and Kinds of EmploymentDocument183 pagesLabor Cases Security of Tenure and Kinds of EmploymentSilvia DamasoNo ratings yet

- Chapter 13 Employee Benefits Noe 13th EdDocument66 pagesChapter 13 Employee Benefits Noe 13th EdbryanbernabeNo ratings yet

- H.Q. Mushroom Farm Inspection ReportsDocument239 pagesH.Q. Mushroom Farm Inspection ReportsTyler OlsenNo ratings yet

- Outsourcing To IndiaDocument14 pagesOutsourcing To Indiaapi-337582893No ratings yet

- Gateway B2+ Test Unit 9 BDocument6 pagesGateway B2+ Test Unit 9 Bana maria csalinas100% (2)

- Chapter 6 Business IssuesDocument11 pagesChapter 6 Business IssuesAndy LaluNo ratings yet

- Labor ExamDocument9 pagesLabor ExamEunice Kalaw VargasNo ratings yet

- Bankard, Inc. Vs NLRC G.R. No. 171664, March 6, 2013 IssueDocument7 pagesBankard, Inc. Vs NLRC G.R. No. 171664, March 6, 2013 IssueJel LyNo ratings yet

- Inside Wiremen Pattern Agreement GuideDocument65 pagesInside Wiremen Pattern Agreement GuideIBEWBrotherhoodNo ratings yet

- Wcms 845714Document19 pagesWcms 845714Hờ HờNo ratings yet

- Importance of Industrial RelationsDocument2 pagesImportance of Industrial RelationsshashimvijayNo ratings yet

- Labor 1 - Digests - 091515Document8 pagesLabor 1 - Digests - 091515Karla BeeNo ratings yet

- Smart Core FinalDocument18 pagesSmart Core FinalREDMOON4No ratings yet

- (Freshmen's Final Report) Human Resource Management - Introducing To BusinessDocument26 pages(Freshmen's Final Report) Human Resource Management - Introducing To BusinessNguyễn Thiên PhúcNo ratings yet

- Child Labor vs. Child StarsDocument25 pagesChild Labor vs. Child StarsZarah Jane Lim100% (6)

- Econ Edx SuggestedAnswers 2019 Paper1Document10 pagesEcon Edx SuggestedAnswers 2019 Paper1Abhishek JoshiNo ratings yet

- Earnings & Rewards 2Document1 pageEarnings & Rewards 2amNo ratings yet

- Itf Imec International Ibf Cba 2019-2022Document15 pagesItf Imec International Ibf Cba 2019-2022vlknNo ratings yet