Q

Q

You might also like

- Income Tax Return Sat-Ita22: Official StampDocument6 pagesIncome Tax Return Sat-Ita22: Official Stamptsere butsere50% (2)

- Chapters 5-6: Use The Following For The Next Two QuestionsDocument9 pagesChapters 5-6: Use The Following For The Next Two QuestionsJane Ruby Jenniefer67% (3)

- Kings Jews Money Massacre and E - 2010kaiser PDFDocument257 pagesKings Jews Money Massacre and E - 2010kaiser PDFMiggy A. L. EsqiNo ratings yet

- ZF 5hp24Document46 pagesZF 5hp24Davidoff Red100% (1)

- Crime Scene QuizDocument24 pagesCrime Scene Quizjjpietra100% (1)

- ACCTG 029 - Final Quiz 1Document1 pageACCTG 029 - Final Quiz 1mcespressoblendNo ratings yet

- Investment Analysis and Portfolio Management 2012Document61 pagesInvestment Analysis and Portfolio Management 2012Nelson Ivan Acosta100% (1)

- Accounts AssignmentDocument17 pagesAccounts AssignmentApoorvNo ratings yet

- Extraordinary General Assembly Dividend Distribution ProposalDocument3 pagesExtraordinary General Assembly Dividend Distribution Proposalrefik_rfkNo ratings yet

- Reviewer Finals Tax 301Document4 pagesReviewer Finals Tax 301Jana RamosNo ratings yet

- Analisis ProfitabilitasDocument6 pagesAnalisis Profitabilitastheresia paulintiaNo ratings yet

- SAA - Annual Certificate of Capital GainsDocument1 pageSAA - Annual Certificate of Capital Gainssaeed abbasiNo ratings yet

- Tax Calculator - Indian Income Tax 2008-09Document7 pagesTax Calculator - Indian Income Tax 2008-09Jayamohan100% (29)

- Intercorporate InvestmentsDocument14 pagesIntercorporate InvestmentsYisbel CarrascoNo ratings yet

- Ipo - Financial - statements-EN 2Document99 pagesIpo - Financial - statements-EN 2SaranzayaGanbaatarNo ratings yet

- Indo PacksDocument1 pageIndo PacksChandan SharmaNo ratings yet

- DLF Limited: Long Way To Bottom: SellDocument17 pagesDLF Limited: Long Way To Bottom: Sellnirav87404No ratings yet

- CBE Dec 22 - ADocument16 pagesCBE Dec 22 - ANguyễn Hồng NgọcNo ratings yet

- BFD Merged Q Tahapopatia +923453086312Document96 pagesBFD Merged Q Tahapopatia +923453086312Abdul BasitNo ratings yet

- Crash Landing On You Company Financial StatementsDocument6 pagesCrash Landing On You Company Financial StatementsEmar KimNo ratings yet

- Intacc2-Quiz ExamDocument5 pagesIntacc2-Quiz ExamCmNo ratings yet

- BT B Sung Chapter 45Document2 pagesBT B Sung Chapter 45Yến Nhi VũNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument7 pages© The Institute of Chartered Accountants of IndiaSarvesh JoshiNo ratings yet

- 1b Final Accounts of Companies - StdtsDocument4 pages1b Final Accounts of Companies - StdtsGodson0% (1)

- Module 4 - Consolidation Subsequent To The Date of Acquisition (Hand - Outs 1)Document3 pagesModule 4 - Consolidation Subsequent To The Date of Acquisition (Hand - Outs 1)ariannealcaraz6No ratings yet

- Rajesh Bora Itr PLBS 2022Document5 pagesRajesh Bora Itr PLBS 2022ABDUL KHALIKNo ratings yet

- Astra Agro Lestari TBK: Soaring Financial Performance in 3Q20Document6 pagesAstra Agro Lestari TBK: Soaring Financial Performance in 3Q20Hamba AllahNo ratings yet

- Cash Flow Statement Cashflows From Operations Cash Receipts From CustomersDocument16 pagesCash Flow Statement Cashflows From Operations Cash Receipts From CustomersAfruza Akter MunniNo ratings yet

- Mixed Income Earner ITR PreparationDocument2 pagesMixed Income Earner ITR PreparationTony Rose Arzaga100% (1)

- 1st Case Study - Financial Statement AnalysisDocument6 pages1st Case Study - Financial Statement AnalysisKimberly SoqueNo ratings yet

- Income Year: 2019-2020, Assessment Year: 2020-2021Document9 pagesIncome Year: 2019-2020, Assessment Year: 2020-2021Istiaque AhmadNo ratings yet

- BusCom Seatwork - 05 15 2021Document4 pagesBusCom Seatwork - 05 15 2021Joshua UmaliNo ratings yet

- Cinemax Limited (CININD) : Disappointing On The Margins FrontDocument6 pagesCinemax Limited (CININD) : Disappointing On The Margins Frontjass200910No ratings yet

- July 2019Document1 pageJuly 2019Geet InamatiNo ratings yet

- 1st-Case-Study - Financial-Statement-Analysis - Group 5Document18 pages1st-Case-Study - Financial-Statement-Analysis - Group 5gellie villarinNo ratings yet

- Ch03 ShowDocument54 pagesCh03 ShowMahmoud AbdullahNo ratings yet

- Partnership - Jaboy - v2.1.1Document19 pagesPartnership - Jaboy - v2.1.1Van Dahuyag100% (1)

- Mid Term FIN 514Document4 pagesMid Term FIN 514Showkatul IslamNo ratings yet

- FAM FormulaDocument19 pagesFAM Formulasarthak mendirattaNo ratings yet

- Prime Finance First MF2012Document1 pagePrime Finance First MF2012Abrar FaisalNo ratings yet

- Fa May June - 2012Document4 pagesFa May June - 2012xodic49847No ratings yet

- Salary Sleep OctoberDocument1 pageSalary Sleep Octobermayank dubeyNo ratings yet

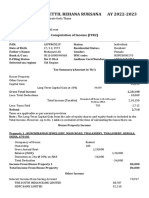

- AY2022-23 KALLA PUTHIYAVEETTIL REHANA RUKSANA-ASFPR0552F-ComputationDocument3 pagesAY2022-23 KALLA PUTHIYAVEETTIL REHANA RUKSANA-ASFPR0552F-ComputationSourabh PunshiNo ratings yet

- Intel Corporation Q2 2010 Earnings Review: ATF CapitalDocument6 pagesIntel Corporation Q2 2010 Earnings Review: ATF CapitalAndre SetiawanNo ratings yet

- Cash Flow Statements Notes and Practical ExercisesDocument9 pagesCash Flow Statements Notes and Practical ExercisesRNo ratings yet

- CBCS 3.3.3 Corporate Valuation and Restructuring 2020Document4 pagesCBCS 3.3.3 Corporate Valuation and Restructuring 2020Bharath MNo ratings yet

- Boi Form S-1 Annual Report On Actual Operations: GuidelinesDocument8 pagesBoi Form S-1 Annual Report On Actual Operations: GuidelinesAdy100% (1)

- Announcement June 2020 - tcm387-605455Document2 pagesAnnouncement June 2020 - tcm387-605455Valamunis DomingoNo ratings yet

- CVMA ResvisionDocument3 pagesCVMA ResvisionApurva RamtekeNo ratings yet

- 2007 Carl & Ruth Shapiro Family Foundation 990 (Includes Madoff Investment)Document42 pages2007 Carl & Ruth Shapiro Family Foundation 990 (Includes Madoff Investment)jpeppard100% (4)

- ChinaNet 2012 Investor PresentationDocument74 pagesChinaNet 2012 Investor PresentationJosé ivan LópezNo ratings yet

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 176386120100121 Assessment Year: 2020-21Document7 pagesItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 176386120100121 Assessment Year: 2020-21Annie SNo ratings yet

- ADVANCED FINANCIAL REPORTING - PDF Nov 2012Document10 pagesADVANCED FINANCIAL REPORTING - PDF Nov 2012Nitin ChoudharyNo ratings yet

- Consolidated FSDocument5 pagesConsolidated FSNicah AcojonNo ratings yet

- 01 - Exercises Session 1 - EmptyDocument4 pages01 - Exercises Session 1 - EmptyAgustín RosalesNo ratings yet

- SS Tutorial 3 Sample ExamDocument4 pagesSS Tutorial 3 Sample ExamFeahRafeah KikiNo ratings yet

- Earnings Deductions MTH - Rate Arrears Total Earned Arrears Total DedDocument1 pageEarnings Deductions MTH - Rate Arrears Total Earned Arrears Total DedShubham GargNo ratings yet

- Perpetual - Financial StatementsDocument4 pagesPerpetual - Financial StatementsJeon Cyrone CuachonNo ratings yet

- Section B:: 1. Are The Following Balance Sheet Items (A) Assets, (L) Liabilities, or (E) Stockholders' Equity?Document11 pagesSection B:: 1. Are The Following Balance Sheet Items (A) Assets, (L) Liabilities, or (E) Stockholders' Equity?18071369 Nguyễn ThànhNo ratings yet

- Income Tax Law for Start-Up Businesses: An Overview of Business Entities and Income Tax LawFrom EverandIncome Tax Law for Start-Up Businesses: An Overview of Business Entities and Income Tax LawRating: 3.5 out of 5 stars3.5/5 (4)

- Renewal Form of Joint Venture.2Document4 pagesRenewal Form of Joint Venture.2Rick Clarence Paglicawan50% (2)

- Bridging An AXI4-Lite Interface To DRP InterfacesDocument9 pagesBridging An AXI4-Lite Interface To DRP InterfacesAmit JainNo ratings yet

- Tupad Annex A Dole Overall ListDocument68 pagesTupad Annex A Dole Overall ListJobeth AndoyNo ratings yet

- 1st CASE SET - COMMREVDocument88 pages1st CASE SET - COMMREVJam PagsuyoinNo ratings yet

- (CD) Dai-Chi Vs Villarama - G.R. No. 112940 - AZapantaDocument1 page(CD) Dai-Chi Vs Villarama - G.R. No. 112940 - AZapantaThe Concerned Lawstudent100% (1)

- Manage Invoice Options - US1 Business UnitDocument2 pagesManage Invoice Options - US1 Business UnitI'm RangaNo ratings yet

- His Defense of The Native's Pride and Dignity As People, Rizal Wrote Three Significant Essays While AbroadDocument42 pagesHis Defense of The Native's Pride and Dignity As People, Rizal Wrote Three Significant Essays While AbroadYang VictoriaNo ratings yet

- Language Programs and Policies in Multilingual Societies - Activity 3Document4 pagesLanguage Programs and Policies in Multilingual Societies - Activity 3Angel Rodriguez75% (4)

- GST Export Invoice: DHL Jaipur Jaipur Singapore SingaporeDocument13 pagesGST Export Invoice: DHL Jaipur Jaipur Singapore SingaporeEdward Roy “Ying” AyingNo ratings yet

- Adobe Scan 03 Dec 2022Document2 pagesAdobe Scan 03 Dec 2022Om DubeyNo ratings yet

- Sps. Lumanas Vs Sps. SablasDocument1 pageSps. Lumanas Vs Sps. SablasMark Catabijan CarriedoNo ratings yet

- Creative Styles Candle Business Final DocsDocument112 pagesCreative Styles Candle Business Final DocsTatine AvelinoNo ratings yet

- Poaching RulingDocument32 pagesPoaching RulingEriq GardnerNo ratings yet

- Model Question BBS 3rd Taxation in NepalDocument6 pagesModel Question BBS 3rd Taxation in NepalAsmita BhujelNo ratings yet

- But The Fruit of The Spirit Is LoveDocument1 pageBut The Fruit of The Spirit Is LovextneNo ratings yet

- Financing DecisionsDocument14 pagesFinancing DecisionsNandita ChouhanNo ratings yet

- Previews 1938599 Pre PDFDocument11 pagesPreviews 1938599 Pre PDFAhmed Mohamed LabibNo ratings yet

- BUS424 Chapter3 7Document25 pagesBUS424 Chapter3 7Anonymous taCBG1AKaNo ratings yet

- LEA121 Introduction To Industrial Security ConceptDocument35 pagesLEA121 Introduction To Industrial Security ConceptC-Maine OdaragNo ratings yet

- US Internal Revenue Service: f941sb AccessibleDocument1 pageUS Internal Revenue Service: f941sb AccessibleIRSNo ratings yet

- 4th Grade Indian in The CupboardDocument16 pages4th Grade Indian in The Cupboardapi-251212745No ratings yet

- Insurance Law in India Question and AnswerDocument15 pagesInsurance Law in India Question and AnswerMaitrayee NandyNo ratings yet

- Internship ReportDocument45 pagesInternship ReportNafiz FahimNo ratings yet

- CCC419 Advance Notice AGM2009Document2 pagesCCC419 Advance Notice AGM2009gallerycourtNo ratings yet

- How Do They CompareDocument2 pagesHow Do They Compareapi-471523403No ratings yet

- Session - Methods of ValuationDocument12 pagesSession - Methods of ValuationAshwik reddyNo ratings yet

- Eapply4Ui - Application For Unemployment Insurance Review PageDocument5 pagesEapply4Ui - Application For Unemployment Insurance Review PagePAKOUSCOUSINMAI50% (2)

Download as pdf or txt

You might also like

- Income Tax Return Sat-Ita22: Official StampDocument6 pagesIncome Tax Return Sat-Ita22: Official Stamptsere butsere50% (2)

- Chapters 5-6: Use The Following For The Next Two QuestionsDocument9 pagesChapters 5-6: Use The Following For The Next Two QuestionsJane Ruby Jenniefer67% (3)

- Kings Jews Money Massacre and E - 2010kaiser PDFDocument257 pagesKings Jews Money Massacre and E - 2010kaiser PDFMiggy A. L. EsqiNo ratings yet

- ZF 5hp24Document46 pagesZF 5hp24Davidoff Red100% (1)

- Crime Scene QuizDocument24 pagesCrime Scene Quizjjpietra100% (1)

- ACCTG 029 - Final Quiz 1Document1 pageACCTG 029 - Final Quiz 1mcespressoblendNo ratings yet

- Investment Analysis and Portfolio Management 2012Document61 pagesInvestment Analysis and Portfolio Management 2012Nelson Ivan Acosta100% (1)

- Accounts AssignmentDocument17 pagesAccounts AssignmentApoorvNo ratings yet

- Extraordinary General Assembly Dividend Distribution ProposalDocument3 pagesExtraordinary General Assembly Dividend Distribution Proposalrefik_rfkNo ratings yet

- Reviewer Finals Tax 301Document4 pagesReviewer Finals Tax 301Jana RamosNo ratings yet

- Analisis ProfitabilitasDocument6 pagesAnalisis Profitabilitastheresia paulintiaNo ratings yet

- SAA - Annual Certificate of Capital GainsDocument1 pageSAA - Annual Certificate of Capital Gainssaeed abbasiNo ratings yet

- Tax Calculator - Indian Income Tax 2008-09Document7 pagesTax Calculator - Indian Income Tax 2008-09Jayamohan100% (29)

- Intercorporate InvestmentsDocument14 pagesIntercorporate InvestmentsYisbel CarrascoNo ratings yet

- Ipo - Financial - statements-EN 2Document99 pagesIpo - Financial - statements-EN 2SaranzayaGanbaatarNo ratings yet

- Indo PacksDocument1 pageIndo PacksChandan SharmaNo ratings yet

- DLF Limited: Long Way To Bottom: SellDocument17 pagesDLF Limited: Long Way To Bottom: Sellnirav87404No ratings yet

- CBE Dec 22 - ADocument16 pagesCBE Dec 22 - ANguyễn Hồng NgọcNo ratings yet

- BFD Merged Q Tahapopatia +923453086312Document96 pagesBFD Merged Q Tahapopatia +923453086312Abdul BasitNo ratings yet

- Crash Landing On You Company Financial StatementsDocument6 pagesCrash Landing On You Company Financial StatementsEmar KimNo ratings yet

- Intacc2-Quiz ExamDocument5 pagesIntacc2-Quiz ExamCmNo ratings yet

- BT B Sung Chapter 45Document2 pagesBT B Sung Chapter 45Yến Nhi VũNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument7 pages© The Institute of Chartered Accountants of IndiaSarvesh JoshiNo ratings yet

- 1b Final Accounts of Companies - StdtsDocument4 pages1b Final Accounts of Companies - StdtsGodson0% (1)

- Module 4 - Consolidation Subsequent To The Date of Acquisition (Hand - Outs 1)Document3 pagesModule 4 - Consolidation Subsequent To The Date of Acquisition (Hand - Outs 1)ariannealcaraz6No ratings yet

- Rajesh Bora Itr PLBS 2022Document5 pagesRajesh Bora Itr PLBS 2022ABDUL KHALIKNo ratings yet

- Astra Agro Lestari TBK: Soaring Financial Performance in 3Q20Document6 pagesAstra Agro Lestari TBK: Soaring Financial Performance in 3Q20Hamba AllahNo ratings yet

- Cash Flow Statement Cashflows From Operations Cash Receipts From CustomersDocument16 pagesCash Flow Statement Cashflows From Operations Cash Receipts From CustomersAfruza Akter MunniNo ratings yet

- Mixed Income Earner ITR PreparationDocument2 pagesMixed Income Earner ITR PreparationTony Rose Arzaga100% (1)

- 1st Case Study - Financial Statement AnalysisDocument6 pages1st Case Study - Financial Statement AnalysisKimberly SoqueNo ratings yet

- Income Year: 2019-2020, Assessment Year: 2020-2021Document9 pagesIncome Year: 2019-2020, Assessment Year: 2020-2021Istiaque AhmadNo ratings yet

- BusCom Seatwork - 05 15 2021Document4 pagesBusCom Seatwork - 05 15 2021Joshua UmaliNo ratings yet

- Cinemax Limited (CININD) : Disappointing On The Margins FrontDocument6 pagesCinemax Limited (CININD) : Disappointing On The Margins Frontjass200910No ratings yet

- July 2019Document1 pageJuly 2019Geet InamatiNo ratings yet

- 1st-Case-Study - Financial-Statement-Analysis - Group 5Document18 pages1st-Case-Study - Financial-Statement-Analysis - Group 5gellie villarinNo ratings yet

- Ch03 ShowDocument54 pagesCh03 ShowMahmoud AbdullahNo ratings yet

- Partnership - Jaboy - v2.1.1Document19 pagesPartnership - Jaboy - v2.1.1Van Dahuyag100% (1)

- Mid Term FIN 514Document4 pagesMid Term FIN 514Showkatul IslamNo ratings yet

- FAM FormulaDocument19 pagesFAM Formulasarthak mendirattaNo ratings yet

- Prime Finance First MF2012Document1 pagePrime Finance First MF2012Abrar FaisalNo ratings yet

- Fa May June - 2012Document4 pagesFa May June - 2012xodic49847No ratings yet

- Salary Sleep OctoberDocument1 pageSalary Sleep Octobermayank dubeyNo ratings yet

- AY2022-23 KALLA PUTHIYAVEETTIL REHANA RUKSANA-ASFPR0552F-ComputationDocument3 pagesAY2022-23 KALLA PUTHIYAVEETTIL REHANA RUKSANA-ASFPR0552F-ComputationSourabh PunshiNo ratings yet

- Intel Corporation Q2 2010 Earnings Review: ATF CapitalDocument6 pagesIntel Corporation Q2 2010 Earnings Review: ATF CapitalAndre SetiawanNo ratings yet

- Cash Flow Statements Notes and Practical ExercisesDocument9 pagesCash Flow Statements Notes and Practical ExercisesRNo ratings yet

- CBCS 3.3.3 Corporate Valuation and Restructuring 2020Document4 pagesCBCS 3.3.3 Corporate Valuation and Restructuring 2020Bharath MNo ratings yet

- Boi Form S-1 Annual Report On Actual Operations: GuidelinesDocument8 pagesBoi Form S-1 Annual Report On Actual Operations: GuidelinesAdy100% (1)

- Announcement June 2020 - tcm387-605455Document2 pagesAnnouncement June 2020 - tcm387-605455Valamunis DomingoNo ratings yet

- CVMA ResvisionDocument3 pagesCVMA ResvisionApurva RamtekeNo ratings yet

- 2007 Carl & Ruth Shapiro Family Foundation 990 (Includes Madoff Investment)Document42 pages2007 Carl & Ruth Shapiro Family Foundation 990 (Includes Madoff Investment)jpeppard100% (4)

- ChinaNet 2012 Investor PresentationDocument74 pagesChinaNet 2012 Investor PresentationJosé ivan LópezNo ratings yet

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 176386120100121 Assessment Year: 2020-21Document7 pagesItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 176386120100121 Assessment Year: 2020-21Annie SNo ratings yet

- ADVANCED FINANCIAL REPORTING - PDF Nov 2012Document10 pagesADVANCED FINANCIAL REPORTING - PDF Nov 2012Nitin ChoudharyNo ratings yet

- Consolidated FSDocument5 pagesConsolidated FSNicah AcojonNo ratings yet

- 01 - Exercises Session 1 - EmptyDocument4 pages01 - Exercises Session 1 - EmptyAgustín RosalesNo ratings yet

- SS Tutorial 3 Sample ExamDocument4 pagesSS Tutorial 3 Sample ExamFeahRafeah KikiNo ratings yet

- Earnings Deductions MTH - Rate Arrears Total Earned Arrears Total DedDocument1 pageEarnings Deductions MTH - Rate Arrears Total Earned Arrears Total DedShubham GargNo ratings yet

- Perpetual - Financial StatementsDocument4 pagesPerpetual - Financial StatementsJeon Cyrone CuachonNo ratings yet

- Section B:: 1. Are The Following Balance Sheet Items (A) Assets, (L) Liabilities, or (E) Stockholders' Equity?Document11 pagesSection B:: 1. Are The Following Balance Sheet Items (A) Assets, (L) Liabilities, or (E) Stockholders' Equity?18071369 Nguyễn ThànhNo ratings yet

- Income Tax Law for Start-Up Businesses: An Overview of Business Entities and Income Tax LawFrom EverandIncome Tax Law for Start-Up Businesses: An Overview of Business Entities and Income Tax LawRating: 3.5 out of 5 stars3.5/5 (4)

- Renewal Form of Joint Venture.2Document4 pagesRenewal Form of Joint Venture.2Rick Clarence Paglicawan50% (2)

- Bridging An AXI4-Lite Interface To DRP InterfacesDocument9 pagesBridging An AXI4-Lite Interface To DRP InterfacesAmit JainNo ratings yet

- Tupad Annex A Dole Overall ListDocument68 pagesTupad Annex A Dole Overall ListJobeth AndoyNo ratings yet

- 1st CASE SET - COMMREVDocument88 pages1st CASE SET - COMMREVJam PagsuyoinNo ratings yet

- (CD) Dai-Chi Vs Villarama - G.R. No. 112940 - AZapantaDocument1 page(CD) Dai-Chi Vs Villarama - G.R. No. 112940 - AZapantaThe Concerned Lawstudent100% (1)

- Manage Invoice Options - US1 Business UnitDocument2 pagesManage Invoice Options - US1 Business UnitI'm RangaNo ratings yet

- His Defense of The Native's Pride and Dignity As People, Rizal Wrote Three Significant Essays While AbroadDocument42 pagesHis Defense of The Native's Pride and Dignity As People, Rizal Wrote Three Significant Essays While AbroadYang VictoriaNo ratings yet

- Language Programs and Policies in Multilingual Societies - Activity 3Document4 pagesLanguage Programs and Policies in Multilingual Societies - Activity 3Angel Rodriguez75% (4)

- GST Export Invoice: DHL Jaipur Jaipur Singapore SingaporeDocument13 pagesGST Export Invoice: DHL Jaipur Jaipur Singapore SingaporeEdward Roy “Ying” AyingNo ratings yet

- Adobe Scan 03 Dec 2022Document2 pagesAdobe Scan 03 Dec 2022Om DubeyNo ratings yet

- Sps. Lumanas Vs Sps. SablasDocument1 pageSps. Lumanas Vs Sps. SablasMark Catabijan CarriedoNo ratings yet

- Creative Styles Candle Business Final DocsDocument112 pagesCreative Styles Candle Business Final DocsTatine AvelinoNo ratings yet

- Poaching RulingDocument32 pagesPoaching RulingEriq GardnerNo ratings yet

- Model Question BBS 3rd Taxation in NepalDocument6 pagesModel Question BBS 3rd Taxation in NepalAsmita BhujelNo ratings yet

- But The Fruit of The Spirit Is LoveDocument1 pageBut The Fruit of The Spirit Is LovextneNo ratings yet

- Financing DecisionsDocument14 pagesFinancing DecisionsNandita ChouhanNo ratings yet

- Previews 1938599 Pre PDFDocument11 pagesPreviews 1938599 Pre PDFAhmed Mohamed LabibNo ratings yet

- BUS424 Chapter3 7Document25 pagesBUS424 Chapter3 7Anonymous taCBG1AKaNo ratings yet

- LEA121 Introduction To Industrial Security ConceptDocument35 pagesLEA121 Introduction To Industrial Security ConceptC-Maine OdaragNo ratings yet

- US Internal Revenue Service: f941sb AccessibleDocument1 pageUS Internal Revenue Service: f941sb AccessibleIRSNo ratings yet

- 4th Grade Indian in The CupboardDocument16 pages4th Grade Indian in The Cupboardapi-251212745No ratings yet

- Insurance Law in India Question and AnswerDocument15 pagesInsurance Law in India Question and AnswerMaitrayee NandyNo ratings yet

- Internship ReportDocument45 pagesInternship ReportNafiz FahimNo ratings yet

- CCC419 Advance Notice AGM2009Document2 pagesCCC419 Advance Notice AGM2009gallerycourtNo ratings yet

- How Do They CompareDocument2 pagesHow Do They Compareapi-471523403No ratings yet

- Session - Methods of ValuationDocument12 pagesSession - Methods of ValuationAshwik reddyNo ratings yet

- Eapply4Ui - Application For Unemployment Insurance Review PageDocument5 pagesEapply4Ui - Application For Unemployment Insurance Review PagePAKOUSCOUSINMAI50% (2)