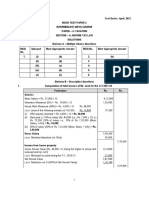

Residential Status, Exempt Income & AMT - Solution

Residential Status, Exempt Income & AMT - Solution

You might also like

- Apple Blossom Cologne Company Common Size Financial Statement Desember 31, 2003Document1 pageApple Blossom Cologne Company Common Size Financial Statement Desember 31, 2003Lintang UtomoNo ratings yet

- Quiz 2.1 - Individual Taxpayers and Quiz 3.1 - INCOME TAX ON CORPORATIONSDocument5 pagesQuiz 2.1 - Individual Taxpayers and Quiz 3.1 - INCOME TAX ON CORPORATIONSHunternotNo ratings yet

- Soal - Home Office Vs Branch (40%) : Total Informasi TambahanDocument2 pagesSoal - Home Office Vs Branch (40%) : Total Informasi Tambahanshani100% (1)

- Worksheet PalaganasDocument38 pagesWorksheet PalaganasMomo HiraiNo ratings yet

- Basics & House Property - PaperDocument5 pagesBasics & House Property - PaperLaavanya JainNo ratings yet

- Basics & House Property - PaperDocument5 pagesBasics & House Property - PaperVenkataRajuNo ratings yet

- MCQ CH 12 - Set-Off and Carry Forward of Losses - Nov 23Document10 pagesMCQ CH 12 - Set-Off and Carry Forward of Losses - Nov 23NikiNo ratings yet

- Setoff and Carry ForwardDocument5 pagesSetoff and Carry ForwardSrinivas T. Raju100% (1)

- Residential Status, Exempt Income & AMT - PaperDocument6 pagesResidential Status, Exempt Income & AMT - PaperBharatbhusan RoutNo ratings yet

- New SyllabusDocument16 pagesNew Syllabusmyash6136No ratings yet

- Adobe Scan 09 Nov 2023Document11 pagesAdobe Scan 09 Nov 2023Sanskruti BarikNo ratings yet

- Nanadanam Key-1Document6 pagesNanadanam Key-1santha kumariNo ratings yet

- Bos 59265Document46 pagesBos 59265oproducts96No ratings yet

- tax qpDocument6 pagestax qpAashish kumarNo ratings yet

- Questio 1Document8 pagesQuestio 1gurukulmaterialNo ratings yet

- TAX PLANNING & COMPLIANCE - ND-2022 - Suggested - AnswersDocument9 pagesTAX PLANNING & COMPLIANCE - ND-2022 - Suggested - AnswersMohammad FaridNo ratings yet

- Cim 8682 Taxation Question Paper (Ahemadabad)Document3 pagesCim 8682 Taxation Question Paper (Ahemadabad)Pomi ShiyaNo ratings yet

- Direct Tax-IDocument21 pagesDirect Tax-Ivivek rajakNo ratings yet

- TAX PLANNING & COMPLIANCE - ND-2022 - QuestionDocument6 pagesTAX PLANNING & COMPLIANCE - ND-2022 - QuestionsajedulNo ratings yet

- Time Allowed: 3 Hours Maximum Mark: 100: Executive ProgrammeDocument18 pagesTime Allowed: 3 Hours Maximum Mark: 100: Executive ProgrammeDevendra AryaNo ratings yet

- Document From Rajan®Document5 pagesDocument From Rajan®Anit LuckyNo ratings yet

- CS Executive OLD SYLLABUS MCQs JUNE 2024 by CA Vivek GabaDocument269 pagesCS Executive OLD SYLLABUS MCQs JUNE 2024 by CA Vivek GabaParitoshNo ratings yet

- Mohit Agarwal QP Tax LawsDocument17 pagesMohit Agarwal QP Tax LawsManisha DasNo ratings yet

- Income Tax Divyastra CH 2 Scope of Total Income RDocument15 pagesIncome Tax Divyastra CH 2 Scope of Total Income Rjhansiaj06No ratings yet

- Sem - IV Taxation - I Sample Paper-1Document5 pagesSem - IV Taxation - I Sample Paper-1yadavkari497No ratings yet

- Sa 3 DT NovDocument9 pagesSa 3 DT NovRishabh GargNo ratings yet

- Part - I (MCQS) All Mcqs Are Compulsory: Permission Is Punishable OffenceDocument12 pagesPart - I (MCQS) All Mcqs Are Compulsory: Permission Is Punishable OffenceShashwat SharmaNo ratings yet

- Taxation-II (Honors) 2022-23Document5 pagesTaxation-II (Honors) 2022-23futureisgreat0592No ratings yet

- GKJ Taxation Final (Sums)Document7 pagesGKJ Taxation Final (Sums)ankandas3498No ratings yet

- IncomeTax-IIDocument7 pagesIncomeTax-IIAditya .cNo ratings yet

- Paper 16Document5 pagesPaper 16VijayaNo ratings yet

- Series I - QuestionsDocument11 pagesSeries I - QuestionsAlok MishraNo ratings yet

- 23 Tax JuneDocument16 pages23 Tax JunemistryankusNo ratings yet

- Tax 2 AnsDocument12 pagesTax 2 AnsCollege CollegeNo ratings yet

- @ProCA - Inter DT Residential Status Question Bank Nov2022Document53 pages@ProCA - Inter DT Residential Status Question Bank Nov2022hero36407No ratings yet

- 75780bos61308 p4Document30 pages75780bos61308 p4Sathvika SathuNo ratings yet

- Tax AnswersDocument168 pagesTax AnswersukqrnnnjhfwsxqoykuNo ratings yet

- Question Test Paper 2 - NOV 2023Document2 pagesQuestion Test Paper 2 - NOV 2023ABCXYZNo ratings yet

- Income Tax Divyastra CH 12 Set Off Carry Forward of Losses RDocument17 pagesIncome Tax Divyastra CH 12 Set Off Carry Forward of Losses R655priya THAPANo ratings yet

- CT 1 A SolutionDocument2 pagesCT 1 A SolutionAnsary LabibNo ratings yet

- Income Tax 1 - 20223Document3 pagesIncome Tax 1 - 20223nimalpes21No ratings yet

- MTP 12 17 Questions 1696512917Document11 pagesMTP 12 17 Questions 1696512917harshallahotNo ratings yet

- PEOBLEMS2Document3 pagesPEOBLEMS2Awesome AngelNo ratings yet

- Final DT 30 QPDocument6 pagesFinal DT 30 QPshivam chaturvediNo ratings yet

- RA - M16UCM12 - B.Com. - 24.03.2021 - FNDocument4 pagesRA - M16UCM12 - B.Com. - 24.03.2021 - FNkavinilavan14072004No ratings yet

- Paper7 Set1 NDocument7 pagesPaper7 Set1 NSanchit ShrivastavaNo ratings yet

- It 1Document18 pagesIt 1naheensyeda20No ratings yet

- MTP 2 TaxDocument10 pagesMTP 2 TaxPrathmesh JambhulkarNo ratings yet

- IncomeTax-2Document6 pagesIncomeTax-2Aditya .cNo ratings yet

- Clubbing, Set-Off & Deduction U - C VI-A - SolutionDocument6 pagesClubbing, Set-Off & Deduction U - C VI-A - SolutionBharatbhusan RoutNo ratings yet

- (I) (B) (Ii) (D) (Iii) (D) (Iv) (C) (V) (A) (Vi) (C) (Vii) (A) (Viii) (D) (Ix) (C) (X) (C)Document8 pages(I) (B) (Ii) (D) (Iii) (D) (Iv) (C) (V) (A) (Vi) (C) (Vii) (A) (Viii) (D) (Ix) (C) (X) (C)santosh palNo ratings yet

- UntitledDocument11 pagesUntitleddeepika devsaniNo ratings yet

- Aditya Sharma - II Mid Term PaperDocument4 pagesAditya Sharma - II Mid Term PaperAditya SharmaNo ratings yet

- Total Income (RTP+PYP)Document27 pagesTotal Income (RTP+PYP)zaydumaarNo ratings yet

- DT BB TestDocument5 pagesDT BB TestMayank GoyalNo ratings yet

- CA FINAL Class Test Paper MAY/NOV-22 Exams Topics: Basics, Capital Gain & IFOSDocument8 pagesCA FINAL Class Test Paper MAY/NOV-22 Exams Topics: Basics, Capital Gain & IFOSMayank GoyalNo ratings yet

- Icai Module QuestionsDocument26 pagesIcai Module QuestionsrachitNo ratings yet

- Capital Gain and IFOS - SolutionDocument6 pagesCapital Gain and IFOS - SolutionVenkataRajuNo ratings yet

- DT 2 New Question PaperDocument11 pagesDT 2 New Question Paperneha manglaniNo ratings yet

- MBA183F3: RamaiahDocument5 pagesMBA183F3: Ramaiahvijay shetNo ratings yet

- Aggregation of Income and Set-Off of LossDocument25 pagesAggregation of Income and Set-Off of Lossmamnanitushar13No ratings yet

- Question TAX GMDocument7 pagesQuestion TAX GMAshutosh Kr. Sahuwala 7bNo ratings yet

- Container Port Performance Index 2022: A Comparable Assessment of Performance Based on Vessel Time in PortFrom EverandContainer Port Performance Index 2022: A Comparable Assessment of Performance Based on Vessel Time in PortNo ratings yet

- Cambridge IGCSE™: Economics 0455/21 May/June 2022Document23 pagesCambridge IGCSE™: Economics 0455/21 May/June 2022Tanvita KoushikNo ratings yet

- Topic 1Document26 pagesTopic 1Mohd NajitNo ratings yet

- Hayat ProposalDocument22 pagesHayat Proposalsebehadinahmed1992No ratings yet

- Lecture2020 SSP 9757Document30 pagesLecture2020 SSP 9757Sebastian ZhangNo ratings yet

- Release NotesDocument13 pagesRelease NotesJbNo ratings yet

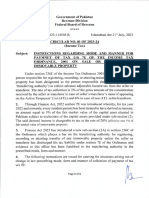

- 2023721217646921CircularNo 1of2023-2024Document4 pages2023721217646921CircularNo 1of2023-2024krebs38No ratings yet

- Chapter 07 9E Problem SolutionsDocument23 pagesChapter 07 9E Problem Solutionsjames50% (2)

- Tax II Chapter IDocument49 pagesTax II Chapter IsejalNo ratings yet

- Subject Financial Accounting and Reporting Chapter/Unit Chapter 2/part 1 Lesson Title Accounting and Business Lesson ObjectivesDocument16 pagesSubject Financial Accounting and Reporting Chapter/Unit Chapter 2/part 1 Lesson Title Accounting and Business Lesson ObjectivesAzuma JunichiNo ratings yet

- MAERSK - Annual Report - 2022Document4 pagesMAERSK - Annual Report - 2022ccs sandeepNo ratings yet

- Effects of Population Growth On Economic Development in Developing CountriesDocument6 pagesEffects of Population Growth On Economic Development in Developing CountriesJohn Jayson OstagaNo ratings yet

- What Is The Solvency RatioDocument2 pagesWhat Is The Solvency RatioDarlene SarcinoNo ratings yet

- Overview of Financial Statement Analysis Multiple Choice QuestionsDocument41 pagesOverview of Financial Statement Analysis Multiple Choice QuestionsNhã ThiiNo ratings yet

- Student: Choo Wei Sheng Instructor: Riayati Ahmad Date: 2/3/21 Course: Eppd1013 Microeconomics 1 Set 2 - Book: Perloff: Microeconomics, 8e, Global Edition Time: 7:47 PMDocument2 pagesStudent: Choo Wei Sheng Instructor: Riayati Ahmad Date: 2/3/21 Course: Eppd1013 Microeconomics 1 Set 2 - Book: Perloff: Microeconomics, 8e, Global Edition Time: 7:47 PMChoo Wei shengNo ratings yet

- Netflix PESTEL AnalysisDocument10 pagesNetflix PESTEL AnalysisSteve RogersNo ratings yet

- S3 Ch2 More About Percentages QDocument12 pagesS3 Ch2 More About Percentages QF2D 10 FUNG SZE HANGNo ratings yet

- IT Module No. 7: Introduction To Regular Income TaxDocument13 pagesIT Module No. 7: Introduction To Regular Income TaxjakeNo ratings yet

- BDMN Annual Report 2020 ENGDocument768 pagesBDMN Annual Report 2020 ENGastri meliaNo ratings yet

- Five Major AccountsDocument16 pagesFive Major AccountsNimrod CabreraNo ratings yet

- Appeals Court-Reply To Response To Irs Brief To Appeals Court-4!14!12Document38 pagesAppeals Court-Reply To Response To Irs Brief To Appeals Court-4!14!12Ask MeforitNo ratings yet

- Final Book WorkDocument229 pagesFinal Book WorkAron Yohannes Gimisso100% (1)

- Note Receivable Problem 6 1 To 6 5Document11 pagesNote Receivable Problem 6 1 To 6 5Jewel Mercano PabalinasNo ratings yet

- Incomet-Problems - WITH SOLUTIONS-UPDATED VERSIONDocument20 pagesIncomet-Problems - WITH SOLUTIONS-UPDATED VERSIONJulius Atilano GallegoNo ratings yet

- IAR Auditing ConclusionDocument23 pagesIAR Auditing Conclusionmarlout.sarita100% (1)

- Business Math Qtr1 Week 6Document2 pagesBusiness Math Qtr1 Week 6Joan BalmesNo ratings yet

- Problems and Prospects of Marketing in Developing Economies - The Nigerian Experience PDFDocument10 pagesProblems and Prospects of Marketing in Developing Economies - The Nigerian Experience PDFaliNo ratings yet

Download as pdf or txt

You might also like

- Apple Blossom Cologne Company Common Size Financial Statement Desember 31, 2003Document1 pageApple Blossom Cologne Company Common Size Financial Statement Desember 31, 2003Lintang UtomoNo ratings yet

- Quiz 2.1 - Individual Taxpayers and Quiz 3.1 - INCOME TAX ON CORPORATIONSDocument5 pagesQuiz 2.1 - Individual Taxpayers and Quiz 3.1 - INCOME TAX ON CORPORATIONSHunternotNo ratings yet

- Soal - Home Office Vs Branch (40%) : Total Informasi TambahanDocument2 pagesSoal - Home Office Vs Branch (40%) : Total Informasi Tambahanshani100% (1)

- Worksheet PalaganasDocument38 pagesWorksheet PalaganasMomo HiraiNo ratings yet

- Basics & House Property - PaperDocument5 pagesBasics & House Property - PaperLaavanya JainNo ratings yet

- Basics & House Property - PaperDocument5 pagesBasics & House Property - PaperVenkataRajuNo ratings yet

- MCQ CH 12 - Set-Off and Carry Forward of Losses - Nov 23Document10 pagesMCQ CH 12 - Set-Off and Carry Forward of Losses - Nov 23NikiNo ratings yet

- Setoff and Carry ForwardDocument5 pagesSetoff and Carry ForwardSrinivas T. Raju100% (1)

- Residential Status, Exempt Income & AMT - PaperDocument6 pagesResidential Status, Exempt Income & AMT - PaperBharatbhusan RoutNo ratings yet

- New SyllabusDocument16 pagesNew Syllabusmyash6136No ratings yet

- Adobe Scan 09 Nov 2023Document11 pagesAdobe Scan 09 Nov 2023Sanskruti BarikNo ratings yet

- Nanadanam Key-1Document6 pagesNanadanam Key-1santha kumariNo ratings yet

- Bos 59265Document46 pagesBos 59265oproducts96No ratings yet

- tax qpDocument6 pagestax qpAashish kumarNo ratings yet

- Questio 1Document8 pagesQuestio 1gurukulmaterialNo ratings yet

- TAX PLANNING & COMPLIANCE - ND-2022 - Suggested - AnswersDocument9 pagesTAX PLANNING & COMPLIANCE - ND-2022 - Suggested - AnswersMohammad FaridNo ratings yet

- Cim 8682 Taxation Question Paper (Ahemadabad)Document3 pagesCim 8682 Taxation Question Paper (Ahemadabad)Pomi ShiyaNo ratings yet

- Direct Tax-IDocument21 pagesDirect Tax-Ivivek rajakNo ratings yet

- TAX PLANNING & COMPLIANCE - ND-2022 - QuestionDocument6 pagesTAX PLANNING & COMPLIANCE - ND-2022 - QuestionsajedulNo ratings yet

- Time Allowed: 3 Hours Maximum Mark: 100: Executive ProgrammeDocument18 pagesTime Allowed: 3 Hours Maximum Mark: 100: Executive ProgrammeDevendra AryaNo ratings yet

- Document From Rajan®Document5 pagesDocument From Rajan®Anit LuckyNo ratings yet

- CS Executive OLD SYLLABUS MCQs JUNE 2024 by CA Vivek GabaDocument269 pagesCS Executive OLD SYLLABUS MCQs JUNE 2024 by CA Vivek GabaParitoshNo ratings yet

- Mohit Agarwal QP Tax LawsDocument17 pagesMohit Agarwal QP Tax LawsManisha DasNo ratings yet

- Income Tax Divyastra CH 2 Scope of Total Income RDocument15 pagesIncome Tax Divyastra CH 2 Scope of Total Income Rjhansiaj06No ratings yet

- Sem - IV Taxation - I Sample Paper-1Document5 pagesSem - IV Taxation - I Sample Paper-1yadavkari497No ratings yet

- Sa 3 DT NovDocument9 pagesSa 3 DT NovRishabh GargNo ratings yet

- Part - I (MCQS) All Mcqs Are Compulsory: Permission Is Punishable OffenceDocument12 pagesPart - I (MCQS) All Mcqs Are Compulsory: Permission Is Punishable OffenceShashwat SharmaNo ratings yet

- Taxation-II (Honors) 2022-23Document5 pagesTaxation-II (Honors) 2022-23futureisgreat0592No ratings yet

- GKJ Taxation Final (Sums)Document7 pagesGKJ Taxation Final (Sums)ankandas3498No ratings yet

- IncomeTax-IIDocument7 pagesIncomeTax-IIAditya .cNo ratings yet

- Paper 16Document5 pagesPaper 16VijayaNo ratings yet

- Series I - QuestionsDocument11 pagesSeries I - QuestionsAlok MishraNo ratings yet

- 23 Tax JuneDocument16 pages23 Tax JunemistryankusNo ratings yet

- Tax 2 AnsDocument12 pagesTax 2 AnsCollege CollegeNo ratings yet

- @ProCA - Inter DT Residential Status Question Bank Nov2022Document53 pages@ProCA - Inter DT Residential Status Question Bank Nov2022hero36407No ratings yet

- 75780bos61308 p4Document30 pages75780bos61308 p4Sathvika SathuNo ratings yet

- Tax AnswersDocument168 pagesTax AnswersukqrnnnjhfwsxqoykuNo ratings yet

- Question Test Paper 2 - NOV 2023Document2 pagesQuestion Test Paper 2 - NOV 2023ABCXYZNo ratings yet

- Income Tax Divyastra CH 12 Set Off Carry Forward of Losses RDocument17 pagesIncome Tax Divyastra CH 12 Set Off Carry Forward of Losses R655priya THAPANo ratings yet

- CT 1 A SolutionDocument2 pagesCT 1 A SolutionAnsary LabibNo ratings yet

- Income Tax 1 - 20223Document3 pagesIncome Tax 1 - 20223nimalpes21No ratings yet

- MTP 12 17 Questions 1696512917Document11 pagesMTP 12 17 Questions 1696512917harshallahotNo ratings yet

- PEOBLEMS2Document3 pagesPEOBLEMS2Awesome AngelNo ratings yet

- Final DT 30 QPDocument6 pagesFinal DT 30 QPshivam chaturvediNo ratings yet

- RA - M16UCM12 - B.Com. - 24.03.2021 - FNDocument4 pagesRA - M16UCM12 - B.Com. - 24.03.2021 - FNkavinilavan14072004No ratings yet

- Paper7 Set1 NDocument7 pagesPaper7 Set1 NSanchit ShrivastavaNo ratings yet

- It 1Document18 pagesIt 1naheensyeda20No ratings yet

- MTP 2 TaxDocument10 pagesMTP 2 TaxPrathmesh JambhulkarNo ratings yet

- IncomeTax-2Document6 pagesIncomeTax-2Aditya .cNo ratings yet

- Clubbing, Set-Off & Deduction U - C VI-A - SolutionDocument6 pagesClubbing, Set-Off & Deduction U - C VI-A - SolutionBharatbhusan RoutNo ratings yet

- (I) (B) (Ii) (D) (Iii) (D) (Iv) (C) (V) (A) (Vi) (C) (Vii) (A) (Viii) (D) (Ix) (C) (X) (C)Document8 pages(I) (B) (Ii) (D) (Iii) (D) (Iv) (C) (V) (A) (Vi) (C) (Vii) (A) (Viii) (D) (Ix) (C) (X) (C)santosh palNo ratings yet

- UntitledDocument11 pagesUntitleddeepika devsaniNo ratings yet

- Aditya Sharma - II Mid Term PaperDocument4 pagesAditya Sharma - II Mid Term PaperAditya SharmaNo ratings yet

- Total Income (RTP+PYP)Document27 pagesTotal Income (RTP+PYP)zaydumaarNo ratings yet

- DT BB TestDocument5 pagesDT BB TestMayank GoyalNo ratings yet

- CA FINAL Class Test Paper MAY/NOV-22 Exams Topics: Basics, Capital Gain & IFOSDocument8 pagesCA FINAL Class Test Paper MAY/NOV-22 Exams Topics: Basics, Capital Gain & IFOSMayank GoyalNo ratings yet

- Icai Module QuestionsDocument26 pagesIcai Module QuestionsrachitNo ratings yet

- Capital Gain and IFOS - SolutionDocument6 pagesCapital Gain and IFOS - SolutionVenkataRajuNo ratings yet

- DT 2 New Question PaperDocument11 pagesDT 2 New Question Paperneha manglaniNo ratings yet

- MBA183F3: RamaiahDocument5 pagesMBA183F3: Ramaiahvijay shetNo ratings yet

- Aggregation of Income and Set-Off of LossDocument25 pagesAggregation of Income and Set-Off of Lossmamnanitushar13No ratings yet

- Question TAX GMDocument7 pagesQuestion TAX GMAshutosh Kr. Sahuwala 7bNo ratings yet

- Container Port Performance Index 2022: A Comparable Assessment of Performance Based on Vessel Time in PortFrom EverandContainer Port Performance Index 2022: A Comparable Assessment of Performance Based on Vessel Time in PortNo ratings yet

- Cambridge IGCSE™: Economics 0455/21 May/June 2022Document23 pagesCambridge IGCSE™: Economics 0455/21 May/June 2022Tanvita KoushikNo ratings yet

- Topic 1Document26 pagesTopic 1Mohd NajitNo ratings yet

- Hayat ProposalDocument22 pagesHayat Proposalsebehadinahmed1992No ratings yet

- Lecture2020 SSP 9757Document30 pagesLecture2020 SSP 9757Sebastian ZhangNo ratings yet

- Release NotesDocument13 pagesRelease NotesJbNo ratings yet

- 2023721217646921CircularNo 1of2023-2024Document4 pages2023721217646921CircularNo 1of2023-2024krebs38No ratings yet

- Chapter 07 9E Problem SolutionsDocument23 pagesChapter 07 9E Problem Solutionsjames50% (2)

- Tax II Chapter IDocument49 pagesTax II Chapter IsejalNo ratings yet

- Subject Financial Accounting and Reporting Chapter/Unit Chapter 2/part 1 Lesson Title Accounting and Business Lesson ObjectivesDocument16 pagesSubject Financial Accounting and Reporting Chapter/Unit Chapter 2/part 1 Lesson Title Accounting and Business Lesson ObjectivesAzuma JunichiNo ratings yet

- MAERSK - Annual Report - 2022Document4 pagesMAERSK - Annual Report - 2022ccs sandeepNo ratings yet

- Effects of Population Growth On Economic Development in Developing CountriesDocument6 pagesEffects of Population Growth On Economic Development in Developing CountriesJohn Jayson OstagaNo ratings yet

- What Is The Solvency RatioDocument2 pagesWhat Is The Solvency RatioDarlene SarcinoNo ratings yet

- Overview of Financial Statement Analysis Multiple Choice QuestionsDocument41 pagesOverview of Financial Statement Analysis Multiple Choice QuestionsNhã ThiiNo ratings yet

- Student: Choo Wei Sheng Instructor: Riayati Ahmad Date: 2/3/21 Course: Eppd1013 Microeconomics 1 Set 2 - Book: Perloff: Microeconomics, 8e, Global Edition Time: 7:47 PMDocument2 pagesStudent: Choo Wei Sheng Instructor: Riayati Ahmad Date: 2/3/21 Course: Eppd1013 Microeconomics 1 Set 2 - Book: Perloff: Microeconomics, 8e, Global Edition Time: 7:47 PMChoo Wei shengNo ratings yet

- Netflix PESTEL AnalysisDocument10 pagesNetflix PESTEL AnalysisSteve RogersNo ratings yet

- S3 Ch2 More About Percentages QDocument12 pagesS3 Ch2 More About Percentages QF2D 10 FUNG SZE HANGNo ratings yet

- IT Module No. 7: Introduction To Regular Income TaxDocument13 pagesIT Module No. 7: Introduction To Regular Income TaxjakeNo ratings yet

- BDMN Annual Report 2020 ENGDocument768 pagesBDMN Annual Report 2020 ENGastri meliaNo ratings yet

- Five Major AccountsDocument16 pagesFive Major AccountsNimrod CabreraNo ratings yet

- Appeals Court-Reply To Response To Irs Brief To Appeals Court-4!14!12Document38 pagesAppeals Court-Reply To Response To Irs Brief To Appeals Court-4!14!12Ask MeforitNo ratings yet

- Final Book WorkDocument229 pagesFinal Book WorkAron Yohannes Gimisso100% (1)

- Note Receivable Problem 6 1 To 6 5Document11 pagesNote Receivable Problem 6 1 To 6 5Jewel Mercano PabalinasNo ratings yet

- Incomet-Problems - WITH SOLUTIONS-UPDATED VERSIONDocument20 pagesIncomet-Problems - WITH SOLUTIONS-UPDATED VERSIONJulius Atilano GallegoNo ratings yet

- IAR Auditing ConclusionDocument23 pagesIAR Auditing Conclusionmarlout.sarita100% (1)

- Business Math Qtr1 Week 6Document2 pagesBusiness Math Qtr1 Week 6Joan BalmesNo ratings yet

- Problems and Prospects of Marketing in Developing Economies - The Nigerian Experience PDFDocument10 pagesProblems and Prospects of Marketing in Developing Economies - The Nigerian Experience PDFaliNo ratings yet