Final Intership Report Sample

Final Intership Report Sample

You might also like

- Ross GuideDocument107 pagesRoss Guidegarimag2k100% (1)

- Agreement For The Purchase of Gold BarDocument29 pagesAgreement For The Purchase of Gold BarHolicks Enterprises Limited100% (1)

- Format of Internship Report Cover Page - pdf-1Document6 pagesFormat of Internship Report Cover Page - pdf-1Kirubel Ayele100% (1)

- NITIE Casebook PDFDocument162 pagesNITIE Casebook PDFSai Tapaswi ChNo ratings yet

- Accounting and Financial Management Module GuideDocument274 pagesAccounting and Financial Management Module GuideFrancis Mtambo100% (1)

- Final Intership Report SampleDocument32 pagesFinal Intership Report SampleMaham QureshiNo ratings yet

- WrittingDocument149 pagesWrittingNicky ElizabethNo ratings yet

- Research Thesis - Pubudu KarunaratneDocument117 pagesResearch Thesis - Pubudu KarunaratnechathuriNo ratings yet

- 04 - How To Write A Report WellingtonDocument41 pages04 - How To Write A Report WellingtonColin RobertsNo ratings yet

- How To Write A Business ReportDocument37 pagesHow To Write A Business Reportfofsid21No ratings yet

- 2023 SHBM - Internship Report GuideDocument16 pages2023 SHBM - Internship Report GuideYasmine BahtaouiNo ratings yet

- 1 - Summer Training HandbookDocument49 pages1 - Summer Training HandbookPardeep SharmaNo ratings yet

- VBS Report Writing Guide 2017Document41 pagesVBS Report Writing Guide 2017Stella NguyenNo ratings yet

- Writing A Business ReportDocument41 pagesWriting A Business ReportNancy SrivastavaNo ratings yet

- BRM Report - Group 13Document19 pagesBRM Report - Group 13jassi4584No ratings yet

- resume 模版Document26 pagesresume 模版jiayi.yanNo ratings yet

- Summer Training Handbook 2015 (Pg.29 To 45)Document49 pagesSummer Training Handbook 2015 (Pg.29 To 45)Gurpreet Singh CheemaNo ratings yet

- Technical WritingsDocument7 pagesTechnical WritingsdevimstaraNo ratings yet

- WSBG Report Writing Guide 2017Document42 pagesWSBG Report Writing Guide 2017Cafe MusicNo ratings yet

- AIT Internship Report GuidelinesDocument12 pagesAIT Internship Report GuidelinesMIchaelNo ratings yet

- Prime Bank & Lanka Bangla FinanceDocument108 pagesPrime Bank & Lanka Bangla FinanceSaddam Hossain EmonNo ratings yet

- MBA Assignments Guide: HandbookDocument60 pagesMBA Assignments Guide: Handbooksuad550No ratings yet

- General Guidelines For Industrial Attachment FinalDocument6 pagesGeneral Guidelines For Industrial Attachment FinalBilly NdawanaNo ratings yet

- Tutorial Letter 101/3/2019: Strategic SourcingDocument34 pagesTutorial Letter 101/3/2019: Strategic SourcingloshniNo ratings yet

- Academic Report Writing TemplateDocument6 pagesAcademic Report Writing Templatesarcozy922No ratings yet

- Corporate AccountingDocument29 pagesCorporate AccountingSajeevNo ratings yet

- MC New ReportDocument51 pagesMC New Reportk07011994No ratings yet

- Business Report HandbookDocument9 pagesBusiness Report Handbookbill padersanNo ratings yet

- Fomat Advisory Report Versie 21 November 2017Document17 pagesFomat Advisory Report Versie 21 November 2017MacMillanDAN100% (1)

- COMM 2 NotesDocument7 pagesCOMM 2 NotesGeorges ChouchaniNo ratings yet

- Internship Report FormatDocument5 pagesInternship Report FormatAhsan NaeemNo ratings yet

- Report & Proposal Writing: Self Learning GuideDocument40 pagesReport & Proposal Writing: Self Learning GuideJodin Alido MahinayNo ratings yet

- MCIOBDocument10 pagesMCIOBvsimeunovic1No ratings yet

- Eco Internship Report WritingDocument5 pagesEco Internship Report WritingMunazza WardakNo ratings yet

- Table of ContentsDocument11 pagesTable of ContentsUsman ManiNo ratings yet

- Internship Report FinalDocument35 pagesInternship Report FinalNeshNo ratings yet

- Table of ContentsDocument10 pagesTable of Contentsnaveed_mirzamanNo ratings yet

- Job Application GuideDocument29 pagesJob Application GuideSeb TegNo ratings yet

- SWOT Report Jannat CTBDDocument52 pagesSWOT Report Jannat CTBDkawshik007No ratings yet

- Business Model For After School ProgramDocument53 pagesBusiness Model For After School ProgrampatNo ratings yet

- Guidelines For Internship Program of BBA Students: Department of Business AdministrationDocument7 pagesGuidelines For Internship Program of BBA Students: Department of Business AdministrationTanzia RahmanNo ratings yet

- FRA ProjectDocument63 pagesFRA ProjectRisa SahaNo ratings yet

- Ridoy Saha Internship ReportDocument58 pagesRidoy Saha Internship ReportSelim KhanNo ratings yet

- Commonsense Leadership in The WorkplaceDocument25 pagesCommonsense Leadership in The WorkplaceKhương NguyễnNo ratings yet

- Updated by Sherry SkinnerDocument48 pagesUpdated by Sherry SkinnerPrashant PrajapatiNo ratings yet

- Outline Internship 2023Document6 pagesOutline Internship 2023Yasmin RabbaniNo ratings yet

- Summer Internship Guidelines - 2019Document34 pagesSummer Internship Guidelines - 2019sambit kumar100% (1)

- SHBM - Internship Report Guide - VFDocument15 pagesSHBM - Internship Report Guide - VFchoukri mohamedNo ratings yet

- New (Carlton) - Business Professional Ethics - UDE 19 Case Review 30% CO3 Continuous AssessmentDocument4 pagesNew (Carlton) - Business Professional Ethics - UDE 19 Case Review 30% CO3 Continuous AssessmentAliciaNo ratings yet

- Engineering Resume GuideDocument50 pagesEngineering Resume Guidebrody lubkeyNo ratings yet

- An Internship Report On Kandel S. & Associates: by Puja Bogati Roll No: 19032387 P.U Registration No: 2018-2-03-2135Document25 pagesAn Internship Report On Kandel S. & Associates: by Puja Bogati Roll No: 19032387 P.U Registration No: 2018-2-03-2135Santosh ThapaliyaNo ratings yet

- World University of Bangladesh (Repaired)Document44 pagesWorld University of Bangladesh (Repaired)MD. MAZHARUL HAQUENo ratings yet

- College of Busines and EconomicsDocument51 pagesCollege of Busines and Economicshabtamu tadesseNo ratings yet

- Are You the New Manager?: Techniques, Guidelines, and Strategies for a Successful First YearFrom EverandAre You the New Manager?: Techniques, Guidelines, and Strategies for a Successful First YearNo ratings yet

- Resume and Letter Transformation Made Easy: The Made Easy Series Collection, #2From EverandResume and Letter Transformation Made Easy: The Made Easy Series Collection, #2No ratings yet

- Successfully Managing Your Engineering Career: No Nonsence Manuals, #5From EverandSuccessfully Managing Your Engineering Career: No Nonsence Manuals, #5No ratings yet

- Sustainable Entrepreneurship: A Guide to Strategic Business Management for for Small Entrepreneurs in the Wine Industry and beyondFrom EverandSustainable Entrepreneurship: A Guide to Strategic Business Management for for Small Entrepreneurs in the Wine Industry and beyondNo ratings yet

- STMT Ent BookDocument2 pagesSTMT Ent BookNasir GhaniNo ratings yet

- SCM Assignment 3 - Syed Ijlal HaiderDocument5 pagesSCM Assignment 3 - Syed Ijlal HaiderSyed Ijlal HaiderNo ratings yet

- Automotive in 2023Document9 pagesAutomotive in 2023RaúlNo ratings yet

- GrowwDocument2 pagesGrowwKate pNo ratings yet

- Agrarian ReformDocument43 pagesAgrarian ReformRalph MarronNo ratings yet

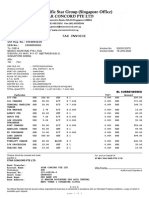

- Invoice SII22012979Document2 pagesInvoice SII22012979Summersky9333No ratings yet

- Gen2 Mod (EV)Document14 pagesGen2 Mod (EV)thanggimme.phanNo ratings yet

- External ObsolescenceDocument9 pagesExternal ObsolescencemilsbozNo ratings yet

- HRA DeclarationFormDocument1 pageHRA DeclarationFormmsmr14No ratings yet

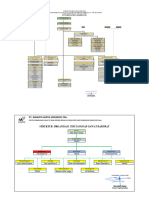

- Struktur Oganisasi Proyek, Dan TGDDocument9 pagesStruktur Oganisasi Proyek, Dan TGDAbdee Prinzen WidyaNo ratings yet

- Appendix 10.1 Certificate of Inward Remittance (Cir) of Foreign Exchange No. Ccyy-Nnnnnn-BbbbbbbbbbbDocument4 pagesAppendix 10.1 Certificate of Inward Remittance (Cir) of Foreign Exchange No. Ccyy-Nnnnnn-BbbbbbbbbbbRalph AcobaNo ratings yet

- CFAS - Lec. 9 PAS 21 and 23Document22 pagesCFAS - Lec. 9 PAS 21 and 23latte aeriNo ratings yet

- Final Exam - ACCT 5001P - Fall 2022Document23 pagesFinal Exam - ACCT 5001P - Fall 2022shuvorajbhattaNo ratings yet

- Hindenburg Vs AdaniDocument51 pagesHindenburg Vs AdaniShataddru NilNo ratings yet

- Floor Plan of Auditiorium (SCALE:-1:200) Balcony Floor Plan of Auditiorium (SCALE: - 1:200)Document1 pageFloor Plan of Auditiorium (SCALE:-1:200) Balcony Floor Plan of Auditiorium (SCALE: - 1:200)Rajeshwari YeoleNo ratings yet

- Output Maximisation:: Objectives of The FirmDocument8 pagesOutput Maximisation:: Objectives of The Firmshikah sidarNo ratings yet

- 10 Economic Principles (Diotay, Richard JR)Document2 pages10 Economic Principles (Diotay, Richard JR)RICHARD JR DIOTAYNo ratings yet

- Competitiveness in Global Trade: The Case of The Automobile IndustryDocument25 pagesCompetitiveness in Global Trade: The Case of The Automobile IndustryKhánh Nguyễn NgHNo ratings yet

- Type of Industry PDFDocument28 pagesType of Industry PDFSuzannePadernaNo ratings yet

- NITdw 21Document15 pagesNITdw 21Kartik JoshiNo ratings yet

- Entrepreneurial Finance 4th Edition Leach Test BankDocument12 pagesEntrepreneurial Finance 4th Edition Leach Test BankDanielWilliamskpsrq100% (16)

- 4 FHPL 07072021 ReimbursemetDocument3 pages4 FHPL 07072021 ReimbursemetHOD (MVGR Civil)No ratings yet

- Trends and Challenges in Indonesian Infrastructure InvestmentDocument13 pagesTrends and Challenges in Indonesian Infrastructure InvestmentArkan DiptyoNo ratings yet

- An Update On Cost and Scale-Up Factors - Donald S. Remer (2008)Document14 pagesAn Update On Cost and Scale-Up Factors - Donald S. Remer (2008)Bryan Vidal TorricoNo ratings yet

- Fucking Report in TechnoshitDocument38 pagesFucking Report in TechnoshitJason DelumenNo ratings yet

- Draft Assignment 2Document15 pagesDraft Assignment 2Ho Thi Lan Vy (FGW DN)No ratings yet

- Where Data Is No Rocket Science !: Be No Date HS Code Product Description QuantityDocument22 pagesWhere Data Is No Rocket Science !: Be No Date HS Code Product Description QuantityPermesh GoelNo ratings yet

- Athenian Tetradrachm Coinage of The FirsDocument26 pagesAthenian Tetradrachm Coinage of The Firsolaf75No ratings yet

- Investment Calculator - 1Document2 pagesInvestment Calculator - 1Ionut FratilaNo ratings yet

Download as docx, pdf, or txt

You might also like

- Ross GuideDocument107 pagesRoss Guidegarimag2k100% (1)

- Agreement For The Purchase of Gold BarDocument29 pagesAgreement For The Purchase of Gold BarHolicks Enterprises Limited100% (1)

- Format of Internship Report Cover Page - pdf-1Document6 pagesFormat of Internship Report Cover Page - pdf-1Kirubel Ayele100% (1)

- NITIE Casebook PDFDocument162 pagesNITIE Casebook PDFSai Tapaswi ChNo ratings yet

- Accounting and Financial Management Module GuideDocument274 pagesAccounting and Financial Management Module GuideFrancis Mtambo100% (1)

- Final Intership Report SampleDocument32 pagesFinal Intership Report SampleMaham QureshiNo ratings yet

- WrittingDocument149 pagesWrittingNicky ElizabethNo ratings yet

- Research Thesis - Pubudu KarunaratneDocument117 pagesResearch Thesis - Pubudu KarunaratnechathuriNo ratings yet

- 04 - How To Write A Report WellingtonDocument41 pages04 - How To Write A Report WellingtonColin RobertsNo ratings yet

- How To Write A Business ReportDocument37 pagesHow To Write A Business Reportfofsid21No ratings yet

- 2023 SHBM - Internship Report GuideDocument16 pages2023 SHBM - Internship Report GuideYasmine BahtaouiNo ratings yet

- 1 - Summer Training HandbookDocument49 pages1 - Summer Training HandbookPardeep SharmaNo ratings yet

- VBS Report Writing Guide 2017Document41 pagesVBS Report Writing Guide 2017Stella NguyenNo ratings yet

- Writing A Business ReportDocument41 pagesWriting A Business ReportNancy SrivastavaNo ratings yet

- BRM Report - Group 13Document19 pagesBRM Report - Group 13jassi4584No ratings yet

- resume 模版Document26 pagesresume 模版jiayi.yanNo ratings yet

- Summer Training Handbook 2015 (Pg.29 To 45)Document49 pagesSummer Training Handbook 2015 (Pg.29 To 45)Gurpreet Singh CheemaNo ratings yet

- Technical WritingsDocument7 pagesTechnical WritingsdevimstaraNo ratings yet

- WSBG Report Writing Guide 2017Document42 pagesWSBG Report Writing Guide 2017Cafe MusicNo ratings yet

- AIT Internship Report GuidelinesDocument12 pagesAIT Internship Report GuidelinesMIchaelNo ratings yet

- Prime Bank & Lanka Bangla FinanceDocument108 pagesPrime Bank & Lanka Bangla FinanceSaddam Hossain EmonNo ratings yet

- MBA Assignments Guide: HandbookDocument60 pagesMBA Assignments Guide: Handbooksuad550No ratings yet

- General Guidelines For Industrial Attachment FinalDocument6 pagesGeneral Guidelines For Industrial Attachment FinalBilly NdawanaNo ratings yet

- Tutorial Letter 101/3/2019: Strategic SourcingDocument34 pagesTutorial Letter 101/3/2019: Strategic SourcingloshniNo ratings yet

- Academic Report Writing TemplateDocument6 pagesAcademic Report Writing Templatesarcozy922No ratings yet

- Corporate AccountingDocument29 pagesCorporate AccountingSajeevNo ratings yet

- MC New ReportDocument51 pagesMC New Reportk07011994No ratings yet

- Business Report HandbookDocument9 pagesBusiness Report Handbookbill padersanNo ratings yet

- Fomat Advisory Report Versie 21 November 2017Document17 pagesFomat Advisory Report Versie 21 November 2017MacMillanDAN100% (1)

- COMM 2 NotesDocument7 pagesCOMM 2 NotesGeorges ChouchaniNo ratings yet

- Internship Report FormatDocument5 pagesInternship Report FormatAhsan NaeemNo ratings yet

- Report & Proposal Writing: Self Learning GuideDocument40 pagesReport & Proposal Writing: Self Learning GuideJodin Alido MahinayNo ratings yet

- MCIOBDocument10 pagesMCIOBvsimeunovic1No ratings yet

- Eco Internship Report WritingDocument5 pagesEco Internship Report WritingMunazza WardakNo ratings yet

- Table of ContentsDocument11 pagesTable of ContentsUsman ManiNo ratings yet

- Internship Report FinalDocument35 pagesInternship Report FinalNeshNo ratings yet

- Table of ContentsDocument10 pagesTable of Contentsnaveed_mirzamanNo ratings yet

- Job Application GuideDocument29 pagesJob Application GuideSeb TegNo ratings yet

- SWOT Report Jannat CTBDDocument52 pagesSWOT Report Jannat CTBDkawshik007No ratings yet

- Business Model For After School ProgramDocument53 pagesBusiness Model For After School ProgrampatNo ratings yet

- Guidelines For Internship Program of BBA Students: Department of Business AdministrationDocument7 pagesGuidelines For Internship Program of BBA Students: Department of Business AdministrationTanzia RahmanNo ratings yet

- FRA ProjectDocument63 pagesFRA ProjectRisa SahaNo ratings yet

- Ridoy Saha Internship ReportDocument58 pagesRidoy Saha Internship ReportSelim KhanNo ratings yet

- Commonsense Leadership in The WorkplaceDocument25 pagesCommonsense Leadership in The WorkplaceKhương NguyễnNo ratings yet

- Updated by Sherry SkinnerDocument48 pagesUpdated by Sherry SkinnerPrashant PrajapatiNo ratings yet

- Outline Internship 2023Document6 pagesOutline Internship 2023Yasmin RabbaniNo ratings yet

- Summer Internship Guidelines - 2019Document34 pagesSummer Internship Guidelines - 2019sambit kumar100% (1)

- SHBM - Internship Report Guide - VFDocument15 pagesSHBM - Internship Report Guide - VFchoukri mohamedNo ratings yet

- New (Carlton) - Business Professional Ethics - UDE 19 Case Review 30% CO3 Continuous AssessmentDocument4 pagesNew (Carlton) - Business Professional Ethics - UDE 19 Case Review 30% CO3 Continuous AssessmentAliciaNo ratings yet

- Engineering Resume GuideDocument50 pagesEngineering Resume Guidebrody lubkeyNo ratings yet

- An Internship Report On Kandel S. & Associates: by Puja Bogati Roll No: 19032387 P.U Registration No: 2018-2-03-2135Document25 pagesAn Internship Report On Kandel S. & Associates: by Puja Bogati Roll No: 19032387 P.U Registration No: 2018-2-03-2135Santosh ThapaliyaNo ratings yet

- World University of Bangladesh (Repaired)Document44 pagesWorld University of Bangladesh (Repaired)MD. MAZHARUL HAQUENo ratings yet

- College of Busines and EconomicsDocument51 pagesCollege of Busines and Economicshabtamu tadesseNo ratings yet

- Are You the New Manager?: Techniques, Guidelines, and Strategies for a Successful First YearFrom EverandAre You the New Manager?: Techniques, Guidelines, and Strategies for a Successful First YearNo ratings yet

- Resume and Letter Transformation Made Easy: The Made Easy Series Collection, #2From EverandResume and Letter Transformation Made Easy: The Made Easy Series Collection, #2No ratings yet

- Successfully Managing Your Engineering Career: No Nonsence Manuals, #5From EverandSuccessfully Managing Your Engineering Career: No Nonsence Manuals, #5No ratings yet

- Sustainable Entrepreneurship: A Guide to Strategic Business Management for for Small Entrepreneurs in the Wine Industry and beyondFrom EverandSustainable Entrepreneurship: A Guide to Strategic Business Management for for Small Entrepreneurs in the Wine Industry and beyondNo ratings yet

- STMT Ent BookDocument2 pagesSTMT Ent BookNasir GhaniNo ratings yet

- SCM Assignment 3 - Syed Ijlal HaiderDocument5 pagesSCM Assignment 3 - Syed Ijlal HaiderSyed Ijlal HaiderNo ratings yet

- Automotive in 2023Document9 pagesAutomotive in 2023RaúlNo ratings yet

- GrowwDocument2 pagesGrowwKate pNo ratings yet

- Agrarian ReformDocument43 pagesAgrarian ReformRalph MarronNo ratings yet

- Invoice SII22012979Document2 pagesInvoice SII22012979Summersky9333No ratings yet

- Gen2 Mod (EV)Document14 pagesGen2 Mod (EV)thanggimme.phanNo ratings yet

- External ObsolescenceDocument9 pagesExternal ObsolescencemilsbozNo ratings yet

- HRA DeclarationFormDocument1 pageHRA DeclarationFormmsmr14No ratings yet

- Struktur Oganisasi Proyek, Dan TGDDocument9 pagesStruktur Oganisasi Proyek, Dan TGDAbdee Prinzen WidyaNo ratings yet

- Appendix 10.1 Certificate of Inward Remittance (Cir) of Foreign Exchange No. Ccyy-Nnnnnn-BbbbbbbbbbbDocument4 pagesAppendix 10.1 Certificate of Inward Remittance (Cir) of Foreign Exchange No. Ccyy-Nnnnnn-BbbbbbbbbbbRalph AcobaNo ratings yet

- CFAS - Lec. 9 PAS 21 and 23Document22 pagesCFAS - Lec. 9 PAS 21 and 23latte aeriNo ratings yet

- Final Exam - ACCT 5001P - Fall 2022Document23 pagesFinal Exam - ACCT 5001P - Fall 2022shuvorajbhattaNo ratings yet

- Hindenburg Vs AdaniDocument51 pagesHindenburg Vs AdaniShataddru NilNo ratings yet

- Floor Plan of Auditiorium (SCALE:-1:200) Balcony Floor Plan of Auditiorium (SCALE: - 1:200)Document1 pageFloor Plan of Auditiorium (SCALE:-1:200) Balcony Floor Plan of Auditiorium (SCALE: - 1:200)Rajeshwari YeoleNo ratings yet

- Output Maximisation:: Objectives of The FirmDocument8 pagesOutput Maximisation:: Objectives of The Firmshikah sidarNo ratings yet

- 10 Economic Principles (Diotay, Richard JR)Document2 pages10 Economic Principles (Diotay, Richard JR)RICHARD JR DIOTAYNo ratings yet

- Competitiveness in Global Trade: The Case of The Automobile IndustryDocument25 pagesCompetitiveness in Global Trade: The Case of The Automobile IndustryKhánh Nguyễn NgHNo ratings yet

- Type of Industry PDFDocument28 pagesType of Industry PDFSuzannePadernaNo ratings yet

- NITdw 21Document15 pagesNITdw 21Kartik JoshiNo ratings yet

- Entrepreneurial Finance 4th Edition Leach Test BankDocument12 pagesEntrepreneurial Finance 4th Edition Leach Test BankDanielWilliamskpsrq100% (16)

- 4 FHPL 07072021 ReimbursemetDocument3 pages4 FHPL 07072021 ReimbursemetHOD (MVGR Civil)No ratings yet

- Trends and Challenges in Indonesian Infrastructure InvestmentDocument13 pagesTrends and Challenges in Indonesian Infrastructure InvestmentArkan DiptyoNo ratings yet

- An Update On Cost and Scale-Up Factors - Donald S. Remer (2008)Document14 pagesAn Update On Cost and Scale-Up Factors - Donald S. Remer (2008)Bryan Vidal TorricoNo ratings yet

- Fucking Report in TechnoshitDocument38 pagesFucking Report in TechnoshitJason DelumenNo ratings yet

- Draft Assignment 2Document15 pagesDraft Assignment 2Ho Thi Lan Vy (FGW DN)No ratings yet

- Where Data Is No Rocket Science !: Be No Date HS Code Product Description QuantityDocument22 pagesWhere Data Is No Rocket Science !: Be No Date HS Code Product Description QuantityPermesh GoelNo ratings yet

- Athenian Tetradrachm Coinage of The FirsDocument26 pagesAthenian Tetradrachm Coinage of The Firsolaf75No ratings yet

- Investment Calculator - 1Document2 pagesInvestment Calculator - 1Ionut FratilaNo ratings yet