Download as pdf or txt

You might also like

- SIE QuickSheet, 2E PDF (Secured)Document4 pagesSIE QuickSheet, 2E PDF (Secured)Henry Jose Codallo Siso90% (10)

- Original PDF Financial Statement Analysis and Security Valuation 5th Edition PDFDocument41 pagesOriginal PDF Financial Statement Analysis and Security Valuation 5th Edition PDFgordon.hatley642100% (38)

- Inbm 110 - Accounts Study Sheet: Chapter 1 & 2Document5 pagesInbm 110 - Accounts Study Sheet: Chapter 1 & 2Laura TaiNo ratings yet

- CASHFLOW The Board Game Personal Financial Statement PDFDocument1 pageCASHFLOW The Board Game Personal Financial Statement PDFfpenalozal100% (1)

- Uber, Operational StrategyDocument22 pagesUber, Operational StrategyNoelraj Kalkuri100% (3)

- CASHFLOW The Board Game Personal Financial StatementDocument1 pageCASHFLOW The Board Game Personal Financial StatementGejehNo ratings yet

- CASHFLOW The Board Game Personal Financial StatementDocument1 pageCASHFLOW The Board Game Personal Financial StatementKakz KarthikNo ratings yet

- CASHFLOW The Board Game Personal Financial Statement PDFDocument1 pageCASHFLOW The Board Game Personal Financial Statement PDFCarl SoriaNo ratings yet

- Session 1 Practice 3Document4 pagesSession 1 Practice 3yimin liuNo ratings yet

- Accounting Workbook Section 4 AnswersDocument49 pagesAccounting Workbook Section 4 AnswersAhmed Zeeshan100% (25)

- Non Current Asset Questions For ACCADocument11 pagesNon Current Asset Questions For ACCAAiril RazaliNo ratings yet

- Accounting Cheat SheetDocument2 pagesAccounting Cheat Sheetrio_harcanNo ratings yet

- CASHFLOW The Board Game Personal Financial StatementDocument1 pageCASHFLOW The Board Game Personal Financial StatementKNNo ratings yet

- Independent Work: by The Discipline AccountingDocument7 pagesIndependent Work: by The Discipline AccountingРадько Вікторія ВікторівнаNo ratings yet

- 2Document4 pages2Janea Lorraine TanNo ratings yet

- Fin - BIP-ACC-211-Week-8-9Document10 pagesFin - BIP-ACC-211-Week-8-9gelNo ratings yet

- Adobe Scan 13-Oct-2022Document1 pageAdobe Scan 13-Oct-2022Abhishek SinghNo ratings yet

- Grant: SubsidyDocument10 pagesGrant: SubsidyFatima MianoorNo ratings yet

- Class Notes - INDAS 102Document15 pagesClass Notes - INDAS 102Shivaji hariNo ratings yet

- 14.1 11.1 Debit & Credit PDFDocument24 pages14.1 11.1 Debit & Credit PDFJoi JoiNo ratings yet

- Notes - AS 19Document16 pagesNotes - AS 19pandyji8453No ratings yet

- Ammu Inflation & Unemployment English NotesDocument5 pagesAmmu Inflation & Unemployment English NotesAnimated TamashaNo ratings yet

- FAR1-All IASs SummaryDocument14 pagesFAR1-All IASs SummaryanasfinkileNo ratings yet

- IntacDocument1 pageIntac2022301307No ratings yet

- Module 2 ACCTDocument17 pagesModule 2 ACCTFathimath NoohaNo ratings yet

- FAA - Unit 2 - 21 (Journal & TB)Document15 pagesFAA - Unit 2 - 21 (Journal & TB)Pranjal ChopraNo ratings yet

- FAA - Unit 2 - 21 (Journal & TB)Document15 pagesFAA - Unit 2 - 21 (Journal & TB)Pranjal ChopraNo ratings yet

- Kuliah - Week 1 (Pengantar Analbi)Document1 pageKuliah - Week 1 (Pengantar Analbi)Falisha RivienaNo ratings yet

- ATM Session 2Document14 pagesATM Session 2Saksham AgrawalNo ratings yet

- CASHFLOW JuegoDocument1 pageCASHFLOW JuegoRebeca Valverde DelgadoNo ratings yet

- CASHFLOW The Board Game Personal Financial StatementDocument1 pageCASHFLOW The Board Game Personal Financial StatementCarl SoriaNo ratings yet

- CASHFLOW The Board Game Personal Financial Statement PDFDocument1 pageCASHFLOW The Board Game Personal Financial Statement PDFfpenalozalNo ratings yet

- 13 Short Term FinancingDocument3 pages13 Short Term FinancingIrene LimpinNo ratings yet

- CASHFLOW The Board Game Personal Financial Statement PDFDocument1 pageCASHFLOW The Board Game Personal Financial Statement PDFArifNo ratings yet

- CASHFLOW The Board Game Personal Financial StatementDocument1 pageCASHFLOW The Board Game Personal Financial StatementUtiyyalaNo ratings yet

- Zyanne BaringDocument7 pagesZyanne BaringKeziah ChristineNo ratings yet

- Rastriya Banijya Bank Ltd. (Document9 pagesRastriya Banijya Bank Ltd. (Pradip HamalNo ratings yet

- AccountingDocument67 pagesAccountinggunanNo ratings yet

- Name of The Public Trust - Balance Sheet As On 31St March, 2004Document2 pagesName of The Public Trust - Balance Sheet As On 31St March, 2004NIKHIL KASATNo ratings yet

- Governmental Handout IIDocument10 pagesGovernmental Handout IIHoang HaNo ratings yet

- 03 Accounts Receivable Management - LectureDocument28 pages03 Accounts Receivable Management - LectureChelsea ManuelNo ratings yet

- Personal Financial StatementDocument3 pagesPersonal Financial StatementIra Hilado BelicenaNo ratings yet

- Accounting Standards PDFDocument43 pagesAccounting Standards PDFSai Krishna TejaNo ratings yet

- Unit #11Document10 pagesUnit #11Asif FarooqNo ratings yet

- Friday of Tax Chapter 1Document11 pagesFriday of Tax Chapter 1Vanessa vnssNo ratings yet

- Chart of AccountsDocument3 pagesChart of AccountsmiirahsinNo ratings yet

- UC Regent Varner - Financiacl DisclosureDocument7 pagesUC Regent Varner - Financiacl DisclosureSpotUsNo ratings yet

- Lcci LV I TextDocument65 pagesLcci LV I TextPyin Nyar AungNo ratings yet

- Financial Statement AnalysisDocument13 pagesFinancial Statement AnalysisValerie RogatskinaNo ratings yet

- Financial Accounting & Decision Making NotesDocument27 pagesFinancial Accounting & Decision Making Notessuhanibhatt90No ratings yet

- Balance SheetDocument1 pageBalance Sheetcaitlyn keisha almeidaNo ratings yet

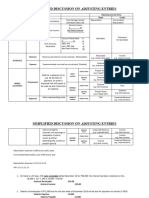

- Kinds of Adjusting Entries 1Document2 pagesKinds of Adjusting Entries 1Marc Justine Gamiao GoNo ratings yet

- Partnership LiquidationDocument2 pagesPartnership LiquidationNikki RunesNo ratings yet

- Financial Accounting Chapter 1 - 3: By: Stefanie (125180444) Angela (125180447) Yuvina (125180464)Document20 pagesFinancial Accounting Chapter 1 - 3: By: Stefanie (125180444) Angela (125180447) Yuvina (125180464)Elafan storeNo ratings yet

- IC Real Estate Balance Sheet Template 10522Document2 pagesIC Real Estate Balance Sheet Template 10522Deepanshu ChauhanNo ratings yet

- Balance SheetDocument2 pagesBalance SheetRae FernandezNo ratings yet

- Balance SheetDocument3 pagesBalance SheetIrfan GulNo ratings yet

- Chapter 2 MindmapDocument1 pageChapter 2 MindmapKiều Trần Nguyễn DiễmNo ratings yet

- Financial Ratio Analysis FormulaDocument1 pageFinancial Ratio Analysis FormulaChrista LenzNo ratings yet

- Thursday of Tax Chapter 1Document10 pagesThursday of Tax Chapter 1yi ShiNo ratings yet

- BE Message Format 2.3 06.11.2017Document1 pageBE Message Format 2.3 06.11.2017raviNo ratings yet

- Content/Elements of Business Plan: Mary Mildred P. de Jesus SHS TeacherDocument28 pagesContent/Elements of Business Plan: Mary Mildred P. de Jesus SHS TeacherMary De JesusNo ratings yet

- Personal Financial Statement: Small BusinessDocument3 pagesPersonal Financial Statement: Small Businessmdyafi8084No ratings yet

- Capital Budgeting SummaryDocument8 pagesCapital Budgeting Summaryparvez ansariNo ratings yet

- SBP Consolidated-ReportDocument265 pagesSBP Consolidated-ReportBilal ZaidiNo ratings yet

- The Future Starts Today, Not Tomorrow.: Chapter 8: Overview of Working Capital ManagementDocument29 pagesThe Future Starts Today, Not Tomorrow.: Chapter 8: Overview of Working Capital ManagementIni IchiiiNo ratings yet

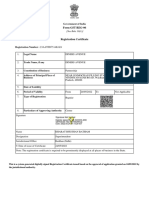

- Certificate of Business Name Registration: MGTV Sari Sari StoreDocument2 pagesCertificate of Business Name Registration: MGTV Sari Sari StoreMaria MalangNo ratings yet

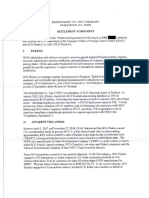

- Scgplastics SettlementDocument5 pagesScgplastics SettlementTCIJNo ratings yet

- MCQ Cost of Capital GoodsDocument16 pagesMCQ Cost of Capital Goodsbetang0998No ratings yet

- Strategic Plan: December 2019Document27 pagesStrategic Plan: December 2019Vedhica AgarwalNo ratings yet

- COP12 KYC Policy and Procedures Template 1Document2 pagesCOP12 KYC Policy and Procedures Template 1Pooh HuiNo ratings yet

- Chapter 2 Banking OperationsDocument24 pagesChapter 2 Banking OperationsVishvesh ShahNo ratings yet

- 2018 Topic TestDocument7 pages2018 Topic Testjuniorpula8052No ratings yet

- B01032 - Chapter 07 - The Stock Market, The Theory of Rational Expectations and The Efficient Market HypothesisDocument14 pagesB01032 - Chapter 07 - The Stock Market, The Theory of Rational Expectations and The Efficient Market HypothesisDương Thị Kim HiềnNo ratings yet

- Chapter 8-Problem 6Document6 pagesChapter 8-Problem 6kakaoNo ratings yet

- ImrozDocument3 pagesImrozShivendra PandeyNo ratings yet

- R D V Stock Preferred of ValueDocument42 pagesR D V Stock Preferred of ValueJesper N. Qvist100% (4)

- Electricity Bill PDFDocument1 pageElectricity Bill PDFSantanu KumarNo ratings yet

- Bank Alfalah 1Document123 pagesBank Alfalah 1muhammadtaimoorkhan100% (2)

- September 29, 2017 Strathmore TimesDocument28 pagesSeptember 29, 2017 Strathmore TimesStrathmore TimesNo ratings yet

- Sakthi Fianance Project ReportDocument61 pagesSakthi Fianance Project ReportraveenkumarNo ratings yet

- State of The Municipality Address by Mayor Rolando B. Distura 2013, Dumangas, IloiloDocument102 pagesState of The Municipality Address by Mayor Rolando B. Distura 2013, Dumangas, IloiloLakanPHNo ratings yet

- Draft Agreement Vessel - BIMCO 2005 (Part I)Document2 pagesDraft Agreement Vessel - BIMCO 2005 (Part I)Domi Rompar100% (1)

- Chapter 11 Valuation Using MultiplesDocument22 pagesChapter 11 Valuation Using MultiplesUmar MansuriNo ratings yet

- TicketDocument4 pagesTicketMohamed EbrahimNo ratings yet

- Practical Auditing ch01Document15 pagesPractical Auditing ch01Rhea Royce CabuhatNo ratings yet

- Maybank Credit Cardmembers Are Advised To Completely Understand The Product Term & Conditions Before EnrolmentDocument6 pagesMaybank Credit Cardmembers Are Advised To Completely Understand The Product Term & Conditions Before EnrolmentMr DummyNo ratings yet

- Answers To Mcqs TutorialDocument30 pagesAnswers To Mcqs TutorialDuy TrịnhNo ratings yet